Quote 3 The defensive (or passive) investor will place his chief emphasis on the avoidance of serious mistakes or losses. His second aim will be freedom from effort, annoyance, and the need for making frequent decisions. Indeed, Graham sketched out an asset allocation strategy that is still a perfectly sensible starting point:

Quote 4 He [the passive investor] should divide his funds between high-grade bonds and high-grade common stocks. We have suggested as a fundamental guiding rule that the investor should never have less than 25% or more than 75% of his funds in common stocks, with a consistent inverse range of between 75% and 25% in bonds. There is an implication here that the standard division should be an equal one, or 50–50, between the two major investment mediums. Of course, you couldn’t just buy a globally diversified ETF in Graham’s time. But his advice readily translates into the purchase of a large cap index tracker such as an MSCI World ETF and a high-quality government bond ETF. Beyond that, Graham was clearly an advocate of the buy and hold strategy:

££££££££££

For he, read he, she, or any colour of the rainbow.

abrdn Asian Income Fund Ltd ex-dividend date abrdn Diversified Income & Growth PLC dividend payment date Bankers Investment Trust PLC ex-dividend date Brunner Investment Trust PLC ex-dividend date Chelverton UK Dividend Trust PLC ex-dividend date City of London Investment Trust PLC ex-dividend date CQS Natural Resources Growth & Income PLC ex-dividend date CQS New City High Yield Fund Ltd ex-dividend date Doric Nimrod Air Three Ltd ex-dividend date Doric Nimrod Air Two Ltd ex-dividend date Foresight Solar Fund Ltd ex-dividend date Henderson Far East Income Ltd ex-dividend date JPMorgan Global Core Real Assets Ltd ex-dividend date Law Debenture Corp PLC dividend payment date Pacific Horizon Investment Trust PLC ex-dividend date

Up to 16.8% yields! Here are the 10 highest-paying dividend stocks in the FTSE 350

Story by Zaven Boyrazian

So, what are the biggest opportunities I think are out there for income investors to consider right now?

Top 10 income stocks

In order of dividend yield, here are the largest payouts in the FTSE 350 that make me think they’re worth investors researching further.

Ithaca Energy – 16.75%

NextEnergy Solar Fund – 10.76%

Energean – 10.27%

SDCL Energy Efficiency Income Trust – 10.25%

Phoenix Group Holdings – 10.24%

M&G – 9.73%

TwentyFour Income Fund – 9.47%

Legal & General – 9.27%

Abrdn – 9.25%

British American Tobacco – 8.77%

It doesn’t take more than a quick glance to notice a lot of the income opportunities lie within the energy and financial services sector. Both industries are being riddled with uncertainty right now. The oil & gas sector is tackling supply chain terrors from the ongoing and horrendous conflicts in Ukraine and Gaza. Meanwhile, insurance and investment companies are at the mercy of interest rate fluctuations.

However, it’s not exactly a secret that by capitalising on unloved companies, tremendous returns can potentially be unlocked. After all, that’s often where some of the biggest bargains can be found.

So, is now the time to start thinking about snapping up these businesses while they’re still cheap? Not necessarily. Let’s take a closer look at the current pack leader, Ithaca Energy.

Risk vs reward

With the firm’s medium-term production output seemingly set in stone, management feels comfortable enough to return $500m of dividends to shareholders in 2024 and 2025, fuelling the stock’s impressive 16.8% dividend yield. But if that’s the case, why haven’t investors been rushing to buy its shares

The problem is a looming risk of equity dilution. Acquiring Eni’s oil & gas assets is going to require quite a bit of capital. And with debt being quite expensive right now, that likely means a whole bunch of new shares are likely to be issued, sending the stock price firmly in the wrong direction.

At the same time, the UK windfall taxes on energy companies are expected to take quite a toll on earnings in the current tax year. And profitability could come under further pressure if unforeseen complications emerge during the integration process.

In other words, Ithaca’s yield appears to be high due to high levels of uncertainty. If the company manages to defy expectations, opportunistic investors could reap tremendous returns. But the opposite is also true. And should the worst come to pass, a 16.8% yield may quickly evaporate.

Therefore, when exploring high-yield opportunities, investors must consider the risks attached to an investment. Otherwise, it’s easy to tumble into an income trap.

I think everything posted made a great deal of sense. But, think on this, what if you added a little information? I mean, I don’t want to tell you how to run your website, but suppose you added a title to possibly grab folk’s attention? I mean Compound growth: A powerful argument for investing long term. – Passive Income is a little boring. You could glance at Yahoo’s front page and watch how they create post headlines to get people interested. You might try adding a video or a pic or two to grab people interested about everything you’ve got to say. In my opinion, it might bring your blog a little livelier.

