3 Best Dividend Stocks With 6%+

Yields And Attractive Valuations

Apr 30, 2026

Steven Cress, Quant Team

SA Quant Strategist

Follow Seeking Alpha on Google for the latest stock news

Summary

- In today’s income landscape, selectivity remains critical. High yields can signal risk, but stocks with strong fundamentals prove that higher yields can coexist with discounted valuations.

- Higher oil prices can create downside pressure on even the best dividend stocks, as investors price in higher-for-longer interest rates.

- However, the underlying cash flow strength, FFO growth, and balance sheet health in these Strong Buy stocks help mitigate risk.

- For patient investors, periods of volatility and price weakness may offer attractive entry points, allowing the opportunity to lock in attractive yields ahead of a more normalized macro environment.

- I am Steven Cress, Head of Quantitative Strategies at Seeking Alpha. I manage the quant ratings and factor grades on stocks and ETFs in Seeking Alpha Premium. I also lead Alpha Picks, which selects the two most attractive stocks to buy each month, and also determines when to sell them.

Best Dividend Stocks: Yield + Quality = ‘Sweet Spot’

Investors looking for the best dividend stocks are often challenged to balance higher yield and higher risk. So, finding quality stocks within this space requires identifying a sweet spot where yields are high but risk is not elevated. Broadly speaking, yields much higher than 6% can signal risk around fundamental weakness or declining growth potential. However, certain sectors, such as real estate, can often support yields in the 9-10% range without sacrificing quality. This is where focusing on Strong Quant Buys with attractive Dividend Grades comes into play.

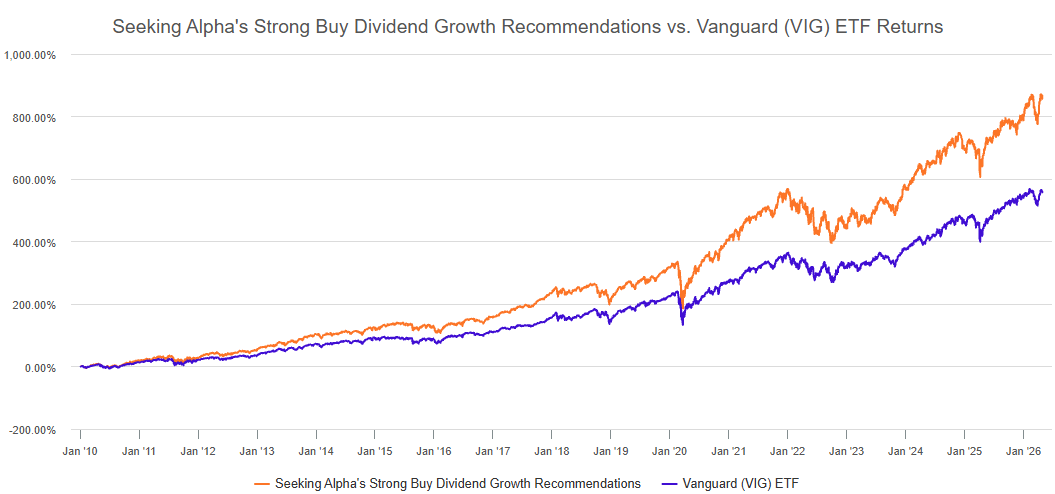

“Quantamental” Analysis Outperforms VIG Over Time

During the last 12 years, Quant’s back-tested strategy has delivered very impressive returns, beating the Vanguard Dividend Appreciation ETF (VIG). Looking ahead, the dividend environment in 2026 remains dependent on Federal Reserve policy and geopolitical uncertainty, which has created volatility in both the fixed-income and high-yield spaces. However, with inflation potentially leveling off and interest rates expected to moderate by year-end, the backdrop for selectively owning high-quality, high-yielding dividend stocks remains attractive. While risk remains in the short term, buying opportunities exist for stocks with solid fundamentals.

