· Total dividends declared of 2.11p per Ordinary Share for the quarter (31 December 2024: 2.11p).

· The Board reconfirms the Company’s full-year dividend target guidance for the year ending 31 March 2026 remains unchanged at 8.43p per Ordinary Share (31 December 2024: 8.43p).

· Dividend cover for the full-year is forecast to be covered in a range of 1.1x – 1.3x by earnings post-debt amortisation.

· Since inception the Company has declared total Ordinary Share dividends of £431m, the equivalent to 82.6p per Ordinary Share.

Image caption,Richard Fisher, with his home brewing kit and Brewdog founder James Watt’s book of business advice

ByCalum Watson

BBC Scotland

Published17 February 2026

Updated 24 minutes ago

Richard Fisher likes beer. He brews his own ale at home and once considered buying a brewery. But he never expected he might lose £12,000 investing in Brewdog.

For the former small business adviser from Suffolk, taking a small stake in the upstart beer company from north east Scotland seemed an opportunity too good to miss.

“Maverick, independent, to a certain extent rebellious – it was all good stuff,” he said.

Richard, 58, is one of more than 200,000 investors who put money into the firm’s “Equity for Punks”, external scheme.

Typically they spent about £500 on shares costing £20-30 each but Richard, seeing the firm’s rapid expansion, invested £12,000 in the hope of a good return.

“I genuinely thought Brewdog would go public, be listed on the stock market with the freedom to buy and sell shares and there was potential to make a bit of profit.”

Even so, there is no guarantee that you will not lose any of your capital. You would have to be extremely unlucky to lose all of your investment but it’s one reason to have a diversified Snowball.

Value Rotation Is Here: How To Position Your Portfolio For Maximum Yield

Feb. 17, 2026

Rida Morwa

Investing Group Leader

Summary

Hold Safety: We will continue to own “safe” assets like Agency MBS, municipal bonds, and preferred equities.

We are buying the “fear” in the public market for credit-risk assets. Institutions are willing to pay near par; we can buy them at a discount.

We are avoiding consumer-dependent dividends (like WEN) in favor of landlords who rent to them (like O).

Valuation Matters: In a high-valuation market, we will realize gains in expensive stocks to fund purchases in bargain sectors.

Looking for a helping hand in the market?

Members of High Dividend Opportunities get exclusive ideas and guidance to navigate any climate.

akinbostanci/iStock via Getty Images

Co-authored with Beyond Saving

Typically, we spend most of our time talking about individual picks in our public articles. Today, we are going to pull back the curtain and provide an article that is usually reserved for our members at High Dividend Opportunities, where we discuss our view of the macro environment and the trends in the market that are driving our decision-making about which sectors to look into for new opportunities and which positions we want to exit.

So, instead of focusing on exactly which picks to buy, let’s talk about where the market is headed and where we want to look for dividends in 2026.

The Rotation to Value

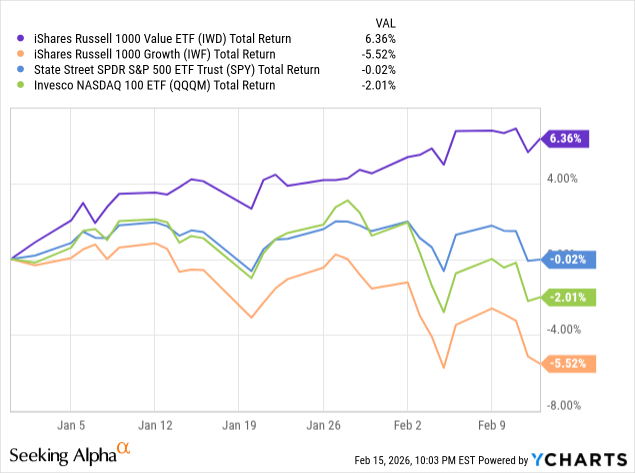

It is still early, but so far, 2026 has been a year of rotation.

The iShares Russell 1000 Value ETF (IWD) is up 6.3%, while the iShares Russell 1000 Growth ETF (IWF) is down 5.5%:

It’s a remarkable shift from last year, where Growth was surging while Value stocks lumbered along.

One month doesn’t make a trend, but there is a sense that the market is cooling on Growth and warming up to Value—but there are also some other notable movements in the market. Today, we want to take a look at the underlying drivers of the market and what that means for dividend investors.

An Emphasis on Safety

As we look at the strongest and weakest price action in our portfolio year-to-date, there appears to be a clear preference in the market for safety. Agency mREITs are up a lot to start out the year, even though they are trading at high premiums to book value.

Additionally, we’ve seen the discounts to NAV shrink for holdings like BNY Mellon Municipal Bond Infrastructure Fund, Inc. (DMB), which was trading at a 10% discount to NAV at the end of December and is now trading at just a 5% discount.

We see reliable dividend growers like Realty Income (O) and Enterprise Products Partners (EPD) seeing some positive momentum after a fairly flat 2025.

Essentially, the holdings in our portfolio that focus on safe credit assets or physical assets like commodities are performing the strongest.

