As the children across Britain sharpen their pencils and go back to school, there are some financial lessons that their parents can learn too.

We asked Britain’s foremost investment managers to share the most important ones they’ve learnt – and how they’ve put them into practice.

What are the most important investment lessons? We ask the experts

by This Is Money

Lesson One: Too much debt just makes companies vulnerable

Early mistakes have led to caution for Richard de Lisle, who manages the VT De Lisle America Fund. He began his investment journey at just 16, only to lose his hard-earned pocket money on a risky bet.

‘I read everything on my paper rounds and did well from Patrick Sergeant in the Daily Mail and Jim Slater in The Telegraph. Those were my favourites. Yes, the Mail had a hand in my career.

‘The FT 30 had fallen more than half in two years. Stock prices were so low that I was seduced by the glamorous Court Line [a former shipping company that became a holiday provider]. It was leading the new package holiday boom, opening up the Spanish Costas to people who’d never been abroad before.’

Despite his tender years, De Lisle even looked at the valuation, including the price-earnings ratio, which shows how much profit a company is making per share. As a rule of thumb, the lower the ratio, the cheaper the company.

‘Its P/E ratio was under four; the yield was 17 per cent. What could go wrong?’ De Lisle asks.

Quite a lot, it turns out.

‘Warren Buffett says that debt just speeds things up and so it does. Today we run a value-based fund. While we like cheap, we don’t like debt. Lesson learned.’

Lesson Two: You’re almost always wrong before you are right

For Laurence Hulse, who manages UK smaller companies’ specialist Onward Opportunities, an internship at Barclays Capital when he was 18 brought a lesson he has lived by all his life.

‘You’re almost always wrong before you are right. This was one of the first ‘lessons’ I was ever taught,’ Hulse says. During his time at Barclays under revered equity trader Howard Spooner, Hulse learned that because you do not usually time the market perfectly, your investment is likely to fall at first.

‘Other than in the unlikely event when you buy at the very lowest price or sell at the very highest price to the penny, you have got to be prepared to be wrong initially,’ Hulse says.

As a result of this lesson, he has learned not to make sudden swerves in his trading. ‘We very rarely trade into or out of a company in one transaction, as to do so would be to assume you have timed things perfectly.’

Lesson Three: Work out whether you are investing…or gambling

John Husselbee, head of multi-asset at LionTrust, learned many of his investment lessons from his family.

‘My father taught me that whenever speculating at the racecourse or a casino, work out beforehand how much money you are prepared to lose betting, then put that amount in a separate pocket to treat as a sunk cost. Whatever is left in that pocket at the end of the day is your good fortune. However, if you have bad luck and your pocket is empty, never add to it – just walk away,’ he says.

From his grandfather, who bet on the horses as well as investing in shares, he learned the difference between investing and gambling.

‘Visiting my grandad on a Saturday morning, we would walk to the newsagent to buy a copy of the FT and the Racing Post. Back home, I would update the prices of Grandad’s shares in his ledger and calculate the profit/loss since purchase.

‘In the meantime, Grandad would study the form to select his bets for afternoon racing live on the telly. We would walk back to the newsagent; Grandad would give me pocket money for sweets and I would wait outside the bookies while he would place his bets.

‘The lesson learnt was the difference between investment and speculation – with the latter you need to be prepared to lose all your money!’

Lesson Four: It’s always darkest just before dawn

For a lesson he has never forgotten, Ian Lance, fund manager in the UK Value & Income team at Redwheel, casts his mind back to a despondent lunch in City of London oyster bar Sweetings, just as Britain was about to crash out of the European Exchange Rate Mechanism (ERM) in September 1992.

‘I calculated the payments on the mortgage my wife and I had taken out to buy our first home a few months earlier at the new interest rate of 12 per cent which the Government had just announced.

‘On finding that our payments were more than our combined salaries and the UK equity market was crashing, I headed down to Sweetings to drown my sorrows.

‘An hour or so later a colleague turned up and announced the stock market was soaring. The rest is history as Britain crashed out of the ERM, interest rates plummeted, and a new equity bull market began.’

What did he learn from this – apart from to take a long lunch now and then? ‘Markets look forward and will peer through the gloom to the sunlit uplands,’ he says. When all about you are despondent, it might be time for things to recover.

