JPMorgan UK Equity Core Active UCITS ETF – A unique approach to UK equities

- 25 March 2026

- QuotedData

- QDprime

A unique approach to UK equities

JPMorgan UK Equity Core Active UCITS ETF (JUKE) is the only European active ETF invested solely in UK equities. Now approaching its fourth anniversary, it has demonstrated an ability to outperform its benchmark, particularly over the past year. This has been achieved through a benchmark-aware, bottom up investment process driven by fundamental research and quantitative analysis, supported by risk controls, with the aim of providing modest long-term outperformance.

2026 could prove a prescient time to invest in, or increase exposure to, UK equities. The asset class has been out of favour for much of the last decade, particularly relative to the US and global markets, but sentiment has begun to shift, with 2025 delivering clear outperformance from UK shares. Over that period, JUKE has generated returns ahead of the benchmark.

Active exposure to UK equities

Launched in June 2022, JUKE provides low-cost, broad-based exposure to UK equities. Using a bottom-up, active approach, the managers adjust weightings based on fundamental research, seeking to outperform the benchmark, and, by extension, passive alternatives.

| 12 months ended | NAV total return (%) | Comparator (%)1 |

|---|---|---|

| 29/02/24 | 0.9 | 0.9 |

| 28/02/25 | 17.9 | 17.7 |

| 27/02/26 | 29.1 | 27.2 |

Source: Bloomberg, Marten & Co. Notes: 1) Vanguard FTSE All Share total return

JUKE – the only pureplay way to access UK equity exposure through an active ETF

JUKE is the only active ETF, invested solely in UK equities, currently available.

JUKE offers a distinct proposition within the European active ETF market: exposure to a portfolio of UK equities. While the active ETF market continues to expand –particularly in global equities and fixed income – JUKE remains, at the time of writing, without a direct peer.

JUKE therefore fills a clear gap in the market. Previously, investors seeking UK equity exposure faced a trade-off. They could either opt for passive ETFs, which offered low fees and transparency but no scope to outperform, or traditional active funds, which provided stock selection and the potential for excess returns, albeit with higher charges, daily dealing rather than intraday liquidity and less transparency. JUKE was designed to sit between these two approaches.

JUKE has proved popular with investors, having received net inflows in each calendar year since inception in 2022, despite the broader pressures across the UK equity sector.

Bottom-up stock selection combined with risk controls

Investors may wish to consult the fund’s website HERE

We met with Callum Abbot, one JUKE’s three portfolio managers, who provided a deep dive into the fund’s investment process. This process is active and bottom-up, combining fundamental research with quantitative analysis. Callum was clear that all investment decisions were ultimately made by a human.

JUKE is explicitly designed to serve as a “core” UK equity allocation, to either sit alongside higher risk funds (including those run by JPMorgan, such as JPMorgan UK Equity Plus Fund), or as an alternative to a passive fund. It is an explicitly “enhanced index” fund, that takes a deliberately low level of active risk.

JUKE is guided by the team’s philosophy that a portfolio that is cheaper than the market, better quality and with stronger momentum will outperform over time. Leveraging the significant research resources available at JPMorgan Asset Management, the team carries out quantitative analysis, ranking all stocks in the investment universe based on their value, quality and momentum characteristics. They also regularly converse with JPMorgan’s internal analysts and speak to external sell-side analysts.

The team explicitly avoids taking big market or macro bets. Callum’s example is that, if UK interest rates appeared likely to fall, JUKE’s manager would not systematically overweight the housebuilding sector, but might instead choose to overweight its favoured individual housebuilding stocks.

JUKE seeks to outperform its benchmark by overweighting stocks the managers believe have the greatest potential to outperform, and underweighting those with the least such potential. The index contains around 550 stocks, compared with around 145 for JUKE. JUKE can afford to ignore many of the stocks at the smaller end of the index, as those outside the FTSE 100 make up less than 20 bps of the total individually, and in many cases much less. The team seeks to avoid a long tail and will only hold smaller companies where it has particularly strong conviction.

The JUKE team use a variety of methods to provide a risk overlay, ensuring they are not inadvertently making large bets that would not be appropriate for a core fund. Firstly, all holdings are continually monitored for newsflow that may affect the team’s view of a stock. The portfolio is also subject to a monthly rebalance, in which overweighted stocks that have performed well are trimmed, and the allocations to other favoured stocks are increased. The team also uses a proprietary risk tool, continually assessing such factors as value versus growth or exposure to “AI losers”, to ensure that the portfolio is not taking unintended risks versus the benchmark. Overall, Callum reports portfolio’s turnover of around 2-3% per month. This is generally consistent regardless of overall market volatility, with the JUKE team aiming to maintain a portfolio that is not vulnerable to major events, relative to the benchmark.

