Here’s how you can aim to retire with £11,973 a year in passive income

It’s never too late to consider the stock market. And with regular investments, a decent passive income might be more achievable than it first appears.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

One way of supplementing the State Pension — currently (23 January) £230.25 a week for those who have a full record of national insurance contributions — is to have a generous passive income earned from dividend shares.

Understandably, some put off saving for their retirement until later in life. Even so, it’s still possible for a person in their 40s to build a decent second income. Here’s how they could aim to match the £11,973 a year paid by the government.

In the beginning…

Personally, I think a Stocks and Shares ISA’s an excellent investment vehicle. Its primary benefit is that income and capital gains can be earned free of tax.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

Current rules permit £20,000 to be invested each year. But a 40-year-old with no savings isn’t going to be able to afford this. Instead, I’d suggest a strategy of investing little and often.

For example, putting £300 a month into an ISA for 26 years (the state retirement age is currently 66) would grow to £256,512, assuming an annual return of 7%.

On retirement, some people prefer to buy dividend shares and live off the income rather than touch their capital. A portfolio of stocks yielding 4.7% would be sufficient to generate a retirement income of £11,973 from the £256,512 sitting in our example ISA.

Sometimes, a high yield can be a warning sign that investors are expecting a cut. Therefore, rather than focus exclusively on the biggest yielders, I think it’s a good idea to have a mix of stocks with the emphasis on identifying reliable dividend payers.

These are often found in ‘boring’ industries like the utilities sector, where reasonably-predictable earnings streams enable steady payouts to be made.

One example is National Grid (LSE:NG.). Or is it? Up until 2025, the electricity company had increased its dividend for 13 consecutive years. It then surprised investors by announcing a £7bn rights issue. This is a reminder that energy infrastructure is expensive.

Although the group spent more on its dividend than before the rights issue, that’s because there were more shares in circulation and the amount per share fell. This highlights the uncertainties surrounding shareholder returns. However, because of its track record and the industry in which it operates, I’m prepared to overlook this and believe it’s a bit of a blip.

Looking ahead

For the year ended 31 March 2025 (FY25), the group reported underlying earnings per share (EPS) of 73.3p. Through until FY29, it hopes to increase this by 6%-8% a year. As a result, the group aims to grow its dividend in line with inflation. At the moment, the stock’s yielding 4%.

This growth in earnings is underpinned by plans to spend £60bn on infrastructure, including £51bn on ‘green projects’, by FY29. Over the next five years, National Grid’s planning for 19GW of additional UK electricity capacity, with half coming from energy-thirsty data centres. The group’s FY25 return on equity of 9% shows that the potential returns on this investment are huge.

For these reasons, I think National Grid could be considered by those looking for a steady dividend share. But there could be some capital growth too. At the top end of its EPS forecast range, its forward (FY29) earnings multiple is an attractive 12.