On the other side of the coin, we are seeing credit risk holdings underperforming. In our portfolio, that primarily means BDCs and CLO funds have been flat to down.

While we continue to believe that credit losses are likely to remain relatively low, there is fear in the equity markets that is being reflected in the price action of businesses and funds that are exposed to credit risk.

This fear isn’t being shared among institutions.

Public vs. Private Credit Concerns

Among many assets, there is a huge discrepancy between what the publicly traded stock market is willing to pay for assets and what institutions are willing to pay.

We’ve seen this in several scenarios in our portfolio. For example, SoftBank (SOBKY) is buying DigitalBridge (DBRG) and taking it private for over a 50% premium to its trading price before the rumor. Apollo Commercial (ARI) announced a deal to sell its entire loan portfolio for 99.7% of its carrying value, while the market was pricing in a 20% discount because it feared the credit risk. Even Realty Income has observed that private capital was willing to pay more for real estate assets and is opening up a fund that the public company will manage.

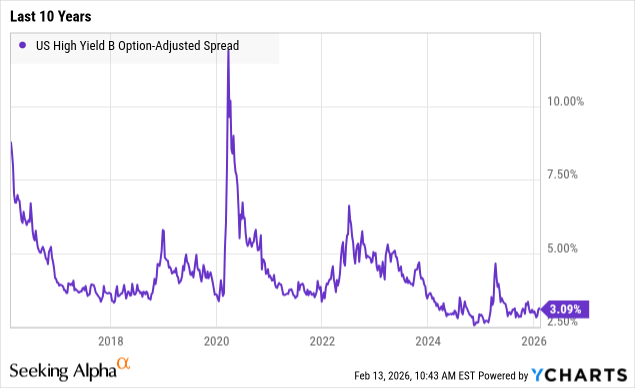

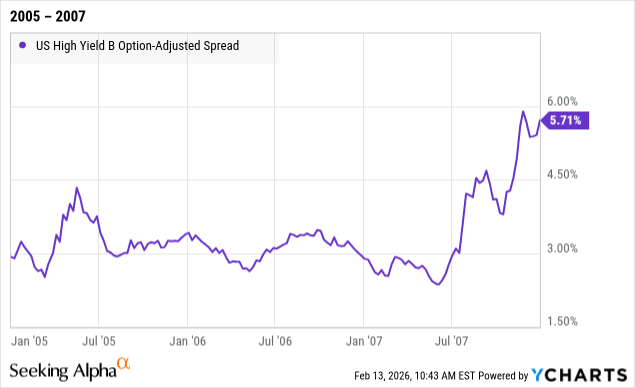

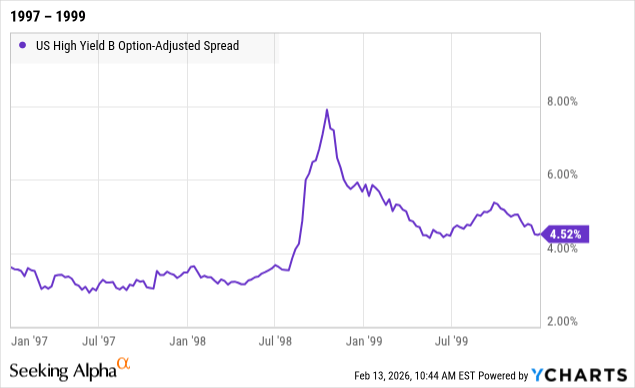

Here is a look at High Yield B Option-Adjusted Spreads. This is the spread that B-rated loans are getting over the benchmark; lower means that institutions are pricing in less default risk:

These spreads are primarily influenced by the supply and demand balance between lenders and borrowers. The B spreads are the most sensitive because it is a credit rating that implies higher risk, but it doesn’t imply that there is distress going on right now. If there are a lot of lenders looking to deploy capital relative to companies looking to borrow, spreads will be lower, and they will accept a lower yield. If there are few lenders relative to the number of companies looking to borrow, then the spreads get higher. This is often indicative of either lenders having a lack of liquidity or lenders deciding that lending money to B credits is too high of a risk.

As a result, it can often serve as the canary in the coal mine, with spreads often widening considerably before a recession starts and even before the stock market declines.

These markets are dominated by institutions, whereas in the stock market, there is significant participation among retail investors. In the stock market, we’re seeing many of our credit-risk-exposed holdings trading at steeper discounts or lower premiums than they have in the past.

