Vanguard economic and market update: Fed rate cut signals confidence

Vanguard’s latest economic and market update, including our outlook for growth, inflation and interest rates.

Shaan Raithatha Senior Economist

Key points

- The US Federal Reserve has cut its policy interest rate for the first time in four years, by 50 basis points.

- The euro area, already in the midst of a policy easing cycle, is seeing growth after stagnation in 2023.

- In the UK, an uptick in services inflation meant the Bank of England did not cut rates at its September meeting.

The US Federal Reserve (Fed) has cut its federal funds rate for the first time in four years. The move signals the Fed’s confidence that US inflation is slowing, as well as a shift in focus to shore up the weakening US labour market. In kicking off its easing cycle, the US now joins the euro area and UK, where central banks had already begun cutting policy rates.

While the US, euro area and UK are seeing varying degrees of economic health, China may struggle to meet its growth target given lacklustre domestic demand. A strong, timely policy response will be required.

United States

The Fed cut its policy interest rate by 50 basis points (bps)1 but did so in the context of economic resilience rather than concerns about a material slowdown.

The Fed’s decision, announced on 18 September, marked a strong start to its easing cycle. The 50-bps reduction in the federal funds rate indicates a target range of 4.75%-5%. The Fed had resisted cuts at previous meetings, which allowed monetary policymakers to see more evidence of slowing inflation and gave them the confidence to cut by 50 bps rather than 25 bps.

At the midpoint of the year, GDP growth was tracking largely in line with Vanguard’s 2% outlook for 2024. The US economy grew more in the second quarter than previously thought, with real GDP rising by an annualised 3%. Strong consumer spending contributed to the growth.

The pace of headline inflation, as measured by the consumer price index (CPI), slowed again in the year to August to 2.5% compared with 2.9% in the year to July. Core CPI, which excludes volatile food and energy prices, rose by 3.2% in the year to August, little changed from July.

Recent data suggest softening in the labour market. There was a second consecutive month of below-consensus job growth, coupled with a recent pattern of downward revisions to already-announced totals. We expect job growth continuing to slow amid moderating economic activity, with the unemployment rate ending the year marginally above current levels (4.2% in August).

Euro area

The euro area is growing after stagnation in 2023. We expect steady—but not spectacular—growth in 2024 as restrictive monetary and fiscal policy constrain activity.

The European Central Bank (ECB) announced a 25-bps cut to its policy rate on 12 September. The decrease in the deposit facility rate, to 3.5%, was the second cut of a cycle that began in June with a similar 25-bps cut. Vanguard does not expect a further cut at the ECB’s October meeting, although we anticipate the easing cycle will resume with a 25-bps cut in December, followed by a quarterly cadence of 25-bps reductions in 2025.

The euro area economy grew again in the second quarter, with real GDP rising by 0.2% compared with the first quarter. This was despite an unexpected drag from Germany, where a rebound in the manufacturing sector remains elusive.

The pace of headline inflation slowed in August, driven by a drop in energy prices. Headline inflation slowed to 2.2% in the year to August—the slowest in three years—compared with 2.6% in the year to July. Core inflation, which excludes volatile food, energy, alcohol and tobacco prices, slowed marginally in August; however, services inflation remained sticky.

The unemployment rate returned to a record low of 6.4% on a seasonally adjusted basis in July, falling from 6.5% in June. We foresee little change to the unemployment rate into year-end.

United Kingdom

In the UK, the Bank of England (BoE) held rates steady at 5% in September after initially cutting in August. We expect rate cuts to resume in the fourth quarter and believe rates will end the year at 4.75%.

The BoE’s decision to keep rates unchanged reflects that risks to resurgent inflation remain, although services inflation, pay growth and GDP data have all undershot expectations since the bank’s last meeting.

GDP growth increased by 0.6% in the second quarter compared with the first. We expect the UK economy to moderate in the second half the year, growing by 1.2% for all of 2024.

The pace of headline inflation held steady at 2.2% in the year to August. Meanwhile, core CPI, which excludes volatile food, energy, alcohol and tobacco prices, jumped to 3.6% in the year to August, compared with 3.3% in the year to July. Vanguard expects core inflation to end 2024 around 2.8% and to hit the BoE’s 2% target by the second half of 2025.

Wage growth cooled to its slowest pace in more than two years in the May-July period, even as the unemployment rate fell to 4.1% and job vacancies decreased for a 26th consecutive reading during that period. We foresee the unemployment rate ending 2024 in the 4%-4.5% range.

China

Sluggish domestic demand has put China’s 2024 growth target of 5% at risk. Fiscal policy in the form of increased government loan issuance in August provides hope, but more of the same will likely be required in the months ahead.

Government loan issuance totalled 900 billion yuan in August, a significant ramp up compared with the 260 billion yuan issued in July. In order for the government to hit its 5% growth target for 2024, this is the type of timely policy response that will be required. On the monetary policy side, we expect the start of the Fed’s rate-cutting cycle could give the People’s Bank of China (PBoC) room to cut as well.

