Published on April 10, 2026

by Val Cipriani

The new tax year is upon us, meaning many investors will have a lump sum to add to their stocks-and-shares Isas – at what is a scary time to go about allocating capital. Recent levels of uncertainty would give pause even to the most veteran of investors.

As a general principle, the right thing to do is stay the course. Review your strategy and portfolio, and as long as they are still right for your goals and time horizon, it’s business as usual. If you are feeling worried about investing a lump sum in one go, you can always drip-feed the money into the market over a few weeks or months.

Still, you might be pondering which types of equity funds are likely to fare best over the next few months if the Middle East ceasefire doesn’t hold, or if volatility returns in another form.

Investors’ Chronicle

A quality resurgence

The theory goes that the most defensive equity sectors comprise companies selling essential goods and services. Broadly, this applies to the likes of consumer staples, healthcare and utilities.

In reality it’s a little more complicated. For example, within healthcare, there are also a number of growth-focused biotech companies that are actually quite racy, while the big pharmaceutical companies make up the more defensive side of the sector. But the idea is that defensive companies’ earnings should prove resilient even during an economic downturn.

Looking for global equity funds with above-average exposure to these sectors will usually lead you to managers deploying a ‘quality’ strategy. The most famous example, Terry Smith’s Fundsmith Equity (GB00B41YBW71), currently has more than half of its portfolio between healthcare and consumer staples, with Unilever (ULVR) as one of its top holdings.

Quality as a style does have a defensive tilt, at least in theory, given it looks for resilient, cash-generative companies with solid balance sheets. But the style has been out of fashion in the past few years and these funds have actually underperformed quite severely, especially in the UK and Europe.

This is partly because valuations had grown pretty demanding, and partly due to sector-specific or company-specific issues, such as the struggles seen at weight-loss drug provider Novo Nordisk (DK:NOVO.B). Arguably, it is also partly because, despite the various geopolitical crises of the past few years, markets remained fairly ‘risk on’ throughout, never really going into defensive mode for prolonged periods of time.

If the war in Iran continues, leading to higher inflation and economic stagnation, will that give quality companies a fresh boost? It could, but with interest rates likely to stay higher for longer, valuations remain a crucial consideration.

