Dr James Fox explores whether it would could be possible to generate enough dividend income to live comfortably and stop working.

Posted by Dr. James Fox

Published 30 May, 2023 11:28 am BST

Like many investors, I receive dividend income from the stocks I own. In my case, dividend-paying stocks represent the core part of my portfolio. But just how much would I need to earn from dividends to live off this income alone? And would it be possible?

Let’s take a close look.

How could it work?

Well, I’d want to build a portfolio of dividend stocks that collectively pay me enough money to live from. Let’s say this is £30,000, but I appreciate this might not be possible in London.

And I’d want to be doing this within an ISA wrapper. That’s because any capital gains, dividends, or interest earned within the ISA portfolio is tax-free.

So, if I was earning £30,000 from dividends, I’d actually be taking home more money than someone on a £45,000 salary — including student loan repayments.

Of course, unless I picked specific stocks, I wouldn’t expect this income to be spread evenly across the year. At this moment, the majority of my portfolio’s income comes around April and May, shortly after the end of the financial year. So that’s something to bear in mind.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

What would it take?

Well, to earn £30,000, I’d need to have at least £375,000 invested in stocks. That’s because I believe the best dividend I can achieve is around 8%. This would involve investing in companies, like Legal & General, that don’t offer much in the way of share price gains.

But what if we don’t have £375,000? And let’s face it, the majority of us don’t.

Well, I’d need to build a portfolio over time. And I could do that using a compound returns strategy. This involves reinvesting my dividends and earning interest on my interest. It’s very much like a snowball effect.

Naturally, there are several key variables here. The starting figure, the yield I can achieve, and the amount of money I contribute from my salary every month.

If I started with £10,000 and stocks yielding 8%, in theory I could reach £375,000 in 19 years. But this would require me to contribute £400 a month and increased this contribution by 5% annually throughout those 19 years.

And by contributing £400 a month, I’d fall way under the maximum annual ISA contribution of £20,000.

Compound returns isn’t a perfect science, and as with any investment, I could lose money. But it’s certainly safer than investing in growth stocks.

About the stocks

Of course, the above is great in theory, but I’d need to pick the right stocks. I’m looking for stocks with strong dividend yields, but I also need to be wary. Big dividend yields can be a warning sign, and the dividend coverage ratio is a good place to start.

Let’s do a one eighty turn and look at the opportunity from the opposite angle, concentrate on the tail and not the body.

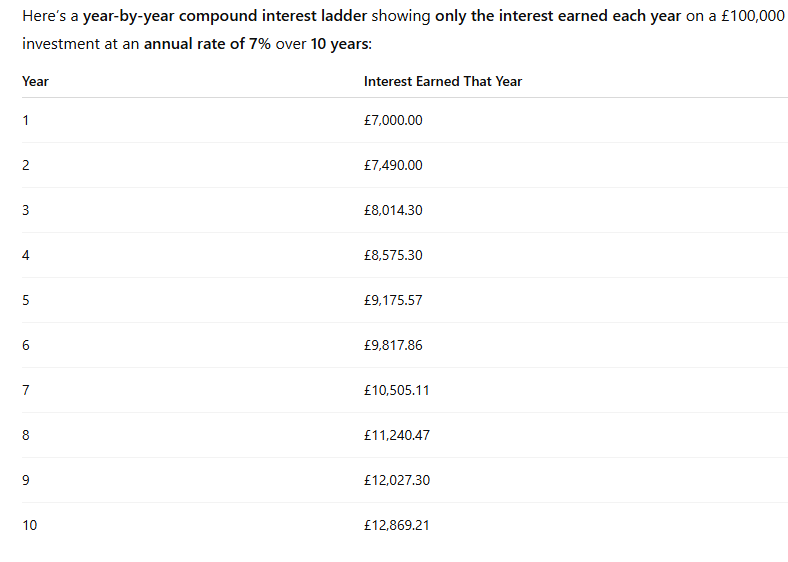

You may only have 10k of seed capital but it’s still the Snowball effect where your income roughly doubles every ten years.

So10k would earn income of £1,286, after twenty years £2,572 and after 30 years £5,144. A yield of 51% on seed capital. You have to allow for inflation but you could also add capital to your Snowball.

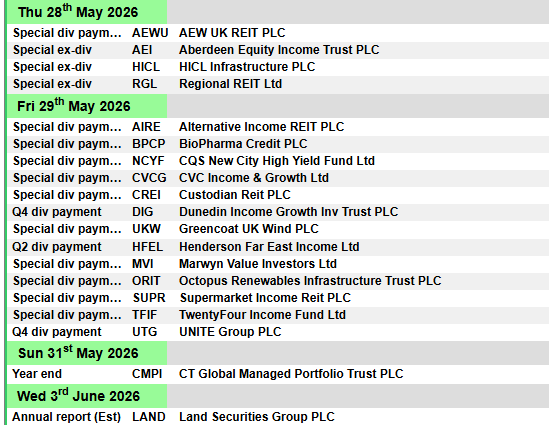

Aberdeen Equity Income Trust PLC ex-dividend date Alliance Witan PLC ex-dividend date BlackRock Greater Europe Investment Trust PLC ex-dividend date Greencoat Renewables PLC ex-dividend date HICL Infrastructure PLC ex-dividend date Regional Reit Ltd ex-dividend date Temple Bar Investment Trust PLC ex-dividend date

This 10.5% Dividend Shines as Americans Get Richer (and Are Less Happy About It)

Michael Foster, Investment Strategist Updated: May 25, 2026

There’s a clear “disconnect” happening in the US economy right now. And most investors are on the wrong side of it.

Funny thing about it is, it’s pretty obvious. We hear about both sides of it in the news daily, but few people truly see it for what it is. And the 10.5% dividend we’re going to discuss today is the perfect play on this misconception.

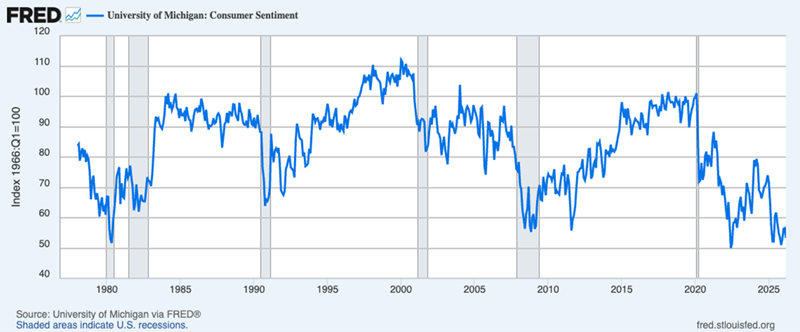

The first part of our opportunity? Consumer sentiment, which I’m sure you’ve heard is in the tank:

Here’s the University of Michigan consumer-sentiment survey over the last 50 years. At the right side of this chart we see that the current level is the lowest it’s been in all of that time.

In other words, Americans today feel worse about the economy than they’ve felt in a couple of generations, more or less. Which is where the other side of our disconnect comes in: In the last year alone, the S&P 500 has returned 25%.

That, of course, is good news for those of us who own stocks, but keep in mind that stocks do return around 10% per year including dividends, on average, so this strong gain clearly shows the value of buying for the long term and being patient.

But the disconnect between stocks’ brilliant performance and lousy sentiment raises another question: Are we headed for a correction?

That’s not what we see in the data. Not even close.

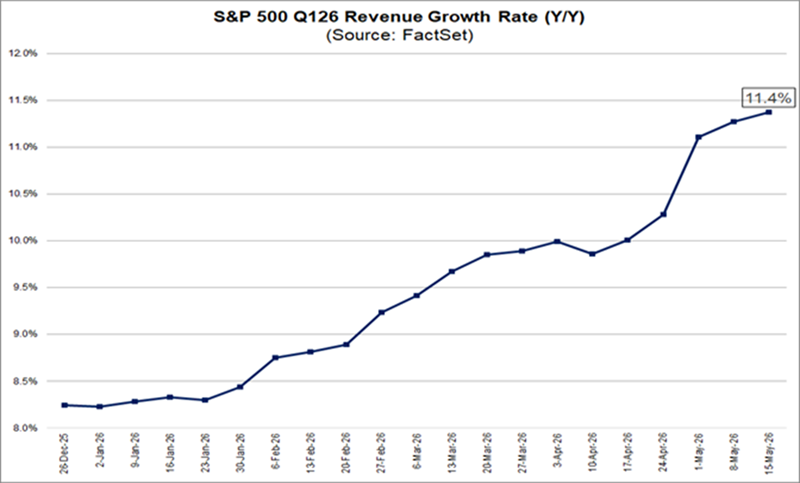

As you can see above, S&P 500 firms booked year-over-year gains north of 11% in Q1. That’s the highest since 2022, and it’s historically very high indeed.

Note also that sales growth has been accelerating for years. That’s in part due to businesses benefitting from the AI boom.

Whatever feelings we may each have about AI, there’s no denying the fact that the AI buildout is benefitting utilities, energy, infrastructure, construction, transport, retail and other industries. That’s showing up in US companies’ bottom lines—even those of some of the riskiest firms out there.