How I Chose the Best Dividend Stocks With 6%+ Yields

To select the best dividend stocks to feature in this article, I used the Seeking Alpha Stock Screener and chose the pre-selected Top Quant Dividend Stocks and filtered for Quant Strong Buys. I then selected stocks with forward yields above 6%, high Valuation Factor Grades, and attractive Dividend Grades.

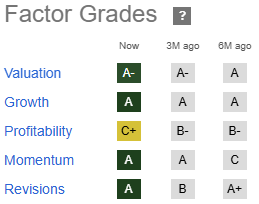

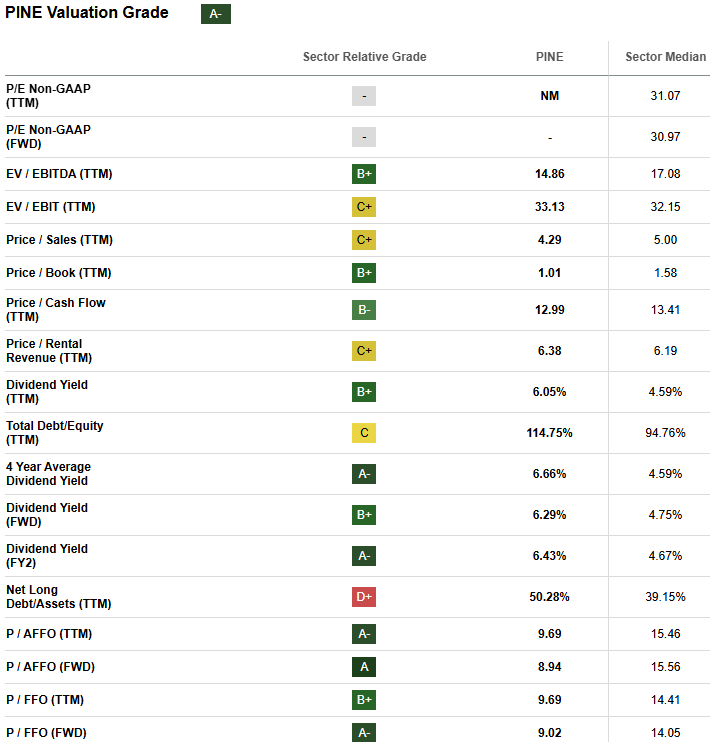

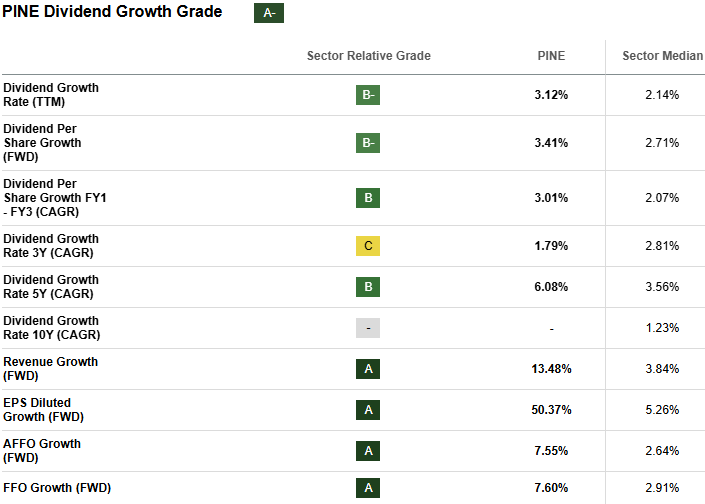

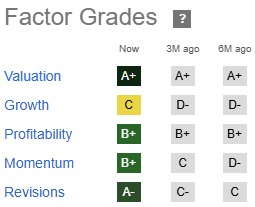

1. Alpine Income Property Trust, Inc. (PINE)

- Yield: 6.29%

- Market Capitalization: $338.82M

- Quant Rating: Strong Buy

- Quant Sector Ranking (as of 04/30/2026): 11 out of 171

- Quant Industry Ranking (as of 04/30/2026): 1 out of 11

- Sector: Real Estate

- Industry: Diversified REITs

Beginning with a small but impressive dividend stock selling at an attractive valuation, Alpine Income Property Trust is a net lease REIT that owns single-tenant retail properties leased to high quality companies under long-term agreements. The company’s portfolio consists of solid retailers, such as Wal-Mart (WMT) and Home Depot (HD), supporting stable and predictable rental income. PINE’s dividend yield tops 6% and is backed by reliable occupancy rates and conservative payout ratios. Despite these strengths, the stock trades at an attractive valuation, which is where we begin the Quant analysis.