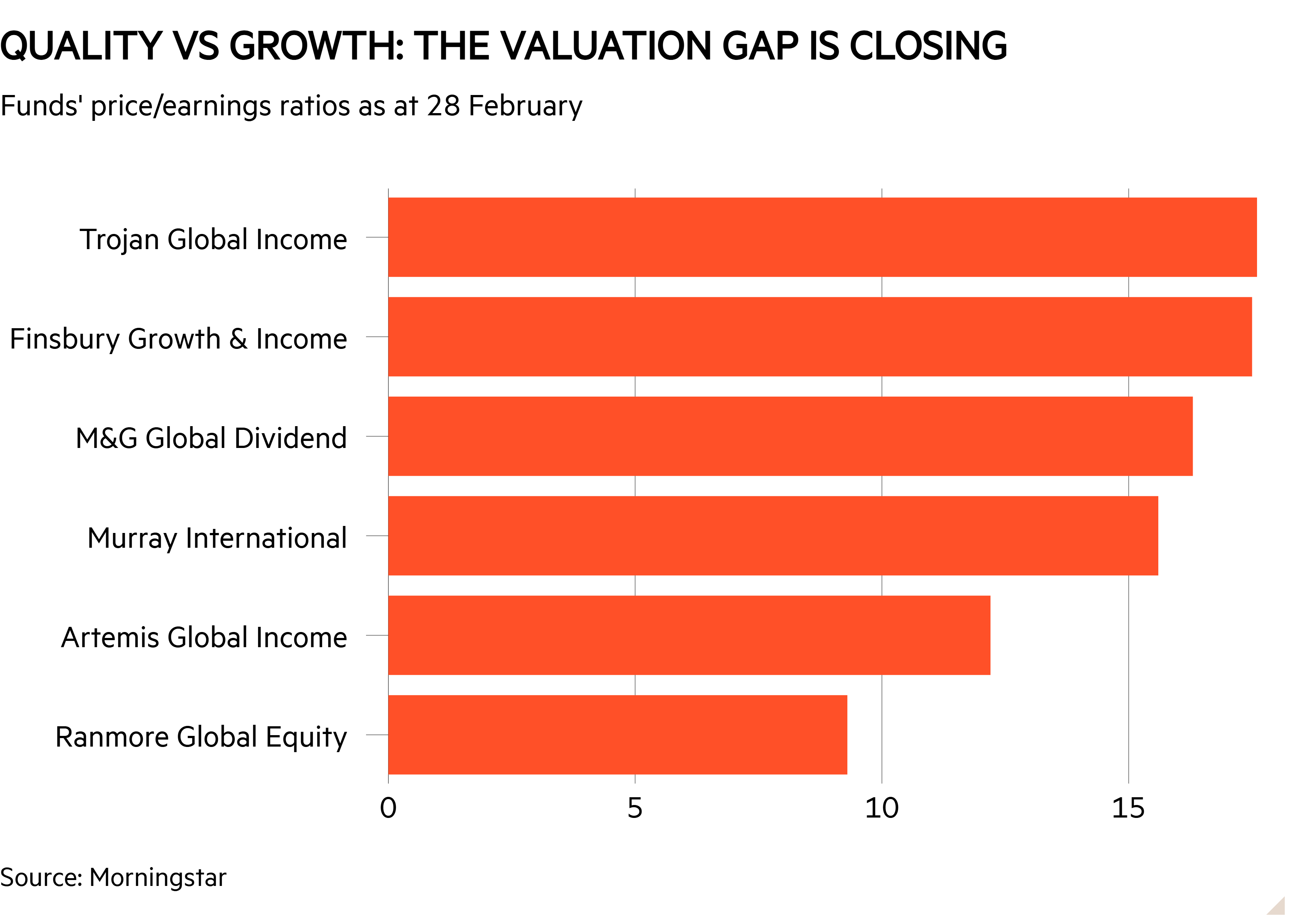

As at the end of 2025, Morningstar estimates that Fundsmith’s portfolio was still trading on a price/earnings (PE) ratio of 24. This will be lower now – the fund has shed about a tenth of its value year to date – but is still not exactly cheap. Some quality companies are starting to look less pricey, however. Unilever, for instance, was trading on a multiple of about 16 at the time of writing, although again this is partly for stock-specific reasons: investors are worried about how energy shocks will affect both its costs and its emerging market customers, and unsure about the planned spin-off of its food business.

The chart below shows how, with value stocks outperforming and quality struggling, the valuation gap between some high-profile value and quality funds is closing somewhat.

Still, a focus on valuations should continue to favour value companies overall. These have been outperforming over the past couple of years, particularly in Europe and the UK. Typical ‘value’ territory usually means a PE ratio no higher than the low teens.

Rob Morgan, chief investment analyst at Charles Stanley, argues: “Regions, sectors and styles that are priced for perfection are more vulnerable, while areas trading on reasonable multiples with solid cash generation offer a better margin of safety. This rewards patience in unloved but fundamentally sound areas.”

Jason Hollands, managing director of Bestinvest, thinks we are entering a period of ‘warflation’ rather than stagflation for the US economy – a temporary rather than permanent energy supply shock, which may not seriously impact the economy or companies, whose earnings expectations and balance sheets still look reasonably resilient. “That said, risks are building: higher energy costs, tighter financial conditions and rising bond yields all increase the probability of slower growth and potential earnings downgrades if the situation persists,” he adds.

Assuming a period of higher energy prices and lower global growth, “the balance of probabilities would favour more value-oriented investment strategies”, he says.

The funds to buy

Experts emphasise the importance of diversification in the current environment. The war could end this month or persist for some time longer yet, so we just don’t know what is going to work. Blending different styles and asset classes is a good starting point.

If you do want to give quality a go but look beyond the usual suspects of Terry Smith and Nick Train, Ben Yearsley, investment director at Fairview Investing, suggests Trojan Global Income (GB00BD82KP33). The fund invests in quality companies “purchased at attractive valuations and held for the long term”. As at the end of February, a third of the fund was in consumer staples, and another 11 per cent in healthcare. It was fairly concentrated, with just 32 stocks, and the top holdings were American derivatives exchange company CME Group (US:CME) and British American Tobacco (BATS).

For value, Hollands suggests the Xtrackers MSCI World Value ETF (XDEV), Murray International (MYI) and Ranmore Global Equity (IE00B61ZVB30). The latter was recently profiled on the IC (‘My favourite holding period is a day’). First, keep in mind that even with trackers, you do still need to take a look at what’s inside; this one still has significant exposure to the US, even if this weighting is less than the broad stock market (42 per cent).

This exposure may not be the worst thing in the world considering value stocks in the US have not rallied as enthusiastically as their European counterparts in the past year or so. Still, the ETF also has a lot in the tech sector (28 per cent), and its biggest holding is semiconductor company Micron Technologies (US:MU), whose share price has increased more than fivefold in the past year.

Meanwhile, Morgan argues for a combination of value and growth strategies. “Higher interest rates raise the cost of capital, so companies with low debt, strong free cash flow, and resilience across the cycle are likely to outperform the highly leveraged, except in the cases of very strong structural growth stories where the debt load melts away,” he says. “It’s therefore a bit of a ‘barbell’ situation for investors.”

He favours a “core of resilient compounders”, provided by value-tilted funds with a focus on earnings growth such as M&G Global Dividend (GB00B39R2Q25) and Artemis Global Income (GB00B5ZX1M70), combined with “a collection of unique growth situations”, such as the companies targeted by Scottish Mortgage (SMT).

For defensive exposure, you could also consider a sector-specific fund, although of course this is a more targeted option, not a core global equity holding. Yearsley suggests taking a look at the listed infrastructure sector, where his fund of choice is First Sentier Global Listed Infrastructure (GB00B24HJL45); Morgan likes FTF ClearBridge Global Infrastructure Income (GB00BMF7D662).

Your articles always leave me thinking.

What an engaging read! You kept me hooked from start to finish.

You’ve sparked my interest in this topic.

Posts like this are why I keep coming back. It’s rare to find content that’s simple, practical, and not full of fluff.

You always deliver high-quality information. Thanks again!