2 Big Dividends on Sale as Warsh Goes “Dirty Harry” on Inflation (Yields Up to 11.9%)

Brett Owens, Chief Investment Strategist

Updated: July 7, 2026

The crowd is still way too worried about interest rates—and their fear is handing us a shot at two stout monthly dividends (yielding up to 11.9%) on the cheap.

We can thank new Fed chair Kevin Warsh for ginning up the panic here. Because he was appointed by President Trump, the suits expected Warsh to push for lower rates right off the hop. Instead, the new Fed chief has gone full Dirty Harry on inflation.

Investors are buying it. But they’re already on the wrong side of the story.

Oil has plunged to around $68 a barrel. And the job numbers for June, out last week, were soft, with the number of new gigs around half of what it was expected to be. That could be a sign of things to come as AI spreads across the economy, providing a sweeping level of automation to white-collar work. Very deflationary.

In the 1990s, the Internet acted as a similar “deflator” on prices. The move from snail mail to email and from fax machines to web browsers made businesses wildly more efficient, which kept a lid on consumer prices.

The bottom line here is that rates will fall. Which brings us back to Warsh.

Even though the president has given him a long leash for now, I expect it to shorten fast when rates and inflation start to ease. When push comes to shove, Warsh will choose self-preservation.

As the wind shifts toward lower rates, I expect the discounts on the two monthly dividend CEFs we’ll discuss next to speed toward par—and possibly beyond.

Monthly Dividend Pick No. 1: A Diversified Pick With a 7.8% Dividend

We’re going to start with a fund holding high-yield stocks and handing us a rich 7.8% dividend (yes, paid monthly).

That would be the BlackRock Enhanced Equity Dividend Trust (BDJ), which is nicely set up for pretty well any market. For starters, its portfolio is balanced among stock sectors. Tech is the biggest slice, but even so accounts for a reasonable 18% of assets, followed by financials (15%), industrials (14%) and healthcare (13%).

Then BDJ adds a dash of global exposure, with about 11% of assets outside the US, in stable countries like the UK, South Korea and Canada.

Let’s get to what we really want to know about here: the (monthly!) dividend, which is not only hefty but has risen a stout 32% in the last decade (not including special dividends—the spikes in the chart below):

Source: Income Calendar

The fund aims to hold at least 80% of its portfolio in dividend-paying stocks. Right now, its holdings include Amazon.com (AMZN), as well as companies like CVS Health (CVS) and Citigroup (C), both of which stand to gain as AI boosts their efficiency.

BDJ is also seeing gains from FedEx (FDX), as the company cuts costs and moves away from lower-margin work (like Amazon deliveries). BDJ also holds Western Digital (WDC), which has soared on booming demand for chips and storage.

The fund further bulks up its dividend by selling options on its holdings. That brings in extra income and further shores up the dividend. It’s a strategy that works particularly well in volatile markets.

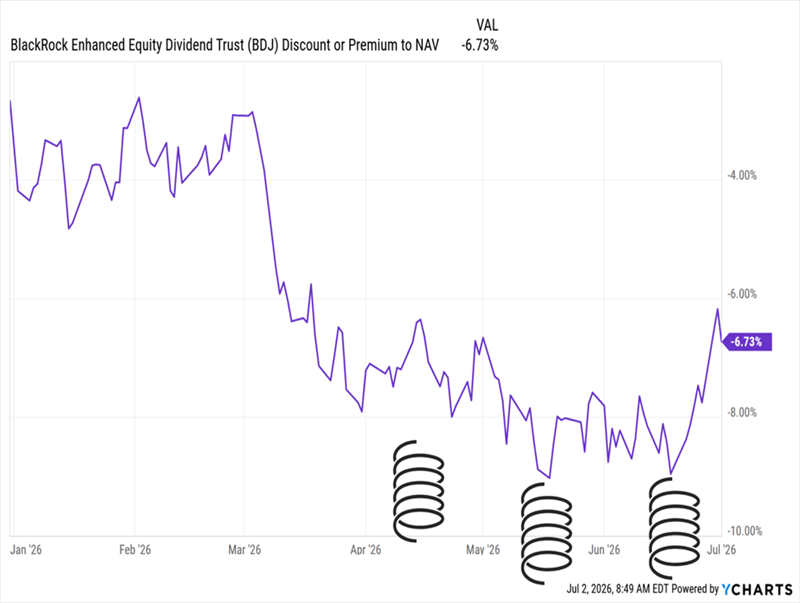

Even so, investors have tossed BDJ aside. As I write this, the fund’s discount to net asset value (NAV, or the value of its underlying portfolio) sits at 6.7%—though it looks like it’s carving out a bottom here, suggesting its next move could be toward par.