Lesson Five: You don’t know as much as you think you know

Jamie Ross, portfolio manager of Henderson Eurotrust, says that the facts available at our fingertips leave us more vulnerable than we know. The biggest lesson of his career, he says, has been that he always needs to focus on one important question when deciding whether to invest or not.

That question is: ‘What makes this a good company?’

‘It leads to all sorts of analysis, from understanding the competitive environment, to assessing pricing power to attempting to determine the sustainability of a company’s margins.’

Without this simple question, he says, it is easy to drown in information about a potential investment and to think you know everything about it.

‘Knowledge is not the same thing as understanding. Even experienced investors can sometimes miss the wood for the trees and suffer from familiarity bias – feeling more comfortable investing in something you ‘know’ lots about.

‘I think about this every time I start to work on a potential new investment.’

Lesson Six: Take the expert advice with a pinch of salt…

Edward Allen, investment director at Tyndall Private Clients, says that for all investment experts’ perceived wisdom they are ‘rarely cynical enough’, so you should never believe what you read from those who don’t have anything to lose from their predictions.

‘Economists and market forecasters have the luxury of being wrong. Investors do not,’ he points out.

‘Understand the biases of an author if you are going to follow their advice and remember that for every balanced, well-reasoned argument for doing something there will be many others for doing the opposite.

‘The investment world is perverse and often seemingly irrational.’

Buffett’s net worth went from approximately $30m to $100m from age 40 to 50. Over the span of the decade a lot happened.

Via his company Berkshire Hathaway, he spent the years buying stock and sizeable shareholdings in several firms that yielded good results. One key point here is that some stocks he bought in the 1970’s are still owned by him today!

An example is GEICO, the insurance company. Buffett invested $4m in the business back in 1976. He kept increasing his shareholding in the firm until 1996, eventually taking over the entire company. In his 40’s, the value of the business increased. Incredibly, the business is still adding to Buffett’s profits today. In the May Q1 report, it reported $703m in earnings.

The point here is that in order for me to generate serious wealth over time, I need to have the right investing mindset. I can often miss out on big returns from stocks by cutting my winners too early and holding my losing ideas for too long. Buying and holding might seem boring, but it’s often the way to gain high profits.

Getting advice from the best

Aged 45, Buffett decided to merge his business with Charlie Munger back in 1976. Munger is another very shrewd investor and has been his right hand man ever since. The advice and help that Munger has proved to be invaluable along the way.

For example, relating to the first point, Munger is quoted as saying that “the big money is not in the buying and selling, but in the waiting.” No doubt he helped Buffett to be patient along the way.

Today, I feel that my chances of increasing my net worth via stocks will be massively helped in listening to other smart investors. The more information I can tap into, the more informed I can be. This relates to specific stock research and also with more general investment advice.

The current plan by re-investing all earned dividends is to have final dividend pension of 14k – 16k, it could be higher but let’s work with 16k.

Based on seed capital of 100k with no further cash added to fuel the fire.

The total pot with another 9 years dividends added should be over 200k but as that’s the unknown, let’s work with 200k.

Under current tax laws, u could withdraw 25% tax free, either for a new car or if u need the income to live on re-invested in a ISA, replicating the Trusts sold or higher yielding Trusts.

(U need to make an allowance for inflation but most of the Trusts will gently increase their dividends).

The dividend take from your pension would reduce by 25%, 4k.

12k of dividends pa, of which u could withdraw using a further 25% relief of tax, as long as current tax law remains the same and your dividend stream remains similar.

One problem for the blog is that the last Labour government taxed dividends inside a pension and may do so again, as it raises a lot of cash (to waste) for no effort and are likely to do so again.

