Top 3 REITs For Reliable Income In Volatile Markets

Apr 08, 2026 MRP, DRH, PINE, LEN.B, PINE.PR.A

Steven Cress, Quant Team

Summary

- REITs outperformed the broader market in Q1 2026, supported by a rotation away from large-cap tech stocks.

- As the markets and risk sectors rally on positive geopolitical news, this could be a good opportunity to add REITs on any rotational related weakness.

- Geopolitical events and midterm elections may usher in more volatility, I highlight three REITs with strong AFFO growth and well-covered dividends in industries riding favorable tailwinds.

- REITs can provide steady income and potential downside resilience in volatile markets. My three picks have an average trailing 12-month dividend yield of 6.9% versus roughly 1.2% for the S&P.

- I am Steven Cress, Head of Quantitative Strategies at Seeking Alpha. I manage the quant ratings and factor grades on stocks and ETFs in Seeking Alpha Premium. I also lead Alpha Picks, which selects the two most attractive stocks to buy each month, and also determines when to sell them.

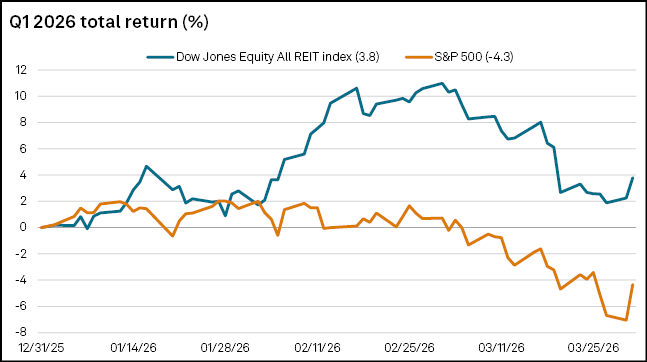

REITs Outperform as Discounted Valuations Attract Income Investors

REITs outperformed the broader market in the first quarter of 2026, supported by discounted valuations, the rotation away from big tech, and improving expectations for interest rate cuts. Performance was pressured later in the quarter by elevated volatility tied to the Middle East conflict and shifting rate expectations, but most subsectors ended the quarter in positive territory, while 33 REITs have raised their dividends so far this year, some by double-digits.

Markets rallied and Treasury yields fell on Wednesday after the U.S. and Iran agreed to a conditional ceasefire framework, led by tech, industrial, and cyclical stocks. Any near-term rotation could create opportunities to buy REITs on the dip, while positioning for volatility tied to geopolitical developments and the upcoming midterm elections. In that environment, REITs can offer relatively steady income and potential downside resilience.

Reliable income, attractive valuations, and structural demand drivers are key reasons SA Analyst Brad Thomas believes it is time to overweight REITs, although he warned that not all REITs are created equal:

REITs are not a monolith. They are a collection of businesses – some average, some exceptional – and the key is to identify durable cash flows, strong management teams, competitive advantages, and intelligent capital allocation. As much as I love REITs, I would not recommend putting all your eggs in one basket.

Backed by tangible assets and contractual revenue streams, REITs can offer durable income to potentially stabilize a portfolio amid elevated volatility and sticky inflation. Investors seeking exposure to REITs can use Seeking Alpha’s quantitative tools to find investments offering solid yields supported by strong fundamentals.

How I Chose Top 3 Strong Buy REITs

Using Seeking Alpha’s REIT Screener, I identified 3 Strong Buy REITs showcasing strong AFFO growth, well-covered dividends, and diverse industry exposure. My three picks offer forward yields of 4.2% to 10.9%.

Seeking Alpha’s Quant REIT Ratings are generated by a proprietary model that analyzes more than 100 metrics for each REIT relative to sector peers and assigns grades across five factors: Growth, Value, Profitability, Revisions, and Momentum. The ratings incorporate key REIT-specific metrics such as FFO, AFFO, FAD, and gross properties. Separate Dividend Grades evaluate each REIT’s payout based on Safety, Growth, Yield, and Consistency relative to sector peers.

In the section below, I highlight context, recent developments, and key metrics supporting each REIT’s Quant Rating.

