The benefits of using investment trusts to build wealth through market cycles is demonstrated by a real-world example.

By Rupert Hargreaves

Investment trusts are the ideal vehicle to build long-term wealth. A real-world example recently posted on LinkedIn by investment manager John Moore makes this point well.

The portfolio was set up in 1999 and initially held Gartmore Shared Junior Zero Div (7.3% by value), English & Scottish Investors (18.4%), Finsbury Trust (18.2%), Law Debenture (19.8%), Majedie Investments (17.7%) and Scottish Mortgage (18.5%). You will notice that some of these no longer exist, while others have changed significantly.

English & Scottish Investors has undergone several reinventions. It became Gartmore Global Trust in 2002 and Henderson Global Trust in 2011. It was merged into Henderson International Income Trust in 2016 and this was then merged with JPMorgan Global Growth & Income (LSE: JGGI) in 2025.

Get 6 free issues +

a free water bottle

Stay ahead of the curve with MoneyWeek magazine and enjoy the latest financial news and expert analysis, plus 58% off after your trial.

Tracing investment trust returns back over multiple decades and mergers is challenging. However, I estimate (using Google’s Gemini AI tool) that an investment of £1 in 1999 would now be worth £7.42 in JGGI shares today – an annual return of 7.8%. The fate of the Gartmore Shared Junior Zero Dividend trust, created in 1993, was less happy. This was a split-capital trust that emerged from Gartmore Value in 1993.

During the late 1990s, split-capital investment trusts with complicated structures became fashionable. Many ended up holding the shares of other splits. This financial engineering was a disaster – when the tech bubble burst, the sector imploded under a mass of debt and cross-shareholdings. By 2003, most split structures had either collapsed or been wound up. The Financial Services Authority, the then-regulator, stepped in and set up a £194 million compensation fund in 2004.

The rest of the portfolio still exists, with some manager and strategy changes. Finsbury Trust is now Finsbury Growth & Income (LSE: FGT) and has been run by Nick Train since Lindsell Train, the company he co-founded, was appointed portfolio manager in 2000. The shares have returned 677% since then, despite recent lacklustre performance.

Why you should consider investment trusts

Majedie Investments (LSE: MAJE) traces its roots back to 1910 as Majedie (Johore) Rubber Estates, a plantation company in Malaysia and is still controlled by the founding Barlow family. In 2002, the trust backed the launch of Majedie Asset Management, which ran its investments until it was acquired by Liontrust in 2022. Today, it is a multi-manager investment trust overseen by Marylebone Partners (now part of Brown Advisory). Gemini estimates that an investment would have returned 4.1% per year between 1999 and 2026.

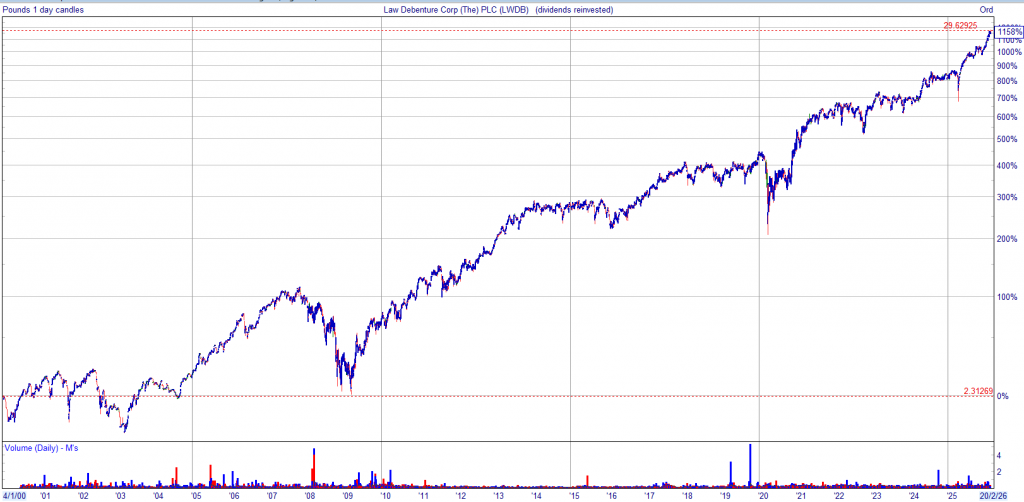

Scottish Mortgage (LSE: SMT) and Law Debenture (LSE: LWDB) will be very familiar to many MoneyWeek readers. Like Majedie, Scottish Mortgage began by funding rubber plantations in Southeast Asia in 1909, but quickly began investing more widely. Today, it holds a high-conviction global portfolio of public and private growth stocks. I calculate it has returned 16.7% since 1999. Law Debenture is a unique combination of a UK equity portfolio and a professional services business. I estimate its annual return has been 11.8%.

So this portfolio has probably returned 11%-12% per year since 1999, compared to 8.2% for the MSCI AC World index, assuming no rebalancing and dividend reinvestment. The performance of the biggest winners more than offsets the losers. Investment trusts can use their fixed capital to invest and survive market cycles that can be terminal for open-ended funds.

This is why the MoneyWeek portfolio, set up in 2012, is based on investment trusts. There have been a few changes over the years, but the goal has remained the same: a global, set-and-forget portfolio. It now holds JGGI, LWDB and SMT (and has held FGT): other positions are AVI Global (LSE: AVI), Caledonia (LSE: CLDN) and Personal Assets (LSE: PNL).

Law Debenture is a unique combination of a UK equity portfolio and a professional services business. I estimate its annual return has been 11.8%.

The obvious question is why LWDB isn’t in your Snowball or why wasn’t is added when Mr. Market gave you the chance ?

It took several years to become an overnight success and it isn’t in the SNOWBALL, although it should be, because of the low yield and when prices fall, yields rise so there are always higher yielding shares to add to the SNOWBALL.

But

This post gave me a new perspective I hadn’t considered.

This was a very informative post. I appreciate the time you took to write it.