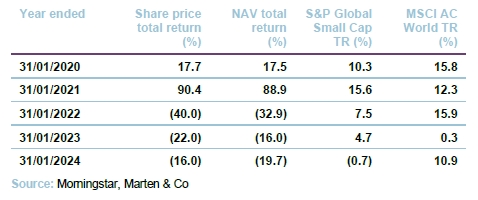

Edinburgh Worldwide – “The opportunity is as exciting as ever”

- 13 February 2024

- QuotedData

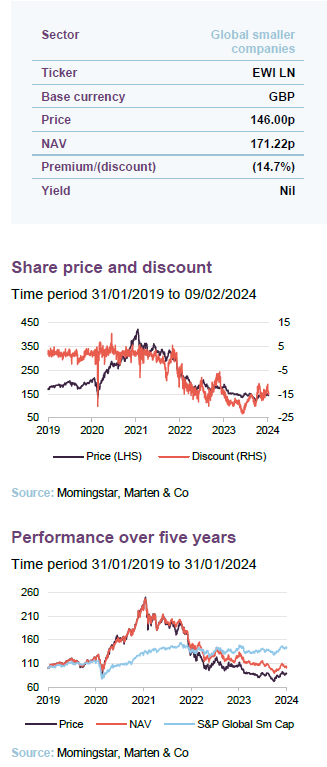

Edinburgh Worldwide

Investment companies | Update | 13 February 2024

“The opportunity is as exciting as ever”

As the rate of inflation continues its descent (barring a small bounce in the UK in December 2023) interest rates look likely to fall. Growth stocks have been recovering and Edinburgh Worldwide (EWI), the most growth-focused of the global smaller companies trusts (see pages 22 and 23) has seen a pickup in its relative performance.

Within the portfolio, valuations are relatively low, and history suggests that we are only at the beginning of what could be a significant period of outperformance.

EWI shareholders could benefit further as this should trigger a narrowing of EWI’s own wider than average discount (see page 27). At the same time, EWI’s managers say that the portfolio remains operationally resilient, technological transformation is continuing, and “the opportunity is as exciting as ever”. Reflecting this, team members have been adding to their EWI shareholdings.

Capital growth from entrepreneurial companies

EWI aims to achieve capital growth from a global portfolio of initially immature entrepreneurial companies, typically with a market capitalisation of less than $5bn at time of initial investment, which are believed to offer long-term (over at least five years) growth potential.

Fund profile

EWI is an investment trust which invests globally in a portfolio of listed and private companies. It aims to profit from a global portfolio of initially immature entrepreneurial companies, typically with a market capitalisation of less than US$5bn at the time of initial investment, which are believed to offer long-term growth potential.

Long-term growth potential

The board chooses to compare the trust’s performance to the S&P Global Small Cap Index (total return in sterling). However, the composition of the index has no bearing on the manager’s choice of stocks or position sizes. As evidence of this, the active share at the end of December 2023 was about 99% (relative to the S&P Global Small Cap Index.

To achieve a spread of risk, the portfolio should have between 75 and 125 holdings and have exposure to at least six countries and 15 industries. No more than 5% of the portfolio will be invested in a single security (at the time of acquisition).

The trust was launched in 1998 but did not adopt its current strategy until 31 January 2014.

EWI’s AIFM is Baillie Gifford & Co Limited, a wholly-owned subsidiary of Baillie Gifford & Co.

Douglas Brodie is the lead manager on the trust and its open-ended equivalent Global Discovery. He is supported by two deputy managers – Svetlana Viteva and Luke Ward – along with two analysts and two product specialists. Collectively, they make up the global discovery team within Baillie Gifford. Some more biographical details are provided on page 30.

The wider firm had £225.7bn of AUM at 31 December 2023 and the global discovery team was managing £2.3bn of that.

Exposure to unlisted securities

Up to 25% of the portfolio (at the time of investment) may be invested in unlisted securities (shareholders approved the increase from 15% to the current limit at the AGM in February 2022).

Up to 25% of the portfolio may be invested in unlisted securities.

At the end of December 2023, 23.9% of EWI’s portfolio was in unlisted securities, some of which are discussed from page 14 onwards. The board and the managers believe that for EWI to gain access to the most exciting immature entrepreneurial companies, increasingly it must have the flexibility to invest across private and listed companies. The reason being that technological advances have lowered the initial capital requirement needed to establish and scale many companies.

The quantum of funding available to promising private companies is considerable. Entrepreneurs may never need to turn to public markets for growth capital, instead choosing to use an IPO as a means to provide liquidity for backers once the business is large and mature.