1. Millrose Properties, Inc. (MRP)

- Market Capitalization: $4.60B

- Quant Rating: Strong Buy

- Sector: Real Estate

- Industry: Other Specialized REITs

- Quant Sector Ranking (as of 4/8/2026): 1 out of 169

- Quant Industry Ranking (as of 4/8/2026): 1 out of 11

- Dividend Yield (FWD): 10.97%

Spun out from homebuilding giant Lennar Corporation (LEN) in 2024, Millrose Properties is a homesite option platform for residential homebuilders with 142,139 homesites in its portfolio across 30 states. Targeting a total addressable market exceeding $170B, Millrose’s business model is benefiting from structural tailwinds as U.S. housing inventory remains near historical lows and homebuilders increasingly seek financing solutions to secure land.

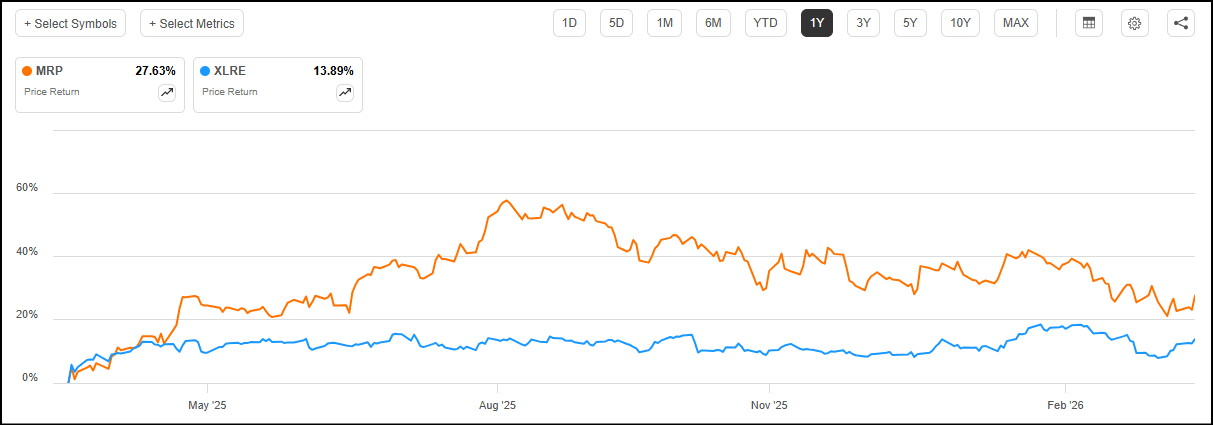

MRP vs. S&P 500 Real Estate Sector (XLRE): 1Y Price Return

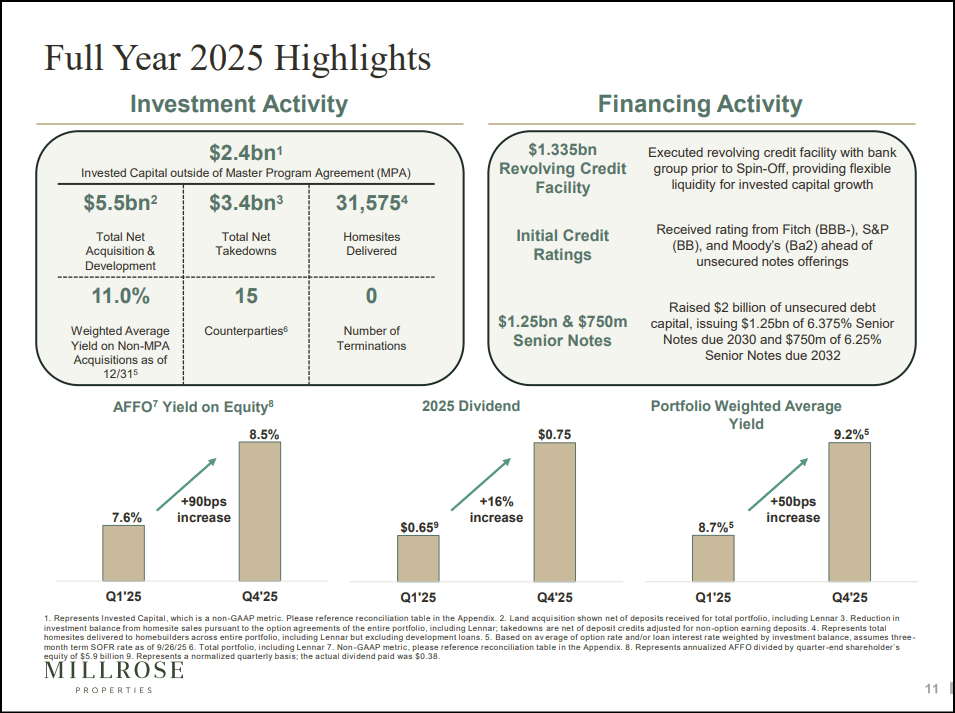

In FY 2025, its first year as a public company, Millrose navigated affordability headwinds and macro uncertainty to deliver 31,575 homesites while topping AFFO guidance as the structural need for housing capital remained unchanged. Invested capital outside the Lennar Master Program Agreement reached $2.4B, generating yields of 11.0%, while reporting zero option terminations across the portfolio.