GDP grew by only 0.7% in the second quarter compared with the first and by 4.7% compared with the second quarter last year. Weaker-than-expected retail sales and industrial production figures suggest that China’s growth momentum slowed in August.

The pace of inflation, as measured by consumer prices, rose 0.6% in the year to August, below expectations and well below the 3% inflation target set by the PBoC. We expect inflation in 2024 to be mild, with headline inflation of 0.8% and core inflation, which excludes volatile food and energy prices, of just 1.0%.

The unemployment rate rose to 5.3% in August from 5.2% in July. Vanguard expects that rate to remain around current levels for the rest of the year.

The points above represent the house view of the Vanguard Investment Strategy Group’s (ISG’s) global economics and markets team as at 19 September 2024.

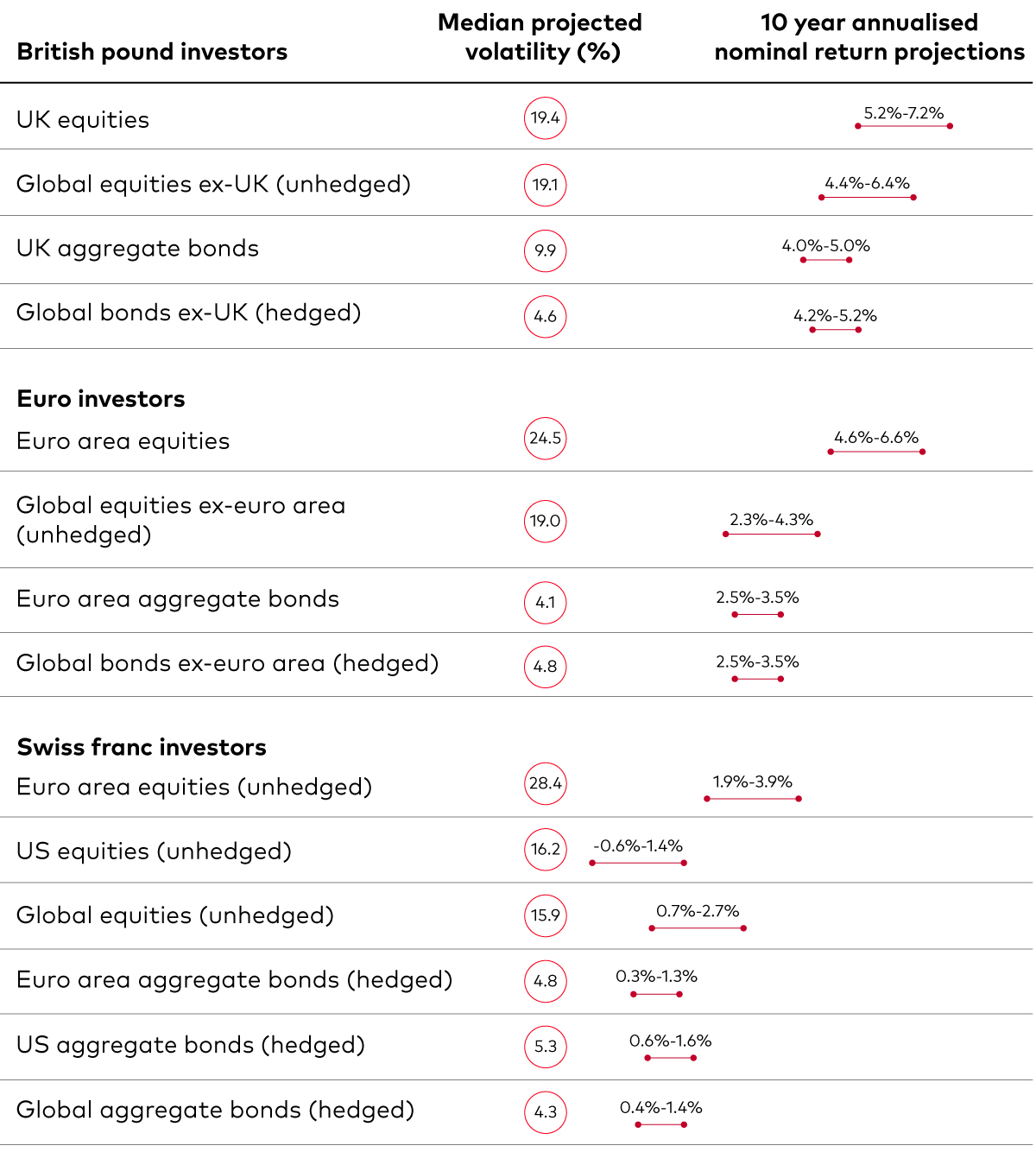

Asset-class return outlook

Vanguard has updated its 10-year annualised outlooks for broad asset class returns through the most recent running of the Vanguard Capital Markets Model® (VCMM), based on data as at 30 June 2024.

Our 10-year annualised nominal return projections, expressed for local investors in local currencies, are as follows2.

Leave a Reply