CALLING TIME ON VSL

Victory Park ends in parking a Defeat

Dear reader

I first wrote about VSL back in October 2023. It wasn’t an “idea of the year” or anything like that. It was something I already held, and the reporting had always been pretty dire so when they announced a wind down, I decided to try to write about it trying to make head or tail of it, if I could. Over 5 articles which were roughly looking at the semi-annual updates I continued to be hopeful it could turn around. The company reports showed a pathway to realisations.

The Oak Bloke’s Substack

Part of this optimism was the fact that some holdings notably WeFox was also held by Chrysalis. Good company and all that.

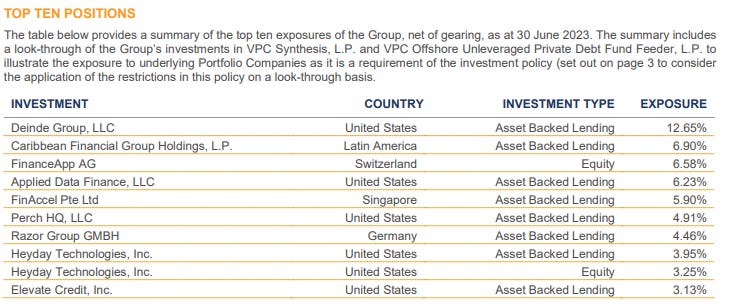

In October 2023 VSL was £200m Asset-backed loans delivering a 14% yield, £150m of near term maturities, -£75m of liabilities, over £100m of equity (plus options) and a £150m market cap. So the thesis was based on VSL info the fund would be debt free and 50% of the market cap returned before we reached 2026. That was the theory; the reality was very different.

These were asset-backed loans with great geographic diversity, a spread of counter parties, the prospect of 12% yield for several years. We’ve had no great recession, no great crisis, and the stock market has been at record levels. Rising interest rates and inflation took their toll on holdings. A lack of exit opportunities and a depressed Venture Capital and M&A environment really didn’t help either. As I write in February 2025 sentiment has improved a little but VC is hardly back to anything approaching real bullishness and positivity.

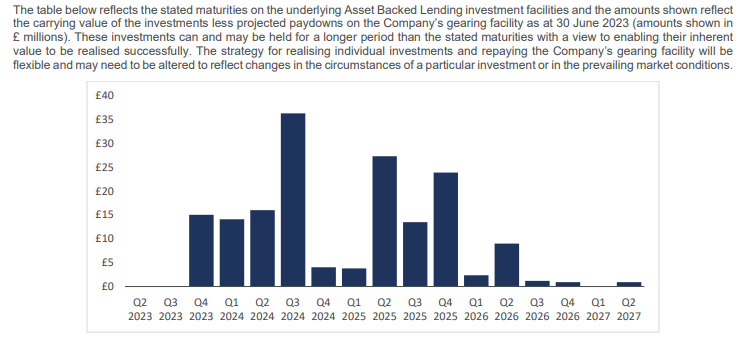

This was the near term expected cash realisations back in October 2023:

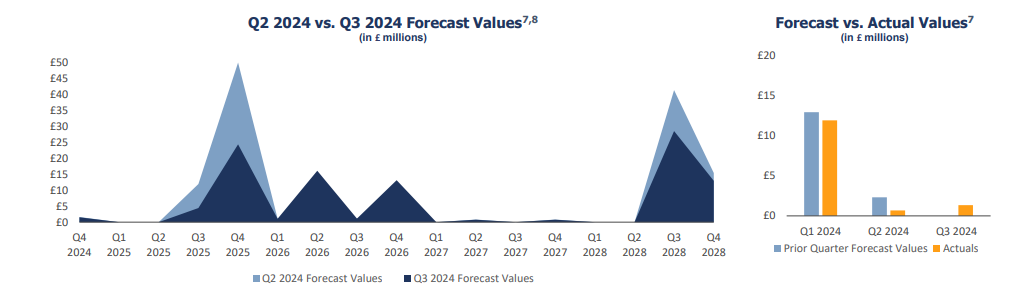

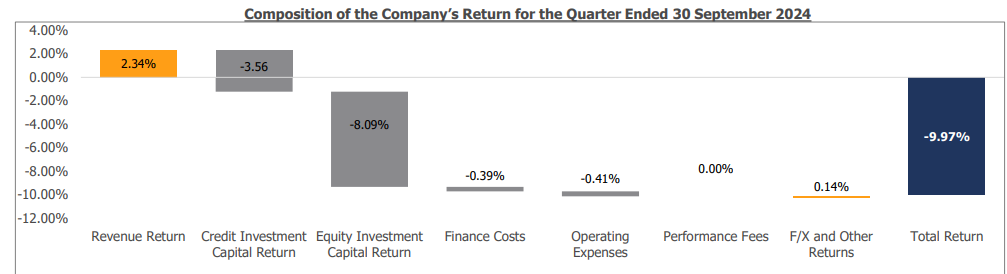

The reality however was, the timelines being reported by the fund proved hopelessly optimistic. Actual maturities have been pushed back and pushed back, quarter after quarter. Even recently this continues to happen. See 2Q24 and 3Q24 below. Have you ever known such a forgiving lender? Payment holiday no problem Mr Customer. We’ll just bump our investor cash forecast back another few years. VSL shrugs.

There have been substantial write offs of equity since October 2023 (-29.2%) but also write offs of asset-backed loans too. (-8.35%)

The fund trades on a 57% discount and once again is and “should be” very tempting. But this RNS at Christmas time was the clincher. Razor is £17m loan and £12m equity so £29m of the £167m NAV. ~20% of the NAV and ~40% of the share price.

VSL had a buy of 70.8p when I first wrote about it. I sold at just 27.2p. So a 43.6p loss. Factor in a capital return of 3.2p and dividends of 11.12p then the loss is a net 29.28p = a 41.3% loss.

Lessons to learn?

As some kind readers have pointed out you can’t win ‘em all and you win some and lose some. Inevitably the hope is to learn lessons.

Of course one lesson is to be sceptical over statements like “overcollateralised protection”. The reality was this protection proved to not be much protection whatsoever.

Should investors not take information at face value? The annual report is subject to audit and PWC were the auditors here and reported no material misstatements.

Should macro considerations have been considered more seriously? A share which lends money at high enough levels of return to sustain a 12%+ yield of course is susceptible to the danger of its customers, already burdened with expensive debt (from VSL) to implode when higher interest rates and rapid inflation tipped them over the edge. That’s entirely plausible and likely, and that is the lesson to learn here.

Anyways, this is the Oak Bloke calling time on VSL. Good luck to remaining holders.

Regards

The Oak Bloke

Leave a Reply