PINE’s ‘A-‘ Valuation Factor Grade and top industry rank are well supported by its forward P/FFO valuation of 9.02, which represents more than a 35% discount to the sector median. This signals that the market is pricing more risk for the stock likely due to its small-cap status. However, when we look at Alpine’s forward growth estimates, a different story unfolds, helping to support the company’s attractive Dividend Growth Grade.

For a REIT like Alpine Income, FFO (funds from operations) is a core earnings driver, so its 7.60% Forward FFO Growth, which is more than double the sector median, more than supports PINE’s valuation. Furthermore, this supports AFFO expansion and dividend increases, reinforcing the 6%-plus yield. When interest rates finally stabilize, net lease REITs like PINE could see further growth along with continued attractive yields. The combination of steady cash flows and discounted pricing highlights the appeal of larger, mid-cap REITs with similar attributes.

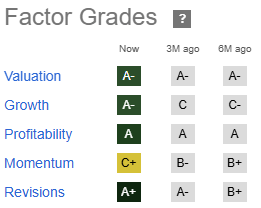

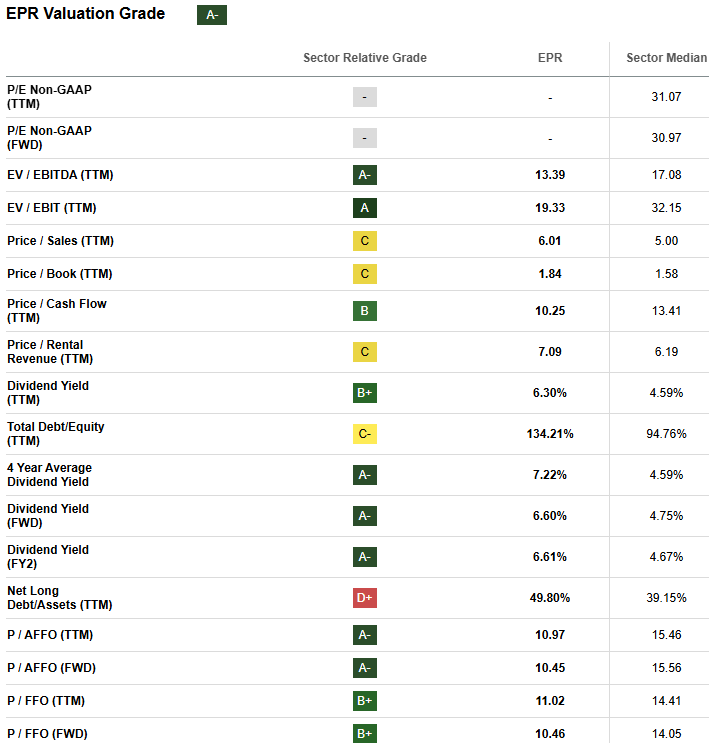

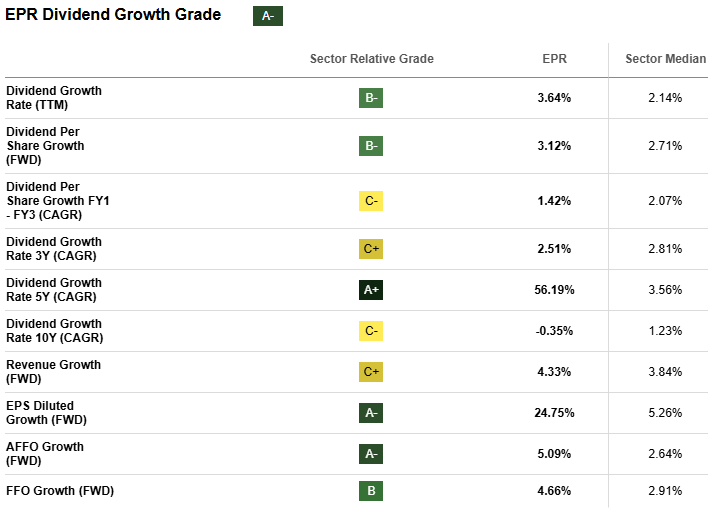

2. EPR Properties (EPR)

- Yield: 6.60%

- Market Capitalization: $4.31B

- Quant Rating: Strong Buy

- Quant Sector Ranking (as of 04/30/2026): 9 out of 171

- Quant Industry Ranking (as of 04/30/2026): 2 out of 3

- Sector: Real Estate

- Industry: Other Specialized REITs

EPR Properties is a specialty REIT that invests in experiential real estate, such as movie theaters, amusement parks, and ski resorts. While this niche space was once associated with higher risk, a combination of a resilient consumer and EPR’s portfolio diversification and consistent rent collection has restored investor confidence. The company’s 6.6% dividend yield is supported by strong cash and tenant health. Meanwhile, its valuation and dividend growth potential remain attractive.