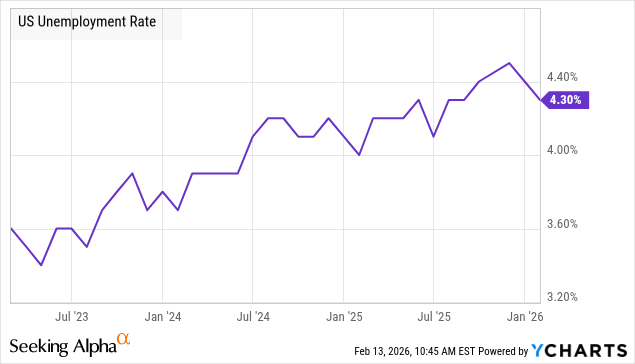

Soft Fundamentals

As we’ve been documenting over the past several years, the fundamentals of the U.S. economy have been getting weaker. Unemployment has been rising steadily for three years:

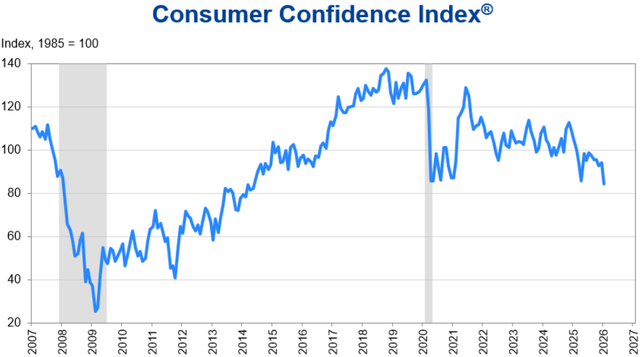

Consumer confidence continues to decline and, as measured by The Conference Board, is at COVID-era lows: Source

The Conference Board

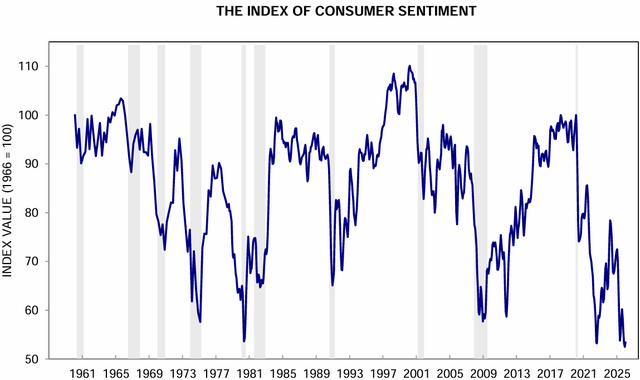

Where the Conference Board reported a sharp drop in January, a similar survey conducted by the UoM (University of Michigan) has a small uptick. However, the UoM survey was already far more bearish, with consumer sentiment near all-time lows: Source

University of Michigan Consumer Sentiment Index 50-Years

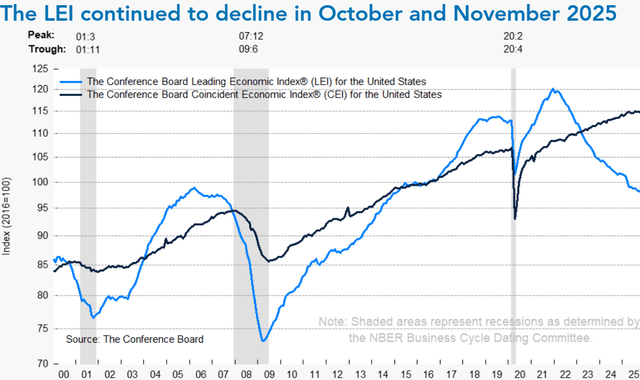

Leading economic indicators continue to decline: Source

The Conference Board

While there are undeniably some hotspots in the economy, like the huge investment being made in data centers, it is one hot sector that is surrounded by a lot of weakness.

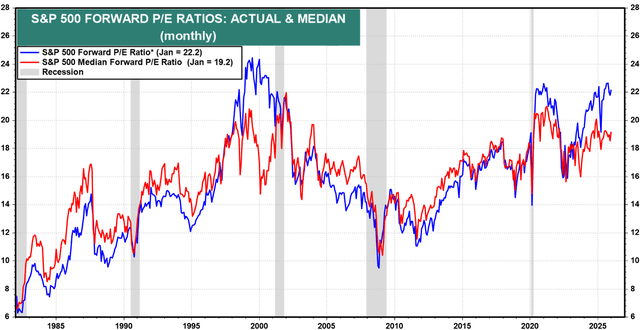

The stock market, on average, is expensive. However, we have seen a diversion that hasn’t occurred since the late 1990s, where the average P/E (price/earnings) ratio of the S&P 500 is materially higher than the median P/E ratio: Source

Yardeni

The median is the company that is in the middle, where 50% of companies in the S&P 500 are trading at higher valuations, and 50% are trading at lower valuations. We discussed the concept of valuation in-depth last month with our members because we believe this is the most important concept in the market today.

Microsoft (MSFT) reported objectively strong results, but the share price declined anyway. We’ve noticed that analysts are asking more questions about the profitability of AI spending rather than just blindly cheering it on. Here is a question that we think exemplifies this concern during the earnings call:

“Keith Weiss Morgan Stanley, Research Division

I’m looking at Microsoft print where earnings is growing 24% year-on-year, which is a spectacular result. Great execution on your part, top line growing well, margins expanding. But I’m looking at after-hours trading and the stock is still down. And I think one of the core issues that is weighing on investors is CapEx is growing faster than we expected and maybe Azure is growing a little bit slower than we expected. And I think that fundamentally comes down to a concern on the ROI on this CapEx spend over time. So I was hoping you guys could help us fill in some of the blanks a little bit in terms of how should we think about capacity expansion and what that can yield in terms of Azure growth going forward. More to the point, how should we think about the ROI on this investment as it comes to fruition?”

