Trust Intelligence from Kepler Partner

CT Global Managed Portfolio (CMPG)14 October 2025

Disclaimer

This is a non-independent marketing communication commissioned by Columbia Threadneedle Investments. The report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on the dealing ahead of the dissemination of investment research.

Portfolio Overview Analyst’s

Portfolio

CT Global Managed Portfolio Trust aims to provide exposure to best-in-class portfolio managers in the investment company universe. The trust comprises two share classes: CMPI, which seeks to deliver an attractive level of income with the potential for income and capital growth, and CMPG, which focuses on maximising capital growth. Once a year, shareholders are given the opportunity to convert shares between the growth and income portfolios at net asset value without incurring UK capital gains tax. This allows shareholders who aren’t investing via a tax-exempt account to adjust their investments in line with their evolving circumstances without incurring a tax bill.

Since 01/06/2025, the two portfolios have been managed by Adam Norris and Paul Green, who have a combined 35 years of investment experience, and succeeded long-standing manager Peter Hewitt (see Management section). A succession plan had been prepared in advance and Peter will support Adam and Paul until his retirement at the end of October. In addition, we note that the new managers have experience managing multi-manager strategies and also benefit from the support of the broader EMEA Multi-Asset Solutions team. The investment objectives of the two share classes remain unchanged, but Adam and Paul bring different views to the table which has already been felt in the portfolios. They aim to build two higher-conviction portfolios over time, holding a smaller number of investment companies in larger position sizes, with the top ten holdings expected to account for a greater proportion of the overall portfolios. They also intend to reduce overlapping exposure across different investment company holdings, with the underlying managers’ skill driving CMPG and CMPI’s NAV performance.

The new managers also want to increase the allocation to global equities while reducing the portfolios’ weighting in UK equities. This does not reflect a view on the valuation of UK equities, but rather a wish to achieve broader global diversification. To that end, they have sold CMPG’s holdings in Lowland Investment Company (LWI). In fact, the growth share class already holds Law Debenture (LWDB), which, like LWI, is managed by Laura Foll and James Henderson, meaning the portfolio is already exposed to their investment process. Moreover, CMPG still has exposure to UK small caps through Aberforth Smaller Companies (ASL), and Adam and Paul assessed that LWI’s small-cap-heavy strategy with an income mandate was not necessary in the portfolio of the growth share class. Adam and Paul have also sold CMPG’s holdings in Finsbury Growth & Income (FGT), as they believe a similar quality defensive exposure can be obtained through global mandates. In contrast, they have added to JPMorgan Global Growth & Income (JGGI) in both CMPG and CMPI portfolios. This trust pays a dividend of at least 4% of NAV as at the end of its previous financial year but differs from traditional equity income strategies, as it focuses on companies with faster earnings growth and superior earnings quality while trading at valuations in line with the broader market, making it suitable for both income and capital growth mandates.

GEOGRAPHICAL BREAKDOWN

Source: Columbia Threadneedle Investments

Like Peter before them, Adam and Paul leverage Columbia Threadneedle’s extensive in-house resources, notably insights from the multi-asset team, to identify areas with strong earnings growth and/or dividend potential over a three-year horizon, as well as tactical opportunities. In a recent meeting, they highlighted four key themes: US equities, emerging market equities, private equity exits, and total return opportunities in infrastructure.

US equities have been volatile since the beginning of the year, notably due to rising trade tensions between the US and the rest of the world. They experienced a sell-off in April following ‘Liberation Day’ (02/04/2025) but have rebounded strongly since, after tariffs were paused and reduced and US corporates reported robust second-quarter earnings. In fact, Adam and Paul expect strong earnings growth to continue, with technology stocks as the main driver. Accordingly, they have been adding to Polar Capital Technology (PCT) in CMPG’s portfolio, which is also invested in Allianz Technology Trust (ATT).

Adam and Paul also see strong prospects for emerging market equities, as they could benefit from a weaker US dollar and robust earnings growth while offering reasonable valuations. They consider Chinese technology a particularly compelling area, with companies trading on attractive multiples, providing growth potential, and undertaking share repurchases. As a result, they have introduced Fidelity Emerging Markets (FEML) and added to Mobius Investment Trust (MMIT) in CMPG’s portfolio, as well as JPMorgan Global Emerging Markets Income (JEMI) in CMPI’s.

Private equity is another area where the new managers see opportunities, as they believe that the dearth of IPOs and weak M&A activity over the past three years has resulted in greater unrealised value across portfolios of private equity trusts. However, Adam and Paul are selective, focusing on those with sensible valuations and clear routes to realisations. For example, they have introduced NB Private Equity Partners (NBPE) into CMPG’s portfolio, noting that NBPE’s holdings are largely mature deals that could benefit from a reopening of IPOs and increased M&A activity. Adam and Paul have also added to Oakley Capital Investments (OCI), which has become CMPG’s largest holding, as the table below shows. They view OCI’s portfolio as high quality and reasonably valued, with realisations already occurring, notably the sale of the legal technology platform vLex in July, at more than a 300% uplift on its December 2024 valuation. Moreover, OCI is trading on a wide discount, c. 25% at the time of writing, which also prompted Adam and Paul to increase their holding.