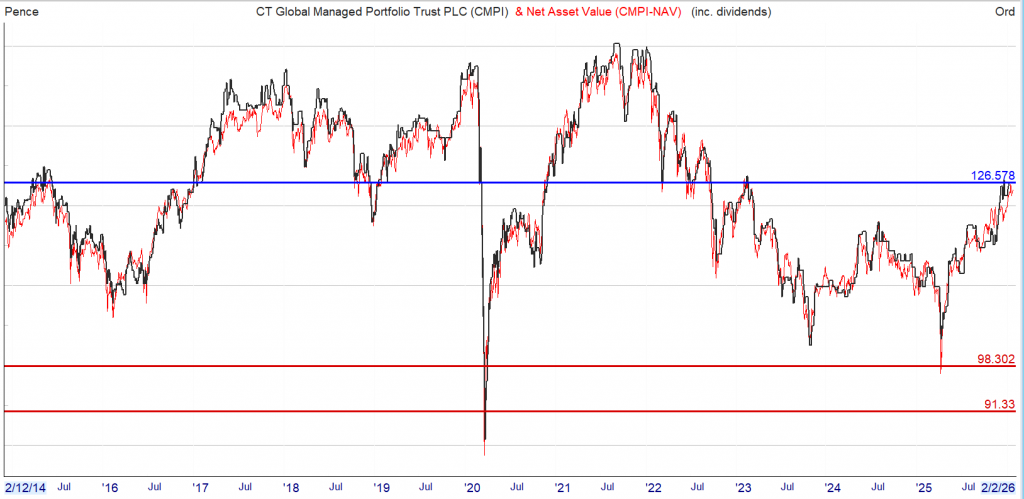

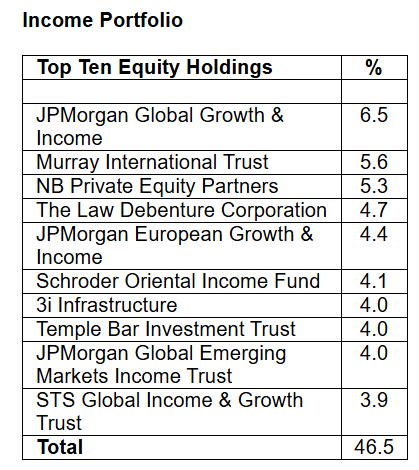

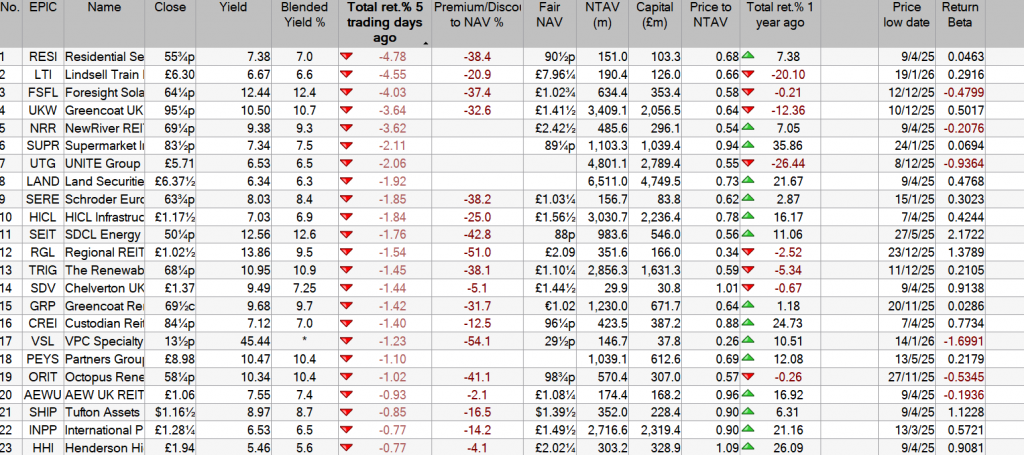

As you can see from the chart, there is a risk to capital but as the intention is never to sell as you need the dividend to pay your bills, it matters not, to you anyway.

The risk is spread over most of the IT income generating shares so the dividend is fairly ‘secure’.

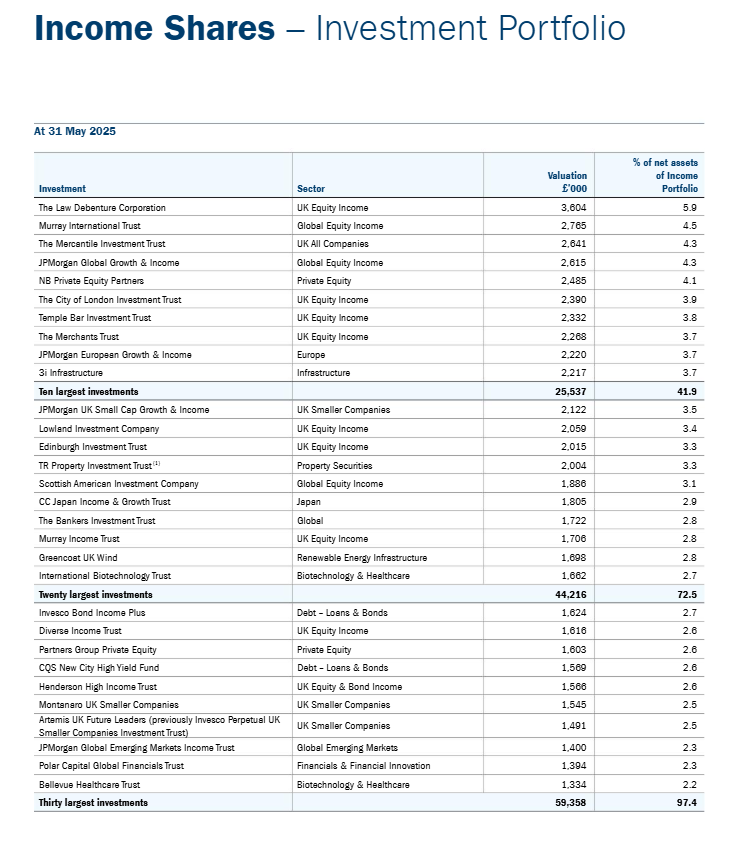

Latest top ten holdings.