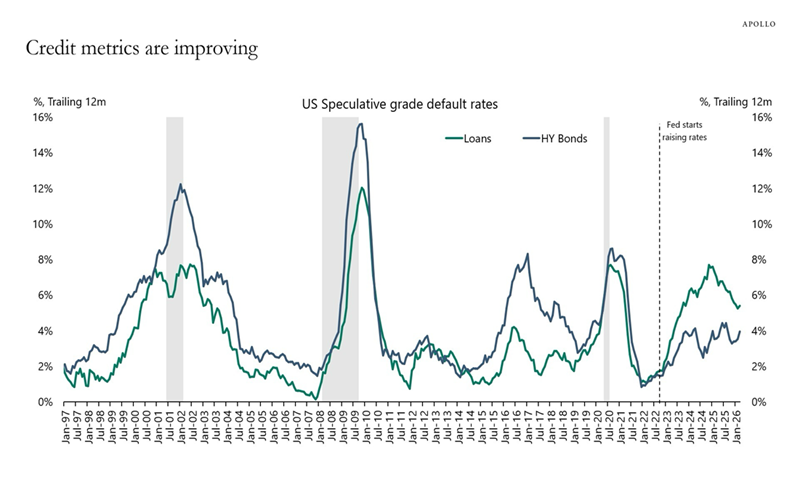

In the speculative credit market, we’re seeing default rates fall significantly. Most crucially, they’re falling fastest in the loan market, which was behind the private-credit panic late last year and earlier this year.

The bottom line is that US companies are, on the whole, doing well. But where does that leave everyday Americans?

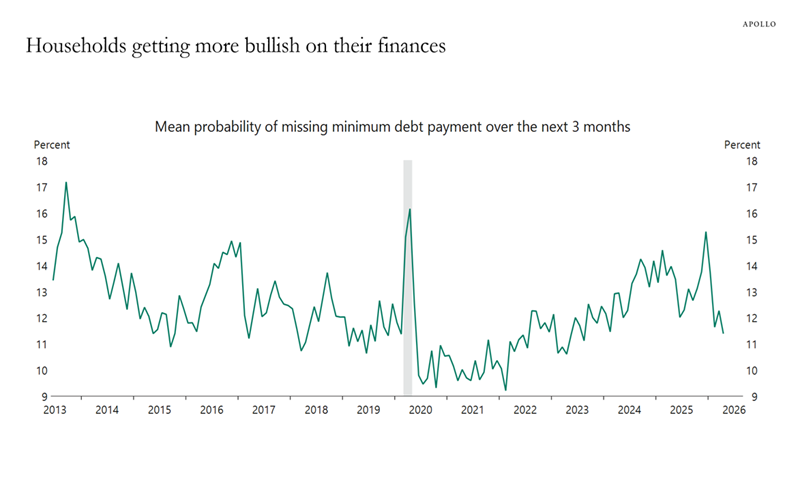

Despite their dour mood, American families have largely been financially healthy throughout this decade. As we can see above, they’re less likely to default on their debts than they were in the 2010s.

There was a trend of rising defaults earlier this decade, as pandemic-relief efforts from the Fed and US Treasury faded. But there’s been a sharp drop in defaults since early 2025. This shows that Americans’ financial health is improving. Part of that may be due to increased opportunities due to the aforementioned AI buildout.

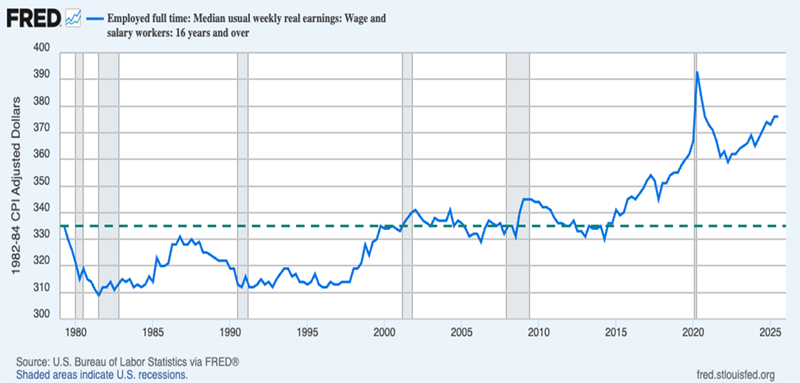

Finally, the chart above shows inflation-adjusted earnings for workers. Note how from 1980 to 2015, wages didn’t really grow at all. Then they began to gain ground in the late 2010s and have continued to rise since.

Funny thing is, Americans generally started making more money in the late 2010s, just when sentiment began to slide. That trend continues to this day, setting up an odd dynamic: People are generally getting richer—and they’re not happy about it!

It’s an odd situation, to be sure, and it sets the stage for euphoric jumps and steep drops in stocks as rising earnings and lousy sentiment battle it out. We saw the dips around a year ago, when the Liberation Day tariffs were announced, and again this year, due to the Iran conflict (and if you go further back, the deep selloff in 2022, on inflation concerns).

All of those moments were buying opportunities, and I firmly believe that will be true of any future pullbacks, too.

This 10.5% Dividend Is a Smart Play on the Earnings/Sentiment Mash-Up

This is where a closed-end fund (CEF) called the Liberty All-Star Equity Fund (USA) comes in. It’s a 10.5%-yielder that holds large cap S&P 500 stocks.

Its top holdings are NVIDIA (NVDA), Microsoft (MSFT), Alphabet (GOOGL), Amazon.com (AMZN), Capital One Financial (COF), Meta Platforms (META), Visa (V) and Wells Fargo & Co. (WFC).

And because USA is a CEF, we can get access to its holdings at a discount to net asset value (NAV, or the value of the fund’s underlying portfolio). That’s a deal that just doesn’t exist with ETFs.

It’s particularly timely in USA’s case because the fund’s already-steep discount means we don’t have to wait to buy the dip here: USA already trades at an 11.3% discount, well below the 7.5% it’s averaged in the last year and far below the 0.7% it’s averaged over the last five years.

Deals like this are difficult to track down in a rising market like this one.

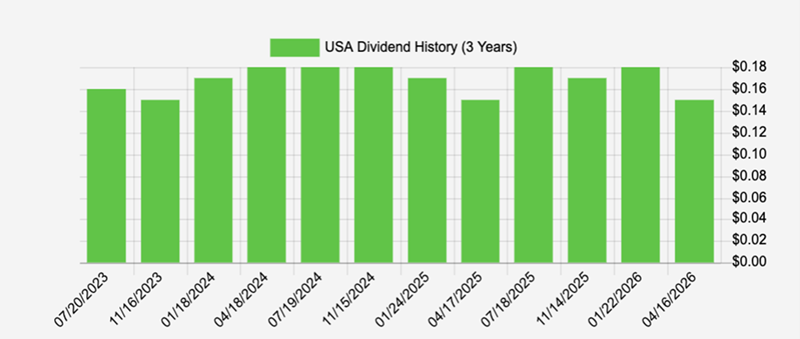

But the most exciting part is that 10.5% dividend, which USA generates by taking the returns on its holdings and “converting” them into an income stream for us. It manages that by linking the dividend to its NAV and committing to paying out roughly 10% of NAV as dividends every year.

That does mean the quarterly payout floats a bit, but we’re okay with that, since the result has been a pretty consistent dividend over the last three years:

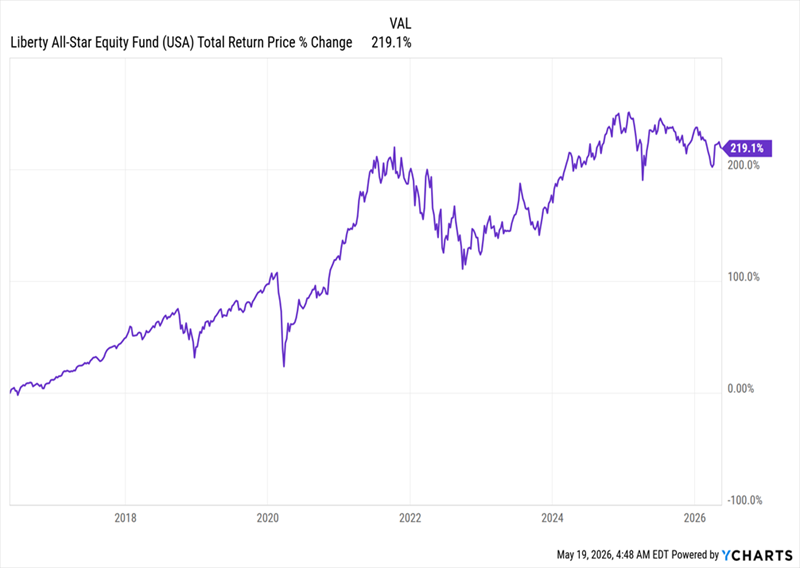

And then there is the fund’s overall performance, which has been strong:

USA Delivers a Steady Long-Term Return

USA has delivered a 12.3% annualized total return over the last decade, and it’s done so consistently, thanks to that strong portfolio.