BDJ Is Cheap—and Its Discount Has Momentum

That’s a great setup to move into this well-constructed fund. The bonus? Since it pays dividends monthly, a buyer today won’t have to wait long to collect their first payout.

Monthly Dividend Pick No. 2: An 11.9% Dividend for 94 Cents on the Dollar

Now let’s swing over to bonds, where another fund from BlackRock stands out: the BlackRock Multi-Sector Income Trust (BIT). (That’s par for the course, as BlackRock is one of the biggest players in the CEF space.)

A key thing to note with BIT is the long average maturity on its credit assets: around 13 years. That’s important because longer-duration bonds do better when rates decline, as they’re more attractive than new (and lower-yielding) debt.

Moreover, BIT’s effective duration is around four years. That’s enough to position it for gains on lower rates without taking on too much risk if rates rise.

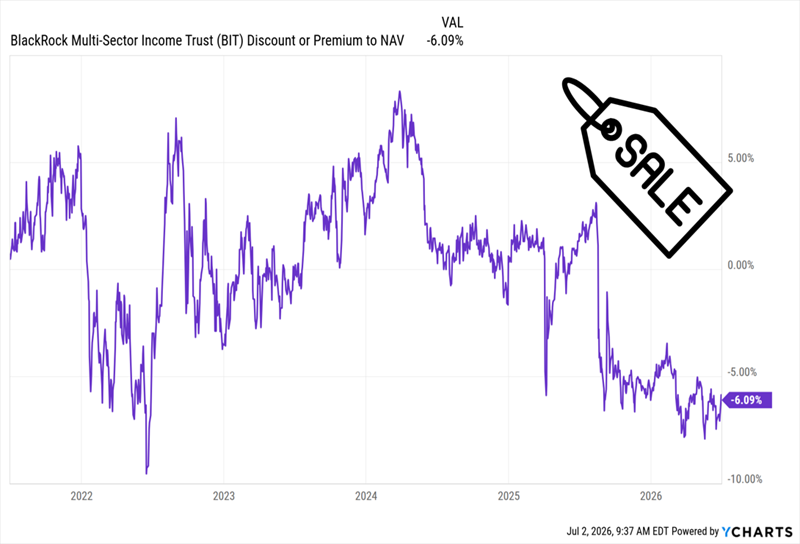

Plus, any rate-rise risk is more than priced into the fund’s 6.1% discount to NAV. That’s a level we haven’t seen since 2022, and then only briefly. And back then, the rate setup was the opposite of today’s: Inflation soared to 9%, and rates shot higher in response.

BIT’s “Back to 2022” Sale

The fund’s drop in valuation looks overdone here. And if you look at the right side of that chart, it looks like that discount is carving out a bottom, similar to what’s happening with BDJ.

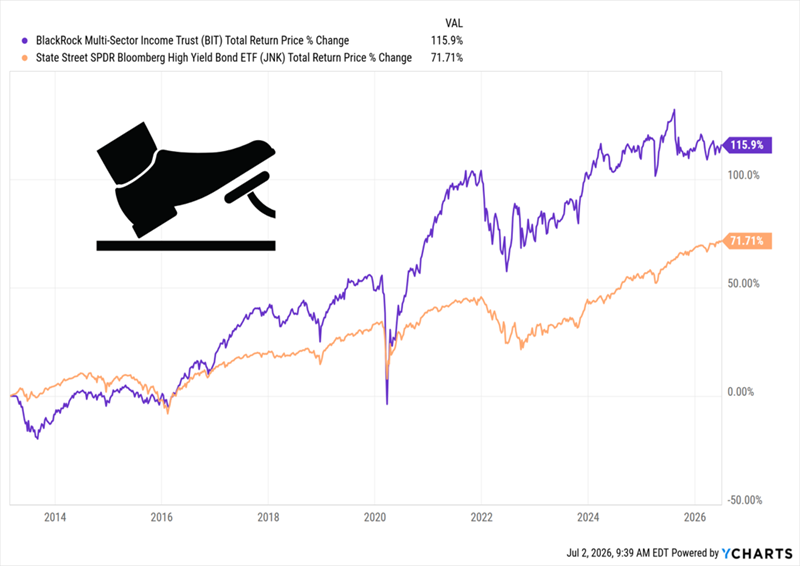

On the performance side, this fund has been around since 2013 and has more than doubled the return of the benchmark US high-yield bond ETF, the SPDR Bloomberg High Yield Bond ETF (JNK), since then.

BIT Laps High-Yield Bonds

Reinvested dividends drove that return, thanks to BIT’s monthly payout, which has not only held steady through the tumult of the last decade (including the aforementioned 2022 bond meltdown)—it’s grown.

Source: Income Calendar

That strong payout record is likely to continue. And in the longer run, a move toward lower rates would act like a vice on the discount, forcing it to close—and help propel the fund’s price higher as it does.