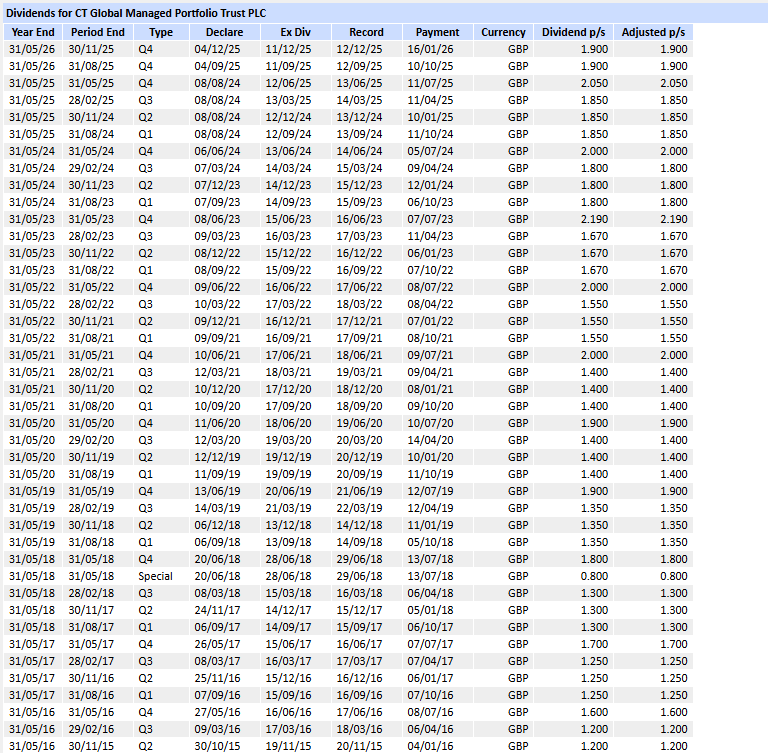

The dividend fcast is 7.6p

CT Global Managed Portfolio Trust PLC (the “Company”) announces a second interim dividend in respect of the financial year to 31 May 2026 of 1.90 pence per Income share.

This dividend is payable on 16 January 2026 to shareholders on the register on 12 December 2025, with an ex-dividend date of 11 December 2025.

The normal pattern for the Company is to pay four quarterly interim dividends per financial year.

As previously announced, in the absence of unforeseen circumstances, it is the Board’s intention to pay four quarterly interim dividends, each of at least 1.90 pence per Income share, so that the aggregate dividends for the financial year to 31 May 2026 will be at least 7.60 pence per Income share (2025: 7.60 pence per Income share).

Anyone who bought at 100p are now receiving a yield of 7.6%

Investor Presentation via Investor Meet Company

CT Global Managed Portfolio Trust PLC (the ‘Company’) is pleased to announce that Adam Norris and Paul Green, Fund Managers, will provide a live presentation which will look back on 2025 and then update investors on both the Income Portfolio and Growth Portfolio going into 2026 via the Investor Meet Company platform on Wednesday 4 February 2026 at 10:00 am GMT.

The presentation is open to all existing and potential shareholders. Questions can be submitted pre-event via your Investor Meet Company dashboard up until 9:00 am GMT on Tuesday 3 February 2026 or at any time during the live presentation.

Investors can sign up to Investor Meet Company for free and add to meet CT Global Managed Portfolio Trust PLC via:

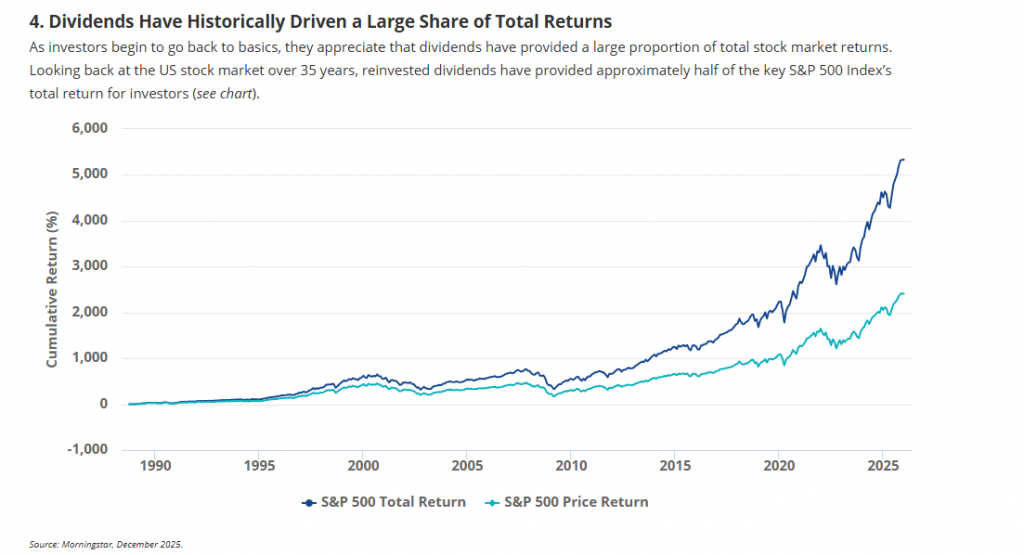

Five Reasons Why Investors are Rediscovering Dividend Stocks

15 January 2026

Martijn Rozemuller CEO – Europe

Amid all of the attention given to AI and the big US tech stocks, the fact that some investors have been quietly rediscovering high dividend stocks is less appreciated. They’re going back to basics, favoring big companies that pay high dividends year after year, providing investors with income that can be reinvested for capital gains.

The question, though, is why did investors flock to high dividend stocks during the year and what does it say about their views on equity markets in 2026 ? In my opinion, dividend stock investing has five main attractions.

Performance History – VanEck Morningstar Developed Markets Dividend Leaders UCITS ETF

2021

2022

2023

2024

2025

ETF

26.94

15.77

11.76

16.00

23.78

MSDMDLGE (Index)

27.24

16.58

12.56

16.71

24.72

Source: VanEck. Past performance does not predict future results. Calendar year as of December 31st, 2025.

1. Dividend Payers Tend to Be More Resilient In uncertain times, the solidity of big companies paying high dividends is more appealing than ever. They have profits backed by strong cash-flows that underpin dividends, even through moderate economic downturns. Their commitment to maintaining, or even growing, annual dividend payments makes them disciplined about the internal projects they spend capital on. These strong fundamentals help explain why dividend strategies can perform comparatively well in both rising and volatile markets, although this is not assured. 2025 illustrated this well, with the TDIV ETF proving less volatile than world markets, represented by the MSCI World Index, following the announcement of US tariffs in April 2025 (see chart). It is worth noting that every situation is unique and past performance does not predict future returns.

