2 Top Dividend Stocks For A ‘Higher-For-Longer’ Rate Environment

Steven Cress, Quant Team

SA Quant Strategist

Summary

- A higher-for-longer interest rate environment has created a restrictive macro landscape where traditional income strategies fail to clear the surging 5.10% long-bond hurdle rate.

- This targeted pair provides a robust “Cash Flow Fortress” capable of absorbing inflationary pressures through exceptional balance sheet strength.

- By combining high-conviction Quant “Strong Buys” with accelerating fundamental momentum, this elite duo delivers an inflation-protected income stream without sacrificing safety or capital growth.

- I am Steven Cress, Head of Quantitative Strategies at Seeking Alpha. I manage the quant ratings and factor grades on stocks and ETFs in Seeking Alpha Premium. I also lead Quant Growth and Income, which is a model portfolio for dividend investors interested in capital appreciation and income.

Higher for Longer

The bull is in the china shop. The “bull” is the equity market, which has been charging to all-time highs despite a brief pullback over the last few days.

The “china shop” would be delicate bonds, which are getting destroyed once again.

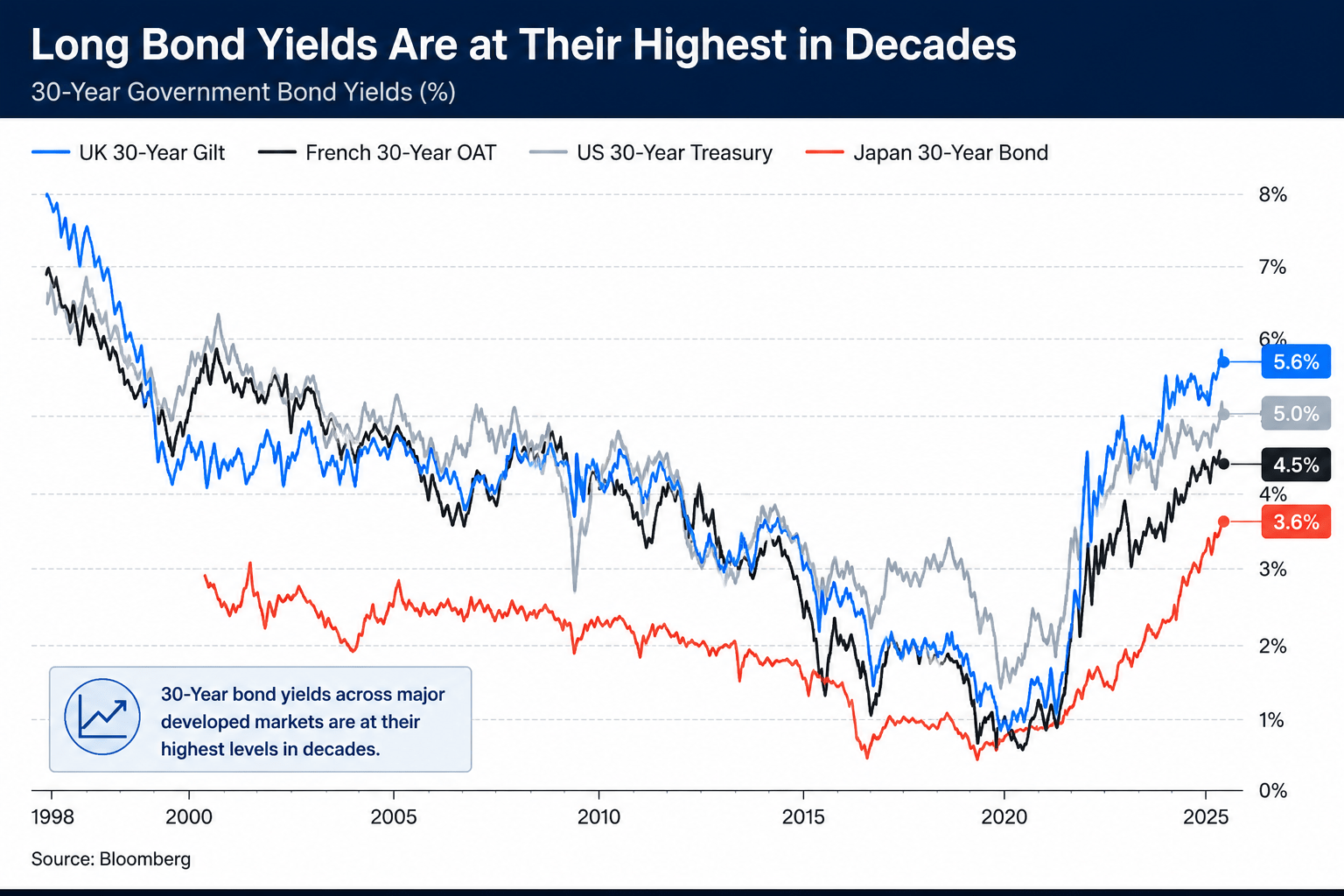

The bond market is selling off at a blistering pace. Yields are surging, and the long end of the curve is flying off the charts. In a matter of weeks, the benchmark 30-year U.S. Treasury yield blasted past 5.10%, hitting its highest level since July 2007.