Driven by a strong pipeline and improving backdrop, Millrose expects AFFO to grow by 10% in FY 2026, and invested capital outside the Lennar MPA to increase by an additional $2B, CEO Darren Richman said in the earnings call:

2025 was a defining year for Millrose. Despite a cautious homebuilding environment, we were embraced across the industry with a reception that exceeded even our own expectations, validating both the concept and our team’s execution. 2025 proved the model. 2026 is where we intend to begin showing its full potential. We believe we have the platform, the pipeline, the partnerships and the track record, and we are just getting started.

According to consensus estimates, Millrose FFO is projected to grow by nearly 30% in FY 2026, backed by bullish sell-side analyst revisions in the past 3 months. Strong FFO margins, cash flow, and return on capital drive an A+ Profitability Grade.

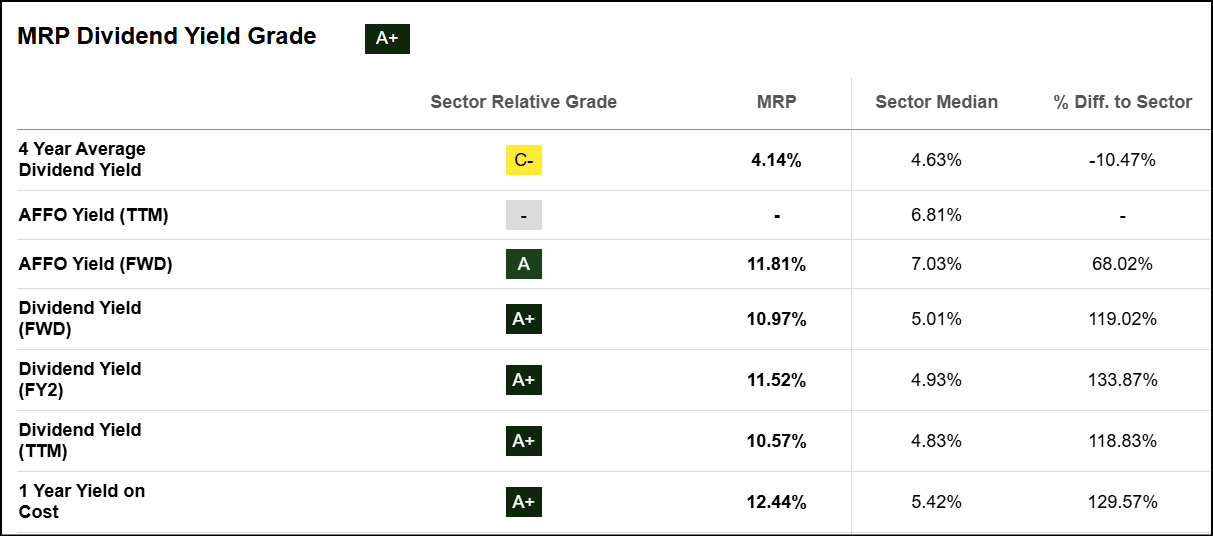

Millrose offers a dividend yielding 10.97%, which is expected to grow in the next two years, supported by strong cash flow generation and AFFO. Exceptional FFO interest coverage and conservative leverage underpin Millrose’s ‘A’ Dividend Safety Grade, which measures a company’s ability to continue paying the current dividend amount.

Although Millrose has increased its dividend each quarter since initiation, its relatively short payout history weighs on the Dividend Consistency Grade. However, the score is likely to improve as the company establishes a longer record of payments. Millrose is trading at a 43% discount to the sector based on a forward price-to-AFFO of 8.6x vs. the sector’s 15x for an A+ Valuation Grade. A high yield, robust AFFO, and strong growth prospects make MRP my top REIT pick.

2. DiamondRock Hospitality Company (DRH)

- Market Capitalization: $1.94B

- Quant Rating: Strong Buy

- Sector: Real Estate

- Industry: Hotel & Resort REITs

- Quant Sector Ranking (as of 4/8/2026): 5 out of 169

- Quant Industry Ranking (as of 4/8/2026): 1 out of 14

- Dividend Yield (FWD): 4.25%

DiamondRock Hospitality owns 35 premium quality hotels concentrated in urban gateways and resort destinations under leading global brands such as Hyatt, Marriott, and Hilton. The portfolio covers 26 geographic markets with 45% of EBITDA deriving from the top five: Boston, Chicago, New York City, the Florida Keys, and Fort Lauderdale.