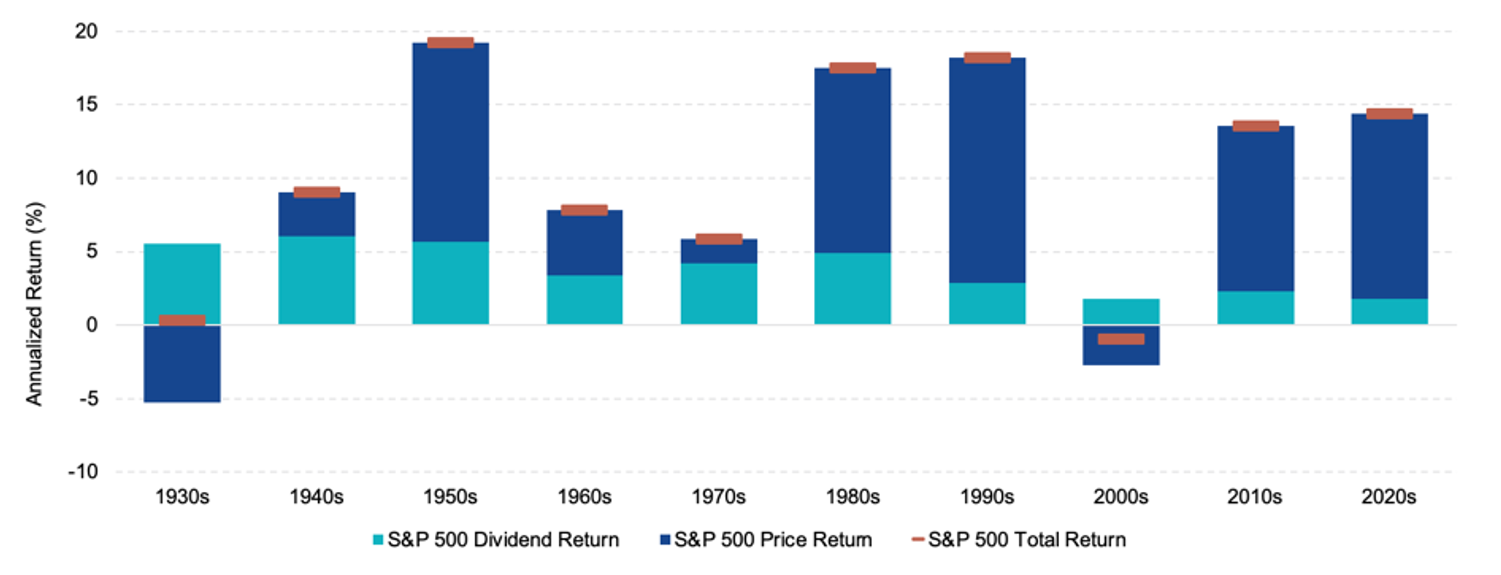

2. Dividends Help Manage Volatility Without Leaving Equities For investors who are nervous about the outlook but do not want to sell, dividend stocks may be the answer. As 2025 shows, they can provide resilience in volatile markets. Our research indicates that dividends have underpinned stock returns over the past 80 years, especially when inflation has spiked higher as it did in the 1940s and 1970s (see chart).

Dividends Are Key In Periods of Muted Returns | Dividend Contribution to S&P 500 Total Return / 1/1/1930 – 30/06/2025

Source: Morningstar, June 2025.

3. Higher-for-Longer Rates Have Changed Investor Priorities After years of low interest rates when investors prized ‘growth at any price’, they once again value cash returns. In the 2010s, exceptionally low rates around zero encouraged investors to put a premium on growth companies in sectors like technology that offered the prospect of high future earnings growth. But with European Central Bank short-term interest rates around 2%, some investors now prefer the tangible returns of high dividends. Even if rates do fall somewhat from here, it appears that investor expectations have shifted.

5. Stability in an AI-Driven Market Lastly, dividend stocks offer the likelihood of greater stability at a time when some investors are nervous that AI stocks might be in a bubble. If for any reason that bubble should burst, the type of well-known stocks in a high dividend ETF are backed by well known, solid companies that have stood the test of time. For instance, the top 10 holdings in our TDIV ETF are large well-known companies from a variety of sectors such as Exxon Mobil, Nestle and Roche (see below).

Top 10 Holdings (%) as of 31 Dec 2025

Total Holdings : 100

HOLDING NAME

Ticker

Shares

Market Value (EUR)

% of Net Assets

EXXON MOBIL CORP

XOM US

2,344,575

240,236,730

5.03

VERIZON COMMUNICATIONS INC

VZ US

6,008,577

208,377,734

4.36

NESTLE SA

NESN SW

2,175,450

184,097,351

3.85

PFIZER INC

PFE US

8,176,829

173,360,253

3.63

ROCHE HOLDING AG

ROG SW

458,275

161,647,043

3.38

SHELL PLC

SHEL LN

4,850,408

152,206,223

3.18

TOTALENERGIES SE

TTE FP

2,503,659

139,178,404

2.91

PEPSICO INC

PEP US

1,128,960

137,960,974

2.89

ALLIANZ SE

ALV GR

347,254

135,602,687

2.84

NOVO NORDISK A/S

NOVOB DC

2,670,969

116,311,223

2.43

Top 10 Total (%)

34.49

These are not recommendations to buy or to sell any security. Securities and holdings may vary.Due to certain corporate actions, the holdings may contain shares with a very small weighting. In addition, more shares may be included in the portfolio than in the normal composition. During the review, these shares normally fall from the index.

Source: VanEck, December 2025.

Key risks to consider alongside these five attractions:

Although dividend stocks may appear attractive for their perceived resilience and income potential, dividends are never assured and can be reduced or suspended, while share prices can still decline significantly. A high-dividend approach may also underperform broader equity markets – particularly during growth-led rallies – and may entail greater exposure to certain sectors or countries, which can amplify the impact of sector- or region-specific setbacks. Returns can be further influenced by currency fluctuations and changes in interest rates. As with any ETF, investors should also take into account product-specific risks, including tracking difference.