The culprit here isn’t a secret. The ongoing energy price shock stemming from the war in Iran has completely opened the doors to macro chaos, sending oil prices soaring and reigniting fears of a second inflation wave in four years.

Any hopes we saw in late 2025 for a central bank policy pivot toward substantial rate cuts have been virtually extinguished. Put out by the return of the restrictive “higher-for-longer” policy that’s now the definitive base case through the end of 2026.

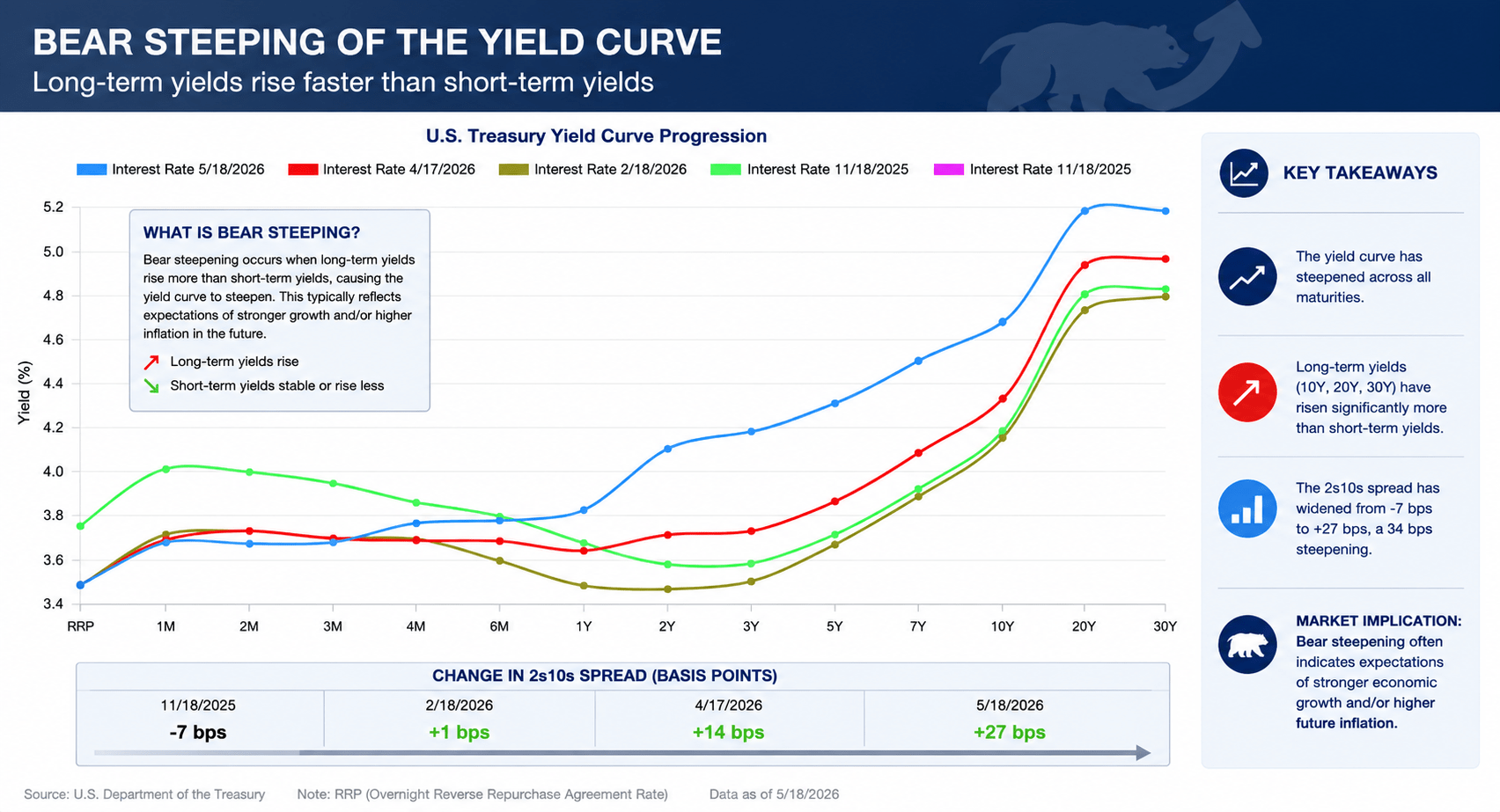

A Bear Steepener

What we’re witnessing right now is a textbook “bear steepening” of the yield curve. A bear steepening occurs when long-term interest rates rise faster than short-term interest rates. These rising yields result in a bond market sell-off on the longer-duration bonds.