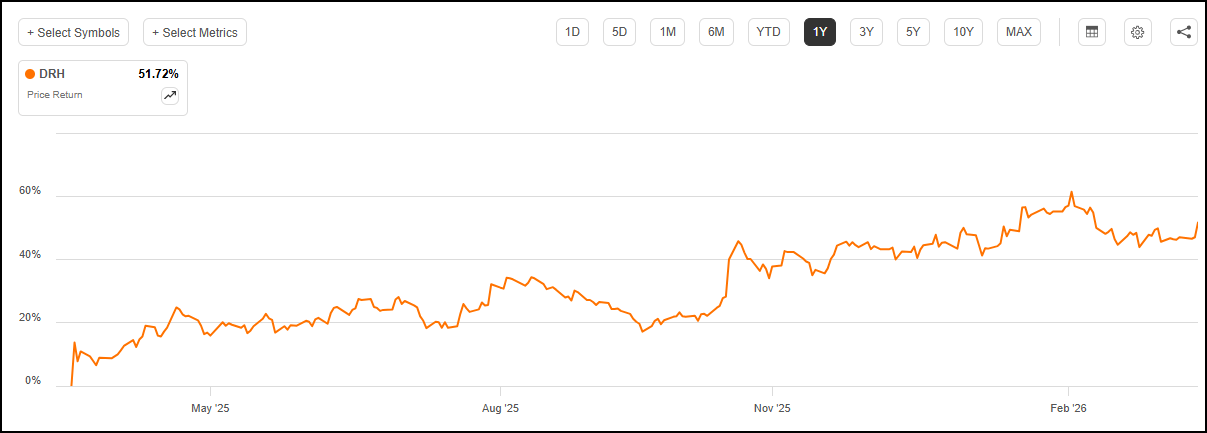

DRH has crushed the market in the past year, alongside top small-cap peers, driving an A- Momentum Grade, as leisure demand remains robust and consumer spending resilient. DRH dipped after the conflict in the Middle East escalated, offering a buying opportunity as it trades at an attractive valuation.

DRH 1Y Price Return

Stronger than expected transient demand and out-of-room spending, offsetting the impact of the government shutdown, helped drive growth in RevPAR, FFO, and net income in FY 2025. Although the political and economic backdrop warrants caution, DRH sees several favorable factors supporting a positive outlook in 2026, including key markets hosting the majority of FIFA World Cup matches, America 250 celebrations, and post-renovation tailwinds.