The small company effect

As we have discussed in our previous notes, a key reason for making an allocation to smaller companies is that, while often perceived as being riskier and therefore more volatile, smaller companies tend to outperform larger companies over the longer term (this is sometimes referred to as the small company effect). This can be due to a variety of factors, but experience tells us that it is intrinsically easier for a smaller company to grow, perhaps doubling or quadrupling in size in a relatively small space of time, than it would be for a comparable much larger company.

It is intrinsically easier for a smaller company to double or quadruple in size.

Many reasons for the small company effect are often cited, including a tendency towards greater nimbleness (smaller companies tend to have less-complex structures that might otherwise prove a barrier to innovation) and a greater range of opportunities due to their size (larger companies are more likely to have to exclude a range of opportunities that are not sufficiently large to meaningfully impact their performance). It is also true that smaller companies are more likely to be in less mature industries where new products are naturally creating new demand and these companies are able to benefit from lower competitive pressures in a market that is naturally expanding. Although there are exceptions, larger companies tend to be in more mature industries where growth can be harder to come by, particularly if a significant element of this has to come from taking market share from competitors.

It is easier to grow in a new industry that is creating its own demand.

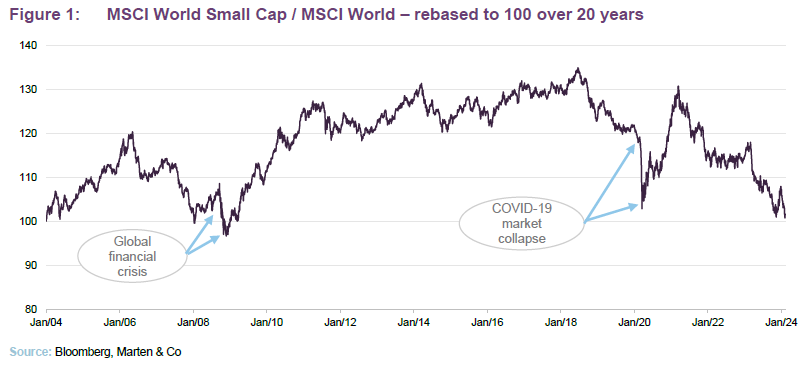

Figure 1 illustrates the performance of global small caps versus global large caps over the last 20 years. It shows that, while there have been distinct periods where global small caps have been out of favour and have underperformed global large caps, these tend to give way to periods of recovery with small caps providing strong outperformance.

As inflation in developed markets peaked some time ago and interest rates now appear to be on a path of retrenchment, growth stocks whose valuations were disproportionately affected by rising interest rates look set to benefit from a strong re-rating from the relatively low valuations that these stocks are trading at versus their own history.

Small cap equities look very cheap versus their history.

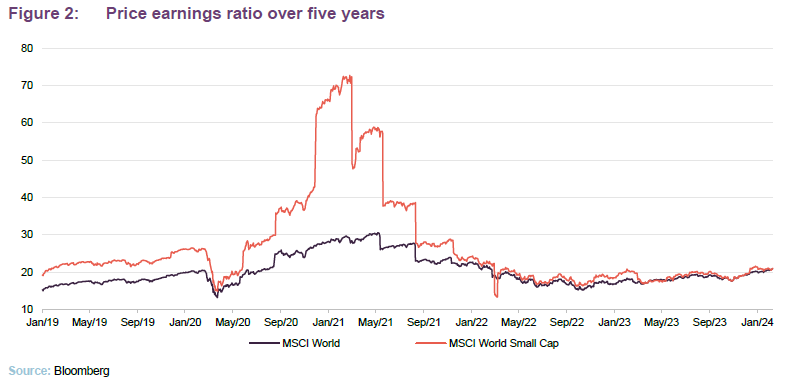

As Figure 2 illustrates, global small caps have tended to trade at a marked premium to global equities as a whole (arguably reflecting their superior growth prospects) but, despite valuations edging up over the last 18 months, small caps still look attractive (a current P/E of 21.1x versus a five-year average of 26.9x), while large caps are close to their longer-term average (a current P/E of 20.7x versus a five-year average 20.3x). We reiterate or view that, when coupled with EWI’s own wider than average discount (see Figure 38 on page 27), this still represents an attractive entry point for the long-term investor.