And since the fund gives out most of its price gains as dividends, you can reinvest in USA and grow your income (and portfolio value) further. Or you could withdraw your dividends and use them to finance your lifestyle, as many retirees do.

The choice is yours, and strong CEFs with proven track records, like USA, make that flexibility possible

Low angle close up color image depicting a man holding a shopping trolley filled with essential fresh groceries in the supermarket.

Global markets are wobbling again, so UK investors looking for stocks to buy need to pay close attention to their options.

Rather than showing signs of resolution, the ongoing conflicts in Ukraine and the Middle East seem to be more uncertain than ever.

Oil prices are swinging wildly as tensions around the Strait of Hormuz increase, leading to growing uncertainty among market analysts.

As these issues drag on, more and more investors are asking: is the stock market heading for a crash?

How to prepare for a stock market downturn

This year, the Dow Jones has flip-flopped between 45,000 and 50,000, while the S&P 500 dipped to 6,340 before surging past 7,500. Meanwhile, the FTSE 100 nearly cracked 11,000 points before briefly falling back below 10,000.

When I see sharp index moves like that, I think less about predicting the next crash and more about making my portfolio resistant to risk.

A few simple actions can help:

Keep some money in cash.

Trim higher-risk positions.

Tilt a little more towards defensive shares.

That does not mean hiding from the market. It means being ready if sentiment turns and investors start moving into bonds and other lower-risk assets, which can feed a broader correction.

What, then, counts as a defensive share?

The advantage of defensive shares

Defensive shares are businesses that tend to hold up better when the economy slows. They often have resilient earnings, dependable dividends, and exposure to sectors with steady demand, like utilities and healthcare.

Many also sell globally, which can smooth out weakness in any single market.

I’ve been exploring passive income streams for a while, and this post gave me a fresh perspective on how RECI could fit into a balanced portfolio. The live tracking aspect seems especially useful for staying realistic about returns instead of just chasing hype. Do you have any thoughts on how it compares to traditional dividend-focused REITs in terms of risk?

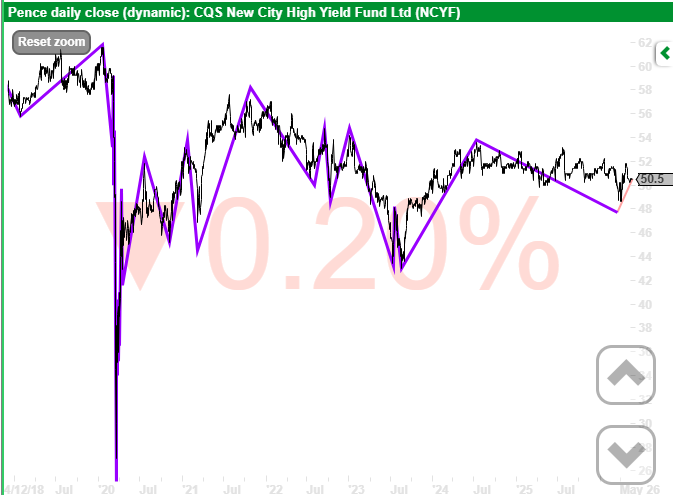

All the companies are loan arrangers, currently all paying a high yield, which tells you all you need to know about the market. The SNOWBALL would like to own NCYF but at a higher yield and at a discount to NAV, which means waiting for a market crash.

Now that’s a scary chart, when the market thought that due to covid companies wouldn’t be able to make loan repayments. Using good ole hindsight it was a great opportunity because as the price fell the yield rose and around the low the dividend was trimmed but the yield was still around 30% (subject to when you bought), where you would still be receiving a similar buying yield.

Back to RECI their loans are secured against property, so they should be a lower risk.

It never stopped the share from falling but it recovered fairly smartly but still not back to its previous price.

If the price rises and the yield falls, you could book your profits and re-invest in a higher yielder/risk IT. If not keep re-investing the dividends either back into CMPI or your Snowball.

The SNOWBALL currently doesn’t invest in CMPI as the earned and re-invested dividend stream means that the SNOWBALL can take more risks when re-investing. When the SNOWBALL nears its drawdown period, it could become a key component of it’s income stream.

4 ETFs Yielding Over 7% That Income Investors Are Quietly Buying

These ETFs are compelling as investors still struggle to capture meaningful yields from equities.

By David Dierking – Mar 22, 2026

Key Points

Income seekers are looking beyond traditional equities for high yields.

Option income strategies remain popular, but investors have been committing money to alternative strategies as well.

These ETFs yielding 7% or more have proved to be good high-income diversifiers, but be aware of the risks.

If you’re a dividend stock investor, things are finally looking better for you in 2026.

After three straight years of underperformance in a market dominated by large-cap tech, dividend stocks have finally swung back into favor. One exchange-traded fund (ETF), the WisdomTree U.S. Total Dividend ETF, is outperforming the S&P 500 by about 5% year to date on the heels of leadership from value and defensive stocks.

But dividend yields are still pretty thin. The Vanguard S&P 500 ETF is only yielding about 1.1%. If you focus more on high yield stocks, you can capture something in the 3% to 4% range. To find something higher than that, you have to consider more niche and unique strategies.

Income investors have been looking into various strategies for high yields. Here are four ETFs that have drawn positive net inflows over the past three months and the past year, but have yet to really capture the market’s attention.

Image source: Getty Images.

1. JPMorgan Equity Premium Income ETF

The JPMorgan Equity Premium Income ETF(JEPI) was one of the biggest success stories of the 2022 bear market. As yields began soaring and fixed income was delivering double-digit losses, covered-call strategies emerged as an alternative to bonds. With yields pushing 10% or higher, they soon drew billions of dollars of investor money.

This fund’s returns have cooled off over the past couple of years during the AI boom, but investor interest hasn’t waned. It’s up to more than $43 billion in assets and has taken in net new money of $2.3 billion in 2026 alone. It has a current yield of 7.6%.

The JPMorgan Equity Premium Income ETF is built on a portfolio of low-volatility stocks, so it’s made for an environment like the one we’re seeing now. It worked well in 2022, and it could work again in 2026.

2. JPMorgan Nasdaq Equity Premium Income ETF

The JPMorgan Nasdaq Equity Premium Income ETF(JEPQ+0.17%) is essentially the Nasdaq 100 version of the fund above. It was just launched in 2022, but it caught the popularity wave of its sister fund and then captured further buying interest due to the bull market in tech stocks. It offers a current yield of 11.4%.Collapse

That higher yield is a product of the higher volatility that comes from the Nasdaq 100 stocks compared to a portfolio of low-volatility stocks. If the major U.S. indexes continue meandering sideways, as they have in 2026, it could be the kind of environment where we see the JPMorgan Nasdaq Equity Premium Income ETF actually outperform the Invesco QQQ ETF.

3. Global X SuperDividend ETF

The Global X SuperDividend ETF(SDIV) is about as pure of a high-yield equity play as you’ll find. Its strategy is simple: Include the 100 highest-yielding equity securities in the world (subject to minimum liquidity and tradable potential). Outside of that, it places almost no restrictions on what can make the cut.

What you end up with is a portfolio that’s heavy in financials (32%), real estate investment trusts (20%), and energy (18%). It’s also very diversified globally. The U.S., developed markets, and emerging markets all have nearly equal allocations of one-third each. It has a current yield of 7.3%.Collapse

Over the past year, investors have loved this fund. It has experienced 14 consecutive months of net inflows, including $60 million so far in March 2026. If that number holds, it would be the biggest monthly net inflow in 12 years.

4. VanEck BDC Income ETF

The VanEck BDC Income ETF(BIZD) is a fund that investors keep dipping their toes into, but it should come with a big warning. This fund invests in business development companies (BDCs), and that means heavy exposure to private credit.

Its three biggest holdings are Ares Capital, Blue Owl Capital, and the Blackstone Secured Lending Fund. Blue Owl, in particular, has been in the news a lot lately for freezing investor capital and halting redemption requests. There can be plenty of potential with this segment of the market, but private credit can be illiquid and risky, as many investors are finding out right now.

The VanEck BDC Income ETF has an attractive yield of 9.6%, but be careful about getting too aggressive with the yield hunting here.

Charcol; and Nick Sutton, sales director, Retirement Solutions

Ms Lowe’s concerns around equity release are completely valid, particularly when it comes to the potential for interest to compound over time. If Ms Lowe were to borrow £250,000 against her £800,000 home, the current best rate available as of today is a 6.4pc monthly equivalent rate (MER), or 6.59pc annual equivalent rate (AER).

If she chose not to make any repayments, the balance after 15 years would grow to approximately £651,261. This gives her the cash now without the need for monthly payments but does of course mean a significant reduction in the value of the estate left behind.

