8.9% Dividend Yield Finally Enters The Buy Zone From Annaly Capital Preferred Share

Mar. 16, 2026

Colorado Wealth Management Fund

Investing Group Leader

Summary

- Yield near 9%. Price support from retail investors about a penny below market price. Solid yield-to-risk ratio. Modest upside.

- Among Annaly Capital Management’s preferred shares, NLY-I is more attractive than NLY-F, benefiting from a favorable dividend calculation and trading at a lower price with a better yield.

- I picked up 4,148 shares of NLY-I, representing over $100k.

- Despite being callable, NLY-I has not been redeemed, and historical trading patterns suggest strong price support just below $25.

- The REIT Forum members get exclusive access to our real-world portfolio. See all our investments here »

Annaly Capital Management (NLY) has 4 series of preferred shares. I’ve traded in them from time to time. Currently, the one I’m excited about is NLY-I (NLY.PR.I).

I’ve written about shares of NLY-I several times. However, it has been rare for us to be able to post bullish ratings on them. Often the shares are just slightly above our targets for entry at The REIT Forum. That means that they are usually around 0.2% to 1.5% above our targets. Our targets adjust for dividend accrual, so they continue to increase leading up to the ex-dividend date, and then they fall by the dividend amount.

Opportunity Strikes

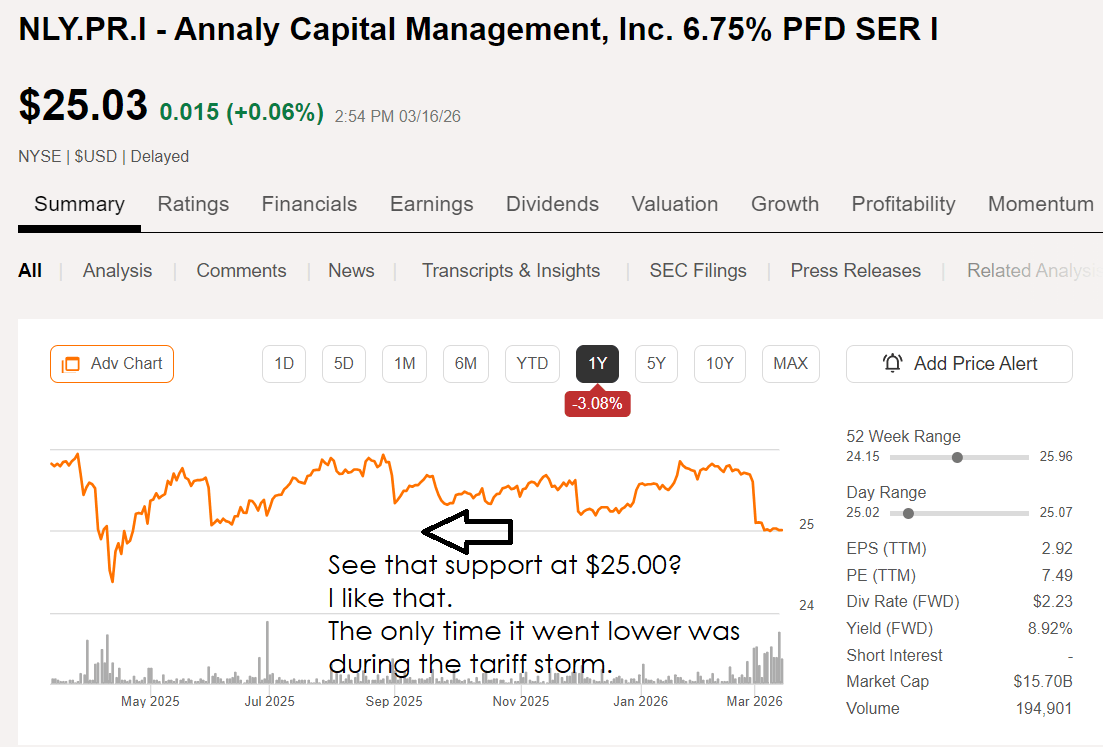

Recently, we have seen a little bit of weakness in shares of NLY-I. The weakness is allowing us to come out with a bullish rating. Presently, shares of NLY-I are trading at $25.01. That gives them an annualized yield to call of about 4.7%. That sounds quite pathetic. However, investors should recognize that the low yield to call would only happen if shares were called immediately. If there is any delay before the call happens, then the investors would be collecting a stripped yield of about 8.94% during that time. That is far more attractive.

