The filtered list for research, note the header is now fall from high, from increase from low. Is the dividend more important in a falling market than majoring on any discount to NAV ? It’s your hard earned, so your decision.

SMIF of interest as they pay a monthly dividend but the final yield is dependant on the final dividend which is variable.

That’s one option, u can buy an annuity paying around 7% and if u die within a few years the capital will form part of your estate, if not hard luck. U of course have to kiss goodbye to your capital.

Another option is to buy a portfolio of ‘secure’ paying Investment Trusts, currently yielding 8% plus and u retain all your capital. As long as u don’t sell the golden geese it should continue to lay golden eggs until u cross the bar. Different strokes for different folks.

Regional REIT Limited (LSE: RGL), the regional property specialist, announces the following trading update for the quarter from 1 April 2024 to 30 June 2024.

Summary of activity in the quarter to 30 June 2024

Lettings

Since 1 April 2024, the Group has made strong progress on lettings, exchanging on six notable leases to new tenants totalling 69,067 sq. ft., amounting to £0.7m per annum (“pa”) of rental income when fully occupied, achieving an average rental uplift of 11.0% against December 2023 ERVs. A further seven leases have renewed amounting to 47,000 sq. ft. and £0.6m pa of rental income.

Sales

Three disposals (plus one part sale) were completed in the quarter to 30 June 2024 with sales proceeds amounting to £6.9 million (before costs), reflecting a net initial yield of 9.6%.

Stephen Inglis, CEO of London & Scottish Property Investment Management, Asset Manager commented:

“During the quarter we were pleased to achieve further progress in the Group’s letting activity and disposal programme, with £0.7m of additional notable rental income from new leases and £6.9 million generated from recent disposals.

As announced on 18 July 2024, the successful capital raise of £110.5m ensures the repayment of the retail bond, facilitate the further reduction of the LTV to 40.6%, and will provide for accretive capital expenditure on assets for the long term.”

Rental Updates

· Ashby Park, Ashby De La Zouch – Ashfield Healthcare Ltd. has let 18,942 sq. ft. of office space to July 2034, with an option to break in 2029, at a rental income of £350,427 pa (£18.50/ sq. ft.).

· Central Park, New Lane, Leeds – QBE Management Services (UK) Ltd renewed its existing leases to June 2025, at a combined rental income of £297,390 pa (£13.79/ sq. ft.) on 21,570 sq. ft. of space, and also renewed its car parking lease for an additional £10,000 pa.

· 1175 Century Way, Thorpe Park, Leeds – Fonemedia Ltd has let 3,524 sq. ft. of office space to May 2029, with an option to break in 2027, at a rental income of £84,576 pa (£24.00 / sq. ft.).

· 1-6 Silver Court, Welwyn Garden City – Telespazio UK Ltd has let 3,873 sq. ft. of office space to April 2027, with an option to break in 2025, at a rental income of £67,800 pa (£17.51/ sq. ft.).

· 84 Albion Street, Leeds – Jugo Digital Ltd has let 1,304 sq. ft. of office space to April 2027, with an option to break in 2025, at a rental income of £66,000 pa (£50.61/ sq. ft.).

· Cardiff Gate Business Park, Cardiff – SMS Energy Services Ltd. renewed its lease to February 2025, at a rental income of £61,908 pa (£14.00/ sq. ft.) on 4,422 sq. ft. of space.

· York House, Felixstowe – Existing tenant Poundland Ltd has renewed existing lease of 7,593 sq. ft. of space at a rental income of £60,000 (£7.90/ sq. ft.). The lease is to April 2027.

· Templeton On The Green, Glasgow – National Society For The Prevention Of Cruelty To Children. renewed its lease to March 2025, at a rental income of £59,820 pa (£12.00/ sq. ft.) on 4,985 sq. ft. of space.

· Oakland House, Manchester – Secretary of State for Levelling Up, Housing & Communities renewed its lease to June 2029, with the option to break in 2027, at a rental income of £59,500 pa (£10.92/ sq. ft.) on 5,450 sq. ft. of space.

· Eagle Court, Coventry Road, Birmingham – Goldbeck Construction Ltd has let 2,863 sq. ft. of office space to May 2025, with an option to break in 2024, at a rental income of £51,534 pa (£18.00/ sq. ft.).

· Murdostoun House, Strathclyde Business Park, Bellshill – ATPAC Ltd has let 3,229 sq. ft. of office space to June 2029, with an option to break in 2027, at a rental income of £41,982 pa (£13.00/ sq. ft.).