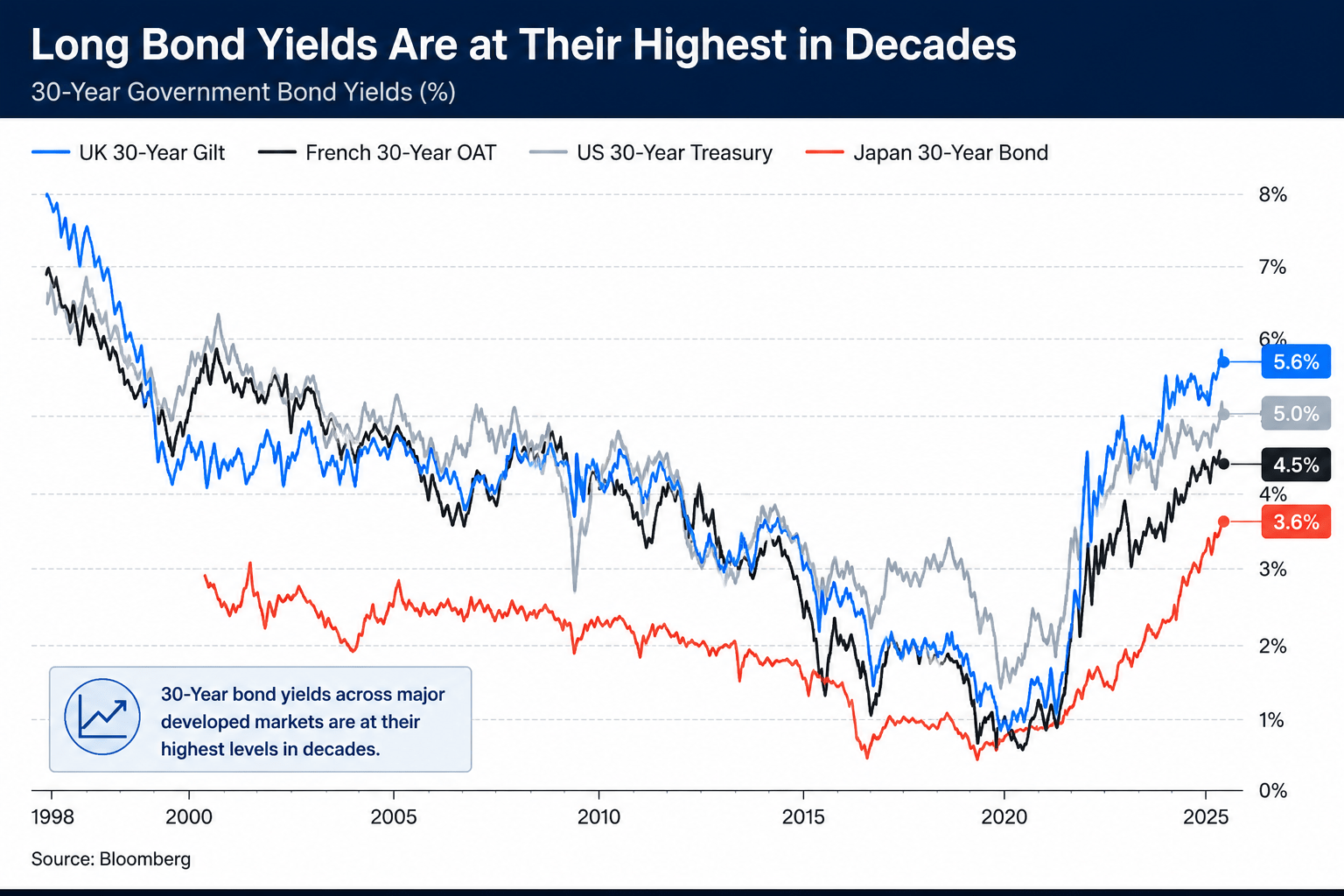

A higher-for-longer interest rate environment has created a restrictive macro landscape where traditional income strategies fail to clear the surging 5.10% long-bond hurdle rate.

This targeted pair provides a robust “Cash Flow Fortress” capable of absorbing inflationary pressures through exceptional balance sheet strength.

By combining high-conviction Quant “Strong Buys” with accelerating fundamental momentum, this elite duo delivers an inflation-protected income stream without sacrificing safety or capital growth.

I am Steven Cress, Head of Quantitative Strategies at Seeking Alpha. I manage the quant ratings and factor grades on stocks and ETFs in Seeking Alpha Premium. I also lead Quant Growth and Income, which is a model portfolio for dividend investors interested in capital appreciation and income.

vicnt/iStock via Getty Images

Higher for Longer

The bull is in the china shop. The “bull” is the equity market, which has been charging to all-time highs despite a brief pullback over the last few days.

The “china shop” would be delicate bonds, which are getting destroyed once again.

The bond market is selling off at a blistering pace. Yields are surging, and the long end of the curve is flying off the charts. In a matter of weeks, the benchmark 30-year U.S. Treasury yield blasted past 5.10%, hitting its highest level since July 2007.

Seeking Alpha, Bloomberg

The culprit here isn’t a secret. The ongoing energy price shock stemming from the war in Iran has completely opened the doors to macro chaos, sending oil prices soaring and reigniting fears of a second inflation wave in four years.

Any hopes we saw in late 2025 for a central bank policy pivot toward substantial rate cuts have been virtually extinguished. Put out by the return of the restrictive “higher-for-longer” policy that’s now the definitive base case through the end of 2026.

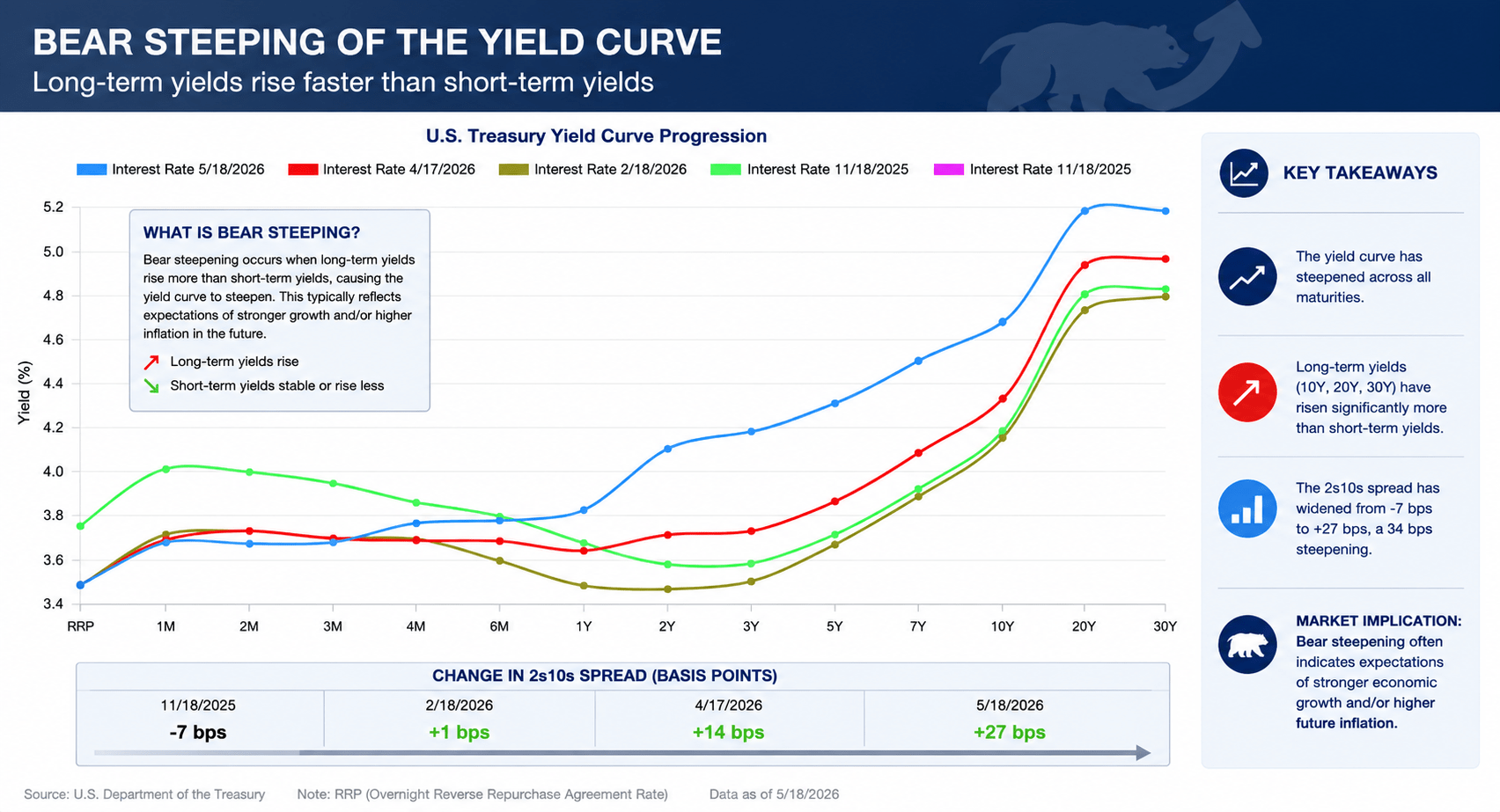

A Bear Steepener

What we’re witnessing right now is a textbook “bear steepening” of the yield curve. A bear steepening occurs when long-term interest rates rise faster than short-term interest rates. These rising yields result in a bond market sell-off on the longer-duration bonds.