In essence, Wall Street is starting to say, “Show me the money!” There isn’t much doubt about the potential for AI and that there will be tons of money to be made, but there are concerns about whether the money will show up in time to justify the trading prices for these stocks. Wall Street is no longer enraptured by the AI arms race; they are starting to ask for tangible results. If they don’t find them, they’ll move on to invest in sectors where tangible results are being realized right now. In a nutshell, that’s exactly what the dot-com bust was all about. It wasn’t that the Internet didn’t have tons of potential; it was about whether that potential was translating into high enough earnings, soon enough, to justify the valuations today. In 2001, the answer was they weren’t.

There are many companies that are trading at low valuations. The strength of the S&P 500 is increasingly relying on a handful of stocks to maintain very high valuations.

What This Means for Income Investors

Let’s put the points we made together:

The market is favoring investments that are perceived as safer.

The public markets are valuing credit risk lower than private markets.

Economic fundamentals are soft, and consumers are struggling.

Some stocks are trading at premium valuations, while others are trading at low valuations.

Putting these together, what does that point to?

Hold Safety

We want to own assets that are perceived as “safe”. Fortunately, we were buying a lot of those in recent years, like mREITs that invest in agency MBS, municipal bond funds, preferred equities, and bonds. We’ve been pounding the table until our hands were bruised about the virtues of fixed-income investments. We continue to believe that these are good investments, even if the prices are higher than they were. These investments are just starting to come back into favor and have some significant upside left to go.

For investors who don’t have a healthy allocation to these investments, there is still time to add them.

Credit Risk Arbitrage Opportunities

For the credit risk portion of our portfolio, there is more opportunity, but also more risk. These investments are trading at lower valuations in the public markets than they can get in the private markets. As a result, the chances of seeing drastic moves like ARI’s decision to sell substantially all of its assets are higher. We could see more of these publicly traded vehicles being taken private or large asset sales from publicly traded companies to private companies to take advantage of the valuation differences. The public companies will be exploring ways to unlock that value, which could create significant upside for public shareholders.

On the risk side, with investor enthusiasm low, prices are likely to remain under pressure. This will be accelerated to the extent that management teams reduce dividends in response to lower interest rates on floating-rate investments or as a strategy to retain capital to make new investments. We expect dividends for BDCs to generally drift downward toward 2021 levels, and CLO equity funds have become a wildcard with a big unknown on whether other funds will follow OXLC’s example and position themselves to have a profile of growing NAV and paying lower dividends or if they will continue to pay out substantially all their cash flow at the expense of NAV.

We believe that long-term credit risk is trading at attractive valuations in the public markets. We believe that the institutions are right, and the risk of defaults is relatively low. But sentiment is negative, and it could become more negative as the year goes on.

Be Aware of the Consumer

When making an investment, we should be aware of whether our dividends are dependent upon a strong consumer. Dividends that stem from areas of relatively inelastic demand should be favored over dividends from sectors that are very elastic.

The Wendy’s Company (WEN) is trading at a 7% yield, but it’s a company that is quite dependent upon consumers being willing to pay for convenience. We expect another dividend cut to be very likely, so we will avoid it.

No doubt, we will see many consumer-centric businesses with yields that tip into our territory. We will exercise caution when choosing whether or not to take advantage of those “deals” because we recognize that the consumer is weak. We would rather own the landlord who rents properties to WEN because WEN is good for the rent even after they cut the dividend. O’s 5% yield > WEN’s 7%.

Be Aware of Valuations

When the market has been generally bullish for an extended period, there is often a tendency for investors to start dismissing the concept of valuation as irrelevant. It is true that buying something cheap doesn’t mean that you’ll make a lot of money right away. It doesn’t mean that the price won’t go lower for an extended period of time. However, in the long run, only two prices matter when calculating your total return: the price you pay and the price you sell at.

Prices bounce all over the place. Valuations go high, they dip low, and they will go to both extremes much further than any amount of staring at numbers can justify. We remember in 2021 when some preferred shares were trading at such high premiums to par that they had a negative yield-to-call, and people were buying preferred equity where the inevitable return was a guaranteed loss. There have been cases of bonds trading at negative yields to maturity.

If that kind of inaccurate pricing can occur in fixed income, where the amount of the interest/dividends is known to the penny, and you can calculate with a pencil and paper the best possible return that you can have by the call date or maturity date, and investors are still buying tickers that are guaranteed to have negative returns—how far off can the market be when the future returns are at best educated guesses that are open to debate? It can be off by a lot, and it can be off for a long time

Eventually, the chickens come home to roost, and the market comes around to recognize the earnings that it previously undervalued, or the earnings fail to materialize, and the price comes down to a level reflecting that. The thing is that there is always a future, so while the market will cross that “fair value” line, it will usually keep going until the extreme is in the opposite direction.