· Beaufort Office Park, Bristol – St John Ambulance renewed its lease to May 2028, with the option to break in 2026, at a rental income of £49,170 pa (£16.50/ sq. ft.) on 2,980 sq. ft. of space.

Subsequent Events summary post 30 June 2024

Since the quarter end, the Group has successfully completed a £110.5m capital raise ensuring the repayment of the £50m retail bond, enabling the reduction of bank facilities by £26.3m, and providing £28.4m for identified accretive capital expenditure projects.

Lettings

· 1175 Century Way, Thorpe Park, Leeds – Greenbelt Group Ltd has let 2,670sq. ft. of office space to July 2029, at a rental income of £64,080 pa (£24.00 / sq. ft.).

Forthcoming Events

5 Aug 202410 Sep 202413 Nov 2024

Annual General MeetingInterim Results AnnouncementQ3 2024 Trading Update

The Results Round-Up – The Week’s Investment Trust Results

Among this week’s results, CT Global Managed Portfolio’s Chairman gets his wish; Scottish American tells a fable; while Pantheon International looks to bust a myth or two.

ByFrank Buhagiar•02 Aug, 2024•

CT Global Managed Portfolio (CMPI/CMPG) waiting for sentiment to improve

CMPI/CMPG’s Annual Report presumably includes twice as many numbers as most other funds. That’s because the trust, which invests in other investment companies, is comprised of two share categories: Income (CMPI) and Growth (CMPG). NAV total return for CMPI came in at +7.0%; CMPG +12.7%. Neither could match the FTSE All-Share’s +15.4%. But over the longer term, CMPG has returned +271.5% over the 15 years to 31 May 2024 (+9.1% compound per year). That beats the FTSE All-Share’s +242.5% (+8.6% compound per year).

Alternative investment companies partly to blame for the underperformance over the latest full year. As Chairman, David Warnock, writes “Discounts remained wide and interest rates which stayed ‘higher for longer’ led to reduced NAVs and share prices.” Good job then, interest rates have peaked, although Warnock believes “It may require actual cuts to be delivered for sentiment to improve; however, it does appear a more favourable environment for equity markets is a distinct possibility.” Right on cue, CMPG’s share price rose on 01 August 2024, the day of the BoE’s first UK rate cut.

Winterflood: “Negative performance in both portfolios largely attributed to widened discounts over FY and the valuation impact from higher discount rates. Annual dividend +2.9% to 7.40p per share, representing 13th consecutive year of dividend growth.”

Smithson (SSON) painting a positive picture

SSON’s -1.8% NAV per share total return for the latest half year couldn’t match the MSCI World SMID Index’s +3.4%. Chair, Diana Dyer Bartlett, describes the performance as “frustrating”. The investment managers describe it as “like watching paint dry”. As the Chair explains “The performance of the MSCI World Index, which is driven by the performance of a small number of very large technology stocks, has been very strong. The MSCI SMID Index has returned 12.8% over that period, whilst the MSCI World Index has returned 31.6%.”

Bartlett still believes good returns can be delivered by investing in small and mid-cap stocks. And the numbers back this up: SSON’s +8.2% annualised NAV per share performance since inception nearly six years ago is 0.5 percentage points higher than the MSCI World SMID Index. As for the paint-watching, the investment managers add “While we may have to remain patient a little longer while the paint dries, we remain very optimistic that the picture will be worth it.” Seems the market agreed. Shares were in demand on the day of the results.

Numis: “We believe that the portfolio has sound fundamentals that place it in a strong position to outperform over the long run and that the shares offer value on a c.11% discount to NAV.”

Scottish American (SAIN), steady as she goes

SAIN posted a +5.5% NAV total return for the latest half year, a little off the benchmark’s +12.2%. Three reasons cited for the underperformance: “market sentiment”; “not owning certain non-yielding or deeply cyclical companies which have benefitted from the current environment”; and “SAINTS’ diversifying investments in property and other areas have underperformed equities”

The Interim Management Report puts the performance into context by drawing on the fable of the race between the hare and the tortoise – hare bounds ahead at the start but becomes so over-confident stops to take a nap. This allows the tortoise, who has maintained a steady pace, to overtake the hare and finish first. “We firmly believe that all is well: perseverance remains the name of the game. The underlying growth of the portfolio remains strong, if a little more ‘tortoise’ than the market’s ‘hare’. We remain staunch believers that focusing on companies which steadily compound their earnings and dividends ever-higher will stand SAINTS’ shareholders in good stead in the long-term.” Shares definitely a tortoise on results day, barely moved.