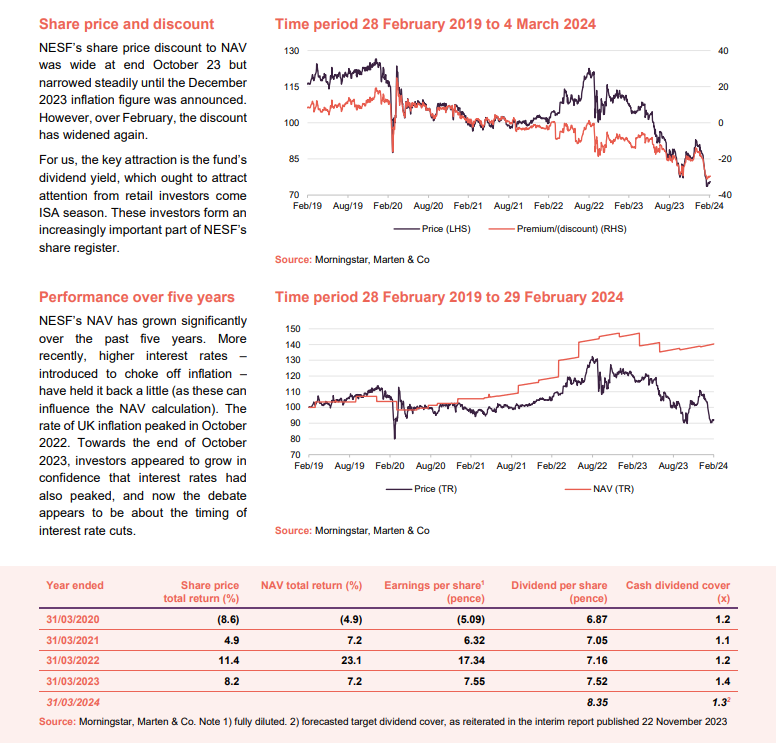

NextEnergy Solar Fund (NESF) is almost 10 years old. Since launch, it has built a £1.2bn, 933MW portfolio of 100 operating solar assets, powering the equivalent of over 330,000 homes, declared dividends totalling £333m, and avoided the emission of about 2.2 Mt CO2e.

NESF is on track to pay 8.35p in dividends, with forecast dividend cover of about 1.3x. Share price weakness that has afflicted the whole sector means that dividend translates to a dividend yield of 11.1%, one of the highest in its sector, and the share price’s near 30% discount to net asset value (NAV) provides the prospect of attractive capital appreciation when sentiment towards the sector recovers.

Interest rates look to have peaked, which is improving sentiment, but there is further to go. We find it hard to comprehend why any stock with a nine-year track record of growing covered dividends in line with inflation would not trade on a much lower dividend yield.

NESF also has one of the largest capital recycling programmes of its peer group, which is aimed at freeing up cash to slash debt, and fund share buybacks and existing and potential construction projects. Those projects should be both NAV- and earnings-enhancing. A re-rating of NESF’s shares is overdue.

Income from solar-focused portfolio

NESF aims to provide its shareholders with attractive risk-adjusted returns, principally in the form of regular dividends, by investing in a diversified portfolio of primarily UK-based solar energy infrastructure and complementary energy storage assets.

At a glance

10th birthday imminent

NESF’s long-term success reflects the strength and depth of the adviser’s business

NESF is just a few weeks off the 10th anniversary of its launch. The company got off to a flying start, helped by its ability to secure access to a portfolio of projects being developed by NextEnergy Capital’s development arm (now called Starlight) and engaging NextEnergy Capital’s experienced operational asset manager, WiseEnergy, to keep the portfolio operating smoothly. The capital that it raised was deployed swiftly and was soon generating income to cover the dividend.

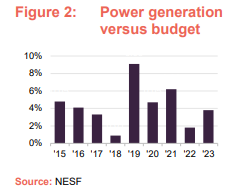

This year’s dividend target is 11% ahead of last year’s

NESF’s board maintains a progressive annual dividend policy, and in line with that the trust has grown its dividend each year since launch. Since its 2016 financial year, NESF’s dividends have always been covered by cash generated from its portfolio. NESF is targeting an 8.35p dividend for its financial year ended 31 March 2024 (FY24) that is 1.3x covered by cash flow. The target was an 11% increase on the total dividend for FY23.

With the share price where it is, that 8.35p translates to a dividend yield of 11.1%. That seems perverse given the dividend growth track record, the cash flow cover, and the relatively predictable nature of NESF’s cash flows.

Keeping the cash flowing

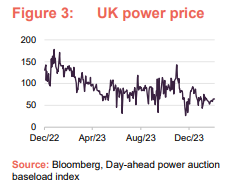

Since launch, NESF has built a good track record of generating more power than budgeted. In part, that reflects a pattern of sunnier weather in the UK in recent years. However, WiseEnergy’s work to keep plants up and running plays a big part in this too. It is responsible for 1,500 solar and battery assets with an installed capacity in excess of 2.5GW, in nine countries.