When a stock in your portfolio is up or down a lot, make sure you take the time to understand how much of that price difference is due to an actual change in earnings and how much is due to a change in valuation. You want to buy at a low valuation and consider selling when investments are trading at a high valuation.

Conclusion

It is a stock-pickers’ market where there are some investments that are simply too expensive to be reasonable investments, some investments that are more expensive but still have a good long-term return profile, and some investments that are absolute bargains.

This is true for dividend investors as much as it is for everyone else. In our portfolio, we have a base with the relative safety of assets like agency MBS, fixed income, and bonds. For several years, this portion of our portfolio actually saw the lowest valuations. That is changing, although there are still opportunities that are attractive long-term.

To that base, we add investments in holdings and sectors that carry more risk but are trading at low valuations. Today, credit risk is a good place to look for investments that are trading at low valuations and paying very high yields.

We will focus on sectors that aren’t dependent on a strong economy. Sectors supported by tangible assets and inelastic consumer demand. Real estate, utilities, infrastructure, and more.

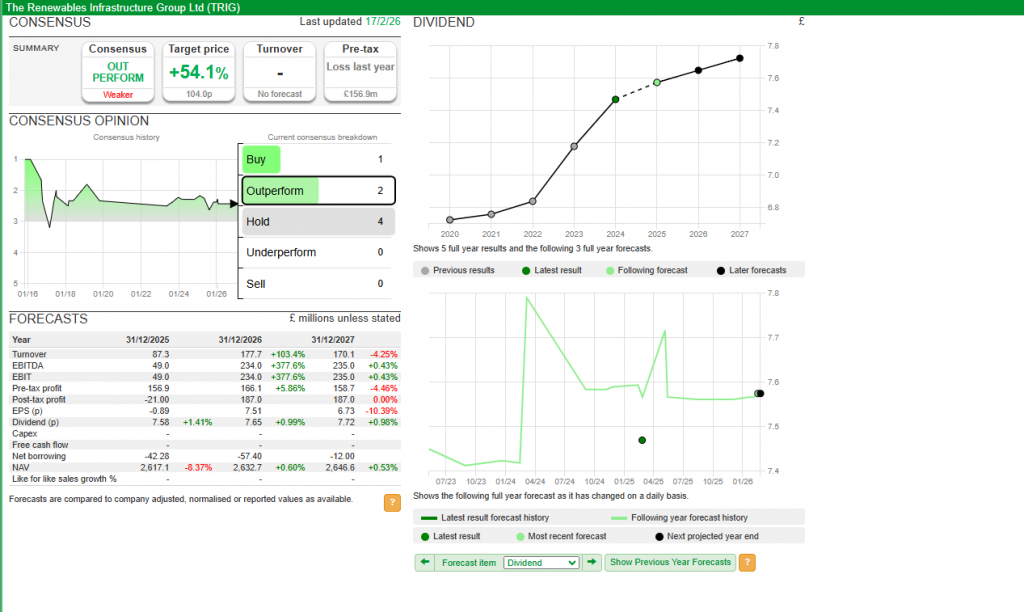

TRIG NAV falls on weaker power price outlook and higher offshore wind discount rates; shares slip

Fiona Craig

LSE:TRIG

Market News

16 February 2026

The Renewables Infrastructure Group (LSE:TRIG) posted a larger-than-anticipated quarterly decline in net asset value, as softer power price assumptions and higher discount rates for UK offshore wind assets weighed on valuations, pushing the stock 2% lower on Monday.

The renewable energy investment trust reported that NAV decreased 5.2% to 104 pence per share in the fourth quarter, down 5.7 pence from 109.7 pence at the end of September. The move translated into a negative total NAV return of 3.7% for full-year 2025.

Management attributed the decline primarily to a 1.8 pence per share reduction linked to lower consultant power price forecast curves, alongside a 1.2 pence impact from a 50 basis point rise in discount rates applied to UK offshore wind projects. A further 1.8 pence per share drag stemmed from generation coming in below budget and operational challenges.

An additional 0.6 pence per share reduction reflected changes to indexation of UK Renewables Obligation Certificates (ROCs), which will now be tied to the Consumer Price Index rather than the previous benchmark.

Electricity generation was 5% below budget during the fourth quarter, largely due to economic and grid curtailment in Sweden. However, this marked an improvement compared with the first half of 2025, when output fell 10% short of plan. Sweden accounts for roughly 14% of TRIG’s portfolio by NAV and has persistently underperformed expectations, analysts said.

“While generation missed budget by 5% in Q4, this is an improvement versus the performance earlier in the year,” said Joseph Pepper, analyst at RBC Capital Markets, which maintains an “outperform” rating on the stock with a 90 pence price target.

“We think management’s target future cover of 1.1-1.2x looks credible given inflation-linked cash flows and an improving debt amortisation profile, although we note that Sweden remains a consistently underperforming geography in the portfolio.”