Seeking Alpha

Understanding What a Bear Steepener Means for the Market

The Fed’s operational lever on interest rates is generally confined to the short end of the curve, orchestrated by the Federal Open Market Committee’s setting of the Federal Funds Rate. The open market, however, holds greater influence over the long end of the curve. With inflation rapidly reigniting, fear of structural and sticky pricing pressures has permeated. In response, investors are demanding a higher premium on government bonds.

Higher yields on 10-, 20-, and 30-year maturities can also act as a direct tax on consumers, significantly increasing the cost of consumer-driven debt. This includes mortgages and auto loans, which are heavily anchored to the benchmark 10-year U.S. Treasury – added pressures to consider for the new Fed Chair.

Welcome to the Party

On May 15, Fed Chair Jerome Powell officially handed over the reins to newly appointed Fed Chair Kevin Warsh, who is set to be sworn in by President Donald Trump on Friday, May 22.

This welcome party has quickly turned into an unwanted surprise party. The FOMC is split along ideological lines, essentially sitting on opposite sides of the room. Warsh is stepping into the most divided Fed since 1992. One camp is fearful of slowing growth and a stagnant labor market, while the other is concerned about a resurgence of high inflation led by the recent commodity shock. In this climate of extreme volatility, noise, policy gridlock, and uncertainty, trying to navigate all of these factors unprepared would be a fool’s errand. Instead, investors have an opportunity to take the smart approach.

Even in times of policy division, they often can’t help but verbalize their fears and/or policy motivations. By analyzing the recent commentary of Fed members combined, we can map those hidden insights directly to Seeking Alpha’s Quant Model, pointing us to two top-rated dividend stocks built to withstand the current market environment.

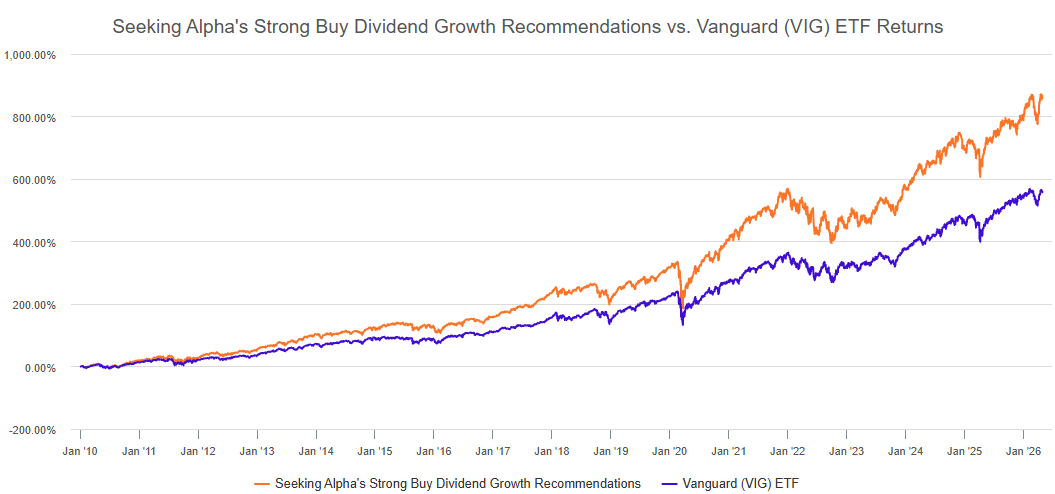

Seeking Alpha’s Quant Model has consistently outperformed the Vanguard Dividend Appreciation ETF (VIG) over the past decade. The historical chart below illustrates the effectiveness of this quantitative approach and sets the table for the strategy we’re discussing today.

Seeking Alpha

Top Dividend Stocks

Today, we’re going to look at recent quotes from Federal Reserve members and pair their commentary with select opportunities according to our Quant Model.

To select the top dividend stocks to feature in this article, I used the Seeking Alpha Stock Screener and chose the pre-selected Top Dividend Stocks and filtered for Quant Strong Buys/Buys only. I then sorted for stocks that exhibited Dividend Safety and Growth Grades of ‘C+’ and higher.

Founded in 1864, the Royal Bank of Canada is the country’s largest financial institution by market capitalization and holds the rare distinction by the International Financial Stability Board of being a “Global Systemically Important Bank” [G-SIB]. As a G-SIB, RY is required to hold higher capital buffers and is met with stricter regulatory oversight due to its importance within the financial system.

This designation is precisely what makes it a safe harbor for income investors worried about potential Fed policy affecting more vulnerable banking institutions.

With the 30-year Treasury yield marching north of 5.10%, traditional commercial banks begin to exercise the very stress test scenarios they prepare for. Rising long-term yields cause unrealized losses on investment holdings to grow and exert undue stress on balance sheets as deposit costs rise and competition for deposit volume increases.

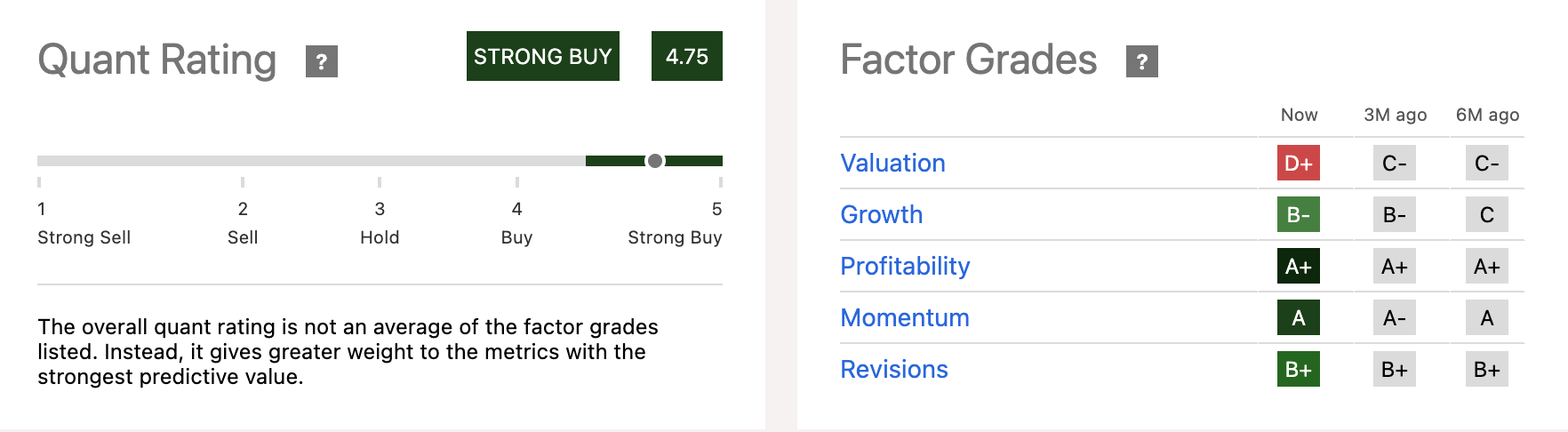

But for a global giant like the Royal Bank of Canada, this market stress can be an opportunity to consider a ‘Strong Buy’ Quant-Rated company like RY.

Seeking Alpha

When a Fed governor explicitly uses phrases such as “undermine bank resilience” or “threaten financial stability,” investors shouldn’t just cover their ears and hope for the best. Federal Reserve Governor Michael S. Barr issued this warning in a recent speech regarding the potential dangers of policy normalization on the financial sector:

I think shrinking the balance sheet is the wrong objective, and many of the proposals to meet this objective would undermine bank resilience, impede money market functioning, and, ultimately, threaten financial stability.

RY is positioned to combat any instability in the financial system due to its consistently high profitability metrics. Recently, RY raised its return on equity target to a baseline of 17%. President and Chief Executive Officer Dave McKay expanded on this achievement in the Q4 earnings call:

As I noted earlier, we are increasing our through-the-cycle medium-term ROE objective to 17%-plus due to the improved cost efficiencies and increased revenue productivity, including strong client flows and funding synergies from deposit growth… Our premium ROE, robust capital generation, and current CET1 ratio give us significant strategic optionality. Even after deploying capital to grow our franchises and pay dividends, we expect to build significant excess capital over the coming years. Net income, net of dividends, and core RWA growth is estimated to add approximately 80 basis points to our CET1 ratio annually.

RY’s strong balance sheet is a catalyst for its ‘A+’ Profitability Grade and is fueled by its ‘A+’ Grade in Cash From Operations, and ‘A-’ Grade in Net Income Margin, which outpaces the sector median by nearly 35%.

