Trust Intelligence from Kepler Partners

Investor Edition

Playing catchup

Discounts have come in for equity trusts, but alternatives are still in the doldrums – we see value in the sector.

Thomas McMahon

Updated 15 Jul 2026

Disclaimer

This is not substantive investment research or a research recommendation, as it does not constitute substantive research or analysis. This material should be considered as general market commentary.

Perceptions take time to change: some of us still need to learn it hasn’t been called Czechoslovakia for 35 years. Similarly, in the investment trust sector, there is still a general perception that discounts are under pressure, but we are no longer sure this is really true – at least in the equity sectors. Equity investment trusts are back within their pre-2022 range on average, albeit at the wider end of it. And the average discount is moving much further back in and then out again on macro newsflow, as we’d expect. Meanwhile, there are a number of equity trusts trading on a premium and issuing new shares, across multiple sectors.

On the other hand, in the alternatives space the picture is different. We have seen some narrowing, with many trusts making big moves back into a narrower trading range, but in aggregate they are still some way short of their pre-2022 normality. The trend is clear though, with corporate activity of all sorts thinning the field and seeing assets come out of the sector, creating a more advantageous environment for the survivors. Here we look at those alternative trusts we think are most likely to see a sustained, significant discount narrowing back to pre-crisis levels.

The backdrop

As analysts, we spend a lot of time discussing NAV returns. It’s the best way to analyse the managers’ performance, and it should also be, subject to caveats, more predictable – at least, the factors that affect the NAV performance of different strategies should be more quantifiable and predictable. But share price returns are what you get, at the end of the day. Indeed, one of the main attractions of our sector is the ability to make exceptional returns by buying something that is out of favour and seeing the discount close when sentiment changes. The challenge is that seeing through poor sentiment, and investing in a contrarian manner, is extremely hard, and involves working against some deep and important human instincts to run with the herd.

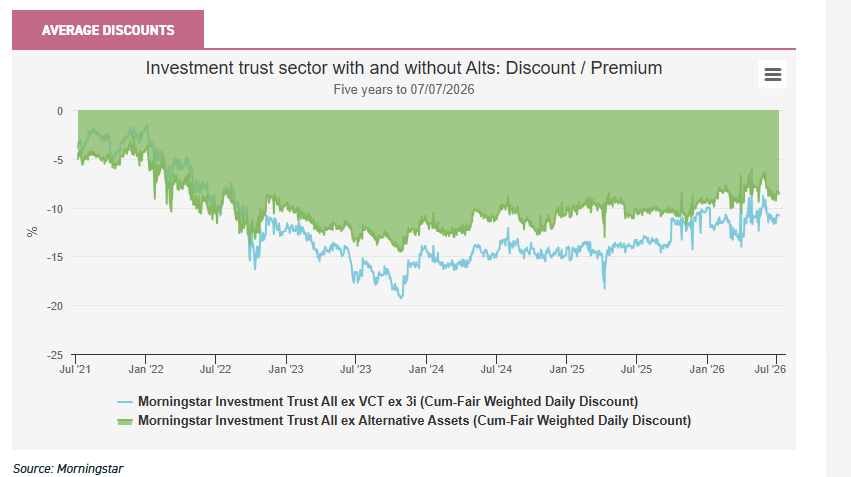

Back in late 2023, discounts were exceptionally wide until there was some certainty that the interest rate hiking cycle had peaked. Morningstar’s index of all investment trusts saw an average discount of over 19% that October. This figure had fallen to 10.8% as of 07/07/2026, having hit single figures in a few days before the latest fighting in the Middle East. Excluding the alternative asset sectors, the picture wasn’t quite so bad three years ago, with the average discount peaking at 14%-15%, and these equity and bond trusts have now established a single figure average discount in 2026, which is at 8.6% at the time of writing but has been as narrow as 6.5% when the conflict has been calm.

average discounts

Equity income strategies have seen a particularly strong recovery in demand, with the UK equity income and global equity income sectors currently both trading on a premium on average. The Asia Pacific equity income sector is meanwhile on a discount of just 1.1%. In the AIC North American sector, BlackRock American Income (BRAI) is seeking shareholder permissions to issue even more shares, the board believing the 15% it can issue not likely to be enough this year. BRAI has performed well, but also importantly, in our view, offers something very different: a heavily quant-based and systematic approach to stock selection which has worked well in US vehicles, along with a tilt to value which is quite rare after 10 to 15 years of value strategies departing and leaving the field to growth. It’s worth noting that at c. £166m in market cap it is “too small” in received wisdom, which perhaps should make boards take note that there is still plenty of demand for smaller trusts if they have the right strategy. It’s easy to see why there might be this recovery in demand for equity income. As rates have come down, equity income yields look more appealing, while the dividend growth they offer looks more attractive when bond yields are expected to fall. But we also think it’s the case that concerns about equity markets selling off have moderated, which makes the growth in equities more attractive.