CMPG/CMPI: TOP TEN HOLDINGS

| CMPG | CMPI | ||||

| Name | AIC sector | Weight (%) | Name | AIC sector | Weight (%) |

| Oakley Capital Investments | Private equity | 5.8 | Law Debenture | UK Equity Income | 5.2 |

| Fidelity Special Values | UK All Companies | 5.3 | JPMorgan Global Growth & Income | Global equity income | 5 |

| Polar Capital Technology | Technology & Technology Innovation | 5.1 | NB Private Equity Partners | Private equity | 3.9 |

| HgCapital Trust | Private equity | 5 | Murray International | Global equity income | 3.8 |

| Law Debenture | UK Equity Income | 4 | Temple Bar | UK Equity Income | 3.6 |

| Allianz Technology Trust | Technology & Technology Innovation | 3.6 | JPMorgan European Growth & Income | Europe | 3.3 |

| Pershing Square Holdings | North America | 3.6 | JPMorgan Global Emerging Markets Income | Global emerging markets | 3.2 |

| JPMorgan Global Growth & Income | Global equity income | 3.5 | 3i Infrastructure | Infrastructure | 3.2 |

| Scottish Mortgage | Global | 3.5 | Lowland Investment Company | UK equity income | 3 |

| AVI Global Trust | Global | 3.1 | Cordiant Digital Infrastructure | Infrastructure | 3 |

| Total | 42.5 | Total | 37.2 | ||

Source: Columbia Threadneedle Investments, as at 31/08/2025

The new managers also see strong total return opportunities in the infrastructure space and have introduced Pantheon Infrastructure (PINT) into both CMPG and CMPI portfolios. PINT provides exposure to infrastructure assets across North America, Europe, and the UK through co-investments. With its focus on areas such as data centres and other digital infrastructure, Adam and Paul see significant growth potential in PINT’s portfolio and believe that future realisations could be supported by private equity capital. Adam and Paul have also introduced Cordiant Digital Infrastructure (CORD) into CMPI’s portfolio. As of 16/09/2025, CORD holds six companies that own infrastructure assets embedded in the digital economy, including communication towers, fibre-optic networks, and data centres, primarily in Europe. The investment company follows a ‘buy, build and grow’ approach, aiming to acquire companies, develop them to increase revenues, and expand their asset base. Adam and Paul note that CORD is highly cash-generative, which has enabled the company to increase its dividend each year since its launch in 2021 (offering a yield of c. 4.5% at the time of writing), while also reinvesting to grow its capital base, providing attractive NAV growth prospects. Given its strong total return potential, Adam and Paul do not rule out introducing CORD into CMPG’s portfolio in the future.

Finally, the new managers have increased CMPI’s holding in BioPharma Credit (BPCR), which specialises in providing loans to companies in the life sciences industry. These companies have struggled to raise capital through equity, as investor appetite for higher-risk, speculative ventures has waned amid a higher interest rate environment. They have also faced regulatory and political risks, including the Trump administration’s plans to introduce drug price controls and the vaccine scepticism of Robert Kennedy Jr., the new Secretary of Health and Human Services. As a result, companies in the life sciences sector have become more reliant on debt. Adam and Paul also note that BPCR charges high interest on its loans, incentivising companies to repay early and incur substantial prepayment fees, which have historically been used to pay special dividends. At the time of writing, BPCR offered a prospective yield of c. 7%.

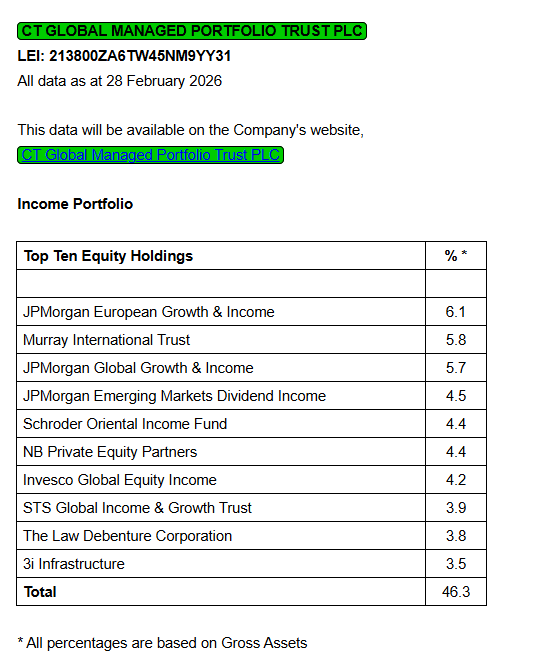

CMPI Current top ten holdings

You’ve built a lot of trust through your consistency.

This was a very informative post. I appreciate the time you took to write it.