From his book How to Make Money in Stocks, he lists twenty one costly mistakes, which I will post over the next few weeks.

Temple Bar Investment Trust Plc – Annual Financial Report for the year ended 31 December 2025

20th March 2026

Temple Bar Investment Trust Plc

Annual Financial Report for the year ended 31 December 2025

London, 20 March 2026 – Temple Bar Investment Trust Plc (LSE:TMPL), the UK-listed investment company that focuses on intrinsic value and long-term growth by investing primarily in UK-listed securities, has today announced annual results for the year ended 31 December 2025.

Highlights:

- Net Asset Value (“NAV”) total return with debt at fair value of +33.9% (2024: +19.9%) once again exceeding the Benchmark, the FTSE All-Share Index, which delivered +24.0% (2024: +9.5%)

- Share price total return of +45.3%, (2024: +19.1%)

- Dividend of 15 pence per ordinary share – an increase of 33.3% (2024: 11.25 pence), representing a yield of 4%

- The Company’s market capitalisation is £1.1bn at the time of writing, up from £776m at the start of 2025

Charles Cade, Chairman of Temple Bar Investment Trust comments:

“2025 was another strong year for the Company’s performance, both in absolute terms and relative to the FTSE All-Share Index, the Company’s benchmark. The Net Asset Value total return with debt at fair value was +33.9% and the share price total return was +45.3%, compared with a total return of +24.0% for the Benchmark.

“Returns were primarily driven by stock selection rather than broader market movements, reflecting the Portfolio Manager’s focus on company fundamentals, valuation discipline and active engagement with investee companies.

“The Board continues to monitor the Company’s net revenue position closely and, based on the latest forecasts, expects to maintain a progressive dividend policy with future annual dividends increasing over time. It is the Board’s current intention to increase the quarterly dividends to 3.90p per share in 2026 (2025: 3.75p per share), an increase of 4.0% on 2025, representing an annualised dividend yield of 4.3%, based on the share price at the time of writing.

I am pleased to report that 2025 was another strong year for the Company’s performance, both in absolute terms and relative to the FTSE All-Share Index, the Company’s benchmark. The Net Asset Value total return with debt at fair value was +33.9% and the share price total return was +45.3%, compared with a total return of +24.0% for the Benchmark.

Since Redwheel took over the management of the Company’s portfolio at the end of October 2020, the Net Asset Value total return to the end of 2025 has been +199.8% compared with +103.7% for the Benchmark, representing outperformance of 8.9% per annum.

Dividend and Dividend Policy

Total dividends for the year amounted to 15.00p per share (2024: 11.25p per share), an increase of 33.3% and representing a yield of 4.0% at the year end.

The Board continues to monitor the Company’s net revenue position closely and, based on the latest forecasts, expects to maintain a progressive dividend policy with future annual dividends increasing over time. However, the pace of this growth is unlikely to match the significant increases seen in the past few years which have been partly due to a strong recovery in underlying dividends post-COVID, but also reflect a change in the Company’s distribution policy.

Last year, the Board recognised that many listed companies have been altering the nature of their distributions to shareholders, with substantial growth in the level of share buybacks either alongside or instead of dividends. According to Computershare’s UK Dividend Monitor, share buybacks represented 42.1% of the total distributions by UK listed companies in 2025. Unlike dividends, share buybacks by portfolio companies are not recognised as revenue in your Company’s accounts. Reflecting this, shareholder authority was obtained at the last AGM to amend the Company’s dividend policy to enhance the dividend it pays from its net revenue by using our capital reserve

Outlook

It would be easy for investors to take fright given the uncertain macro-economic and geopolitical outlook. In the UK, economic growth remains anaemic, with a rising tax burden on businesses and renewed inflationary fears following the recent surge in energy prices. It is worth recognising, though, that the Company’s performance is not closely correlated to the health of the UK economy. Indeed, the Portfolio Manager estimates that only approximately 35% of the underlying revenue of portfolio companies comes from the UK. In part, this reflects the global nature of many UK listed companies, particularly in the Oil and Mining sectors, but it is also a result of the Company’s exposure of up to 30% in businesses listed overseas.

Dividends per Share

It remains the Directors’ intention to distribute, over time, by way of four quarterly dividends, substantially all of the Company’s net revenue income after expenses and taxation. Further, an additional 3.0p per share per annum (0.75p per share per quarter) is currently paid using the Company’s capital reserves.

The Portfolio Manager aims to maximise total returns from the portfolio. The Company has paid dividends totalling 15.0p per ordinary share for the year ended 31 December 2025 (2024: 11.25p), representing a dividend yield of 4.0% at the year-end (2024: 4.1%). The Board hopes to continue sustainable dividend growth over the coming years supported by the use of the Company’s capital reserves. Further information can be found in the Chair’s Statement.

TMPL

Quote

“There are two emotions in the market fear and greed, the problem is we hope when we should fear and fear when we should hope.”

Or

We hope with a losing position that Mr. Market will make good our mistakes.

We fear that Mr. Market will take away part or all of our profit.

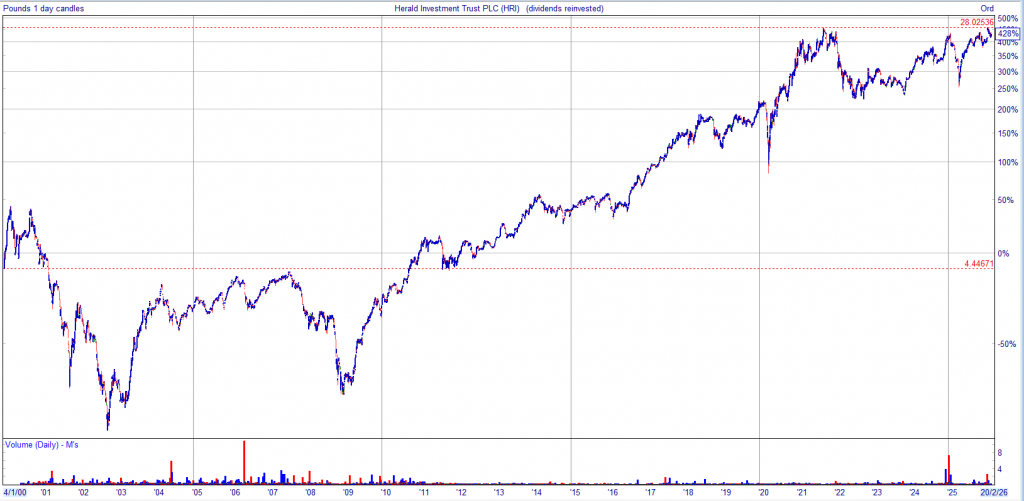

If you bought from the chart, you missed the first part of the reversal but you could have traded most of the rally. After such strong price action, you wouldn’t have needed much persuasion to take all or part profits.

You may have to wait quite a long time to see such a strong chart.

You can only get in at the bottom of a rally and out at the top by luck, so don’t waste too much mental energy beating yourself up when you don’t.

With a cloud chart, generally if the price is above the cloud the sun is shining on your trade.

In the cloud watch to see which way it breaks.

Below the cloud, it’s raining on your parade.

Mr. Market to stay in business ensures nothing works all the time.