Winterflood: “A third of underperformance comes from cyclicals, and another third from not owning Nvidia. Infrastructure (-4.4%) and fixed income (-4.4%) portfolios showed negative returns while property (+3.1%) portfolio made a positive yet modest contribution through income generation.”

Pantheon International (PIN), busting myths

PIN reported a +6.1% increase in NAV per share for the full year. Growth was down to valuation gains but also from the private equity group’s £200 million buyback programme which added +4.7% to NAV. Over ten years, annualised NAV per share growth stands at +13.5%. The portfolio continues to perform well with underlying investments clocking up +17% EBITDA growth and +14% revenue growth. Growth just half the story. Avoiding losses the other and, here too, PIN has a strong track record. The fund’s realised and unrealised loss ratio for all its investments over the last 10 years is just 2.3%.

Chair, John Singer CBE, explains that, as well as the corporate objective to deliver an attractive risk-return over the long term, the fund is on a mission “to dispel the myths that have surrounded the private equity sector for so long”. So, PIN is increasing its marketing efforts to widen its appeal “And we will continue to do this in the spirit of transparency and communication”. That’s the spirit. Market liked what it heard too, share price ticked higher.

Numis: “PIN’s shares currently trade on a c.33% discount, which we believe offers significant value”.

JPMorgan: “Overall we like PIN’s approach to capital allocation and it remains one of our top picks among the diversified listed private equity companies. We remain Overweight.”

RIT Capital Partners (RCP), a fund built for the times

RCP Chairman, Sir James Leigh-Pemberton, described the flexible investor’s half-year investment performance as solid with the NAV per share increasing by 4.2% (including dividends). All three strategic investment pillars – Quoted Equities, Private Investments and Uncorrelated Strategies – performed positively. RCP’s objective is to grow shareholder wealth meaningfully over time, through a diversified and resilient global portfolio. And the numbers show the fund has delivered. “Since inception in 1988, our NAV has averaged an increase of 10.5% per annum (including dividends), with lower volatility than stock markets.”

Looking ahead, the investment managers are not worried about current geopolitical and economic uncertainty, as “Our portfolio is built for times like this – focused on capturing long-term growth opportunities while being resilient through diversification.” Shares showed resilience on results day, closing marginally higher.

Numis: “The discount remains wide at 26% and we believe this offers significant value given improved disclosure and communication, and evidence for progress with realisations in the private portfolio.”

JPMorgan: “We are Overweight RCP which is a constituent of our investment companies model portfolio.”

Henderson Smaller Companies’ (HSL) year of two halves

HSL reported above average NAV growth for the full year: +14.5% NAV total return compares favourably to the AIC UK Smaller Companies sector’s average of +14.1%. The full-year number does not tell the whole story, however. At the half-way stage, NAV total return was a negative 7.7%, meaning NAV put on +24.0% in the second half. Not enough to keep pace with the Deutsche Numis Smaller Companies Index (ex-investment companies). The 3.7% shortfall was put down to stock-specific issues, but fund manager Neil Hermon is not losing much sleep over it thanks to the robust operating performance of the portfolio companies, their sound finances and attractive valuations. Nor is the market it seems, shares only fractionally lower following the results.

Numis: “Henderson Smaller Companies remains one of our top picks within the UK smaller companies sector. We continue to rate the management team highly and believe that following a period of poor performance over the last 2-3 years, the manager is starting to reap the rewards of sticking to the Growth at a Reasonable Price investment approach.”

F&C Investment Trust (FCIT) maintaining balance

FCIT’s +13.2% NAV total return for the half year beat the FTSE All-World Index’s +12.0%. The Fund Manager’s Report highlights the performance of the Magnificent Seven tech giants – Alphabet +31.8%, Microsoft +20.4%, Amazon +28.4%, Apple +10.7%, Nvidia +151.9%, Meta +44.1% and Tesla -20.4% – not just because they have been driving markets, but because FCIT holds every single one of them with all but Tesla featuring in the global fund’s top-ten holdings.

Not that FCIT is putting all its eggs in the technology basket. For “the Company is well positioned to benefit from a broadening of the rally driven by improving economic momentum outside of the US. Our balanced approach within our portfolio across recognised styles, including value, growth/quality and momentum, provides our shareholders with a well-diversified, global equity investment portfolio”. Shares finished the day marginally lower.

Numis: “The fund has a reasonable track record, with NAV total returns broadly in line with the index over one, three and five years.”

JPMorgan: “FCIT also benefits from low fees and is one of the highest quality large cap global investment trusts. We are Overweight FCIT.”

