The written plan for the SNOWBALL was to buy Investment Trusts that yielded 5% or above.

Mr. Market has been very benevolent and the plan has been increased to a base of 7% or above. This means the Snowball will achieve its ten year plan early.

I’ve therefore increased this year’s fcast to £11,200 and the target to £12,000.

The target includes some special dividends and all though it’s likely there will be more special dividends in the financial year 2027, these are not a given.

Current income for the SNOWBALL

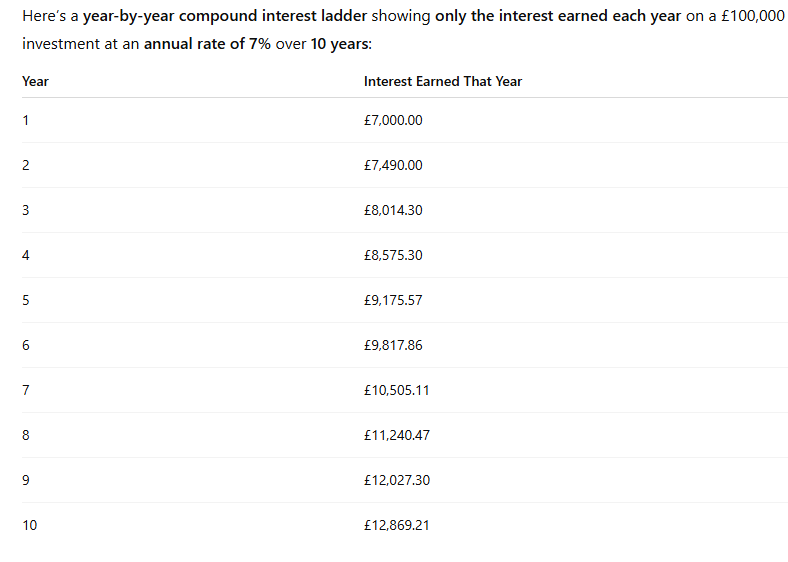

Dividends to date £4,548. Fcast dividends for first the six months £7,681 and the fcast figure for the year £13,400.

The figure of 12k is very important as that means income of 1k a month for re-investment.

The fcast for 2027 has been raised to £12,000 and the target £12,869.

If the fcast and the target is met it will mean the ten year plan has been achieved ahead of the plan.

A question I get asked a lot. Are you sure of the supply ?

Whilst when I predict the future I am often wrong, I expect that there will be a lot of consolidation in the Renewables sector so the next ten year plan could include some pair trading, investing in some higher yielding ETF’s balanced out with some safer lower yielding Investment Trusts, such as CMPI and the Dividend Hero Trusts.

A plan without an end destination, whilst better than no plan is still a bad plan as your retirement income depends on the end destination.

My friend the choice is yours. GL

A history lesson.

Canada Life figures show the 65-year-old with a £100,000 pension pot could buy an annuity linked to the retail price index (RPI) that would generate a starting annual income of £3,896. That’s up from £2,195 in the New Year following a 77% spike in rates this year.

Oct 22

I loved as much as you will receive carried out right here. The sketch is tasteful, your authored material stylish. nonetheless, you command get bought an impatience over that you wish be delivering the following. unwell unquestionably come further formerly again since exactly the same nearly very often inside case you shield this increase.

This is very interesting, You’re a very skilled blogger. I’ve joined your feed and look forward to seeking more of your excellent post. Also, I have shared your web site in my social networks!

smile

This article is a refreshing change! The author’s unique perspective and perceptive analysis have made this a truly fascinating read. I’m grateful for the effort she has put into producing such an enlightening and mind-stimulating piece. Thank you, author, for offering your knowledge and stimulating meaningful discussions through your brilliant writing!

Its like you read my mind! You seem to know so much about this, like you wrote the book in it or something. I think that you can do with some pics to drive the message home a little bit, but instead of that, this is fantastic blog. An excellent read. I will certainly be back.

Its such as you read my mind! You seem to understand a lot about this, like you wrote the ebook in it or something. I believe that you can do with some to drive the message house a bit, however other than that, that is wonderful blog. A fantastic read. I will certainly be back.

I’m amazed by the quality of this content! The author has clearly put a tremendous amount of effort into investigating and organizing the information. It’s refreshing to come across an article that not only gives helpful information but also keeps the readers hooked from start to finish. Great job to him for producing such a brilliant work!

Thank you for the good writeup. It actually was a leisure account it. Glance complicated to far introduced agreeable from you! However, how could we keep in touch?