UK equities: an asset whose time has come?

The UK enjoyed an extremely strong 2025.

UK equities have enjoyed a notable resurgence recently, with indices reaching record highs and delivering strong total returns in 2025. After years of lagging behind global benchmarks that are dominated by US technology giants, the UK market produced one of its best annual performances in decades, outperforming its major peers.

The recovery reflects a mix of cyclical and structural drivers. Higher dividend yields and a rotation into value and income-oriented stocks – long a feature of the UK market relative to the US – have been supportive. Performance has also benefitted from investors broadening their focus beyond mega-cap technology, alongside strength in areas such as financials, natural resources and insurance, which account for a larger share of the UK market.

Figure 1 illustrates this graphically. From launch to the end of 2024, JUKE lagged global equities, reflecting the strong outperformance of the US market relative to the UK. However, 2025 saw a marked reversal, which has extended into the opening weeks of 2026, bringing cumulative relative returns since launch close to parity with the MSCI World Index.

Figure 1: JUKE’s NAV total return relative to MSCI World Index, rebased to 100, since launch to 28

February 2026

Despite this positive recent run, the JUKE team describes the UK market as standing on a large discount to many other markets; for example, the US market continues to trade at around a 50% premium to the UK. Based on forecast earnings growth of more than 10% for the next few years, and a dividend yield of close to 4%, the team believes a strong case can be made for a good total return even without any further re-rating. The UK market has significant exposure to sectors like mining, energy and banks that offer investors genuine diversification and JUKE’s manager believes these are well placed for further upside given where they currently are in their cycles.

Current overweight positions – examples

Serco

Serco is an outsourcing company providing services to government across defence, transport, justice, health and immigration. The position was originally purchased on valuation grounds. Since then, the company has secured some important contract wins, which have helped drive a re-rating but, while the valuation is now not as compelling, for JUKE this has been replaced by a positive momentum story.

Coca-Cola HBC

Coca-Cola HBC (formally Coca-Cola Hellenic Bottling Company) is the third largest Coca-Cola anchor bottler (a large, strategically important bottling partner), which operates across multiple markets in Europe and further afield. The JUKE team particularly likes the company’s exposure to higher growth developing markets, where rising incomes and increasing urbanisation are supporting strong demand for soft drinks.

Domestic banks

UK domestic banks had an exceptional year of share price growth in 2025. However, their valuations are still only roughly in-line with their long-term averages, despite what JUKE’s manager believes is an above-average cycle for the sector. Interest rate exposure in the sector is hedged, meaning that the benefits from the recent period of higher rates is spread over the longer term. The banks seem to have more regulatory and political support than in the recent past, and – despite the UK economy’s struggles – there is still potential volume growth for the sector.

Construction

The construction industry has become more disciplined recently, limiting its exposure to fixed-price contracts following a series of costly setbacks in the past. End markets continue to see significant investment – for example new schools and hospitals – leading to stronger order books. Callum says that companies such as Morgan Sindall are benefitting from the push for office fitouts from companies coaxing workers back to the workplace.

Current underweight positions – examples

REITS

The Real Estate Investment Trust (REIT) sector is highly sensitive to interest costs, so the current environment of higher rates after a prolonged period of near-zero rates is unhelpful. In addition, JUKE’s manager believes that the REIT’s underlying assets are of relatively poor quality, particularly in the retail and office subsectors.

Beverage companies

Companies such as Diageo have had a difficult period recently. Partly this is cyclical, with consumers’ inventories of – in particular – spirits taking some time to unwind, given the surge of buying during Covid. Also, the steep price increases during the pandemic now require incomes to catch up. There is also the longer-term structural issue of whether people are drinking less alcohol, and whether this trend will persist. Although the JUKE team believes the evidence for this remains inconclusive, the issue is casting a shadow over the sector.

Structure

JPMorgan UK Equity Core Alpha is listed on a number of exchanges (see Figure 2), with both distribution and accumulation classes available. All share classes are denominated in sterling.