In the growth equity sectors the picture is a bit more mixed, with strong divergence between winners and losers. Many of the ‘losers’ have been or are in the process of winding up or merging themselves away, and as the number of options in a sector falls, the remainder benefit from an improving technical picture. But good performance has also been rewarded, with top-performing trusts and those with a distinctive remit achieving very narrow discounts.

We have seen Scottish Mortgage (SMT) move from a 22% discount to a 7.7% discount over the past three years, and even trade on a premium for some time ahead of the SpaceX IPO. Given the huge size of this trust, at £18bn in total assets, and the huge number of shareholders, this is very meaningful for sector averages as well as investor sentiment. On the other hand, the much smaller Lindsell Train (LTI) has seen its discount move from low single figures to c. 20% over the same period: less significant for sector averages, but indicative that performance is being rewarded in some cases while other trusts are falling meaningfully out of favour. In the Europe sector, we have seen JPMorgan European Growth & Income (JEGI) and Fidelity European (FEV) enjoy meaningful discount narrowing, while the growthier strategies of Baillie Gifford European Growth (BGEU) and BlackRock Greater Europe (BRGE) have seen their discounts widen. In our view, discounts in the equity sectors can be considered back to ‘normal’: risk aversion and macro concerns are seeing them move in and out within single digits, while the success or failure of a strategy explains relative discounts. We would say, though, that the latter effect is still very pronounced compared to pre-2022, i.e. investors are currently very unforgiving about poor performance.

What about alternatives?

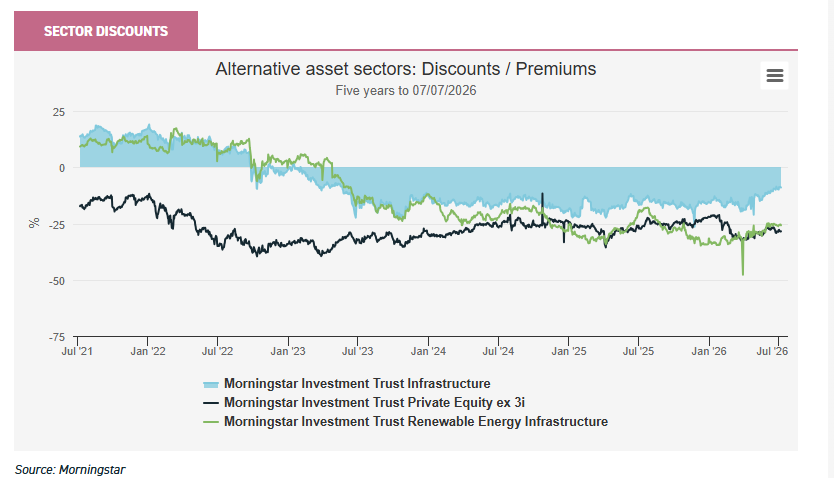

If we look at the alternative sectors, at the top level discounts don’t really seem to have moved much yet. The chart below shows the discounts of the renewable, infrastructure and private equity sectors over the past three years. Private equity looks stuck in its post-2023 range, as does renewable energy infrastructure. Only the infrastructure sector seems to be on an inward trend.

sector discounts

Prima facie, the changing rates outlook should have been positive for alternatives too. However, there are a number of factors that explain why discounts might have been slower to come in. One is simply the lead time between investment and maturity for income investors. If investors switched from alts to bonds over 2022 and 2023, they would have enjoyed yields peaking in October 2023, but then seen the opportunities get steadily less and less attractive – that index now yields 7%. On average, high yield bonds have a maturity of around three years, so anything invested at that point will have to be reinvested soon, if it hasn’t already been traded. It is true that sterling high yield is still trading closer to its peak back then, but this is a small market in international terms and dominated by some ‘interesting’ credits like Thames Water. For a diversified investor looking to reinvest, we think the yieldcos in the investment trust sector are only going to look more attractive in the coming months and years. The AIC Debt – Loans & Bonds sector moved decisively onto a premium in mid-2024, with around 8% seemingly being what investors are looking for in a high yield or otherwise riskier bond portfolio. We think as rate cuts make this harder for the conventional bond portfolios to generate, and as other risk factors recede, the high yields on offer in many of the alternatives will come down to this sort of number and lower, and bring in the discounts.