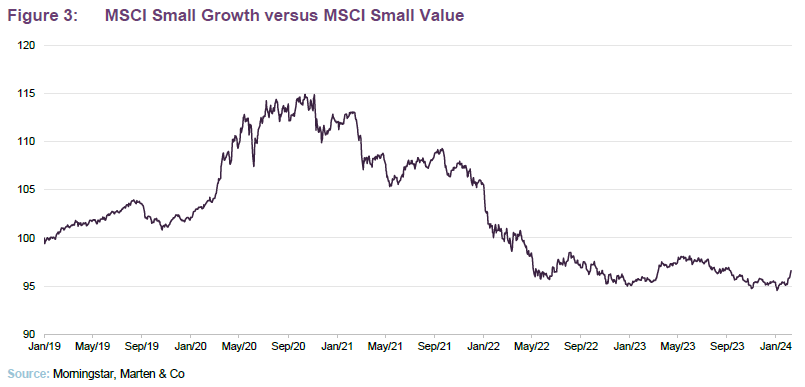

As Figure 33 on page 23 illustrates, EWI’s focus is on small-cap growth stocks and, while the performance of small cap growth versus small-cap value appears to have stabilised recently (see Figure 3), it is clear that small-cap growth suffered heavily from the rotation out of growth into value that began in late 2020. As explained above, we think that small cap growth is well positioned for a recovery from this nadir.

As Figure 33 on page 23 illustrates, EWI’s focus is on small-cap growth stocks and, while the performance of small cap growth versus small-cap value appears to have stabilised recently (see Figure 3), it is clear that small-cap growth suffered heavily from the rotation out of growth into value that began in late 2020. As explained above, we think that small cap growth is well positioned for a recovery from this nadir.

The impact of generative AI

The release of Chat GPT-4 in March 2023 jumpstarted a period of mania in markets for anything related to artificial intelligence (AI), which led to a remarkable run of outperformance for the ‘magnificent seven’ mega-cap tech stocks with exposure to the theme: Apple, Microsoft, Amazon, Alphabet, Meta, Nvidia and Tesla. These stocks were collectively up 80% over the year, while the remaining 493 stocks that make up the S&P 500 index were relatively flat at around 5%.

The release of Chat GPT-4 started a period of AI-related mania in markets.

Generative AI has been an incredibly hot topic and, as markets have settled after this initial sprint, EWI’s managers have been doing a lot of work reflecting on its impact – looking not just at primary effects but also second order impacts. For example, within the portfolio, Upwork is becoming more profitable as it is getting paid to find AI talent, while CyberArk has been doing well as cybersecurity has moved up most businesses’ agendas. As a result, EWI’s managers have evolved their thinking, and this has given rise to some portfolio changes.

Hardware 2.0

Traditionally, hardware and software have been seen as very different businesses that require different skill sets and have significantly different drivers and revenue streams. For decades, software – aided by higher IP and greater defensive moats – is where the bulk of value-adding innovations have arisen.

The lines between hardware and software are becoming blurred.

Hardware, in comparison, has been a much more commoditised business. The industry innovated, but with competition limiting the ability of the industry to expand margins, it has tended to be the case that software businesses have built on hardware’s development successes and captured a disproportionate amount of the value added. Microsoft was always touted as a better investment than IBM, for example. However, because of the impact of AI on the development of software, all of this is changing and the lines between software and hardware development are increasingly being blurred.

Increasingly, value-creating innovation has been coming through on the hardware side.

EWI’s managers observe that we are now seeing much more value-creating innovation coming through on the hardware side and they expect this trend to continue. They cite the example of 3D printers, where they say that the applications of this potentially game changing technology are being driven by the technological limits of both the hardware and software but, with software development evolving, the opportunities increasingly hinge on the capabilities of the hardware. However, whereas previously hardware and software tended to be separate businesses, to maintain a competitive advantage the two need to progress in tandem.

To capitalise on Hardware 2.0, EWI’s managers are allocating towards earlier stage companies that the market is struggling to value.

EWI’s managers say that the big question is, how do they capitalise on opportunities in the evolving hardware landscape in the market? They say that they are allocating away from more mature businesses (for example, Axon Enterprise and CyberArk) and reallocating to earlier stage growth companies (for example, Oxford Nanopore and Transmedics). They argue that the market is not yet extending its horizon far enough to value these earlier-stage hardware-orientated companies properly, which is creating an opportunity for longer-term investors such as EWI.

In the private company space – the managers have also been moving more towards holdings that are hardware-focused for the same reason, as well as those that are a key part of the AI toolset. For example, they see satellite connectivity (think SpaceX) as a game changer for AI as systems such as SpaceX’s Starlink network will allow AI to be used anywhere, with the myriad of benefits this could bring.

EWI’s managers point out that this is where the trust’s closed end structure comes into its own as many of these investments are not suitable for inclusion in an open-ended fund but EWI’s structure allows it to arbitrage this market inefficiency.