Figure 2: JPMorgan UK Equity Core Active UCITS ETF, available exchanges

| Distribution | Accumulation |

|---|---|

| London Stock Exchange: JUKE LN | London Stock Exchange: JUKC LN |

| Cboe DXE (Chicago): JUKEX I2 | Cboe DXE (Chicago): JUKCX I2 1 |

| Tradegate (Deutsche Boerse): BBLE TH | Tradegate (Deutsche Boerse): BBLD TH |

| Swiss Exchange: JUKC SW |

Source: JPMorgan Asset Management, Bloomberg. Notes: 1) Pending listing

Liquidity & spreads

Figure 3: Average daily liquidity and bid-ask spread of share classes, 12 months to 3 March 2026

As shown in Figure 3, trading is dominated by the two London share classes, which also have the lowest average bid-ask spread, at below 0.3%. There is trading in the other classes but it is limited, and often at a much wider spread.

For consistency, we have referred to the fund throughout this note by the ticker JUKE, on the basis that the default for many investors is to hold the distribution class.

Tracking error

JUKE’s tracking error is low.

JUKE’s one-year tracking error to 28 February 2026 was 1.3%, measured as the standard deviation of the difference between its returns and those of the benchmark. This is at the lower end of expectations for an active ETF, even one with a broadly quantitative approach and a holdings profile still close to the index. It suggests limited return divergence, albeit with scope for modest outperformance.

Callum explains that the team operates with a “risk budget” for divergence from the index. Much of this is focused on stock selection, where the team believes it has an edge. There is 30-50 bps of active positioning at a stock and sector level, with a typical active share of 18-20%.

The monthly rebalance ensures that JUKE continually reverts to the level of risk that the team aims for.

Fees

JUKE’s fees are very competitive.

JUKE’s total expense ratio (TER) is 0.25%, covering the management fee as well as custody, administration, audit and regulatory costs. The fee accrues daily and is reflected in the NAV. It excludes portfolio transaction costs and investor-level costs such as bid-ask spreads and brokerage commissions.

Callum describes JUKE as the lowest cost way of accessing JPMorgan’s active UK range of funds.

JUKE’s TER is higher than that charged for passive ETFs, which typically charge between 0.12% and 0.22%. However, given the active approach, which is absent in passive products, the fee remains competitive.

Top 10 holdings

JUKE’s top ten holdings are the same as the benchmark’s.

JUKE’s top 10 holdings mirror those of the benchmark, although the weightings differ in each case. The largest overweights are to Shell and Rio Tinto, while the biggest underweight is to Unilever. The top 10 is marginally more concentrated than the index, a pattern reflected across the portfolio as a whole: JUKE holds around 145 stocks versus around 550 for the benchmark, 240 of which sit within the broader financials sector.

For the purpose of this report, we have used the Vanguard FTSE All Share Index Unit Trust income units, which seek to track the returns of the FTSE All-Share Index.

Figure 4: Top 10 holdings as at 31 January 2026

| Holding | Sector | Allocation 31 January 2026 (%) | Comparator(%) | Relative |

|---|---|---|---|---|

| HSBC | Banks | 8.0 | 7.8 | 0.2 |

| AstraZeneca | Pharmaceuticals | 7.3 | 7.2 | 0.1 |

| Shell | Oil & gas | 6.0 | 5.7 | 0.3 |

| Rolls-Royce Holdings | Aerospace & defence | 3.8 | 3.6 | 0.2 |

| Unilever | Personal care | 3.4 | 3.8 | (0.4) |

| British American Tobacco | Tobacco | 3.2 | 3.3 | (0.1) |

| GSK | Pharmaceuticals | 2.9 | 2.7 | 0.2 |

| Rio Tinto | Industrial metals & mining | 2.8 | 2.5 | 0.3 |

| BP | Oil & gas | 2.7 | 2.6 | 0.1 |

| Barclays | Banks | 2.5 | 2.4 | 0.1 |

| Total of top 10 | 42.6 | 41.6 |

Source: JPMorgan Asset Management, Marten & Co

Asset allocation

While still broadly aligned with the benchmark, JUKE’s sector allocation shows greater divergence than is typical for an “index plus” active ETF. As Figure 5 illustrates, the fund is overweight in 10 of the 11 largest sectors, with only gas, water & multi-utilities sector underweight. These are offset by a 3.6% underweight to the catch-all “others” category.

Figure 5: JUKE sector allocation as at 31 January 2026

Figure 6: JUKE sector allocation relative to comparator (%)

Performance

Relative performance has been strong, particularly recently.