TRIG reiterated its dividend target for fiscal 2026 at 7.55 pence per share, unchanged year-on-year. Net dividend cover for fiscal 2025 was reported at 1.0 times. On a gross basis, excluding annual amortising debt repayments, dividend cover stood at 2.1 times. Management continues to guide toward net dividend cover of 1.1 to 1.2 times over the medium term.

The company had previously cautioned that dividend cover would be “tight” for fiscal 2025.

Shares closed Friday at 69.20 pence, implying a discount of about 34% to the newly reported NAV, broadly aligned with the peer group average discount of around 35%.

“Given the quantum of the quarterly movement this morning we would expect shares to trade lower today,” Pepper said.

TRIG’s portfolio includes approximately 90 renewable energy assets across six countries, with about half of its exposure in the UK, leaving it sensitive to domestic regulatory developments and wholesale power price trends. The trust primarily invests in operational wind and solar projects, with UK offshore wind forming a substantial component of its holdings.

It is your duty to check the announced current dividends and any future dividends for the shares in your Snowball.

Two 9% Dividends on Sale (Up to 17% Off). Thank the Software Selloff.

Michael Foster, Investment Strategist Updated: February 16, 2026

The recent plunge in software stocks is another reminder that AI is rattling through the economy, setting off rapid change and disruption wherever it goes.

Investors sold software stocks on fears that new AI tools will make it easier for individuals to create their own apps, potentially taking business from software developers.

This is a big change—and here’s some news that might surprise you: For income investors, it sets up another way to tap AI’s growth for dividends. We welcome that; in the early days of AI, the only real ways to get in were through low- (or no-) payers like NVIDIA (NVDA).

Just last July, research had shown that software developers actually coded more slowly when using AI tools. Now that Claude Code and updated versions of Codex from ChatGPT are rolling out—and OpenAI is promising more tools for developers soon—software is turning into something users make for themselves, rather than buy from someone else.

Investors’ focus, as a result of this development, has been on software companies, specifically how vulnerable their businesses really are to this shift. But we’re not going to focus on that today. We’re more interested in the productivity gains these new tools will unleash—and exactly what impact they’ll have on our dividends.

Productivity in Overdrive

The bottom line here is that if everyone can create software, it will result in a consumer surplus that will support the economy. That could come in the form of consumers and companies saving money on software subscriptions; building their own, personalized tools; or requiring fewer developers.

This is a compelling story for investors, and it’s another in a long line of AI innovations behind the S&P 500’s 16% gain over the last year, ahead of its 10.5% average annual return. I see above-average stock performance continuing as these new tools boost productivity and free up more cash for other spending.

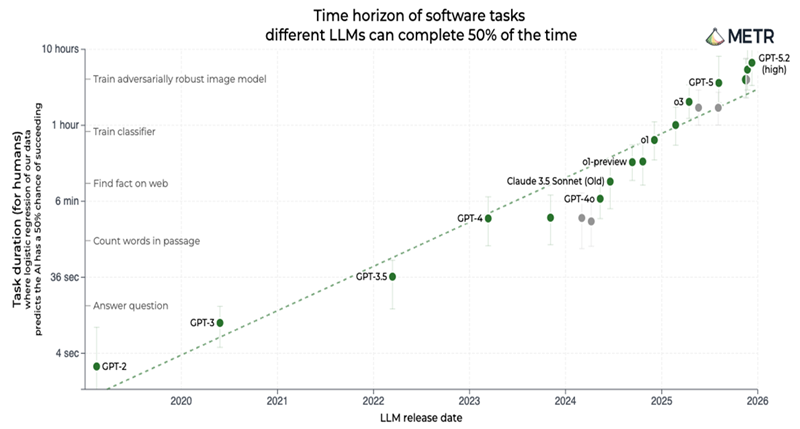

But let’s pause for a moment and try to come to grips with exactly how much of a productivity boost we can expect here.

This is a pretty popular (and controversial) chart in the AI world. It tracks how long of a task an AI model can successfully perform. Right now, it shows that our third-best model can perform a task that would normally require 6.6 hours of human labor.

Our best models haven’t been tested yet because they were literally released in the last couple of weeks (things are happening that quickly!).

So while we do not know how much better our best models are, we do know that they are better. Time will tell. But what this really signals is that we’re past the debate of whether AI makes engineers more productive. We’re now debating how much more productive it will make them.

What’s the Dividend Play Here?

Those who hear “AI” and think “buy NVIDIA” are behind the curve (and not only due to the stock’s lame 0.02% yield!).

That said, we want to keep buying tech, even after the sector’s run-up in the last few years, but we want to focus on other sectors primed to benefit from AI’s strong potential, too: Utilities, for example, are well-known plays on AI’s soaring energy use, and data-center demand is likely to help real estate investment trusts (REITs).

Such a broad-based bullish story is best for income investors who are broadly invested in the market and have strong income to tide them over during micro-panics like the one that hit software stocks.

That’s why, rather than try to pick individual stocks, we look to CEFs that benefit from rising productivity across the economy.