Understanding What a Bear Steepener Means for the Market

The Fed’s operational lever on interest rates is generally confined to the short end of the curve, orchestrated by the Federal Open Market Committee’s setting of the Federal Funds Rate. The open market, however, holds greater influence over the long end of the curve. With inflation rapidly reigniting, fear of structural and sticky pricing pressures has permeated. In response, investors are demanding a higher premium on government bonds.

Higher yields on 10-, 20-, and 30-year maturities can also act as a direct tax on consumers, significantly increasing the cost of consumer-driven debt. This includes mortgages and auto loans, which are heavily anchored to the benchmark 10-year U.S. Treasury – added pressures to consider for the new Fed Chair.

Welcome to the Party

On May 15, Fed Chair Jerome Powell officially handed over the reins to newly appointed Fed Chair Kevin Warsh, who is set to be sworn in by President Donald Trump on Friday, May 22.

This welcome party has quickly turned into an unwanted surprise party. The FOMC is split along ideological lines, essentially sitting on opposite sides of the room. Warsh is stepping into the most divided Fed since 1992. One camp is fearful of slowing growth and a stagnant labor market, while the other is concerned about a resurgence of high inflation led by the recent commodity shock. In this climate of extreme volatility, noise, policy gridlock, and uncertainty, trying to navigate all of these factors unprepared would be a fool’s errand. Instead, investors have an opportunity to take the smart approach.

Even in times of policy division, they often can’t help but verbalize their fears and/or policy motivations. By analyzing the recent commentary of Fed members combined, we can map those hidden insights directly to Seeking Alpha’s Quant Model, pointing us to two top-rated dividend stocks built to withstand the current market environment.

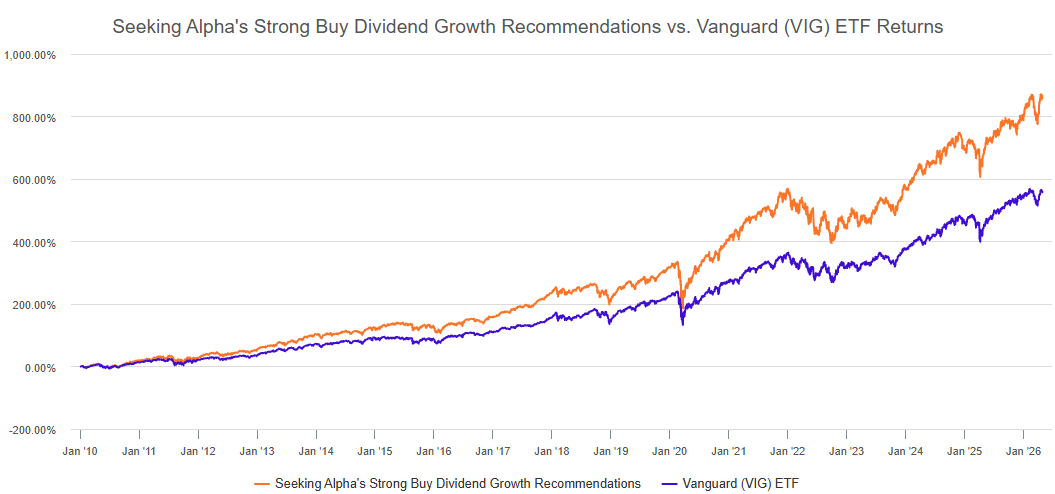

Seeking Alpha’s Quant Model has consistently outperformed the Vanguard Dividend Appreciation ETF (VIG) over the past decade. The historical chart below illustrates the effectiveness of this quantitative approach and sets the table for the strategy we’re discussing today.

Top Dividend Stocks

Today, we’re going to look at recent quotes from Federal Reserve members and pair their commentary with select opportunities according to our Quant Model.

To select the top dividend stocks to feature in this article, I used the Seeking Alpha Stock Screener and chose the pre-selected Top Dividend Stocks and filtered for Quant Strong Buys/Buys only. I then sorted for stocks that exhibited Dividend Safety and Growth Grades of ‘C+’ and higher.