Starting with EPR’s 10.46 forward P/FFO, this valuation metric suggests a discount of about 25% to the sector median. With growth improving and strong (its ‘A-‘ Growth Factor Grade has jumped up from a ‘C’ in three months), EPR appears ready to support its attractive 6.6% yield. This helps explain the REIT’s sector-leading Dividend Growth metrics.

EPR’s forward FFO Growth of 4.66% is significantly ahead of sector peers, which weigh in at an average of 2.91, and its Dividend Growth Rate – CAGR – over the past five years is more than 10x the sector. With consumer spending remaining resilient through recent geopolitical concerns and the potential for normalization later in the year, EPR offers a unique blend of income and recovery driven upside. That combination leads to a smaller-cap real estate company that operates in a different space but with similarly compelling valuation and yield profiles.

3. The RMR Group (RMR)

- Yield: 10.37%

- Market Capitalization: $556.53M

- Quant Rating: Strong Buy

- Quant Sector Ranking (as of 04/30/2026): 5 out of 171

- Quant Industry Ranking (as of 04/30/2026): 1 out of 3

- Sector: Real Estate

- Industry: Diversified Real Estate Activities

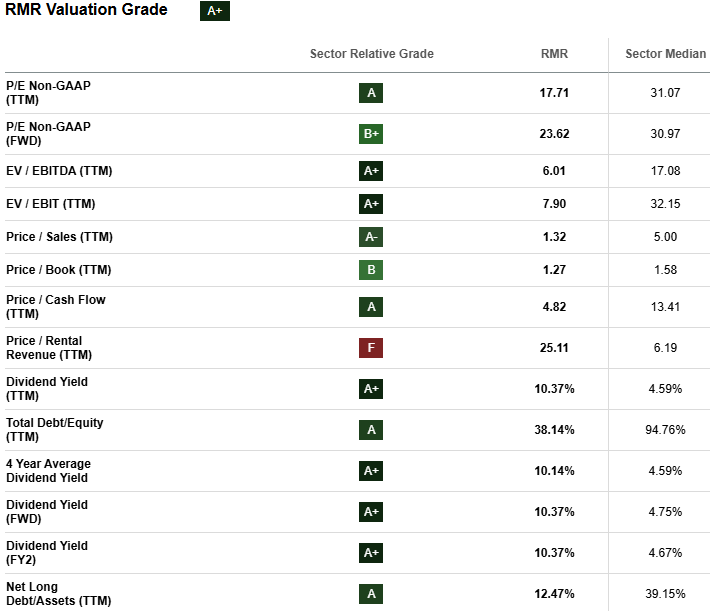

The RMR Group is not a REIT but an alternative asset management company specializing in real estate and operating companies. So, rather than owning and operating the real estate directly, it earns management fees tied to assets that are owned by REITs. This asset light model generates strong margins and supports its high dividend, offering investors exposure to real estate without the downsides of direct property ownership. RMR has demonstrated consistent fee collection and cash flow stability. This status leads to dividend safety and is complemented by an attractive valuation.