This 9.3% Dividend Is a Smart Play on a More Productive Economy

There are a lot of high-yielding closed-end funds (CEFs) that fit that bill. One of my favorites is the Liberty All-Star Growth Fund (ASG). This fund, a holding of my CEF Insider service, yields 9.3% as I write this.

ASG isn’t exclusively a tech fund, as it holds a basket of other stocks of all sizes, including property manager FirstService (FSV) and Pennsylvania-based Ollie’s Bargain Outlet Holdings (OLLI). But it does hold NVIDIA, alongside other blue chip tech stocks like Alphabet (GOOGL), Amazon.com (AMZN), Microsoft (MSFT), Apple (AAPL) and Meta Platforms (META).

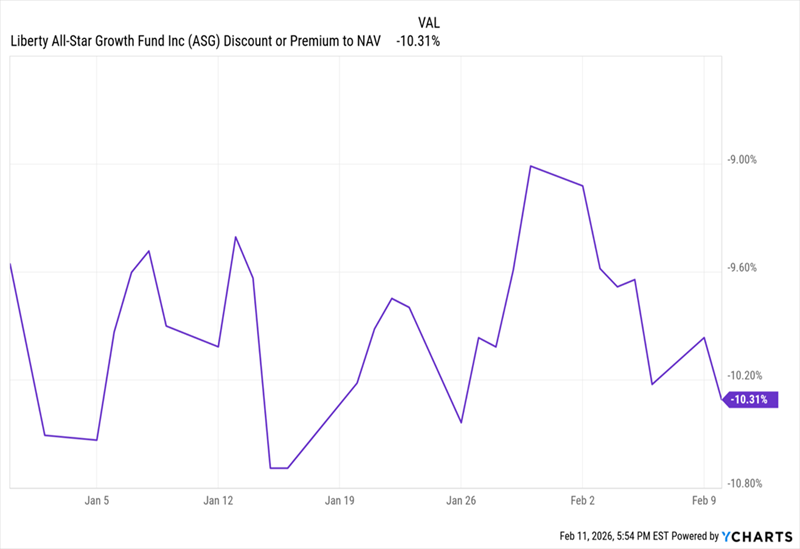

Crucially, ASG also sports a wide discount to net asset value (NAV, or the value of its underlying portfolio). That’s because conservative income investors, in response to the pullback in software stocks, have oversold this growth-oriented fund.

ASG’s “Discount Dip” Serves Up a Solid Entry Point

The result is that we can buy ASG’s diverse portfolio for around 90 cents on the dollar.

We also like ASG for its dividend policy, as it ties its payout to the performance of its portfolio. So the better the fund’s portfolio performs, the faster the payout grows—a sweet setup in an economy getting a nice productivity boost.

A Deep-Discounted 9.6% Payer for Aggressive Investors

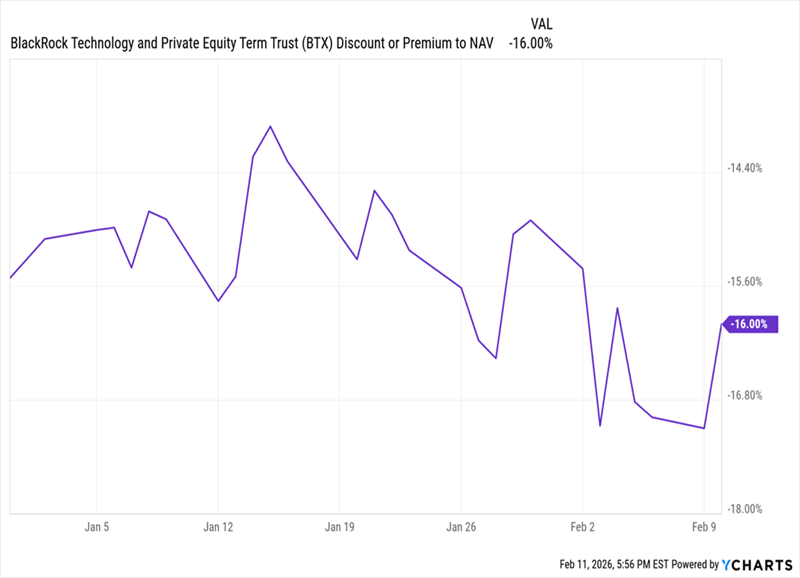

Another, more speculative option is the 9.6%-yielding BlackRock Technology and Private Equity Term Trust (BTX). As the name says, it has a wide variety of high-tech companies both public and private, such as NVIDIA (NVDA), quantum-computing firm PsiQuantum, Fabrinet (FN), whose technology helps manufacturing firms improve their processes, and AI infrastructure firm Celestica (CLS).

Gains from these stocks have helped shore up the fund’s dividend, so we’re looking at more income security in the near term.

And since most CEF investors are more conservative—and thus more easily spooked by negative headlines—this fund’s discount tends to fluctuate more widely than that of the more broad-based ASG. The recent software selloff has pushed it deeper into bargain territory.

Oversold BTX Trades for 84 Cents on the Dollar

Let me leave you with the idea that there are hundreds of CEFs that are well-positioned to profit from this revolution in automation. That shift is not being priced in because markets are moving too slowly to keep up with AI. That gives us a rare opportunity to buy high-yielding funds like these, whose discounts are unusually wide in relation to their history.

