Foresight Solar, the fund investing in solar and battery storage assets to build income and growth, announces its results for the year ended 31 December 2025.

Financial highlights

· Delivered a dividend of 8.10 pence per share (pps) for the year, supported by robust operational performance and active power price hedging, with 1.3x cover in line with the Company’s target.

· Announced a target dividend of 8.10pps for 2026, providing flexibility to allocate surplus cash, including to build future dividend cover. At the 23 March 2026 share price, this represents a 13.4% dividend yield.

· Expected 1.1x dividend cover for 2026. Production year-to-date and current contracted revenue hedges are expected to provide 1.0x cover. Uncontracted revenues offer additional upside as energy prices remain elevated.

· Maintained total gearing comfortably within investment policy limits at 41.2%.

· Returned £56.1 million to shareholders through a combination of dividends and share buybacks.

“Based on our track record, I am pleased to announce a target dividend of 8.10pps for 2026. After careful consideration, the Board concluded that it is in the best interest of shareholders to maintain the dividend target. We recognise the importance of cash yield to our investors and remain committed to a progressive dividend strategy. However, holding the target gives us more flexibility to allocate surplus cash, including to build dividend cover for future periods.

BlackRock World Mining Trust PLC ex-dividend date Chelverton UK Dividend Trust PLC ex-dividend date Fidelity European Trust PLC ex-dividend date Gore Street Energy Storage Fund PLC ex-dividend date Pantheon Infrastructure PLC ex-dividend date Primary Health Properties PLC ex-dividend date Ruffer Investment Co Ltd ex-dividend date Schroder Japan Trust PLC ex-dividend date SEGRO PLC ex-dividend date US Solar Fund PLC ex-dividend date Value & Indexed Property Income Trust PLC ex-dividend date

Anyone who invested money in a FTSE 100 index tracker at the start of the month may wish to look away now because returns have been ugly…

Posted by Edward Sheldon, CFA

Published 22 March

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

Image source: Getty Images

It’s fair to say that the UK’s FTSE 100 index has lost its momentum recently. After rising to near 11,000 in late February, it has plummeted amid geopolitical instability, surging oil prices, and talk of higher interest rates.

Here, I’m going to reveal how much £10,000 invested in a Footsie index tracker at the start of March would now be worth. Let’s crunch the numbers.

The index has tanked

There are a number of FTSE 100 tracker products available today. I’m going to focus on the iShares Core FTSE 100 UCITS ETF (acc) (LSE: CUKX).

I’ve chosen this one because it’s quite popular with UK investors. It also reinvests all dividends from Footsie companies meaning that share price performance gives us an idea of total returns (gains plus dividends).

Now, this ETF ended February at a price of 22,040p. So, let’s say an investor was able to buy at that price and they invested £10,000 in it.

Today – roughly three weeks later – that £10,000 would be worth about £9,140 (almost 9% less). Because as I wrote this on Friday (20 March) afternoon, the ETF’s share price is 20,135p.

The takeaways

Now, I’m not saying that this is a bad product (it’s a solid product that could be worth considering for a portfolio). Volatility like this is part of investing.

But there are a few key takeaways from these numbers. One is that a simple index tracker which is only focused on one geographic market like this doesn’t guarantee portfolio success.

By including a range of different ETFs and/or individual stocks in a portfolio, investors could have potentially obtained better returns. I’ll point out that one of my favourite ETFs, the HANetf Future of Defence ETF (another product worth considering) is actually up for the month so this could have provided some portfolio protection.

Another takeaway is that it can pay to drip feed money into the market slowly. Had the investor put £3,000 into the Footsie tracker fund at the start of the month instead of £10,000, they could potentially put another £3,000 in today at much lower prices and then another £4,000 at a later date, smoothing out their entry prices (I’m assuming here that they weren’t putting £10,000 into the market regularly).

What’s next for the FTSE 100?

Will the FTSE 100 bounce back? I think so – history shows that it’s able to recover from turbulence like this.

However, at this stage, it’s hard to know if we’ll see a ‘V-shaped’ recovery. If the Middle East conflict drags on and oil prices remain elevated, the index could remain under pressure (high oil prices tend to hurt economic growth).

So, I think the key is to remain diversified and think long term (and potentially consider buying opportunities).

