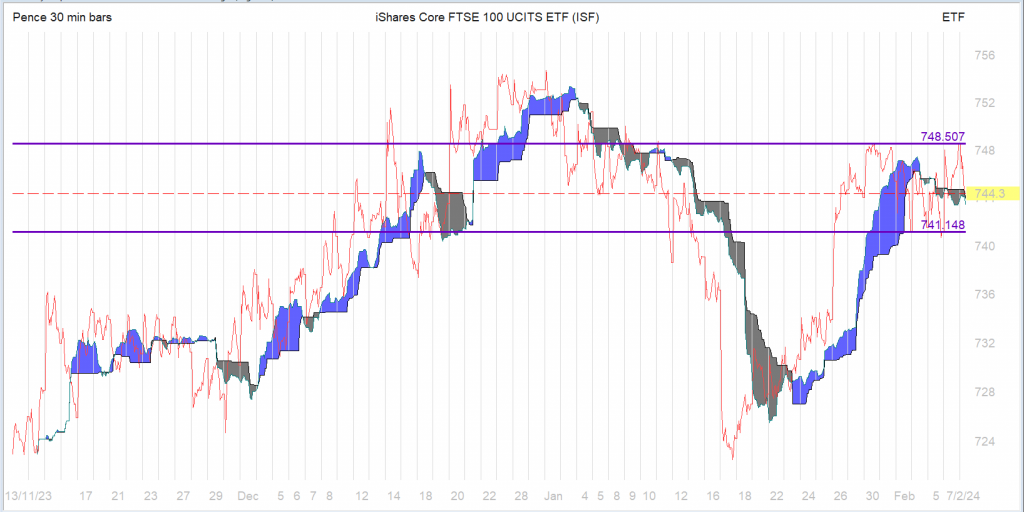

Watch to see which way it breaks, I think it’s going lower

but I have a 50/50 chance of being right and

I also have a 50/50 chance of being wrong.

Investment Trust Dividends

Watch to see which way it breaks, I think it’s going lower

but I have a 50/50 chance of being right and

I also have a 50/50 chance of being wrong.

With 2 portfolio companies still to declare their dividends

for the quarter the fcast is £2,566.00

Whilst a good foundation for the year do not scale up

to arrive at the figure for the year.

https://quoteddata.com/research

Interview with Ross Grier from NextEnergy Capital – QuotedData

I’ve bought for the portfolio 11055 shares

in Next Energy NESF for 9k.

The price is still falling but the buying yield is 10%.

Dividend:

· Dividend of 4.18p per ordinary share for the period ended 30 September 2023 (30 September 2022: 3.76p).

· Target dividend of 8.35p per ordinary share for the year ended 31 March 2024 (a year-on-year increase of 11%).

· Forecasted target dividend cover remains c.1.3x for the financial year ending 31 March 2024.

· Total dividends declared since IPO of £318m or 63.7p per share.

22 Nov 2023

Custodian Property Income REIT plc

(“Custodian Property Income REIT” or “the Company”)

Third quarter trading update shows rental growth supporting fully covered dividends

Custodian Property Income REIT (LSE: CREI), which seeks to deliver an enhanced income return by investing in a diversified portfolio of smaller, regional properties with strong income characteristics across the UK, today provides a trading update for the quarter ended 31 December 2023 (“Q3” or the “Quarter”).

Leasing activity continues to support rental growth and underpin fully covered dividends

Valuations

Investment Manager’s commentary

UK property market

2023 saw rising interest rates, weak investor sentiment and low transaction volumes. This was in contrast to occupier demand which delivered rental growth and has further improved the reversionary potential in Custodian Property Income REIT’s portfolio, which is now greater than it was at the start of 2023.

Investor sentiment towards real estate appears to have been closely correlated with the expected trajectory of interest rates, as determined by inflation data. Consensus opinion and the interest rate forward curve suggest that the next move for interest rates will be down, with the potential for a number of base rate cuts in late 2024 and into 2025, subject of course to an improving geopolitical environment. This should be positive for real estate investors and occupiers.

Asset management

Over the 12 months to 31 December 2023 the passing rent of the Company’s portfolio has grown by c.3% to £43.4m and ERV has grown from £48.4m to £50.1m, an increase of c.3.5%, demonstrating the continued prospects for strong rental performance which will support earnings and the companies aim of paying fully covered dividends.

The Investment Manager has remained focused on active asset management during the Quarter, completing four rent reviews at an aggregate 21% increase in annual rent from £1.1m to £1.4m, and re-gearing four leases which secured £0.5m of annual rent. These initiatives increased property capital value by £1.0m. The new leases had a weighted average unexpired term to first break or expiry (“WAULT”) of five years, with the overall portfolio WAULT remaining at 4.8 years.

Details of these asset management initiatives are shown below:

Rent reviews

New leases

Since the Quarter end the Company has completed seven further asset management initiatives, including:

Since the Quarter end the Company has also settled the following rent reviews at an aggregate 29% ahead of previous passing rent with:

Disposals

Acknowledging the higher cost of variable rate debt, of which the company currently has £50m drawn under its Lloyds Bank revolving credit facility (“RCF”), steps have been taken to advance a number of property sales, where special purchasers can unlock prices ahead of valuation, but more importantly ahead of the cost of the RCF, in order to enhance earnings per share.

