Temptation of NESF

A tidy 12% yield from Next Energy Solar – is this an OB2025 idea?

Dear reader

I previously wrote in my article “what’s occurring”:

NESF might not be everyone’s cup of tea but at the end of the day when all’s said and done, is it tidy?

Thanks for reading The Oak Bloke’s Substack! Subscribe for free to receive new posts and support my work.

NESF is another FTSE250 company potentially for my ideas for 2025. The second of four FTSE250 companies in the OB 25 Ideas for 25. Don’t worry reader, I’ve not entirely turned my back on nano caps. Having started a list of 20 I was agonising over further ideas I felt carried merit. So I decided since the next year is (20)25 that the idea for OB 25 ideas for 25 had a nice ring to it. More for you to read, reader. More opportunities for harrumphers to harrumph about things. More for eagle-eyed readers to use along with their skill and timing to turn ideas into profitable outcomes.

And learning from fellow racer, Mr Arby, I’ve furthermore decided that one of these ideas will be weighted. More on that in a future article.

Next Energy Solar

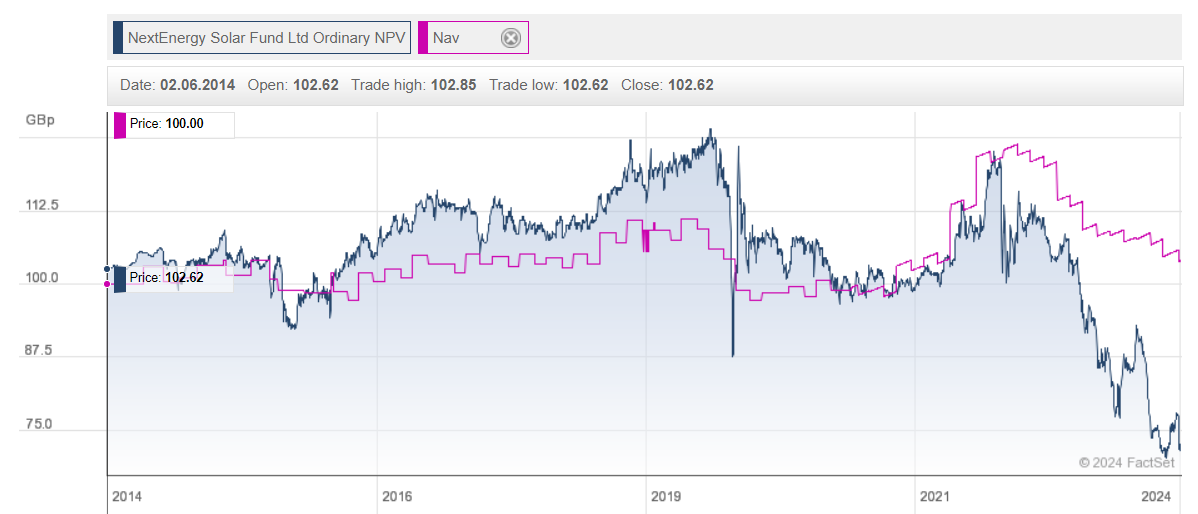

NESF is a large solar investment trust with 102 assets and capacity of 983MW. After years of trading at a premium to NAV, both its NAV and share price have fallen away, albeit its NAV has reverted to 2021 levels – do we see a clue there that temporary factors created “noise” which increased and then decreased its assets?

Yes.

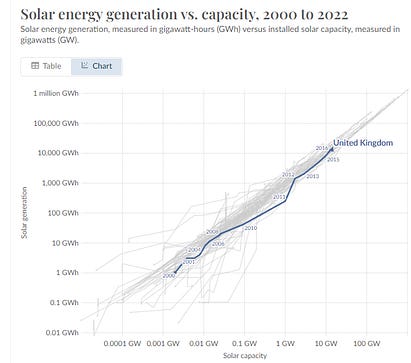

NESF has a large UK footprint, with 10% Italy, and 5% RoW. Its assets are long life, and 983MW capacity and 599GWh generated in 2023 tells us that the energy yield was 7.3% of capacity, while in 2022 the energy yield was 9.1% (599000/(933*365*24)). The yield fell to just 6.9% in 1H25

The yield was spot on to the average based on our world in data (you can click on the chart below). It reveals that capacity and generation are fairly consistent between countries. I had wrongly assumed that yield for the UK was lower than say Italy or the Sahara Desert, but the data doesn’t show that. So 85% of solar being in the UK isn’t the disadvantage I’d first imagined it would be. At least not using today’s technology.

The answer to this apparent riddle/contradiction is a lower temperature offsets lower irradiance. While more irradiance means more power, more heat shortens the life of equipment and reduces the efficiency of solar too. That factoid gobsmacked me.

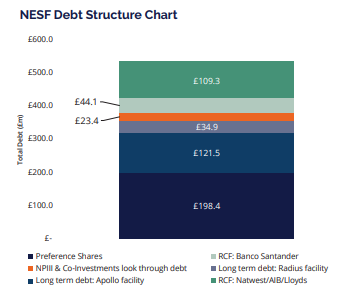

NESF appears to have a large portfolio of assets, with low costs of debt (70% fixed and 30% floating but on very advantageous rates of SONIA + 1.2% and +1.5%) and using asset sales to reduce the more expensive RCF debt. £21.8m of short-term RCF was paid down in the period to 30/09/24.

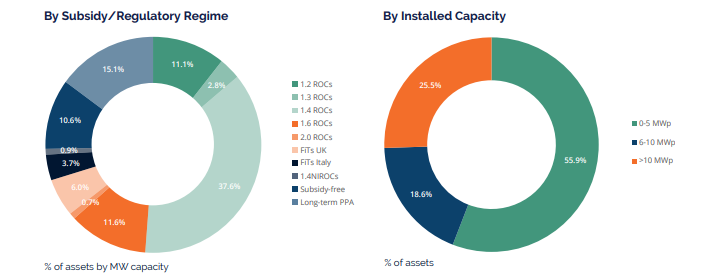

Revenue has a degree of protection from price fluctuations through hedging, ROC (renewable obligation certificates) and subsidies. About 90% of capacity is subsidised, so power prices alone only apply to 10%. Its 50MW of energy storage is live (70% owned) and 250MW is pre-construction

As at 30/9/24 NESF had agreed fixed UK pricing (hedged) covering 94.4% of budgeted generation for the 2024/25 financial year, 81% of budgeted generation for the 2025/26 financial year and 69% for the 2026/27 financial year, 62% for 2027/208 and 61% for 2028/2029.

Income in the September 2024 interim covers dividends 1.5X NESF proudly proclaim.

Show me the money the OB says. Read on to find out what I found.

Leave a Reply