At 30 September 2023, around half of NESF’s revenues were coming from inflation-linked, government-backed subsidies, and these had a weighted average life of 11.4 years. In addition, as at 31 December 2023, NESF had pre-sold 98% of its FY24 generation at an average price of £79.2/MWh, 74% of FY25’s generation at £84/MWh, and 29% of FY26’s at £101.2/MWh.

Power prices have been volatile but remain well above pre-COVID averages. NESF’s power price forecasts (which combine prices for the pre-sold power with forecasts from three independent energy market consultants) were adjusted at end December to reflect a decrease in short-term (2023-2027) UK power price forecasts provided by the consultants, mainly as a result of lower gas price futures (the pric of gas tends to set the marginal cost of electricity as the grid is reliant on gas peaking plant to balance power demands), influenced by above-average gas storage levels and milder weather across winter 23/24.

Adding value with new investments

Roughly £500m pipeline of new solar projects and battery storage projects

At end December 2023, NESF had identified a pipeline of new solar projects and battery storage projects totalling about £500m. Assets under construction tend to be written up in value once the associated construction risks have passed and they become operational. In addition, the extra revenue that they generate contributes to NESF’s cash flows. Starlight, the development arm of the wider NextEnergy group and an important source of potential investments for NESF, has 8.3GW of projects under development across five markets, underpinning NESF’s long-term investment pipeline.

We described in our December 2022 note how NESF was partnering with battery storage specialist Eelpower to build on the opportunity in that area. At that time, NESF’s first standalone battery project was under construction and the advisers were looking at the potential for co-locating batteries at NESF’s then 99 operating solar sites. There has been some welcome progress since then.

Portfolio

100th operational solar asset

NESF energised its 100th operating solar asset in the summer of 2023. Whitecross is a 36MW solar fam in Lincolnshire. It is contracted to sell power through a CFD that it successfully bid for in the government’s fourth auction round that concluded in 2022. Whitecross is one of the five subsidy-free assets that NESF decided to put up for sale in its capital recycling programme – see below.

Camilla battery project nearing completion

On the energy storage front, NESF is on track to energise its first (and – the manager notes – outside of the battery storage specialists, the peer group’s first) standalone battery project, Camilla, a 50MW project in Fife, Scotland shortly. Camilla is expected to offer high single-digit returns. It will benefit from some grid-related revenues, including £202k of contracted revenue for the period 1

October 2024 through to the end of September 2025, secured through the National Grid ESO;’s latest T-1 capacity auction. However, the bulk of its earnings will come from arbitraging fluctuations in power prices. NESF also has a 6MW storage project under construction that is co-located with its North Norfolk solar farm.

In addition, planning applications are underway for a number of other co-location projects, and NESF has a 250MW pre-construction battery-storage project in the East of England (near the Walpole substation that handles inbound power from three offshore wind farms) that NESF bought in October 2022. The project will be developed in a joint venture with Eelpower, with a target energisation date in 2025.

NESF’s £50m stake in the NextPower III ESG fund (NPIII) gives it exposure to a 1.9GW globally diversified portfolio of 173 solar assets. That fund committed the last of its capital in the final quarter of 2023, including deals to add a 140MW portfolio in Italy and a 55MW portfolio in Spain. NESF has two co-investments that it has made alongside NPIII that are due to come online in the first half of 2024 (these were on a no fee, no carry basis alongside other institutional investors); Agenor (50MW in Spain – NESF owns 24.5%) & Santerem (210MW in Portugal – NESF owns about 13%).

Capital recycling programme

Our last note, published in July 2023, focused on NESF’s plan to recycle capital from its portfolio of subsidy-free solar assets, with the proceeds of disposals used to reduce borrowings and fund a potential share buyback.