My 5 Top Monthly Dividend CEFs Pay Out 60 Times a Year (and Yield 9.3%, Too)

These two are just the start. Truth is, equity CEFs focused on rising productivity are at the very heart of my “60 Paycheck Dividend Plan.”

As the name suggests, the 5 CEFs that make up this “plan” each pay dividends monthly. That’s 5 dividend payouts a month, or 60 every year! They throw off a rich 9.3% average dividend between them, too.

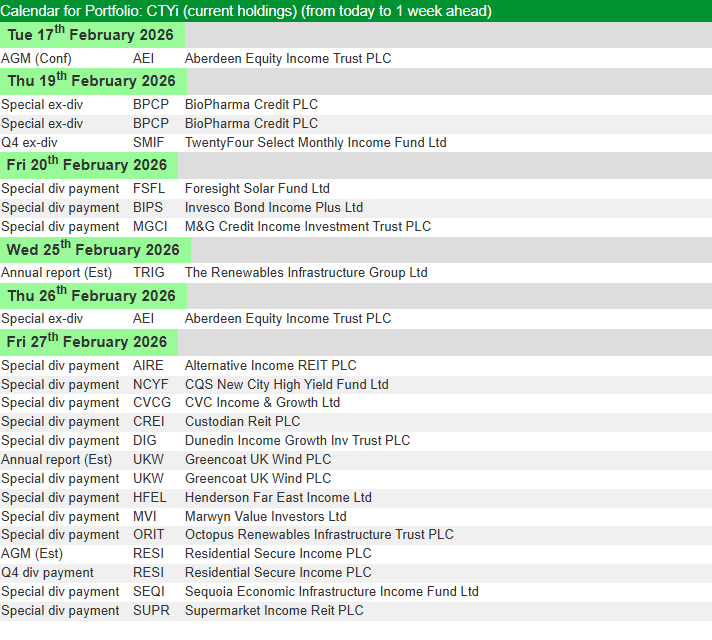

BioPharma Credit PLC ex-dividend date Greencoat Renewables PLC ex-dividend date Impax Asset Management Group PLC ex-dividend date Mountview Estates PLC ex-dividend date Shires Income PLC ex-dividend date

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

Even with the UK stock market reaching new record highs lately, there are still plenty of FTSE shares offering generous dividend yields. And if these payouts can be maintained, investors could go on to earn an absurd amount of passive income.

That’s what’s brought Greencoat UK Wind (LSE:UKW) back in my sights. Renewable energy stocks continue to be unpopular in 2026. But new evidence is emerging that Greencoat shares could be a phenomenal long-term opportunity. And if that’s the case, its 10.6% payout could pave the way to exceptionally lucrative results.

So, is now the right time to go against the crowd and aim to earn a massive passive income?

Why is the yield so high?

Despite hiking its dividend by more than 130% since its IPO, Greencoat’s double-digit dividend yield stems from a painful fall in Greencoat’s share price.

Down around 35% since the start of 2023, the shares now trade at a 26.6% discount to net asset value (NAV). And to be fair, there are some valid concerns to justify this large discount.

In April this year, the Renewable Obligations (RO) scheme will be switching its inflation index from the retail price index (RPI) to the consumer price index (CPI). While CPI is a generally more accurate measure, it’s also often 1% to 2% lower than RPI, resulting in a significant reduction in long-term subsidy revenue for green energy generators.

At the same time, with more energy capacity being added to the national grid, long-term power price forecasts have been steadily dropping, placing further pressure on Greencoat’s projected cash flow. Combining all that with some fairly weak wind speeds over the last few years, it’s not surprising to see investor sentiment sour.

A hidden buying opportunity?

Despite some valid criticisms, investor pessimism looks like it could be overblown.

The near-30% discount to NAV doesn’t align with what’s happening in the private markets. The fact that Greencoat’s recent asset sales have occurred at NAV is evidence of that. And it shows there is a real disconnect between perceived value and actual value.

This valuation gap is something management has already been taking advantage of. By systematically buying its own stock at a substantial discount, not only is the firm boosting the NAV per share, but it’s also opening the door to a higher dividend per share simultaneously.

What’s more, policy uncertainty surrounding the RO scheme is now resolved. Meanwhile, looking at the group’s performance in the final quarter of 2025, even wind speeds have also started picking up again, with energy generation coming in just 1.6% below budget versus 14% across the first half of the year.

So, where does that leave investors?

Fluctuations in wind speeds remain a persistent threat. And prolonged periods of calm weather could be catastrophic for Greencoat, particularly given its fairly leveraged balance sheet.

However, with the share price barely moving despite substantial policy uncertainty being removed from the equation, it’s hard not to be tempted by the double-digit yield. Even more so, given that dividends are still entirely covered by cash flow.

So, with a favourable risk-to-reward ratio, Greencoat shares could be worth mulling over. But it’s not the only high-yield opportunity on my radar today.