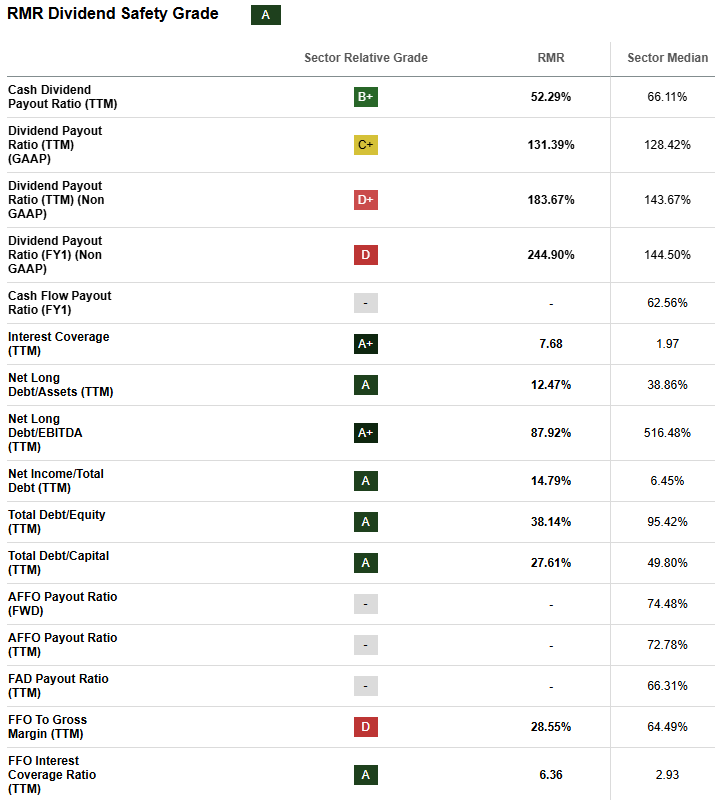

RMR’s forward P/E of 23.62 offers more than a 23% discount to the sector median, and its 4-Year Average Dividend Yield of 10.14% provides historical evidence of its ability to maintain its high dividend. While its ‘C-‘ Dividend Growth Score indicates average growth compared to sector peers, the real estate company’s yield is already high, and its Dividend Safety Score is also attractive.

According to our back-testing, companies with a Dividend Safety Score of at least ‘A-‘ or better have averted a dividend cut 99% of the time. RMR receives a solid ‘A’ grade for dividend safety, which is supported by an FFO Interest Coverage Ratio of 6.36, which is more than double the sector median. This suggests RMR can easily meet its debt obligations, which is a strong signal that its dividend is reinforced by healthy underlying cash flows. For income investors, this presents an opportunity to capture both yield and valuation upside. Taken together, these ideas highlight a broader theme of buying opportunities across the real estate sector.

Conclusion: High Yields and Quality in Best Dividend Stocks

In today’s income landscape, selectivity remains critical. High yields can signal risk, but stocks with strong fundamentals like PINE, EPR, and RMR demonstrate that higher yields can coexist with discounted valuations and attractive Quant Dividend Scores. A near-term risk worthy of consideration is that higher oil prices can create downside pressure on even the best dividend stocks as investors price in higher-for-longer interest rates. However, the underlying cash flow strength, FFO growth, and balance sheet health in these Strong Buy stocks help mitigate risk. For patient investors, periods of volatility and price weakness may offer attractive entry points, allowing the opportunity to lock in attractive yields ahead of a more normalized macro environment.

Leave a Reply