££££££££££££££

Investing your hard earned for your retirement is a very serious topic.

Re-investing dividends can be boring but the biggest downside is that u virtually wishing your life away as u wait for your next dividends to accrue so u can invest in your Snowball.

There are no plans to add videos as there are plenty of videos sites available on the web at present. Tks for taking the time to post your comment.

Quote 1 Investment policy, as it has been developed here, depends in the first place on a choice by the investor of either the defensive (passive) or aggressive (enterprising) role. The aggressive investor must have a considerable knowledge of security values—enough, in fact, to warrant viewing his security operations as equivalent to a business enterprise. Graham typically referred to passive investing as “defensive”. He believed that most people should choose the passive route because only investing professionals could devote the necessary resources to active or “aggressive” investing:

Quote 2 It follows from this reasoning that the majority of security owners should elect the defensive classification. They do not have the time, or the determination, or the mental equipment to embark upon investing as a quasi-business. They should therefore be satisfied with the excellent return now obtainable from a defensive portfolio (and with even less), and they should stoutly resist the recurrent temptation to increase this return by deviating into other paths. In Graham’s book, passive investors were better off sticking to straightforward strategies that minimised error:

££££££££££££££

For, he, read he, she, or any colour of the rainbow.

Next week I’ll publish some advice from Benjamin Graham that has stood the test of time.

Until then WB.

Perhaps no greater tribute can be paid to him than that written by Warren Buffett, who said:

“Ben Graham was far more than an author or a teacher. More than any other man except my father, he influenced my life.”

Investing aside, Buffett movingly said that of all Graham’s virtues, his greatest was generosity. That he was the kind of man who planted trees that others would sit under. By listening to Graham’s advice today, we can benefit from the fruits of his labour, planted years before we were born.

A three-quarter year review of London’s Investment Company Sector

As Q3 2024 wraps up, we analyse London’s investment company sector to identify this year’s winners and losers. The FTSE Closed End Investment Index (FTSE CEI) rose +0.5% for the quarter, maintaining positive returns but trailing the FTSE All-Share’s +9.9% year-to-date. Top-performing sectors include Growth Capital and Leasing, while Renewable Energy Infrastructure and Regional REITs struggled.

By Frank Buhagiar

With the numbers in for Q3 2024, it’s time to check in on London’s investment company space. Which investment companies are having a year to remember and which are having a year to forget?

Three for three

Another positive quarter for the FTSE Closed End Investment Index (FTSE CEI). The sector closed up +0.5% for the three months ended 30 September 2024. That’s a little off the +2.3% sterling total return delivered by the FTSE All-Share over the same period, but at least the record of posting positive returns for each quarter of the year has been maintained: Q1 / Q2 2024, the FTSE CEI was up +2.3% / +3.4% respectively. With just Q4 to go, the clean sweep is on.

Year-to-date, the FTSE CEI is now showing a +6.3% positive return. Once again, a little behind the FTSE All Share’s total return of +9.9% for the first nine months of the year. Barring a barn-stopping Q4, looks like a fourth successive year of the FTSE CEI falling short of the All-Share. As the table below from FTSE Russell shows, 2020, the last year London’s closed-end space outperformed the wider market:

The shoe is on the other foot

Worth pointing out though that London’s investment companies haven’t always struggled to keep pace with the wider market. Indeed, the opposite could be argued – the wider market has struggled to match London’s closed-end sector. For, as the table above shows, over the ten-year period 2014-2023, the FTSE CEI outperformed the wider market in six of the ten years. And it turns out between 2017-2020, the closed-end fund index had its own four-year winning streak. The FTSE All-Share then merely catching up with London’s investment companies.

And according to the above table, the FTSE CEI chalked up a handsome +113% gainbetween 2014-2023. The FTSE All-Share by contrast could only manage a cumulative gain of +68% over the same ten-year period. The FTSE 100 too is only up +68%. Over the ten years to 2023, London’s investment companies have trounced the wider market.

In terms of the average share price discount to net assets, this stood at 13.7% as at end of September, no change on the end of August level. This compares to the average 12.8% discount as at the end of 2023 and 10.8% as at the end of 2022.