Hatherden disposal is a welcome first step in capital recycling programme

As a first step towards this, the company has sold its ready-to-build Hatherden solar farm project for £15.2m (twice what NESF was valuing it at in its NAV calculation). The disposal added 1.27p to the NAV. The proceeds were used to reduce the outstanding balance on NESF’s revolving credit facility (RCF), which was £177m before the disposal. The big uplift reflects the work that the adviser’s team had been doing to enhance the project, including upscaling it from 50MW to 60MW, securing permission for a 7MW co-located energy storage project, and securing a CfD to sell the power produced along the same lines as for Whitecross. It would be wrong to expect similar uplifts for the other four assets, all of which are already operational.

The capital recycling programme is ongoing. The managers say there is interest from multiple parties and expect that the programme will be completed in two further phases (each comprising two assets).

Gearing

Paying down floating rate debt

As at end December 2023, NESF had £163.8m of long-term debt at fixed rates.

The RCFs provided by Banco Santander (£70m) and NatWest (£135m) mature in June 2024. The interest rate on these is at 1.60% and 1.20% over SONIA respectively. The board says it expects the RCF to be refinanced on terms similar to the existing facilities.

The weighted average interest rate on NESF’s debt was 3.9% at end December 2023. In addition, NESF has £200m of long-term preference share finance at a fixed cost of 4.75%. This is an attractive source of finance in the current environment, when costs of capital have risen considerably, and the managers believe that they are a great form of non-amortising debt.

Following the Hatherden disposal, there was a £41.2m undrawn balance on the Banco Santander facility at end December 2023.

Sustainability and biodiversity

As a reminder, NESF is an Article 9 fund under EU SFDR and Taxonomy. At end September 2023, its renewable generation had avoided the production of 2,181ktCO2e since IPO. If the UK is to meet its net zero greenhouse gas emission targets, much more needs to be done and NESF is keen to play its part in this.

NESF is keen to highlight its commitment to biodiversity and has commissioned a new report on this, which should be published soon.

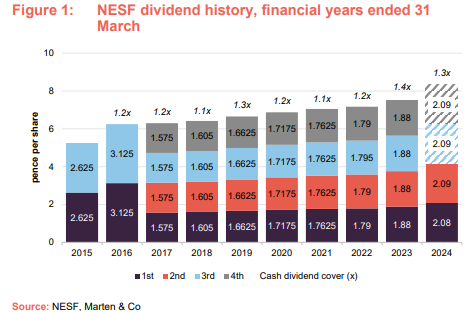

Performance

The end-December NAV fell to 107.7p from 114.3p on 31 March 2023. The main negative drivers of this were higher discount rates used to value the portfolio, and lower forecasted power prices. Offsetting this was an upward move in short-term inflation forecasts and a 1.3p uplift on the sale of Hatherden.

NAV fall driven by higher discount rate, but interest rates look to have peaked

On 17 August 2023, NESF said that it had increased the discount rate for operating UK solar assets with no associated debt by 0.75% to 7.50%. This reflected the higher-interest-rate environment. The weighted average discount rate on the portfolio is now 8.0%. The rate of UK inflation peaked in October 2022 and, barring a small wobble in December 2023, has been declining steadily since, although it remains above target. Towards the end of October 2023, investors appeared to grow in confidence that interest rates had also peaked, and now the debate appears to be about the timing of interest rate cuts.

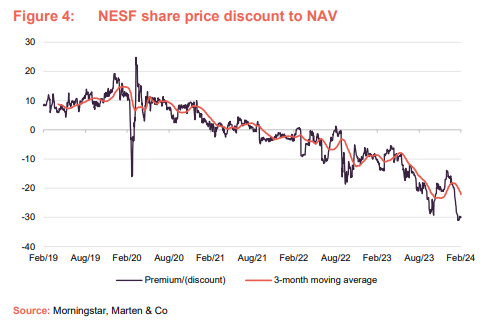

Share price discount

The impact of the shifting sentiment on UK interest rates is obvious in Figure 4. NESF’s share price discount to NAV was particularly wide at end October 23 and narrowed steadily until the disappointing December 2023 inflation figure was announced. However, over February, the discount has widened again. For us, the key attraction of NESF’s shares is the dividend yield, which ought to attract attention from retail investors come ISA season. These investors form an increasingly important part of NESF’s share register.

Discount had been narrowing, yield attraction should help that continue

We are also hopeful that the cost disclosure issues that have plagued the sector and led to selling by professional investors will soon be rectified – you can read more about this on our website.