A volatile stock market gives investors a chance to buy shares with unusually high dividend yields. Stephen Wright highlights one from the FTSE 100.

Posted by Stephen Wright

Published 22 March,

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

Image source: Getty Images

In tough times, the extra income generated by dividend shares can be extremely valuable. And things are pretty tough right now.

Geopolitical tensions are the highest they’ve been in some time. That’s bad for the economy, but it might be good for investors.

Crisis? What crisis?

Covid-19 brought huge amounts of uncertainty and share prices crashed as a result. But this meant dividend yields shot up.

Opportunistic investors were able to take advantage of the uncertainty. And returns for those who bought dividend shares then have been terrific.

The situation today isn’t quite the same – conflict in Iran isn’t the same as a global pandemic. But the overall uncertainty level is extremely high.

With the US focused on the Middle East, some commentators are concerned that things might escalate elsewhere. This includes Taiwan and Eastern Europe.

That might make the situation the most uncertain since the pandemic. And that doesn’t sound like a good time to consider buying stocks.

The stock market, however, is forward-looking. As a result, a number of stocks already look cheap and dividend yields have been rising.

Where to look?

The likes of BP and Shell are obvious potential candidates at a time like this. Both stocks look cheap with oil prices above $95.

I doubt, however, that this is going to remain the case. The US sees higher oil prices as a short-term necessity for long-term political stability.

Whether or not that comes to pass is another question. But I’m doubtful about how long oil prices can remain at these levels.

I think investors need to look past the next few weeks and months. Instead, there’s a chance to focus on companies that can do well for years.

One example is Unilever (LSE:ULVR). The stock is down 14% in the last month and the dividend yield has hit 3.75% as a result.

Opportunities

In recent years, the chance to buy Unilever shares with that kind of dividend yield hasn’t come around often. So it’s worth paying attention when it does.

Investors briefly had the chance a couple of years ago. But the business is arguably in a much stronger position than it was back then.

One thing that hasn’t changed is the company’s scale. This gives it a big advantage when it comes to distribution and this is still firmly intact.

The firm’s brand portfolio, however, is much stronger than it was. Unilever has divested some of its weaker lines to focus on its more valuable ones.

That’s resulted in improved sales growth metrics in recent years. So I think the opportunity might be even better than it was during Covid-19.

Long-term thinking

Investors who can look past short-term challenges can do really well in the stock market. And I think that’s the case with dividend shares right now.

The risk for Unilever remains the prospect of customers trading down to cheaper alternatives. And that’s especially true in an inflationary environment.

The company, though, has some key long-term advantages that put it in a good position to deal with this. These include its brands and its scale.

This is why the firm has such a good record of returning cash to shareholders. And I think the chance to buy it with an unusually high yield is worth taking seriously.

Christopher Ruane zooms in on some aspects of Warren Buffett’s investing approach he thinks could help an ambitious ISA investor try to beat the FTSE 100.

Posted by Christopher Ruane

Published 22 March

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

Image source: The Motley Fool

With the annual contribution deadline for Stocks and Shares ISAs around the corner, many people’s minds are focussed on using up as much of their allowance as they can. But as Warren Buffett showed with his first investments as a schoolboy, even modest-sized investments can be rewarding for someone with a long-term approach and smart approach to the markets.

So, whether with a £20k ISA, a £250k ISA, or simply an ISA with a spare £250 in it, how might someone learn from the Sage of Omaha when it comes to trying to beat the market with their ISA?

Common sense principles apply, no matter the amount

Warren Buffett is pretty clear about some of the basic elements of his investing approach.

For example, for decades he has emphasises not putting all your eggs in one basket, sticking to businesses you feel you understand, building in a margin of safety when valuing a share, and not putting at risk any money you cannot afford to lose (painful though any loss may still be).

Those make sense when investing billions – but they apply equally when putting just a few hundred pounds to work in the stock market.

A few great shares beat lots of merely good ones

Although Buffett diversifies, he does not massively diversify.

Beating the market involves doing better than it. Say you only invest in the 10 shares in the FTSE 100 that do best, by definition you will beat the index. You may even thrash it.

The challenge, of course, is that nobody – not even Warren Buffett – can know in advance how a share will do. Even a brilliant business can run into unforeseen or perhaps unforeseeable problems.

Still, Buffett’s approach has proven successful in beating the market over the long run.