The standouts – regional and sector levels

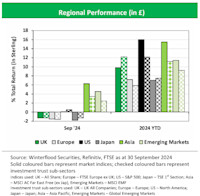

Given the UK market’s well-documented troubles – companies leaving London for the US and elsewhere; pension funds internationalising their portfolios at the expense of UK allocations; and persistently low valuations – perhaps surprising to see the UK All Companies subsector joint top year-to-date in terms of best-performing investment trust region. Alongside North America, UK All Companies up +12.2% over the first nine months of the year. As the below graphic from Winterflood shows, all regions are in positive territory year-to-date with the worst-performing investment trust region Europe still managing a +5.8% gain:

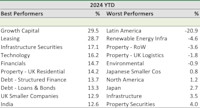

At the wider sector level, Growth Capital tops the list with a +29.5% share price total return to show for the first nine months of the year – the eight-fund sector includes the likes of Chrysalis (CHRY) which recently commenced a share buyback programme as part of its capital allocation programme; Petershill Partners (PHLL) which returned US$222m during the first half of 2024 via a mixture of dividends, a tender offer and buybacks; and the Baillie Gifford-run Schiehallion (MNTN). At the half-year stage, the sector was up +21.53% and was second in the table behind then leader Technology and Technology Innovation which boasted a gain of +28.03%. Three months on and the Technology sector has slipped to fourth after its year-to-date gain shrank to +16.2%. An underwhelming reporting season for the Magnificent Seven mega-techs weighing on sentiment there.

Not far behind Growth Capital is Leasing with a share price total return of +28.7%. Both aircraft and shipping leasing companies have been performing strongly this year. The two Doric Nimrod Air Funds reacted well to news that DNA2 is selling its five remaining aircraft to United Arab Emirates for an aggregate combined total of US$200m or £153.53m. The valuation had positive read across for sister fund DNA3 – share prices of both funds reacted well to the news.

The table below from Winterflood lists the ten best and worst performing sectors year-to-date:

Below Growth Capital and Leasing, interest-rate sensitive subsectors, such as Property, Debt and UK Smaller Companies, well represented in the best performers column. As for the worst performers, sectors comprised of just one or two funds feature highly, including Latin America (BlackRock Latin American) and Property RoW (Ceiba Investments and Macau Property Opportunities). Renewable Energy Infrastructure completes the bottom three – a mix of higher-for-longer interest rates, weaker power prices and bad weather all at work here.

The standouts – investment company level

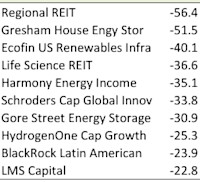

First, the laggards. Regional REIT the worst performer to date – a deeply discounted rights issue to blame. Elsewhere, five Renewable Energy Infrastructure funds in the bottom ten. As highlighted above, a range of top-down reasons for this, but also company-specific ones too. For example, a failure to find a buyer for its portfolio did for Ecofin US Renewables Infrastructure, while the suspension of its dividend didn’t help sentiment at Gresham House Energy Storage.

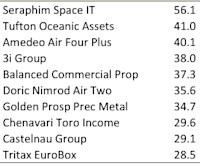

As for the winners, no surprise to learn that investment companies belonging to this year’s top-performing sectors feature highly in the best performers list. In first place, Seraphim Space from Growth Capital keeps hold of top spot, a position it held at the half-year stage. That’s despite seeing its gain on the year fall slightly to +56.1% from +58.72% as at 30 June.

As the table below shows, a small gap between Seraphim and the rest of the pack. The next two top performers both herald from the Leasing sector – Tufton Oceanic Assets and Amedeo Air Four Plus up +41% and +40.1% respectively. DNA2 also makes it into the top ten courtesy of a +35.6% rise.

Elsewhere, strong gold prices lie behind Golden Prospects Precious Metals’ seventh place. Meanwhile 2023’s top performer 3i Group still in the hunt to retain its crown – shares are up +38% over the nine months to end September. A little ground to make up true, but certainly doable. At the half-way stage, 3i shares were up +28% which was only good enough to squeak into the table in tenth place. Three months later and 3i is up to fourth spot. What’s more, the gap between the private equity giant and Seraphim has narrowed from +30.7% to +18.1%. The race to be London’s best-performing investment company in 2024 is well and truly on.

Literacy Capital has raised its management fee while reducing its charitable donations to balance shareholder costs. Tritax EuroBox has switched its recommendation from Segro’s all-share offer to a 69p per share cash bid from Brookfield. Meanwhile, Witan shareholders have approved a merger with Alliance, creating one of the largest London-listed investment companies by market cap.