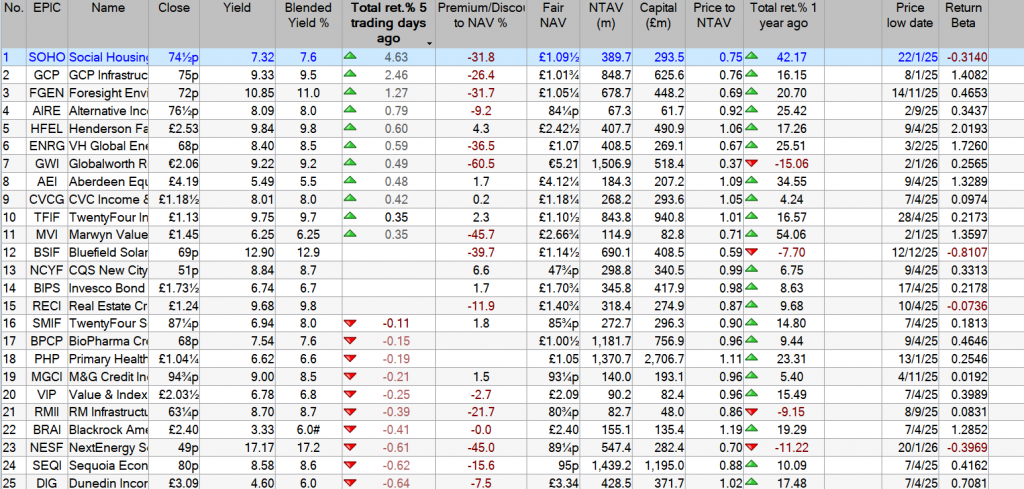

The above are the underperformers from the Watch List, so there may be a higher risk/reward if you trade any of them. Of course there may be some clunkers hiding in the Watch List, so care needed.

The shares trading at a premium, haven’t underperformed but traded exactly how you hoped they would, if they were in your Snowball.

Remember if any of the losers are in your Snowball, you have still earned income to be re-invested back into your Snowball.

Remember, it’s your duty to check the dividend announcements for the share in your Snowball.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

What’s the best passive income idea ? Depending on who you ask, you may well get a lot of different answers. Personally, one of the passive income ideas I like (and use) is investing in the stock market. Specifically, that involves buying shares in proven blue-chip businesses I hope can pay me dividends.

That can earn a lot of passive income, or just a little. It can also require a lot of cash for investing, or just a little. In other words, this flexible approach that can be tailor made for someone’s financial situation and passive income goals.

How shares generate passive income

Not all shares pay dividends and they can be cancelled at any time. So it is important to understand the mechanics of how this approach works.

The amount an investor earns depends on how much they put into shares and at what average dividend yield. Yield is basically the amount of dividends they should earn in a year, expressed as a percentage of what they pay for the shares.

So for example, a yield of 5% means an investor putting £100 into the stock market ought to earn £5 of dividends a year.

Where does the money for dividends come from? A company needs to generate enough spare cash and then can decide whether to pay dividends, or use such cash for something else.

So when on the hunt for shares to buy, I look at a company’s business model and balance sheet. I then try to assess how likely it is to pay dividends in the years to come.

Targeting a specific income

I explained dividend yield above. Say someone wants to target £50 a day of passive income from dividends. That is £18,250 a year.

To keep things simple for explanation, imagine a 10% yield. That would require investing £182,500 in the stock market to hit that target.

However, I do not see 10% as a realistic target for blue-chip shares in today’s market, when the FTSE 100 yields 2.9%. But I do think a 6% goal is credible. That would require investing around £304k in the market. That could be done in one fell swoop (which is unlikely for most of us) or through regular contributions — even small ones — building up over time.

With less money, the same plan could still work, but it would generate less passive income.

One income share I think investors should consider at the moment is asset manager M&G (LSE: MNG), with a 6.6% dividend yield. The company aims to grow its dividend per share each year (something known as a progressive dividend policy) and in recent years it has done that.

Demand for asset management is high and likely to stay so over the long term. I reckon that with its strong brand, international reach and customer base in the millions, M&G has some serious ongoing cash generation potential.

One risk is that choppy markets could lead policyholders to pull out funds. In recent years, the firm has sometimes struggled with the challenge of clients pulling more money out than they put in to its funds.

I hope you had one or two. Past performance is no indication of future performance. One thing is certain that for e.g. SUPR will not make 37% this year and it could be challenging to make 10%.