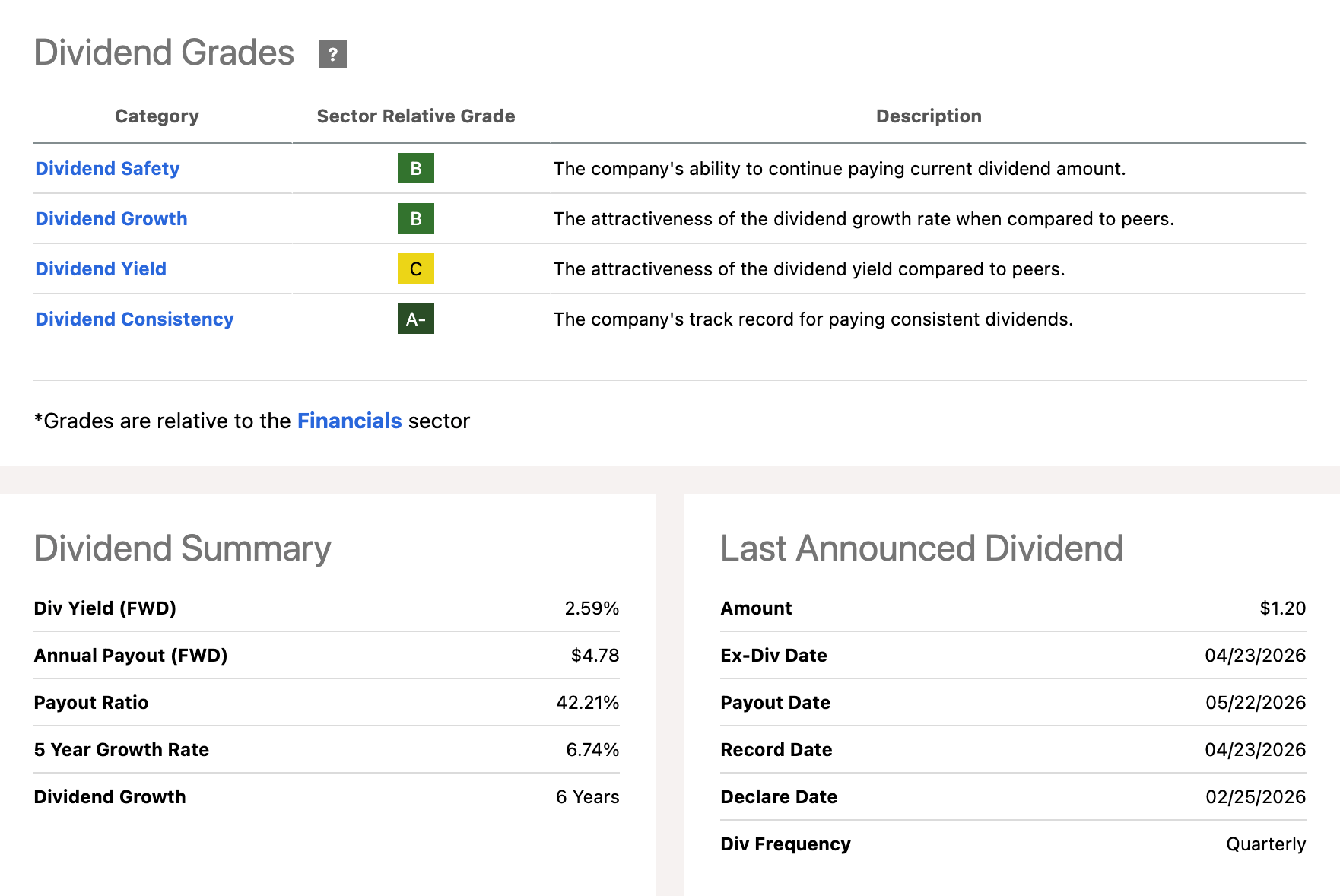

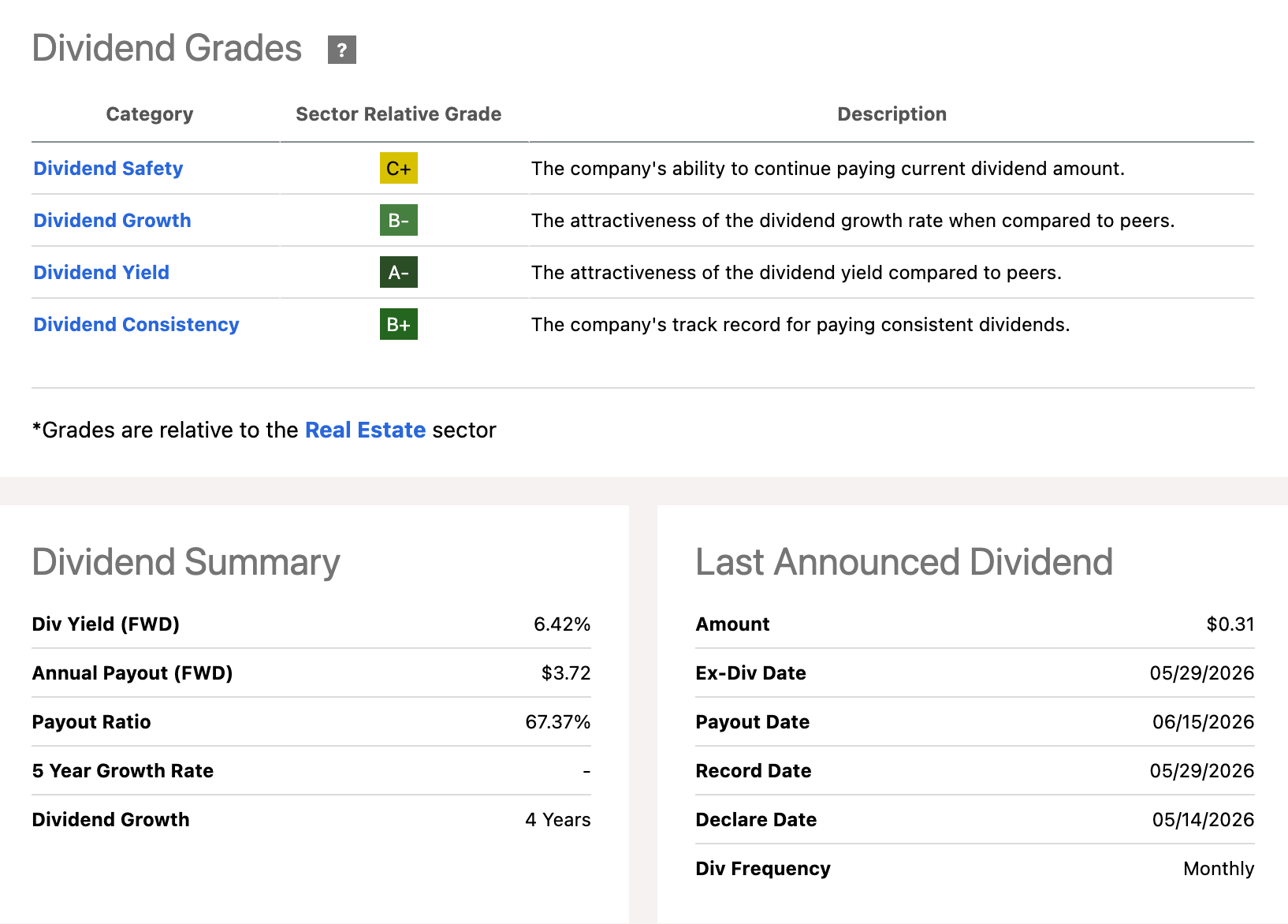

Dividend Grade Scorecard

Seeking Alpha

In its most recent quarter, RBY reported a record net income of $5.8 billion, up 13% year-over-year [YoY]. Backed by this strong cash flow, the bank maintains a secure 42% payout ratio paired with a 6.74% five-year growth rate.

Seeking Alpha

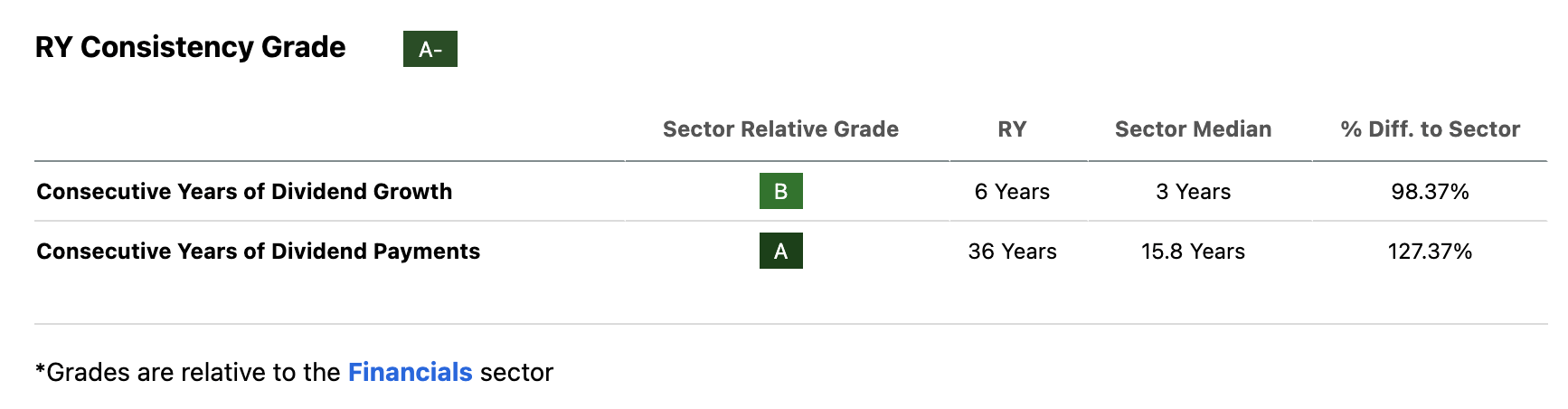

RY’s Dividend Consistency Grade of an ‘A-‘ is backed by its 36-year track record of dividend payments and six-years of dividend growth. Both doubled their respective sector medians, an indication that RY has the potential balance sheet strength to continue rewarding shareholders even in a challenging rate environment.