Figure 7 shows that JUKE has delivered a small but meaningful outperformance of the comparator. Returns tracked the index closely during the first 18 months after launch, but performance diverged positively from the start of 2024 and then over most of 2025. Notably, April 2025 saw a sharp positive uplift in relative performance, during the aftermath of President Trump’s “Liberation Day” tariff announcements which triggered significant market volatility.

Peer group

JUKE is the only European active ETF, currently available, that invests mostly or solely in UK equities. As such, there is no relevant peer group to compare it with.

Figure 7: JUKE’s NAV total return relative to comparator, rebased to 100, since launch to 28

February 2026

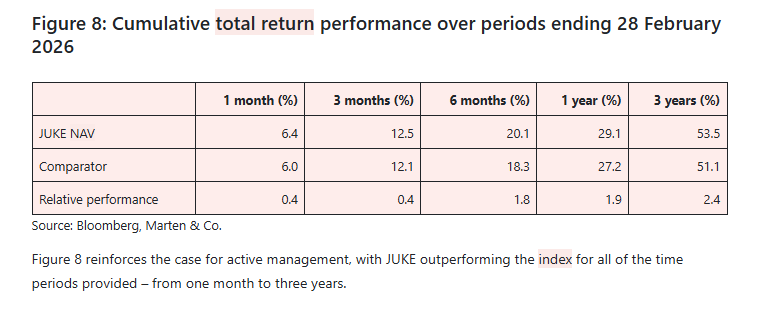

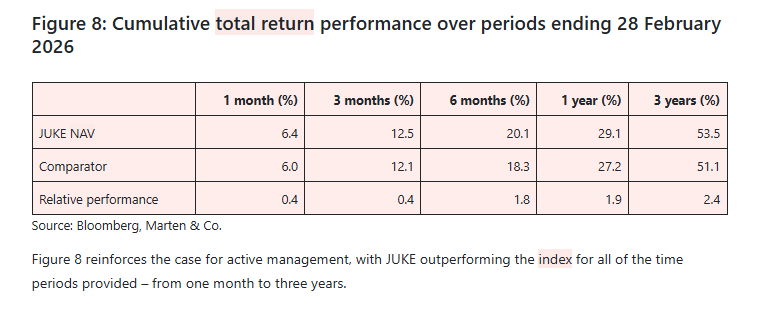

Figure 8: Cumulative total return performance over periods ending 28 February 2026

Source: Bloomberg, Marten & Co.

Figure 8 reinforces the case for active management, with JUKE outperforming the index for all of the time periods provided – from one month to three years.

Dividends

All income is returned to shareholders.

JUKE has both income and accumulation share classes. Its policy is to pass through cash dividends received from underlying holdings to shareholders, either through periodic distributions payouts or reinvestment, rather than retaining income within the fund. Dividends for the income class are typically paid quarterly.

The most recent dividend was 18.93p per share, paid on 6 February 2026, following distributions of 23.9p in November, 31.24p in August and 27.83p in May. Total distributions for the year were 101.9p, equivalent to a yield of 2.6% on the share. price of £38.99 on 20 March. Investors should note that JUKE’s yield may, at times, be higher or lower than that of the index.

Management

JUKE is a sub fund of the JPMorgan ETFs (Ireland) ICAV, an umbrella structure with segregated liability between its sub-funds. It has three named managers: Callum Abbot (14 years at the firm), Christopher Llewelyn (41 years) and Richard Morillot (16 years), giving the team deep experience. Callum and Richard focus on stock selection, while Chris focuses on implementation.

The portfolio management team is part of the international equity group, which comprises 76 investment professionals. Through the proprietary investment platform Spectrum, research is shared openly, fostering a high degree of collaboration across insights, analysis and company meetings.

The fund is managed by J. P. Morgan Asset Management, the asset management division of JPMorgan Chase & Co. The firm is one of the largest investment managers globally, operating across developed and emerging markets with dedicated investment platforms in the UK, Europe, the US and Asia. The firm manages a broad pool of institutional, intermediary and retail assets, offering active index and alternative strategies. Oversight, risk management and regulatory compliance are embedded within JPMorgan Chase’s group-wide governance and control framework.

Part of the deferred compensation of JUKE’s managers goes directly into the funds that they run.

If you had held last year, you take out your profit, keep your capital in the ETF and re-invest into the higher yielding shares in your Snowball and wait for history to repeat.

Leave a Reply