By Frank Buhagiar

Literacy Capital ups its fees

Literacy Capital (BOOK) has gone against the grain and announced an increase in its management fee from 0.9% of NAV to 1.5% of NAV.“As Literacy’s portfolio has grown considerably in recent years, now numbering 19 different businesses, the Investment Manager is keen to ensure that it has the resources necessary to build the scale and capabilities within its team.” The Manager believes that, because BOOK focuses on investing in small businesses, its portfolio companies typically require a higher level of support than other areas of the private equity market. Hence the need to charge higher fees.

To cushion the blow, the private equity fund is cutting the amount it donates to literacy charities. As per the fund’s investment policy, BOOK has made charitable donations equal to 0.9% of net assets every year since 2018. But as the fund’s value has grown, so too has the size of the donations made from £532,000 in 2018 to £2.79 million in 2023. “The Board has concluded that reducing the Company’s charitable donation from 0.9% to 0.5% of net assets per annum enables the Company to retain its unique feature of making a significant difference to children from disadvantaged backgrounds, through continuing to make substantial seven-figure donations on an annual basis, whilst allowing for the Increased Management Fee to be paid without materially increasing the total cost of the combined elements for shareholders.”

Numis: “It is somewhat unusual to see an increase in management fees, which is bucking the trend across much of the sector. However, we note that Literacy Capital is already unusual for a private equity IC, given it has only a base fee, with no performance fees.”

Tritax EuroBox recommends second bid

Tritax EuroBox (EBOX) announced it is ditching its previous recommendation that shareholders ought to accept an all-share offer from Segro (SGRO). That’s because the Board is now recommending a 69p per share cash offer received from Brookfield. Easy to see why. Not only is Brookfield offering cash, but it has been pitched at a small premium to SGRO’s offer. Including dividends, this originally stood at 68.4 pence per EBOX share. But due to market movements, the SGRO bid has since fallen to 65.1p. Ball back in SGRO’s court it would seem.

Or not. For SGRO quickly put out a statement reiterating the benefits of its all-share offer. “This would enable Tritax EuroBox shareholders to retain exposure to the European industrial and logistics sector at this point in the cycle, in the largest and most liquid REIT in Europe, or realise their position for cash given the significant liquidity in SEGRO’s shares. A further announcement will be made if appropriate.” Not sure whose court the ball is in now.

Winterflood: “we view this latest proposal as an improved deal for shareholders, as it provides certainty of transaction price and removes exposure to market movements that would change the implied value of the all-share merger under the SEGRO offer.”

Numis: “there is of course the potential for the Segro share price to rally over the coming weeks increasing the theoretical value of its offer, but ultimately ‘cash is king’ and we expect that the certainty of the Brookfield offer will have strong appeal for many shareholders.”

Alliance Witan merger gets the green light

A case of goodbye Witan, hello Alliance Witan (ALW) after shareholders in the former gave the okay to combine with Alliance on 9 October 2024. No hanging around either. By the next day, Alliance’s name and ticker had been changed to Alliance Witan and ALW respectively, while the newly named fund also took on approximately £1,539 million of net assets from Witan in exchange for 120,949,382 newly issued ALW shares.

JPMorgan: “ALW is now one of the largest London listed investment companies in market cap terms, ranking fifth behind 3i Group (£31.6bn market cap), Scottish Mortgage (£10.9bn), Pershing Square Holdings (£6.4bn) and F&C Investment Trust (£5.1bn).”

The Results Round-Up – The Week’s Investment Trust Results

Seraphim Space Investment Trust (SSIT) saw a £14.1m rise in its spacetech portfolio to £201.5m for the year ending June 2024, driven by new investments and gains. Despite raising c.$900m and strong portfolio growth, its share price remained flat. However, SSIT remains 2024’s top-performing alternatives fund, benefiting from growing demand in cybersecurity, defence, and space technology.

By Frank Buhagiar

Seraphim Space (SSIT) reaches for the stars

SSIT reported a £14.1m increase in the value of its spacetech portfolio to £201.5m over the course of the year ended 30 June 2024. The increase was driven by “additional investments, increased fair value net gains and minimal FX gain.” Growing interest in spacetech couldn’t have hurt though. As CEO, Mark Boggett, notes “the portfolio has defied the difficulties of the wider macroeconomic climate by collectively managing to raise c.$900m from both the private and public capital markets over the course of the year.”

Easy to see why that amount was raised given the “encouraging performance of the portfolio companies. “Buoyed by increasing demand from government customers, the private companies within the top 10 holdings (which together constitute 81.8% of the portfolio fair value and 72.2% of NAV) collectively saw their revenues increase year-on-year by an average of 71% (in Sterling) and 224% (on a fair value weighted basis).” A stellar performance then. But not enough to move the share price higher on the day of the results, although perhaps that was always on the cards as the shares have been this year’s best performer in the alternatives space.