Indeed, between 1965 and 2024, Berkshire Hathaway under his control managed a 5,502,284% change in per-share market value. During that timeframe, even with dividends included, the S&P 500 managed a far more modest (though still impressive) 39,054%.

One thing Warren Buffett always looks for when hunting for great businesses is whether they have an enduring competitive advantage – what he calls a “moat”.

A classic Buffett pick explained

To illustrate that concept, an example is Coca-Cola (NYSE: KO). Berkshire bought a stake decades ago and still holds it, earning hundreds of millions of pounds in dividends annually.

Say someone wanted to replicate the distribution system Coke has built worldwide. Could they do it?

I am not sure. Even if they could, it would take decades and be hugely expensive.What about building a cola brand to rival Coca-Cola?

Many have tried, from PepsiCo to A G Barr (though to be accurate, perhaps Coca-Cola was rivalling the Cumbernauld firm not the other way around, as Barr’s Cola predates the US brand). Yet Coca-Cola remains dominant.

Plus, of course, Coca-Cola has a unique secret recipe.

All of this adds up to a massive moat.

Times change, of course, and Coca-Cola faces business risks today it did not a decade ago, like the rise of weight-loss drugs and geopolitical whiplash against US brands in the current climate of international relations.

Still, Coca-Cola has been raising its dividend per share annually for decades. A strong moat can go a long way!

Harvey Jones examines how investors should respond to the current uncertainty, and urges investors to stay calm even if the stock market does crash.

Posted by Harvey Jones

Published 8 March

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

Image source: Getty Images

Whatever you may have read, the stock market didn’t crash last week. There’s a strict definition of a crash, and the FTSE 100 didn’t meet it.

It didn’t even qualify as a correction, which means a 10% drop over a short period. A crash requires a fall of 20% or more. In the last five trading days, the UK’s blue-chip index slipped 5.74%, largely caused by the war in Iran. So we’re nowhere near a crash yet.

Should you buy Persimmon Plc shares today?

Before you decide, please take a moment to review this report first. Despite ongoing uncertainties from Trump’s tariffs to global conflicts, Mark Rogers and his team believe many UK shares still trade at substantial discounts, offering savvy investors plenty of potential opportunities to learn about.

That doesn’t mean we won’t get there. Given the uncertainty, markets could have a lot further to fall. So what should investors do?

FTSE 100 uncertainty

At The Motley Fool we have a tried and tested approach to moments like this. Don’t panic. Don’t try to second-guess the market. And above all, don’t sell. That only turns a paper loss into a real one.

Instead, sit tight and keep calm. If there’s spare cash available, consider using it to buy strong companies whose share prices have temporarily fallen. That takes courage, of course. It’s not easy to keep a cool head when the headlines are screaming about war. But history shows that even outright crashes don’t last forever.

At some point the panic subsides, bargain hunters move in, and shares resume their long-term upward trend. Short-term market volatility is the price investors pay for the superior long-term returns from equities.

There are exceptions. If someone needs their money soon, say for a house deposit, it probably shouldn’t be in shares in the first place. Ideally, investors should only commit money they won’t need for at least five years, and preferably much longer. With that in mind, opportunities are already emerging.

While the FTSE 100 itself has only dipped modestly, many individual stocks have fallen much further. British Airways owner International Consolidated Airlines Group, housebuilders Persimmon (LSE: PSN) and Barratt Redrow, consumer goods giant Reckitt and engineer Weir Group all dropped around 14% last week. Precious metals miner Fresnillo fell 17%, finally breaking its strong run. They’re firmly into correction territory.

Persimmon shares plunge

Many of them issued news or results last week, so the Iran war isn’t exclusively to blame. Persimmon didn’t though. Housebuilders often struggle in uncertain times. Consumer confidence falls and people become reluctant to make big purchases like homes.

This time, there’s interest rate risk. If rising oil prices push inflation higher, the Bank of England may delay cutting rates, or even increase them. Higher mortgage costs would squeeze housing demand.

However, Persimmon now looks reasonably valued, trading on a price-to-earnings ratio of about 14.3. The dip has also pushed the trailing dividend yield up to 4.6%. There are risks, of course. Housebuilders have struggled since Brexit in 2016. Persimmon shares are up 12% over the past year, but down a painful 55% over five.