Annaly Capital Management Could Have Called

Annaly Capital Management has had plenty of opportunities to call these shares already. They became callable and began floating on June 30, 2024. We are about 21 months past the date when shares became callable.

Further, shares of NLY-F (NLY.PR.F) are also floating-rate shares with a very similar spread. Those shares began floating on September 30, 2022. NLY-F has not been called despite floating for over 3 years.

Relative Value

I believe NLY-I is more attractive than NLY-F because NLY-I costs 36 cents less ($25.01 vs. $25.37) and the yield is better.

The dividend policy results in NLY-I having dividends that are a tiny bit larger. At first glance, it would appear that NLY-F would have the slightly larger dividends because the floating spread is higher by 1.4 basis points (basically a rounding error). However, NLY-I utilizes a more favorable method for calculating dividends. It uses the actual number of days in a dividend period divided by a 360-day year. That sounds complicated, but I’ll make it simple.

- Take 365 days of accrual and divide by 360 days (the official number of days).

- You get 1.0138889.

- Round it to 101.4% because I don’t want to type that many digits again.

- Therefore, NLY-I gets about 101.4% of the dividend accrual that would normally be expected for each year.

Consequently, our targets for NLY-I are slightly higher than our targets for NLY-F. However, the market has been valuing NLY-F at a higher price than NLY-I. Consequently, the annualized yield to call for NLY-F is negative, but the annualized yield to call for NLY-I is okay. Not great, but it’s okay. Remember that you only get such a low yield if the shares are called immediately after you purchase them. If the shares remain outstanding for longer, then the yield turns out quite a bit better. If they are not called at all, then you have a yield around the stripped yield of 8.95% with quarterly payouts. That’s pretty good.

Since the shares could be called on 30 days’ notice, we are coming to our estimate for annualized yield to call using that brief 30-day window. Being stuck with a return of 3% to 5% for a month is not bad. But if you get under 3%, then you really want it to be related to a brief period. This is a bit strange because, all else being equal, you typically want call protection to exist.

You won’t find call protection on the shares that are already floating, though. The floating-rate shares in this sector were all initially fixed-rate shares that switched over to a floating rate at the same time that the shares became callable. Because treasury rates increased significantly a few years ago, the floating-rate shares became significantly more attractive.

Note About NLY-G

NLY-G is almost always above our targets. I punish it for having such a thin floating spread. The market doesn’t seem to mind, but I find it as a bigger issue because it makes NLY-G even more reliant on short-term interest rates.

Setting Targets

One of my goals in setting the targets for NLY-I was that they would result in a very slightly positive yield to call. Today we have a positive yield to call and a slight discount to our target prices. Consequently, I am approaching shares with a mindset of collecting the attractive yield until we see a bump in the price. I believe we will most likely see a modest increase in the stripped price at some point. That means the share price adjusted for dividend accrual would probably increase by 0.5% to 1.5%. So the objective is to collect the dividend yield for now and then eventually collect a modest price improvement.

If we see the stripped price going up by about 1% or 1.5%, that could be a signal to me that it would be time to consider taking the gains and looking to reallocate. These are pretty steady shares, though. If the market tips lower, they probably won’t fall all that much. In that case, I might end up with mediocre performance but strong relative performance. That would still be okay, because it would allow us to reallocate at favorable ratios. Don’t let perfect be the enemy of good.

Of course, it is always possible that a share price could decline further. However, historically, we haven’t seen that much. Since NLY-I began floating, it has very rarely traded below $25. That makes sense for a few reasons. The first is that it results in a yield around 9% or even higher when the Fed funds rate was higher. The next is that there are more buyers for shares around $25 because there are many retail investors who would scan for shares that offered a high yield and traded below $25. That creates a decent level of support for the shares and explains why they have been so resistant to moving below $25 aside from the large hit to the markets around Liberation Day.