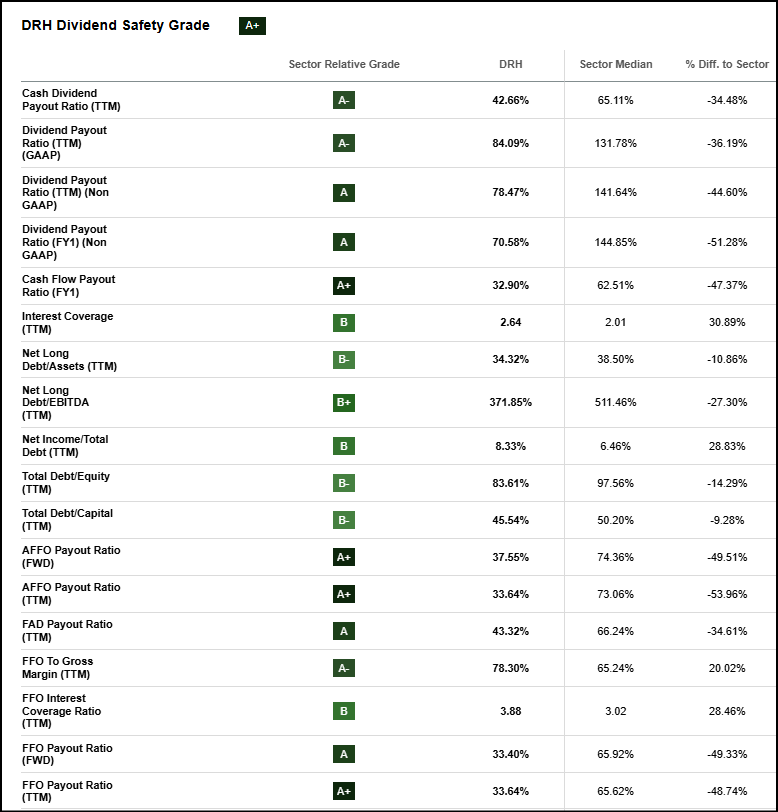

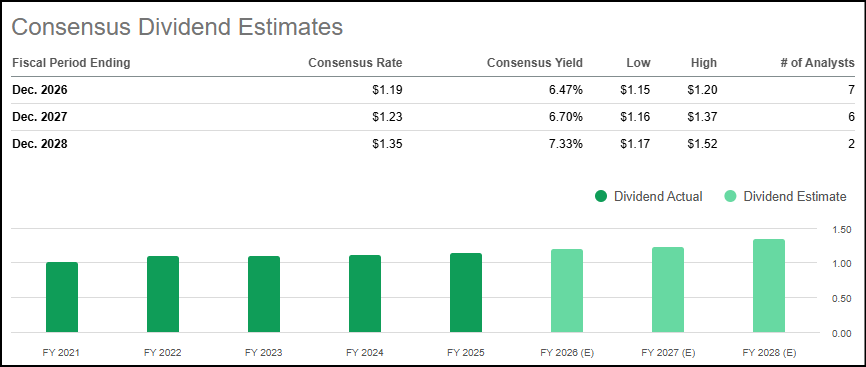

FFO is expected to grow steadily in the next three fiscal years while strong cash flow and AFFO drive an A- Growth Grade, along with a dividend that surged by a CAGR of 60% in the past 3 years. DRH offers a safe dividend yielding 4.25%, supported by payout ratios significantly lower than the sector and solid interest coverage.

DRH is trading at only 9x forward AFFO for a solid Valuation Grade, supported by attractive trailing EV/EBITDA and price/rental revenue multiples relative to sector peers. DRH is a solid addition to my Strong Buy REIT basket, showcasing a visible FFO growth path and well-positioned to ride industry tailwinds in key markets in 2026.

3. Alpine Income Property Trust, Inc. (PINE)

- Market Capitalization: $299.99M

- Quant Rating: Strong Buy

- Sector: Real Estate

- Industry: Diversified REITs

- Quant Sector Ranking (as of 4/8/2026): 8 out of 169

- Quant Industry Ranking (as of 4/8/2026): 1 out of 11

- Dividend Yield (FWD): 6.53%

Alpine Income Property Trust owns and operates 127 net lease properties in 33 states, featuring top franchises such as Lowe’s Companies, Inc. (LOW), DICK’S Sporting Goods, Inc. (DKS), and Walgreens. Alpine offers a stable income profile, supported by a 99.5% occupancy rate with a Weighted Average Remaining Lease Term of 8.4 years.

PINE 1Y Price Return

PINE grew AFFO by 22.7% YoY in Q4 2025, and +8.6% for the full-year, while completing a record $277.7M in investments, including $177M in commercial loan originations and $100.6M in 13 property acquisitions. Annual revenue grew by 15.9% YoY to $60.5M, primarily driven by a sharp increase in interest income from commercial loans and investments alongside modest growth in lease income.

PINE FY 2025 Revenue by Segment

According to company guidance, Alpine expects even more growth in 2026, with AFFO estimated to increase by double digits. The results contributed to strong forward AFFO growth, driving an ‘A’ Growth Grade, supported by bullish long-term FFO estimates from sell-side analysts. PINE offers a fast-growing and consistent dividend yielding 6.53% with a 5Y growth rate of +6%. It is projected to continue growing for the next three fiscal years, adding support to an A- Dividend Growth Grade. PINE has paid out a dividend for six consecutive years – including 6 straight years of growth.

Despite surging momentum in the past year, PINE is trading at 8.7x forward AFFO, driving an attractive valuation. PINE wraps up my basket of Strong Buy REITs for volatile markets, showcasing strong collective fundamentals, high growth, and solid yields.

3 Strong Buy REITs For Reliable Income

REITs were crushing the market to start off the year, supported by hopes of easing interest rates and a rotation out of stretched tech stocks. Although returns were compressed by the volatility fueled by the Iran war, most REIT subsectors finished Q1 2026 in the green, outperforming the broader market. REITs can offer durable cash flow streams and a potential hedge against inflation, but investors should ensure dividends are backed by strong fundamentals. SA Quant identified three REITs with strong AFFO growth and average dividend yields of around 7%.

Leave a Reply