If the conflict drags on and borrowing costs stay high, sales and profits could come under pressure. Even so, for patient investors with a long-term view, I think Persimmon is worth considering.

As for whether we get a full-blown crash next week, nobody knows. But if markets fall further, I’ll be watching stocks like these closely. I can see plenty more FTSE 100 bargains out there today

The planned amount of income was £8,014 and the income figure will be £13,282.00

This figure includes some special dividends so the fcast for the next tax year is £10,500, which means we will achieve year 7 of the plan.

The SNOWBALL has a comparator share VWRP, to compare the income from using the 4% rule, where if the same amount of seed capital for the SNOWBALL was invested it would be worth £148,460. Despite the value falling £8,354 in a month, not too shabby.

The amount of income that could be withdrawn, after allowing for a 3 year cash fund would be just over 5.4k against the SNOWBALL figure of £10,500.

Like many investors who have been in the stock market for a few decades, I have several 10-baggers, or shares whose price soared by 10 times or more, under my belt.

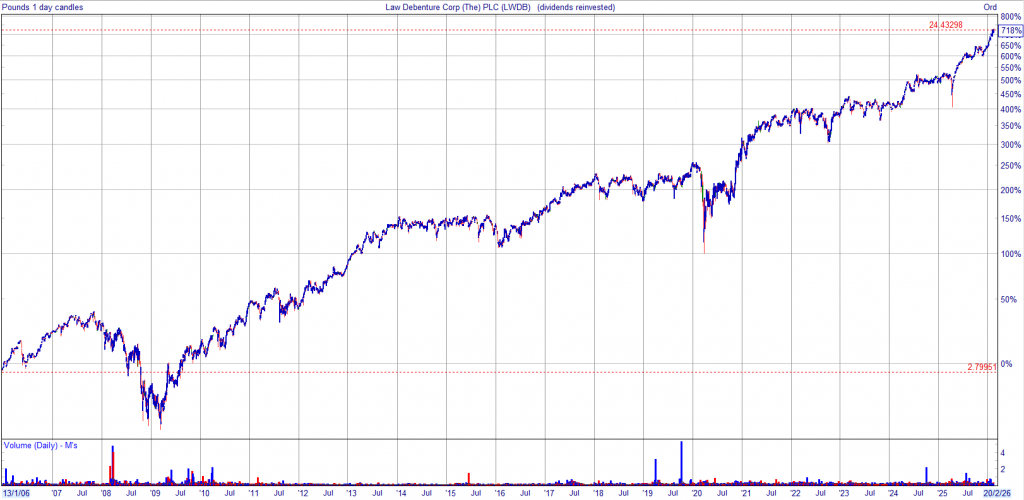

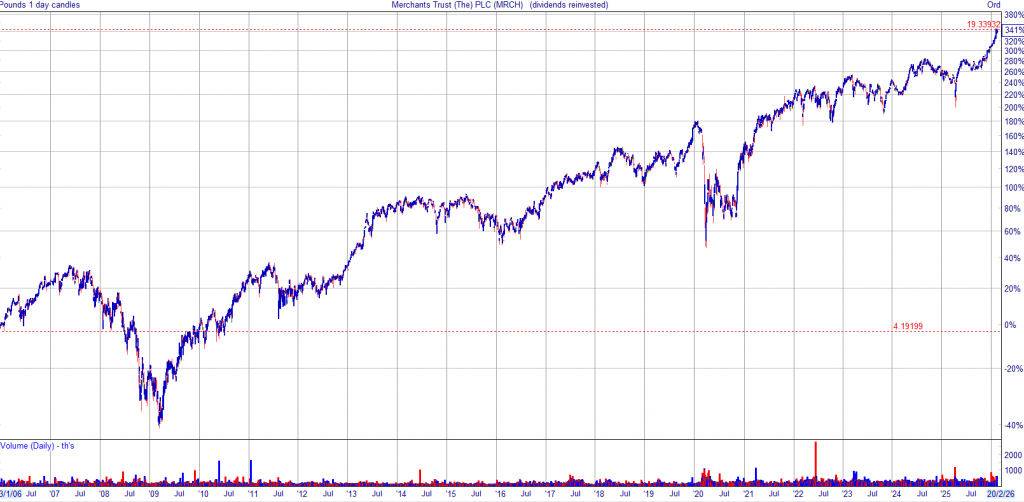

