The SNOWBALL has a comparator share, to monitor the income available from the SNOWBALL and the income from the comparator share VWRP using the 4% rule.

The fcast income for this financial year is £10,500, the actual income will be around 14k but although this extra income could be spent, it’s not guaranteed to be repeatable as it contains some special dividends.

The value of the comparator share VWRP, using 100k of seed capital is £159,642, not too shabby.

Using the 4% rule you could today withdraw income of £6385, if you use the 4% rule, it’s recommended to have a 3 year cash buffer, so you are not selling shares during market crashes.

You have to decide for yourself, how your replace your cash buffer if markets are crashing and you then have to sell shares to replenish your cash buffer, otherwise you are taking a big risk with the rest of your retirement.

One option if your plan includes taking out your tax free amount, to build 25% of your portfolio in VWRP or a similar share.

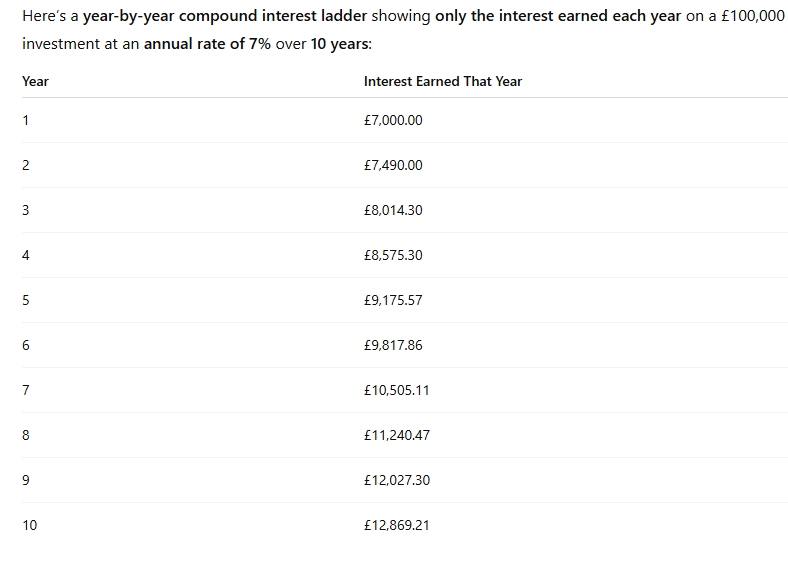

Income using and annual rate of 7% nearly doubles every ten years, if we jump to the 30 year figure, you would receive income of 51k.

The SNOWBALL is currently well ahead of the current plan but 30 years is a long, long time, so if you are not be able to re-invest at that rate every year, your journey may take longer, although with the current enhanced dividends with ETF’s it could be shorter.

The table shows that income using the SNOWBALL would be 51% of seed capital, every year without selling any shares, although it would still be your duty to check the next fcast dividends for your Snowball.

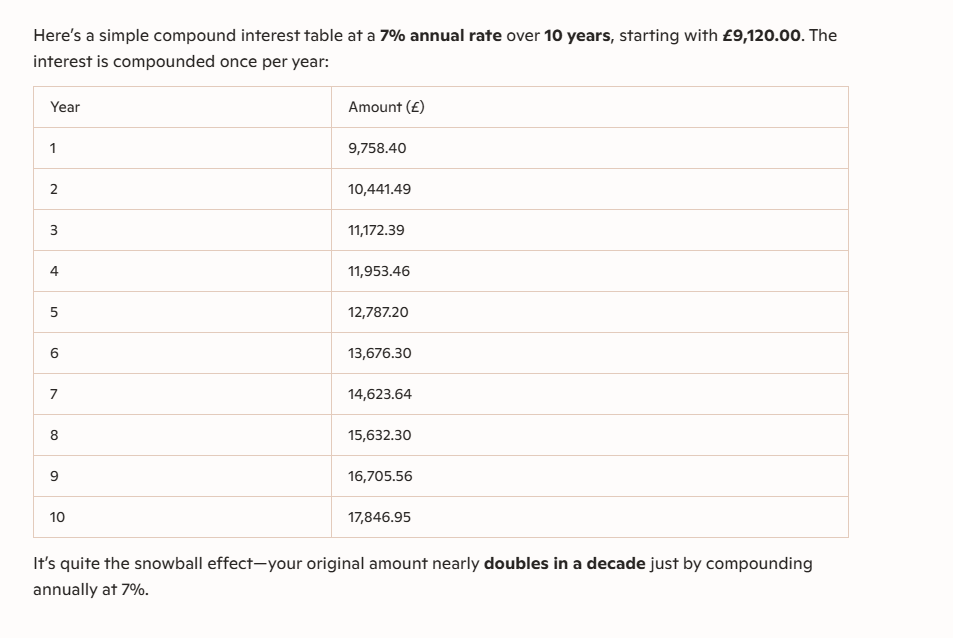

To earn income of 51k per year, VWRP using the 4% rule would have to be valued at around 1.2 million to provide the same amount of income.

Remember the quoted amounts do not take into account inflation

I am grateful for the insights shared in this article