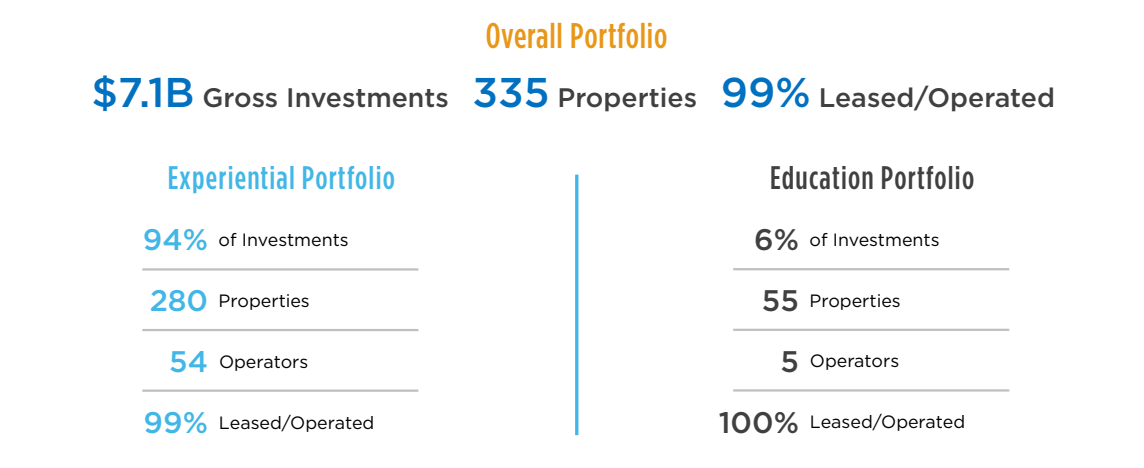

EPR Properties is a premier player in experiential real estate, out-of-home leisure, and entertainment venues. EPR’s portfolio spans across high-traffic destinations such as golf complexes, ski and winter resorts, theme parks, and theaters. This second pick is complimented by the insights shared by Powell during his last press conference heading the FOMC:

Recent indicators suggest that economic activity has been expanding at a solid pace. Consumer spending has been resilient… Inflation has moved up and is elevated, in part reflecting the recent increase in global energy prices.

What Powell signals is that, despite the escalating energy price shock and bump to headline inflation, the US consumer is portraying spending behavior that shows little fear of long-term price pressures.

The Resilient Consumer

I think it’s important to note that consumers are tightening their belts in some areas, specifically related to certain finished goods expenditures such as motor vehicles, but discretionary spending on real-world experiences and events has remained strong. Today’s consumer has shown an inherent behavior to prioritize memories and experiential services over goods.

Over the past four years, the Federal Reserve instituted one of the most restrictive monetary tightening campaigns in decades. Traditional retail and commercial offices were already struggling to come out of the COVID-19 shock, and the higher cost of capital added salt to the wound.

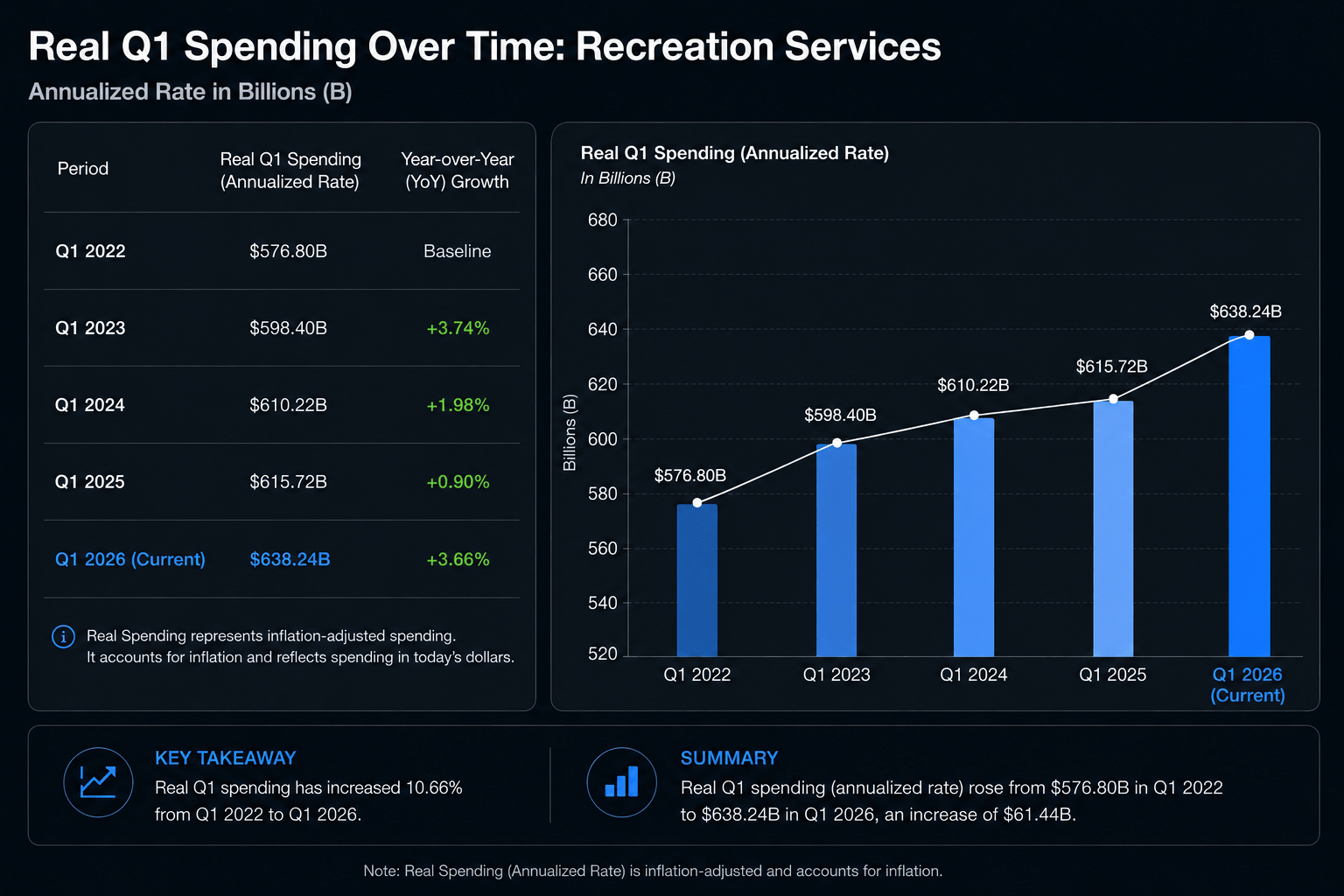

However, recreational demand not only remained resilient but also showed growth during this period. If you take a look at the image below, you’ll see inflation-adjusted spending from consumers on recreation services over the last five first-quarters.

Seeking Alpha, FRED

This structural foundation of consumer behavior and an expanding market is what creates such a strong tailwind for EPR Properties, as 94% of its portfolio is concentrated in experiential properties.

EPR Earnings Presentation

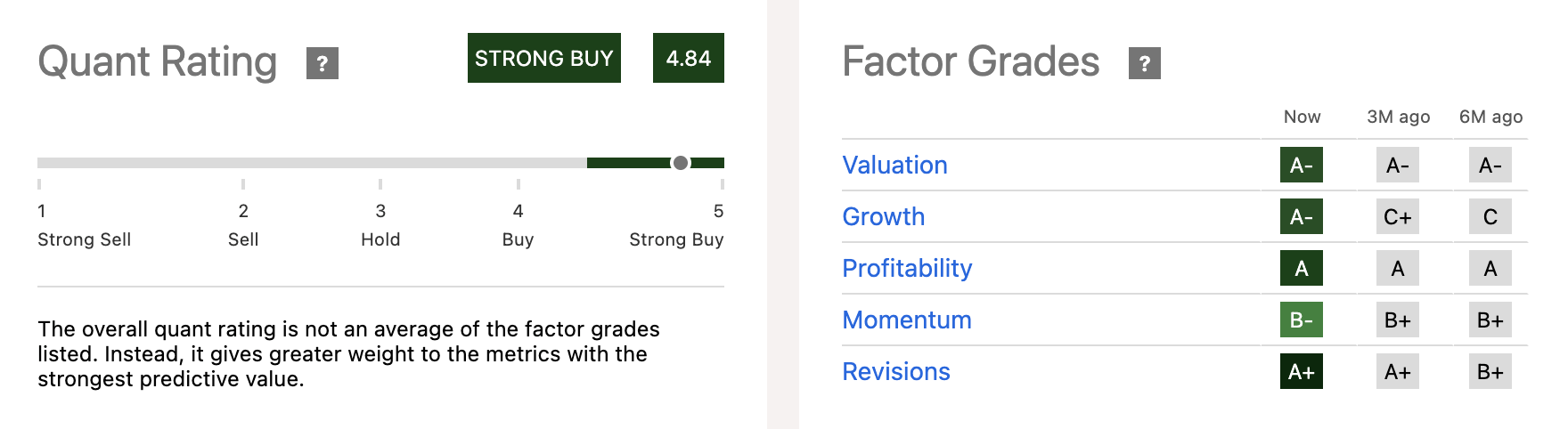

EPR is currently rated as a Strong Buy according to Seeking Alpha’s Quant System, backed by an exceptional suite of underlying Factor Grades.