The Telegraph thinks there’s more to come from JPMorgan UK Small Cap Growth & Income, while The Mail on Sunday believes shares in Cordiant Digital Infrastructure deserve to rebound.

By Frank Buhagiar 30 Jul, 2024

Questor: This fund is riding on smaller companies’ rising tides Whisper it, UK smaller companies are showing signs of life. So much so that The Telegraph’s Questor Column has dusted off a tip it made in summer 2023 – JPMorgan UK Small Cap Growth & Income (JUGI). Actually, two tips. For the £487m trust was only formed in February 2024 following the merger of JPMorgan’s UK Smaller Companies and Mid Cap listed funds. Back then, Questor had been drawn to the fund managers’ strong track record which had seen the small-cap portfolio beat “its stock market benchmark in six of the last seven years. Over a decade it has produced a 206pc total shareholder return – the best in its sector and well ahead of the Deutsche Numis Small Cap index, which has generated just 62pc.”

Over the shorter three-year timeframe, however, the shares have generated a zero total return and that’s including dividends – a symptom of the tough times small caps have had to endure. But what has got Questor excited is the turnaround seen over one year during which JUGI’s shares have risen +39%, “as more investors noticed the incredible bargains that sustained selling by bearish investors had created in smaller UK stocks.” With inflation falling, interest rates expected to be cut and wages rising in real terms, there is “a greater mood of wellbeing.” At least enough of a feel-good factor to show “that the country is not the ‘banana republic’ some overseas investors thought it was”.

So, despite the bounce seen in JUGI’s share price over the past year, Questor believes that “While the early bounce has occurred, we believe there is more to come as UK small companies and the broader stock market comes back into favour. Following the merger, this is a bigger, slightly cheaper growth fund offering an attractive 4pc dividend under a new quarterly payout policy starting next month.” Looks like the fund got the timing of its merger spot on.

Midas: Goals pay dividends for TV tech specialist specialist Cordiant If you are reading this article online in Eastern Europe, Belgium, Ireland or America, it’s quite possible you are doing so with the help of assets owned by Cordiant Digital Infrastructure (CORD). That’s because CORD owns mobile phone towers, cables and data centres in these territories. Assets that, as The Mail on Sunday’s Midas Column writes, “make it possible to buy goods online, stream live TV, make calls, send emails and much else via the internet.” Put simply “Modern life would be almost impossible without these assets.” Not that you would think so, if CORD’s share price was anything to go by. For since joining the London Market in February 2021 at 100p per share, the shares are now at the 76p level.

What’s more the shares trade at a 40% or so discount to the value of CORD’s portfolio – £920million or £1.20 a share at the last count. A number of reasons have been cited including challenging markets and concerns over that £920 million valuation, not helped by peer Digital 9 Infrastructure’s woes. Midas however, thinks “Many of these concerns seem overblown, as Cordiant is well-managed, conservatively financed and has shown it can buy assets well and generate decent income.” Midas takes comfort from the steady rise in dividends from 3p to 4.2p; CORD’s customer base; use of a third-party valuer (accountants BDO); and boss Steven Marshall “energetically buying stock” – he acquired 800,000 more shares last month to bring his holding to over nine million shares.

All of which leads Midas to conclude “Growth is expected to continue at pace and Cordiant should benefit. Shareholders who bought on flotation have been poorly served but, at 76p, the shares deserve to rebound and investors can take heart from the 5 per cent dividend yield along the way.” In short, shareholders are being paid to wait.

Experts debate the impact of rate cuts on equities, bonds and sterling.

By Emma Wallis

News editor, Trustnet

The Bank of England (BoE) cut rates to 5% from5.25% today, following in the footsteps of the European Central Bank, and against the US Federal Reserve, which opted to keep rates higher for longer yesterday, although a September cut is on the cards.

Myriad asset classes are likely to benefit from rate cuts, from small-cap equities to strategic bond funds. Conversely, lower interest rates will push down yields from cash savings accounts and money market funds, and could put sterling under pressure.

Below, experts consider which sectors will prosper during the cutting cycle.

Equities

Stock markets have anticipated and welcomed today’s BoE pivot, said Tom Stevenson, investment director at Fidelity International. “In the past week, the FTSE 100 has risen by 2.6% to within a whisker of its all-time high of 8,446, struck in May.”

Although the Monetary Policy Committee signalled that cuts will be “few and far between”, Martin Currie’s chief investment officer Michael Browne is “more optimistic” about monetary easing. The bank’s hawkish stance “will prove to be unsustainable, in particular if the chancellor delivers a fiscally neutral budget on 30 October,” he said.

