SUPR currently yields 8% and trades at a discount to NAV of 16%.

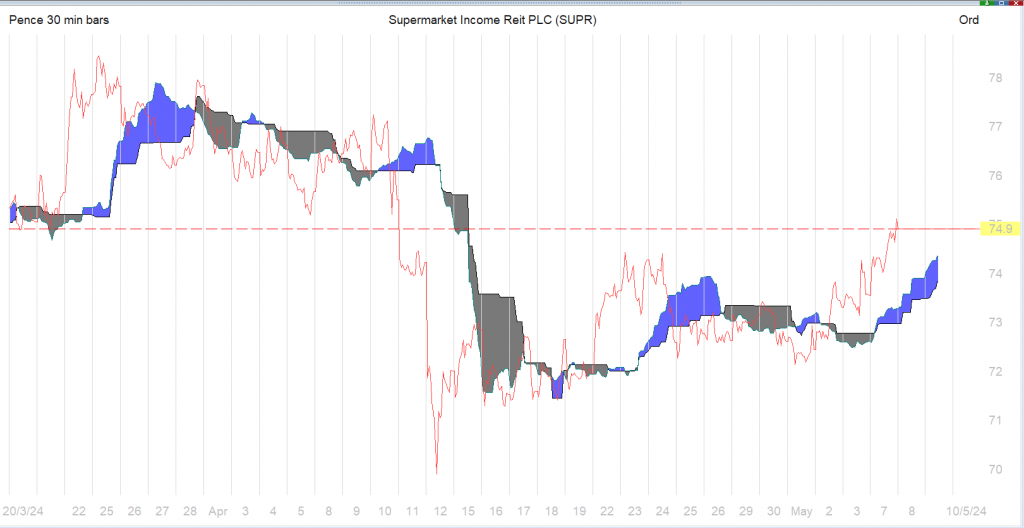

If u study the chart SUPR traded above its NAV and may do so again when interest rates fall. The NAV rises as rents are received and falls back as dividends are paid. No dividends are included in the chart. It’s been a painful period for holders of SUPR as the price fell but out of adversity there was the opportunity to re-invest the dividends because as the price falls the yield rises. The DRIP has been suspended but dealing costs have also fallen and whilst they remain low it’s not much of a fiscal drag on the portfolio.

The dividends have risen by nearly ten percent over 5 years, so IF the price was 100p in five years time the dividend could be 6.5p, a yield of 8.5%. The price would have to rise substantially or the yield to be cut to consider selling the Trust. Maybe some shares could be sold to book a ‘profit’ but that would depend on the yields available in the market at the time.