Seeking Alpha

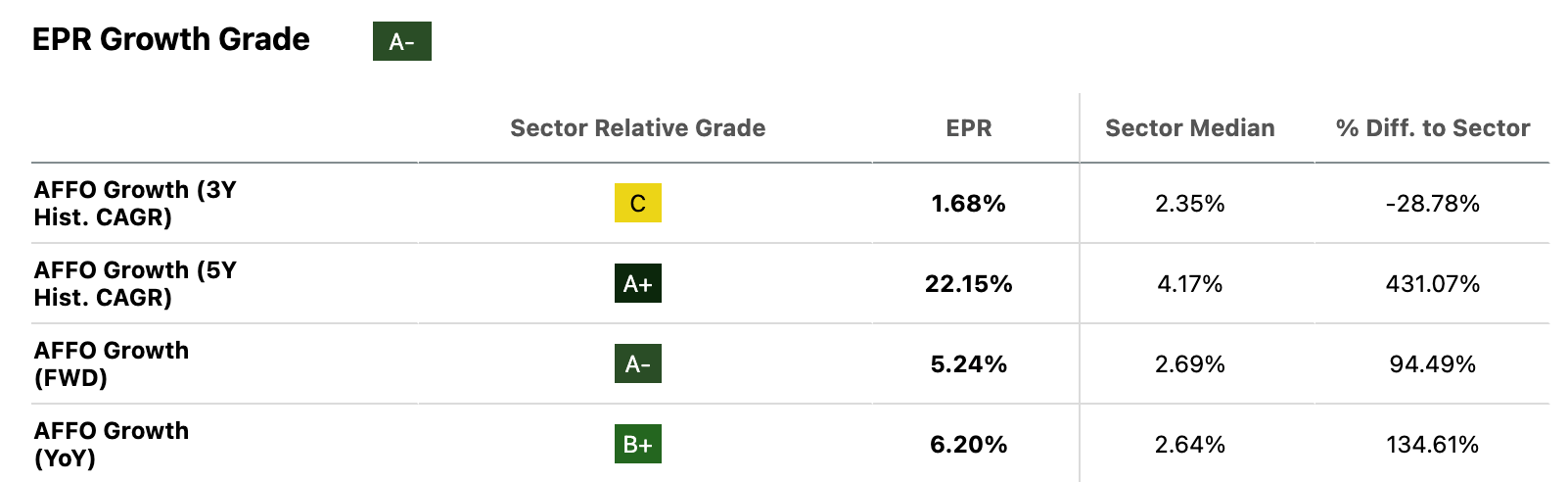

Our Quant System currently highlights EPR’s rapid Growth Grade increase–currently an ‘A-’, when only six months ago it was rated a ’C’. Investors should consider capturing this momentum heading into the summer. As shown below, EPR scores strongly on its AFFO Growth (5Y CAGR and FWD) scores, with its AFFO Growth [FWD] nearly doubling the sector median figure at 5.24%.

Seeking Alpha

In a traditional commercial real estate setup, high interest rates have the potential to derail cash flow as maintenance management costs rise. However, EPR’s triple net lease structure [NNN] protects them from rising inflationary pressures on margins.

Under long-term agreements, tenants are legally obligated to pay for 100% of the property-level costs that are subject to rising input costs. This includes taxes, insurance, and utility costs. This structure has provided an exceptionally strong buffer for AFFO growth.

Additionally, EPR includes annual rent escalators, which are usually tied to the Consumer Price Index [CPI]. This helps to insulate the company’s cash flow from internal cost pressures. And ultimately, providing the basis for a phenomenal dividend profile.

Dividend Grade Scorecard

Seeking Alpha

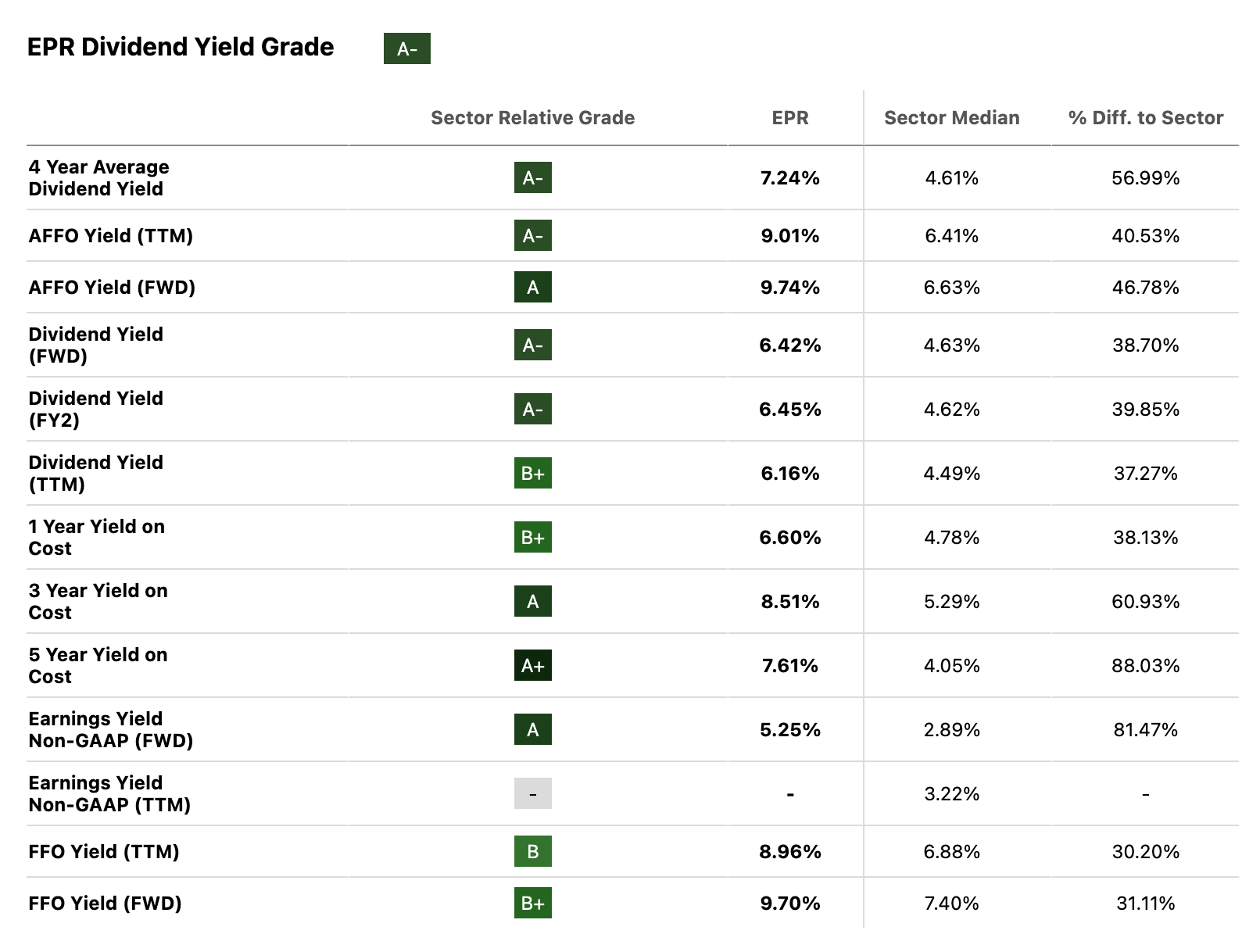

EPR’s balance sheet strength passes through to its incredible ‘A-’ Dividend Yield Grade. The income profile is headlined by its 6.42% Dividend Yield [FWD], outperforming the sector median by 40%. More importantly, its 9.74% AFFO Yield [FWD] is nearly 47% higher than the sector median and provides a profitable yield gap of 3.42%, anchoring the company for strong growth ahead while protecting its payout.

Seeking Alpha

Looking Ahead: Income Investing Strategies

With yields once again on the move, the passive playbook for income investors is quickly becoming obsolete. Navigating this higher-for-longer rate environment requires active management and a tactical rotation into companies that can not just survive, but thrive.

The coming months could be difficult for growth and value opportunities that lack income-generating payments. It’s probably timely for investors to build a portfolio that can withstand volatile markets amid rising inflation concerns, midterm elections, and geopolitical tensions. Ultimately, today’s picks prove that income opportunities are still very much available in today’s market environment–delivering strong, safe returns while actively shielding your capital from broader market volatility