During the Quarter a children’s day nursery in Chesham was sold for £0.55m at valuation.

Since the Quarter end, an industrial unit in Milton Keynes and an office building on Pride Park, Derby have been sold for an aggregate £10.1m. Two further properties in Redhill (former car dealership) and Castle Donington (offices), which are both vacant, are under offer to sell for an aggregate £4.4m. These disposals are expected to complete during the quarter ending 31 March 2024 and proceeds are expected to be used to reduce variable rate borrowings.

Fully covered dividend

The Company paid an interim dividend of 1.375p per share on 30 November 2023 relating to the quarter ended 30 September 2023. The Board has approved an interim dividend per share of 1.375p for the Quarter, fully covered by EPRA earnings, payable on 29 February 2024. The Board is targeting aggregate dividends per share of at least 5.5p for the year ending 31 March 2024. The Board’s objective is to grow the dividend on a sustainable basis, at a rate which is fully covered by net rental income and does not inhibit the flexibility of the Company’s investment strategy.

Borrowings

On 10 November 2023 the Company and Lloyds Banking Group agreed to extend the RCF for a term of three years, with options to extend the term by a further year on each of the first and second anniversaries of the renewal. The RCF includes an ‘accordion’ option with the facility limit initially set at £50m, which can be increased up to £75m subject to Lloyds’ consent. The headline rates of annual interest now include a LIBOR transition fee previously applied separately, increasing by 12bps to between 1.62% and 1.92% above SONIA, determined by reference to the prevailing LTV ratio. As a result there is no change to the aggregate margin from the renewal.

At 31 December 2023 the Company had £190.0m of debt drawn at an aggregate weighted average cost of 4.3% with no expiries until August 2025 and diversified across a range of lenders. This debt comprised:

At 31 December 2023 the Company’s borrowing facilities are:

Variable rate borrowing

Fixed rate borrowing

Each facility has a discrete security pool, comprising a number of individual properties, over which the relevant lender has security and covenants:

Recommended all-share merger with abrdn Property Income Trust Limited (“API”)

On 19 January 2024 the Company announced a recommended all-share merger with API and on 1 February 2024 published an associated combined circular and prospectus incorporating notice of a General Meeting to be held on 27 February 2024. The Board believes that the merger would bring together two complementary portfolios to create a differentiated REIT with enhanced diversification and share liquidity and a fully covered and sustainable dividend for the combined group’s shareholders.

JCGI

“The big story on the markets was the sharp rally in Chinese stocks after a state-backed initiative to stir up interest in equities,” says Russ Mould, Investment Director at AJ Bell.

“The Hang Seng advanced 4% and the SSE jumped 3.2%, some of the biggest one-day gains we’ve seen on the Chinese market in a long time. The Hang Seng Tech index did even better, soaring by 7%.

“A state-owned investment fund indicated it would continue to buy up shares in what looks like a concerted effort to breathe some new life back into Chinese equities after they fell out of favour. The securities regulator also pledged to encourage more long-term funds to buy shares and to encourage companies to buy back more of their own shares.

“A clampdown by the Chinese government on regulation and data protection previously caused jitters on the market and that was followed up by a flop post-Covid economic reopening. With signs the country is finding it harder to sustain strong levels of economic growth, it’s no wonder investors lost interest in the country.

“Investment wisdom suggests the best time to buy equities is when everyone has lost interest, so we’ve seen a few brave outfits take a contrarian view on China in recent months and they will certainly welcome today’s price action. The big unknown is whether this effective stimulus initiative is just a short-term boost or enough to trigger a sustained revival in Chinese markets.

I’ve sold the portfolio shares in HFEL for a profit of

£73.00 including the dividend earned but not received.

The plan is to re-invest the proceeds in NESF where

the similar dividend looks secure but the shares are trading

at a wider discount to NAV, which could improve overall

returns in the long run.

A portfolio buy one day, today is not one day.

Thursday 8 February

Ex-dividend payment date

Aberforth Smaller Cos Trust PLC

Aberforth Split Level Income Trust PLC

Abdrn Property Income

Atrato Onsite Energy PLC

Baronsmead Second Venture Trust PLC

Baronsmead Venture Trust PLC

BlackRock Income & Growth Investment Trust PLC

Bluefield Solar Income Fund Ltd

Chenavari Toro Income Fund Ltd

CVC Income & Growth Ltd – EUR

CVC Income & Growth Ltd – GBP

EJF Investments Ltd

GCP Infrastructure Investments Ltd

Henderson Smaller Cos Investment Trust PLC

Impact Healthcare REIT PLC

Keystone Positive Change Investment Trust PLC

LXi REIT PLC

Octopus Renewables Infrastructure Trust PLC

Picton Property Income Ltd

Residential Secure Income PLC

Taylor Maritime Investments Ltd

© 2026 Passive Income Live

Theme by Anders Noren — Up ↑