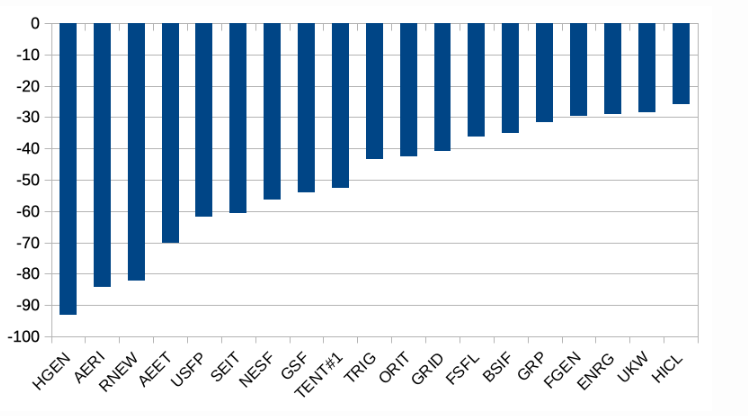

One counter intuitive aspect of energy cost rises that I wanted to flag, is just how badly UK listed Renewables Energy Infrastructure Funds (REIFs) have performed since Putin invaded Ukraine. Below is a chart showing that even the best performing funds, such as HICL and Greencoat UK Wind are down by over -25% since Feb 2022. Solar panel funds like Bluefield Solar Income Fund (BSIF) and Foresight Solar Fund (FSFL) have fared worse, down by almost -40%. Next Energy Solar Fund (NESF) and battery funds like Gore Street Energy Storage (GSF) are down by around -55%. Hydrogen One (HGEN) fell -95% as hydrogen infrastructure is capitally intensive and the returns are uncertain (sound familiar?). The shares were delisted last month.

Since Donald Trump began hostilities against Iran, performance has improved for Greencoat Renewables (GRP) +17% and Octopus Renewables Infrastructure (ORIT) +13%, but these are still down -30% to -40% over the longer term horizon in the chart above.

This can serve as a reminder that investing is not about predicting the future. If you had had perfect foresight that Putin would invade Ukraine, and the Labour governments would be keen to encourage investment in renewables as a source of energy independence, then the REIFs might have seemed like an obvious way to play this theme. The reality was that their business models suffered more from rising interest rates than they gained from rising energy costs.

Posted on 27th May 2026 | By Bruce Packard

Don’t you love markets, you make a market comment as above and then a bid arrives and the whole world of Renewables suddenly appear more appealing.

Leave a Reply