Philosophy and process

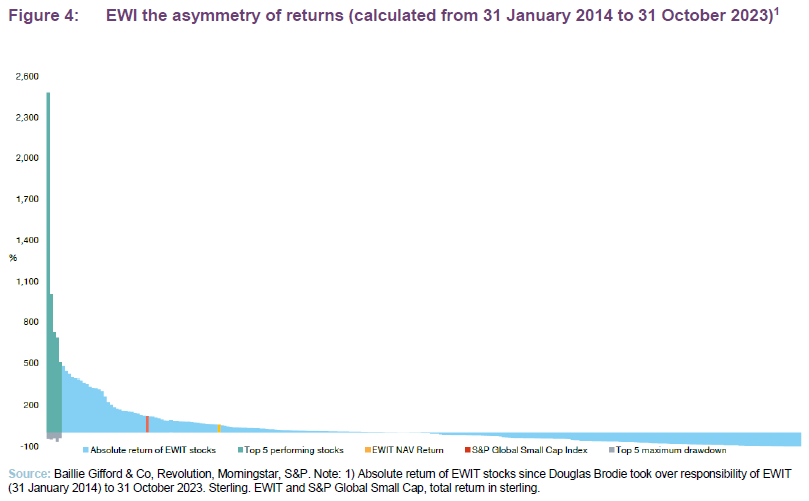

The philosophy that drives the construction of EWI’s portfolio is common to other Baillie Gifford trusts and is based on the manager’s observation of the asymmetry of returns. Only a few stocks have the ability to become global leaders in their fields and sustain that position. The rewards that accrue to them are considerable. By contrast, most companies will struggle to outperform and, as is especially the case with the younger, more immature companies that EWI focuses on, quite a few will fail. It is important that investors in EWI understand this.

Tools and technology have levelled the playing field. Advances such as the internet, cloud computing and online payments are enabling even relatively small businesses to scale fast and address a global market. If the market is global, differences in country and regional macroeconomic and political environments are much less relevant.

A true stock-picking portfolio

EWI, therefore, represents a true stock-picking portfolio, constructed without reference to index weights or to reflect the views of an asset allocation committee. The portfolio has a bias to technology, but as the managers point out, technology is everywhere.

The managers are not compelled to sell good companies on market cap grounds

Potential investments should typically have a market cap of no more than $5bn at the time of initial investment. Nevertheless, the emphasis is on identifying the winners and running with them and EWI may end up with holdings in far larger companies. EWI can act as an incubator of companies that grow to become large enough to be included in Baillie Gifford’s larger-cap strategies and identify up and coming disrupters. However, they can retain exposure to these; the managers are not compelled to sell good companies on market cap grounds.

Only a few stocks have the ability to become global leaders in their fields and sustain that position

This is not a venture portfolio – the managers tend not to consider companies less than $300m–$400m in size – but these are relatively immature companies on the frontiers of change. The uncertain outlook for these businesses makes it hard for the market to value them properly. This is especially true for those companies that are expected to become significantly profitable some years in the future. The managers believe that most of these stocks are poorly understood and that creates the space for bottom-up research to add value. The universe is vast – perhaps 30,000 companies – but most of these will not have the characteristic traits that they are looking for and some entire sectors are not a fit.

The sector is full of companies that are small and will stay that way

The managers seek to assess the potential of the business model and the risk that it does not succeed. Companies need to have a scalable business model and a clear competitive advantage. Credibility of management is very important as is an alignment between the interest of management and investors. Only a very small number of stocks fit their criteria. The sector is full of companies that are small and will stay that way.

EWI’s evergreen structure is an advantage

To deliver transformational growth, a business needs to have a culture of innovation which allows it to identify and solve problems for their customers. It often helps if they are starting with a clean sheet of paper rather than simultaneously managing the decline of an incumbent business. EWI is often a provider of growth capital and, in some instances, this could be before a company is revenue generating (as is the case with many of the trust’s healthcare investments, for example). For the companies, EWI’s evergreen structure is an advantage. It means that they can think long-term without having to be bound to the normal 10-year cycle of private equity LP funds.

Generally, the managers are not keen on situations where a number of companies are competing in the same niche, unless they can demonstrate differentiated propositions, each with their own edge. This is true of the trust’s oncology-focused stocks, for example.

EWI’s board and managers take their stewardship role seriously. However, the company will not seek to influence the strategic direction of the companies that it invests in.

EWI may end up holding a significant stake in a business (Baillie Gifford has informal caps on the size of the stakes held across all funds), especially early in a business’s life. However, the managers are mindful of the daily liquidity in listed stocks and factors that into position sizes. A typical new position will start life in the portfolio as a 0.5%–1.5% position. Where the risks associated with the business model are binary, the position size will be smaller.

Flawed investment cases trigger a sale

Sales are triggered once it is clear that the investment case is flawed. M&A activity is also a source of involuntary sales – often companies end up being taken over for less than the managers think they could be worth. In addition, positions will be re-evaluated and may be sold if the managers feel that the upside is limited.

Thanks for sharing. I read many of your blog posts, cool, your blog is very good.