Board

Kevin Lyon stepped down as chair of the company and as a director on 20 July 2023, and was succeeded by Helen Mahy. On 3 October 2023, NESF said that Paul Le Page would join its board as a non-executive director. He succeeded Vic Holmes as the company’s senior independent director on 1 January 2024 when Vic retired from the board.

Paul is a non-executive director of RTW Biotech Opportunities Fund Limited, TwentyFour Income Fund Limited, and Highbridge Tactical Credit Fund Limited. He stepped down as director and chair of the Audit and Risk Committee of Bluefield Solar Income Fund Limited at the end of September 2023.

On 12 December 2023, NESF announced that a new non-executive director, Caroline Chan, had been recruited. She will take up the role with effect from 1 April 2024. Caroline was a corporate lawyer for over 30 years, working across London, Hong Kong, and Guernsey, where she specialised in investment funds, mergers and acquisitions, financing, and financial services regulatory work. She served previously as a non-executive director of Round Hill Music Royalty Fund Limited and currently serves as a non-executive director of BH Macro Limited.

Source: Marten & Co

IMPORTANT INFORMATION

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on NextEnergy Solar Fund Limited.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

I’ve bought back for the portfolio 6471 shares in FSFL for 6k.

Yielding 7.2% with a better dividend cover ratio than BSIF of 3.5.

This gives the portfolio 4 Trusts to add dividends to as they are received and also any funds received from the Trusts currently with corporate actions.

AEI

AGR

FSFL

PHP

Current cash for re-investment £250.00

Current amount invested in the market £111,626.00* after the deduction of the loss from BSIF

Albert Einstein is often credited with describing compound interest as the eighth wonder of the world.

But even though nobody has any credible evidence of this, I’m not really bothered. That’s because I’m convinced of its merits. And that’s why — just like Warren Buffett — I continue to use all of the dividends I receive to buy more shares.

We’d all love a passive income, regardless where that comes from. Some people in the UK invest in buy-to-let properties, other try their hand at trading.

How do we invest?

If I were new to investing, I’d start by opening an investment account with a reputable brokerage. This involves researching and selecting a platform that aligns with my needs, offering a user-friendly interface and access to a variety of investment options.

Personally, I use the Hargreaves Lansdown platform, but appreciate there are alternatives with lower trading fees.

After this, I would have to define my financial goals. I need to establish what and when I’m investing for. For example, when will I want to start taking a passive income?

Understanding my risk tolerance is crucial in determining the mix of assets in my portfolio. I’d have to educate myself on different investment vehicles, considering stocks, bonds, and even cash.

And finally, when I’m ready, I can start purchasing stocks, bonds, or other investment vehicles.

Compounding is key

If I’m investing £50 a week or £200 a month, I need to appreciate that I’m not going to build a huge portfolio over night.

In fact, the longer I leave my money invested, the faster it grows. And that’s all down to the magical power of compounding. While the initial growth may seem gradual, the power of compounding can significantly amplify returns over time.

As such, it’s essential to stay disciplined and resist the urge to react hastily to short-term market fluctuations.

As the portfolio grows, so does the potential for compounding to work its magic. That’s because I can start earning interest on my interest as well as my contributions.

Compounding takes place when I reinvest my returns year after year. This may involve me reinvesting the dividends I receive.

Or if I invest in a stock like ******, which doesn’t offer a dividend, the company essentially reinvests on my behalf. That’s because it’s focused on growth.

Bringing it all together

A novice investor may look to achieve between 6-10% annually in the way of returns. While an experienced investor might aim for higher returns — perhaps around 10-15% annually.

So if I were starting with nothing, and investing £50 a week, here’s how my investment could grow over 35 years, assuming a 10% annualised return. At the end of the period I’d have £759,327, and it would have generated £71,849 in the final year. Even in 35 years, that’s a strong figure.

£££££££££££££

Government loans (Gilts) pay a guaranteed return so your capital is safe.

Can now be bought from online platforms such as AJ Bell as simply as

any other share. Can be useful if u are saving for a specific purpose on a

set day.

At present yielding around 4% so not suitable for inclusion in the blog

portfolio but could be paired trading with a higher yielding Trust to give

a blended yield of 7% with an extra margin of safety.