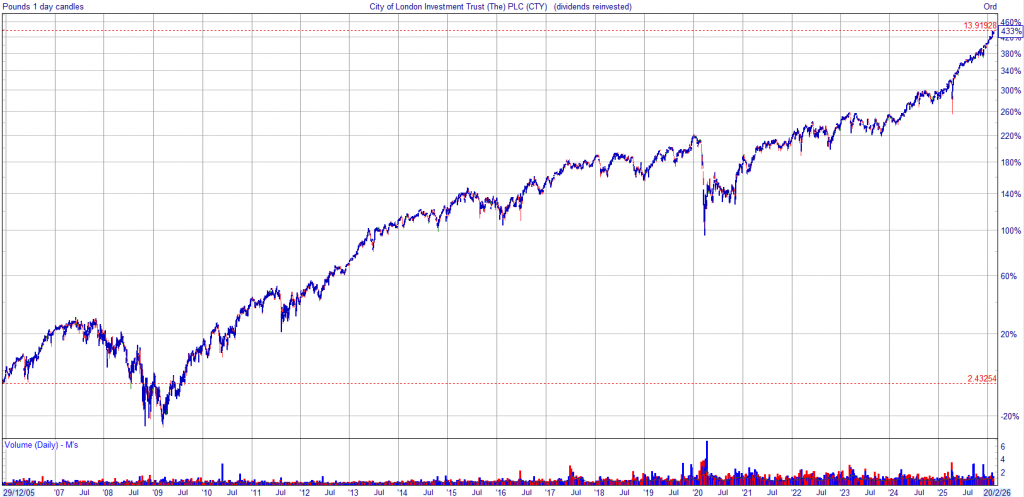

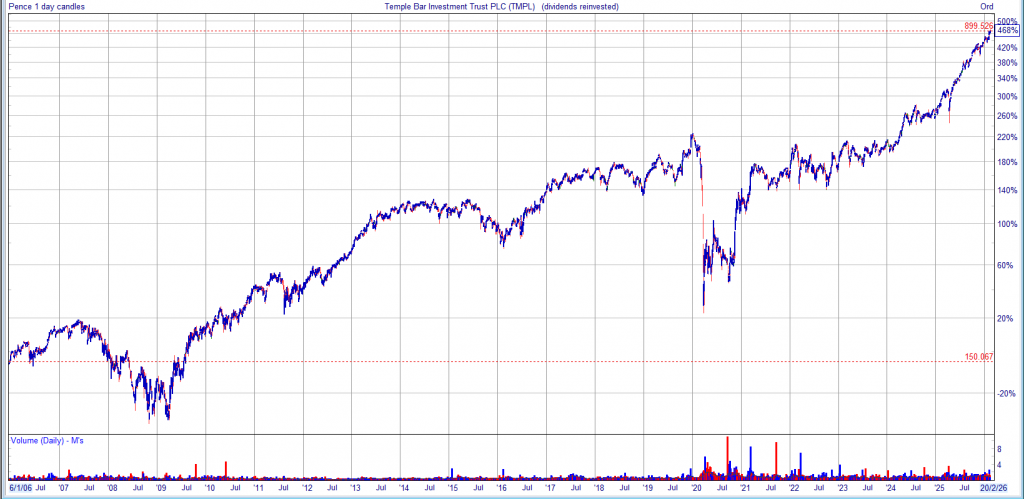

Ian Cowie ii

Interesting to compare charts to see how they react to market panics and how they all recover in time. The charts show a KISS strategy of re-investing all earned dividends back into the share but as the prices get over bought the yield falls and it would be more profitable to re-invest in your Snowball’s higher yielders or squirrel away your dividends to re-invest in market panics.

Remember it’s always easier with

But if you are happy with the yield, your entry price in ten years time will be of little importance, advice only for Trusts with ‘secure’ dividends, such as Dividend Heroes.

With the recent changes to the SNOWBALL the first projection for next year, that starts very soon, where we start with nothing, zilch, zero in the pot is for income above the fcast of £10,500.

With fast changing markets the figure may change if more Trusts reduce their dividends but there is a built in buffer as earned dividends are added to some truly wonderful yields.

There is 10k to be allocated to 2 dividend hero shares, which will add a modest amount of income to the total and unless markets reverse un-expectedly earned dividends may be added to these shares.