Therefore, Martin Currie prefers interest rate sensitive sectors, such as housebuilders, real estate, utilities and green energy.

Hugh Gimber, global market strategist at JP Morgan Asset Management, favours utilities and financials. Due to their long-term predictable cash flows, the valuations of utilities improve when the discount rate is lowered, he explained. Utilities are also benefitting from government spending to prepare electricity grids for increased demand linked to artificial intelligence.

The impact of rate cuts on banks is somewhat ambiguous, Gimber noted. Banks’ profit margins were bolstered by rising rates, but in a cutting cycle, corporate defaults should be contained as borrowing costs fall and refinancing becomes easier. The recent earnings season has shown the strength of banks’ profitability, particularly in Europe, he added.

Domestic small- and mid-caps should also benefit from an improvement in consumer spending and sentiment, said Laura Foll, co-fund manager at Henderson Opportunities Trust, Lowland and Law Debenture.

Gimber however was sceptical about the rotation into small-caps. The reasons why rates are coming down will determine which asset classes do well, he said. In a scenario where inflation has fallen but growth is holding up, rate cuts will be more gradual, and indeed, he expects the BoE to cut once per quarter. If growth falters, however, then central banks will cut rates faster.

The strong rally in US small-caps last month indicates that the market expects growth to persist but the Fed to cut rates imminently and rapidly. “You can’t have everything at the same time,” he explained. “You can’t have rates being slashed and the economy holding up fine. Markets are getting a bit ahead of themselves.”

Fixed income

While bond yields are still high, Colin Finlayson, a fixed income investment manager at Aegon Asset Management, believes investors have a “once in a cycle opportunity now to enter the market”.

He recommended that investors who are underweight fixed income consider increasing their exposure via strategic bond funds. “By having the ability to invest across the fixed income universe and having active management of interest rate risk, this type of strategy can help capture the upside potential available but do so while better balancing risks that the bond market brings,” he explained.

April LaRusse, head of investment specialists at Insight Investment, agreed that a declining interest rate environment should be positive for returns in fixed income.

“Markets are already anticipating rates will fall but there is always the possibility of surprise with rate cuts coming in faster or central banks deciding to do more than is priced in,” she noted.

“Fixed income has the yield, potential for return, risk profile and staying power that many are seeking. We are in a new golden age of bond investing.”

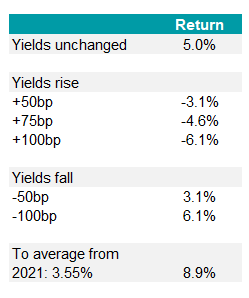

The table below summarises the returns Insight expects a US core bond portfolio to deliver in four scenarios: yields remain unchanged and central banks keep rates on hold; yields rise; yields fall as rates are cut; and yields return to their average levels since 2021. Total returns look attractive in most of these scenarios; yields would have to rise by 75-100 basis points for core bonds to lose money.

Total returns from a US core bond portfolio in relation to yields

Source: Insight Investments

Gimber is also bullish on bonds, which offer diversification against a slump in the global economy as well as income. “You are being paid to wait for something to go awry in the economy,” he said.

Short-dated bonds are most sensitive to central bank rate changes. One to three-year gilts, in particular, could benefit given that prices rise when yields fall, said Daniele Antonucci, chief investment officer of Quintet Private Bank. Within its balanced portfolios, Quintet has increased its exposure to gilts after being underweight for some time.

Other market participants have done likewise, said David Katimbo-Mugwanya, head of fixed income at EdenTree Investment Management. “Shorter-dated bond yields have recently declined faster than those on longer-duration counterparts further out on the curve, indicating that the long-awaited shift came as no surprise to market participants.”

The start of an interest rate cutting cycle should be supportive for gilts across the curve, added David Zahn, head of European fixed income at Franklin Templeton, who is maintaining a long duration position in gilts.

Conversely, Emma Moriarty, a portfolio manager at CG Asset Management, is staying away from long-dated gilts, which she believes are mispriced. If the Labour government increases gilt issuance to plug the “fiscal black hole”, that would exert upward pressure on gilt yields, she explained.

Currency markets

The BoE’s announcement put pressure on the pound today following a strong year so far for sterling. Van Luu, global head of solutions strategy for fixed income and currencies at Russell Investments, said sterling was “vulnerable to a short-term correction” after investors had built up significant long positions in the currency.

Zahn disagreed, saying that the impact on sterling should be “rather muted” given that the BoE is moving in line with the ECB and the Fed is expected to cut soon.