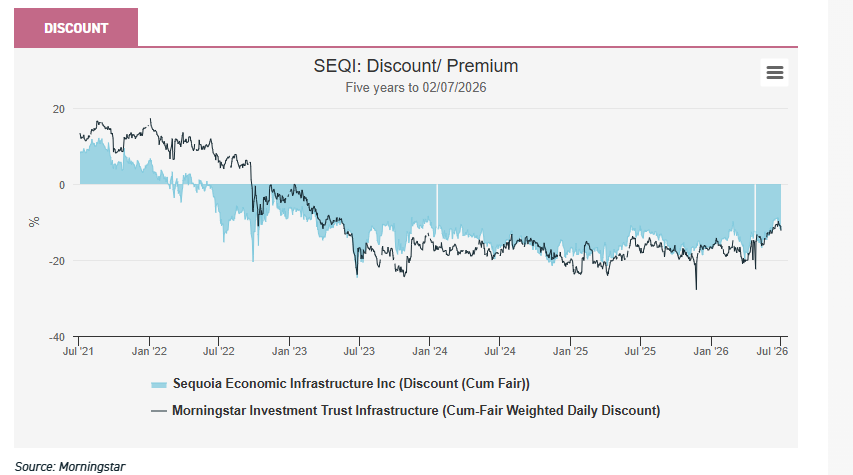

One trust we think looks ripe for a steadily narrowing discount as rates come down is Sequoia Economic Infrastructure Income (SEQI). SEQI makes loans backed by real assets, spread across numerous crucial infrastructure sectors. This yield is generated without the use of structural debt, and it has managed to maintain the same dividend yield since mid-2023, despite the rate cuts seen since then. We think that as yields on cash and government bonds come down, and with spreads in the corporate debt market looking narrow, SEQI’s yield will look ever more attractive to income-seeking investors, particularly considering the defensive characteristics to the infrastructure sector and well diversified portfolio.

Flight to the familiar

Another factor which we think has weighed on SEQI’s discount in recent months is concern about what is happening in the US private debt market. The BDCs that have run into trouble over there could hardly be more different than SEQI. SEQI invests in loans backed by real assets in critical infrastructure sectors and does not gear them up. The US BDCs are typically highly leveraged and lending to asset-light software companies. Private debt is a fairly new concept in the mass market space, so it is natural that investors might be wary, but we think it is now a well-established asset class and it makes no more sense to reject it outright than it would be to eschew equities entirely after a given sector crashes. We think investors are starting to appreciate SEQI is not affected by this US story, and that explains why the discount has come back in after widening in April when the concerns were at their peak.

discount

Source: Morningstar

As a broader point, we think investors have simply become wary of being involved in unlisted assets, and frightened that they are missing some vital information. There has been a lot of scepticism about the valuation and attraction of different unlisted asset classes, often with a specific flavour but, we think, always with an underlying scepticism in common. A few years ago we saw Hipgnosis Songs end its life amidst acrimony over valuations, and we think this created a cloud under which alts as a whole suffered. Some readers may remember that a valuation by Citrin Cooperman was at the heart of the controversy; in 2023 they valued the catalogue Hipgnosis owned at $2.6bn. Blackstone eventually bought the Hipgnosis catalogue for an implied $2.2bn valuation in 2024. Well, in May this year, Blackstone flipped the catalogue (plus some extras) to Sony for $4bn, giving them a handsome return and suggesting the original valuations weren’t too far off at all. 2023 and 2024 were the height of the uncertainty about unlisted assets. We think this sale is just one straw in the wind showing that panic and short-termism set in back then, and it’s now time to take a cooler look.

Another sign is the reopening of the IPO market, most notably with the massive success of SpaceX. SpaceX has been held by a number of investment trusts, from Scottish Mortgage (SMT) through to RIT Capital Partners (RCP), held through a period of ramp-up, massive investment and cash burn, and a lot of scepticism along the way. We can debate the valuation, but it is clearly a massive validation of the model of investing in companies which remain unlisted for much longer than before, and IPO once they are large and mature businesses. Uber is a great example of a company to follow this path much earlier. Before its IPO it was riddled with controversy, and was valued at $120bn at one stage, raising eyebrows. The IPO value ended up being a much lower $76bn, and the shares fell over 2021 and 2022, seeming to show that this model of staying private and unprofitable for longer was going to end up a disaster for early investors. However, Uber has since developed into a highly profitable business, and its market cap has reached $150bn, well ahead of the pre-IPO marks.