Liberum: “SSIT is still the best returning (>£50m market cap) alternatives fund in share price terms YTD, with its discount narrowing by c.17ppts.”

Numis: “In our view, the fund’s addressable market is extensive, with growing demand in a wide variety of areas such as cybersecurity, defence spend and climate change, where using technology in space is becoming increasingly essential. The fund benefits from a team that is well engrained in what is a nascent but growing sector, facilitated by the ‘democratisation’ of the spacetech industry through cost efficiencies stemming from the remarkable progress of SpaceX.”

Winterflood: “This represents a solid set of results, with few surprises. With a range of companies making operational strides, and at a 47% discount, we continue to believe this represents an attractive proposition.”

IPU’s +13.8% NAV total return beat the Deutsche Numis Smaller Companies (+ AIM) index’s +12.1% over the The Results Round-Up The Results Round-U. That will go down well with shareholders who voted for the continuation of the fund at the recent AGM. So too, the promise to pay a special dividend to shareholders.

In terms of the year’s performance drivers, according to the Portfolio Managers, “An improving consumer outlook meant that the consumer discretionary sector was the most positive contributor to portfolio performance, with leisure and media stocks performing well. We also benefitted from our exposure to financials, with rising markets driving the outperformance.” And the managers sound confident for the future “with an improving economic outlook, a continued high level of take-over activity, and the relatively low valuation of UK smaller companies, we believe the sector can continue to make good progress over the next year.” The market is a believer – share price tacked on 5p to close at 418p on the day.

Winterflood: “DPS (dividend per share) 7.7p (H1 FY23: 7.7p), maintaining target yield of 4% on year-end share price. Post period-end, special dividend of 484.85p paid to return capital to shareholders who elected for it. Three-yearly continuation vote passed at AGM in June.”

Mercantile (MRC)geared up for growth

MRC clocked up a +17.6% total return on net assets for the half year, comfortably ahead of the benchmark’s +15%. Share price fared even better with a +25.8% return. That means, the fund’s long-term record of outperformance has improved further – over the ten years to 31 July, the fund has generated an annualised return of +8.5% in NAV terms compared to the benchmark’s +6.1%. And MRC is not just a capital growth play. As the dividend has increased for more than ten successive years, the fund has been recognised by the AIC as a next generation dividend hero.

The Portfolio Managers think this is just the beginning in terms of performance “we believe that we are in the early phases of the potential market recovery, with an improving domestic economic outlook combined with low valuations of UK-listed assets providing an exciting investment opportunity.” Add in “the generally strong financial performance being delivered by our portfolio companies and the breadth of new investment ideas” and it’s easy to why the Portfolio Managers are feeling confident. Also helps explain “our current elevated level of gearing, sitting at around 15%.” Investors liked what they heard – shares closed up 3.5p at 241.5p.

Winterflood: “Outperformance driven by stock selection and gearing. Gearing at period-end was 13.7% (31 January 2024: 13.4%), reflecting managers’ confidence in UK mid and small cap companies.”

Ashoka India Equity’s (AIE) crystal ball earns its keep

AIE had a good year – share price/NAV per share total return came in at +35.9% and 35.5% respectively. To be fair, it was a good year all round as the MSCI India Investable Market Index total return (sterling) topped the lot with a +37.7% total return. The slight underperformance this time round not enough to dent the long-term track record – since the fund’s inception in July 2018, NAV is up +185.0%, share price not far behind up +184.0%, while the index is only up +121.5%.

Chairman, Andrew Watkins, gives the investment management team a mention in despatches “the high regard in which my fellow Directors and I hold the Company’s Investment Manager and Adviser grows by the day.” Before going on to provide an insight into what goes on at the Board’s quarterly meetings “Believe me when I tell you that your Board spends some time at each quarterly meeting with the equivalent of a crystal ball in an attempt to foresee bumps in the road ahead.” As for what the crystal ball is currently saying “Nobody expects the trajectory to be unbroken or without such bumps but, right at this moment, with a (mostly) successful general election behind it, the Modi government looks set fair to continue on its path of growth”. Share price closed a tad lower at 274p following the results – after such a strong share price rise, shareholders perhaps tempted to take some profits off the table.

Numis: “Ashoka India has grown substantially since raising £46m at IPO and now has a market cap of c.£450m. This is a product of both strong NAV performance and secondary issuance, which has resulted in an increased number of portfolio holdings”.