For People Who Are New to Annaly Capital Management

Annaly Capital Management is a mortgage REIT. They own a bunch of mortgage-backed securities. The vast majority of the portfolio is in agency mortgage-backed securities. Those have very strong credit qualities because they are supported by Fannie Mae and Freddie Mac. Consequently, the mortgage REITs that focus on agency mortgages, like Annaly Capital Management, Dynex Capital, and AGNC Investment Corp., typically have a low-risk level for their preferred shares. Some investors absolutely love the business model for the agency mortgage REITs. They see a big dividend yield on the common shares and significant “earnings,” which makes the shares look very cheap on a price-to-earnings multiple.

However, many of those investors don’t understand how the earnings metric for mortgage REITs works. They may be confused with the way yields are calculated based on historical price and how hedges flow through the income statement. Consequently, for most investors, it is much better to focus on the preferred shares. We cover the common shares within our service. However, presently, the REIT forum finds NLY-I much more attractive than the common shares.

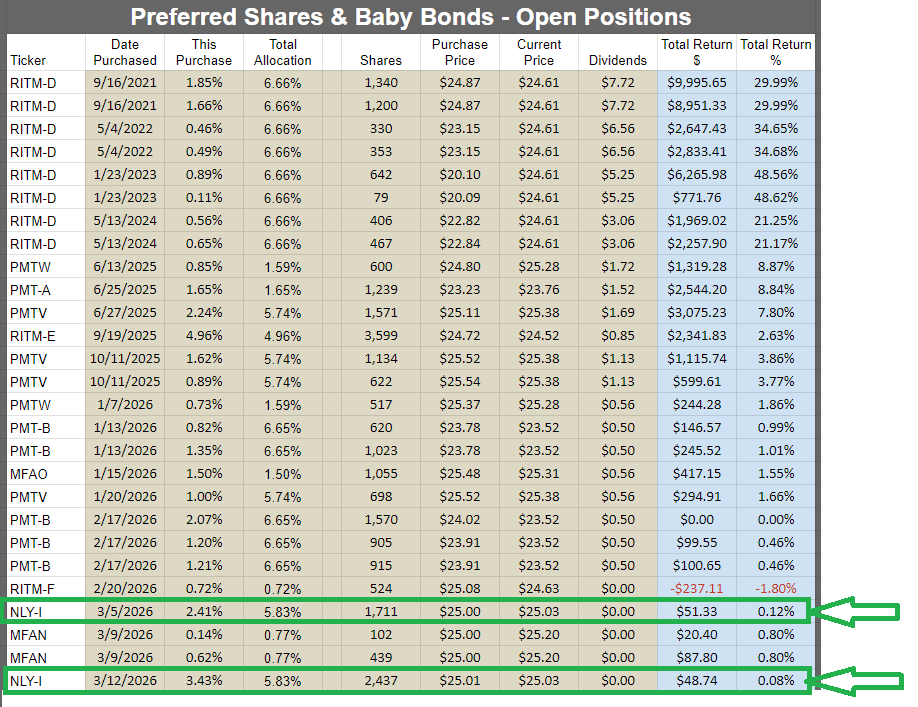

Big Position

I’ve been buying NLY-I lately. This screenshot is from our tool for subscribers that shows all our open positions. We separate the preferred shares and baby bonds from the other sectors, so this only shows the preferred shares and baby bonds:

It cuts off before showing the new positions we added on 3/16/2026, but I think that’s quite a large amount of open trades for an analyst to include in their article.

Conclusion

NLY-I offers an attractive combination of steady valuation and solid dividend yield. While it could drop further, I find it unlikely. I expect quite a bit of resistance around $25.00, as it shows up on the screening tools for more investors when it hits that price or a couple of pennies below.

Consequently, I believe the downside is relatively low while the yield is high. We have the potential for modest upside in the share price, but I would only expect around 1% to 1.5% beyond dividend accrual. Since dividend accrual is running nearly 9%, that’s not too bad.

I put over $100k into acquiring 4,148 shares of NLY-I. I eat my own cooking. Right now, it tastes like 9% with a bit of upside.

We are not rating NLY common shares in this article.

Leave a Reply