In Europe we are also seeing encouraging signs from the unlisted equity space. The IPO of Italy’s Bending Spoons on the Nasdaq was great news for its backers at Baillie Gifford, including BGEU and Schiehallion (MTN). Meanwhile, big fund raises in the space and defence sector have boosted the NAV of Molten Ventures (GROW), most notably the huge up-round for ICEYE, which manufactures and operates advanced satellites. The Molten team note that funding for the larger companies in the venture space has shown a good recovery from its 2022 and 2023 lows, and we are watching to see if this starts to cascade down into the earlier stage and smaller businesses. A bumper IPO of Revolut is still on the cards, which would benefit GROW. Revolut has reported excellent financials and was rewarded by a significant write-up last November. GROW has top-sliced this holding in the up-rounds, but retains a significant position. GROW’s near-60% discount has narrowed massively over the past year, delivering exceptional share price gains, but in our view at 20.5% it remains a significant discount opportunity.

Diversification is back

The artificial intelligence trade has made fortunes for those who invested in Nvidia back in 2022, and the memory manufacturers last year, and has driven returns in a number of related sectors and industries. There is scope for Anthropic to IPO at a valuation of over $1.2trn, which would be great news for SMT and MTN shareholders, and the AI trade is far from over, but we think there is a growing concern to diversify portfolios.

One way of doing this is to look for assets and portfolios which are geared to the current growth trends but for some reason haven’t revalued. We think a good example is Cordiant Digital Infrastructure (CORD). Like GROW, it has significantly rerated, but remains at a c. 20% discount. CORD invests in the “plumbing of the internet”, meaning telecoms towers, fibre-optic networks and data centres. We think it might have been categorised as a yieldco by some investors, but from the start its model of “buy, build and grow” has aimed at a 9% total return, with a dividend providing around half of that. In fact, it has grown the NAV by 13.5% annualised since launch, on our calculations, so out-performed its target and delivered growth a SMID-cap equity trust would be proud of. A particularly exciting element in the portfolio is the Prague Gateway asset, which is a project to build a huge, 26MW data centre. Development is set to begin, and there is potential for this to add a meaningful amount to the NAV over the coming years.

There’s definitely a growing sense of unease in how top-heavy markets have become, and so investors are also likely to be looking for growth opportunities outside the AI trade too. Asian and emerging markets indices are now almost as dependent on the AI trend as US and developed world indices are. There is some respite in markets such as Latin America, where commodities continue to play a major role, but commodity markets are increasingly being driven by expectations on data centre and power grid build out, so even these markets are dependent on AI to some extent. In that light, we think the growth potential in infrastructure should only look more attractive.

Indeed, we think HICL Infrastructure’s (HICL) strategic shift announced at their recent capital markets day could be a catalyst for the market to look again at its proposition. HICL’s discount has narrowed meaningfully from last year’s c. 30%, but still looks attractively wide at 16%. With the portfolio having shifted from essentially a yieldco to a 50/50 split between yield and growth, the plan is now to allocate up to 20% to ‘enhancers’: investments with a higher, 12%+ p.a., expected return, with holding periods expected to be shorter and HICL investing to grow the asset before selling it on. The team see huge opportunity in the need for growth and development in infrastructure to hit social and governmental expectations.

Conclusion

We think yield, a reassessment of unlisted assets, and the need to diversify growth portfolios should all see discounts in the alternatives space trend in over the coming months and years. There has been a lot of consolidation across the sector, with boards merging or winding up their trusts, and this has created a good technical situation for the survivors: when appetite returns, there are fewer options to choose from. Interest rate cuts would be extremely helpful, but are not necessary to see meaningful narrowing in most of the cases discussed. That said, we have seen in the equity sectors that strategies that have performed poorly or failed to buy back shares have been punished hard, and we think it possible that those in the alternative sectors which can’t provide some evidence their NAVs are justified, i.e. through asset sales, could be losers. Equity trust discounts haven’t narrowed across the board, but the winners have outweighed the impact of the losers, and we expect to see a similar Darwinian environment in alternatives.

Leave a Reply