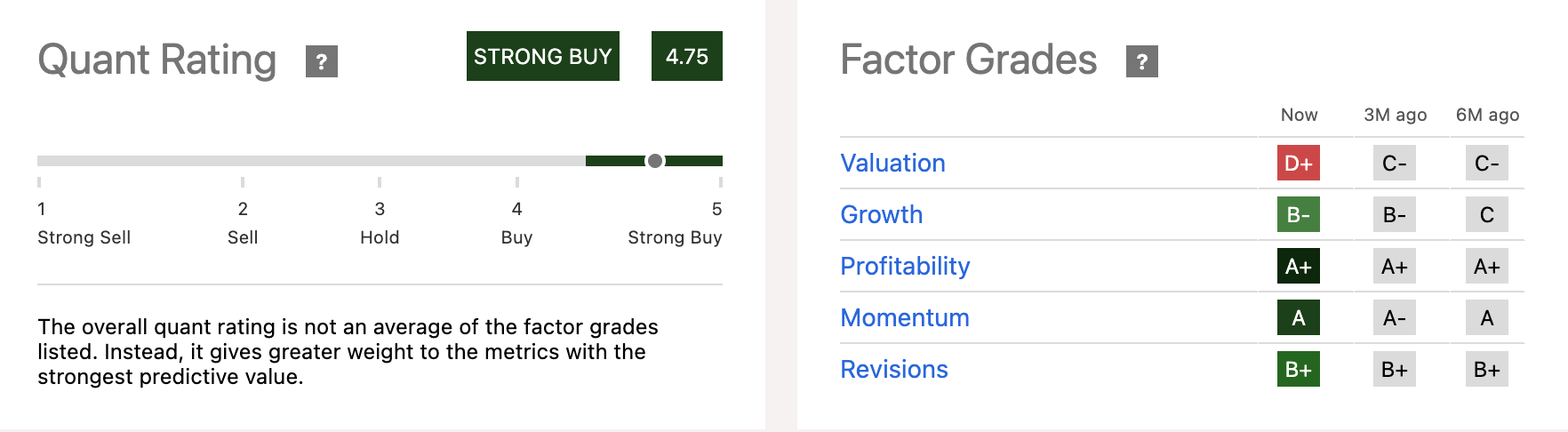

1. Royal Bank of Canada (RY)

- Market Capitalization: $256.5B

- Quant Rating: Strong Buy

- Sector: Financials

- Industry: Diversified Banks

- Quant Sector Ranking: 21 out of 686

- Quant Industry Ranking: 5 out of 69

- Dividend Yield (FWD): 2.6%

Founded in 1864, the Royal Bank of Canada is the country’s largest financial institution by market capitalization and holds the rare distinction by the International Financial Stability Board of being a “Global Systemically Important Bank” [G-SIB]. As a G-SIB, RY is required to hold higher capital buffers and is met with stricter regulatory oversight due to its importance within the financial system.

This designation is precisely what makes it a safe harbor for income investors worried about potential Fed policy affecting more vulnerable banking institutions.

With the 30-year Treasury yield marching north of 5.10%, traditional commercial banks begin to exercise the very stress test scenarios they prepare for. Rising long-term yields cause unrealized losses on investment holdings to grow and exert undue stress on balance sheets as deposit costs rise and competition for deposit volume increases.

But for a global giant like the Royal Bank of Canada, this market stress can be an opportunity to consider a ‘Strong Buy’ Quant-Rated company like RY.

When a Fed governor explicitly uses phrases such as “undermine bank resilience” or “threaten financial stability,” investors shouldn’t just cover their ears and hope for the best. Federal Reserve Governor Michael S. Barr issued this warning in a recent speech regarding the potential dangers of policy normalization on the financial sector:

I think shrinking the balance sheet is the wrong objective, and many of the proposals to meet this objective would undermine bank resilience, impede money market functioning, and, ultimately, threaten financial stability.

RY is positioned to combat any instability in the financial system due to its consistently high profitability metrics. Recently, RY raised its return on equity target to a baseline of 17%. President and Chief Executive Officer Dave McKay expanded on this achievement in the Q4 earnings call:

As I noted earlier, we are increasing our through-the-cycle medium-term ROE objective to 17%-plus due to the improved cost efficiencies and increased revenue productivity, including strong client flows and funding synergies from deposit growth… Our premium ROE, robust capital generation, and current CET1 ratio give us significant strategic optionality. Even after deploying capital to grow our franchises and pay dividends, we expect to build significant excess capital over the coming years. Net income, net of dividends, and core RWA growth is estimated to add approximately 80 basis points to our CET1 ratio annually.

RY’s strong balance sheet is a catalyst for its ‘A+’ Profitability Grade and is fueled by its ‘A+’ Grade in Cash From Operations, and ‘A-’ Grade in Net Income Margin, which outpaces the sector median by nearly 35%.

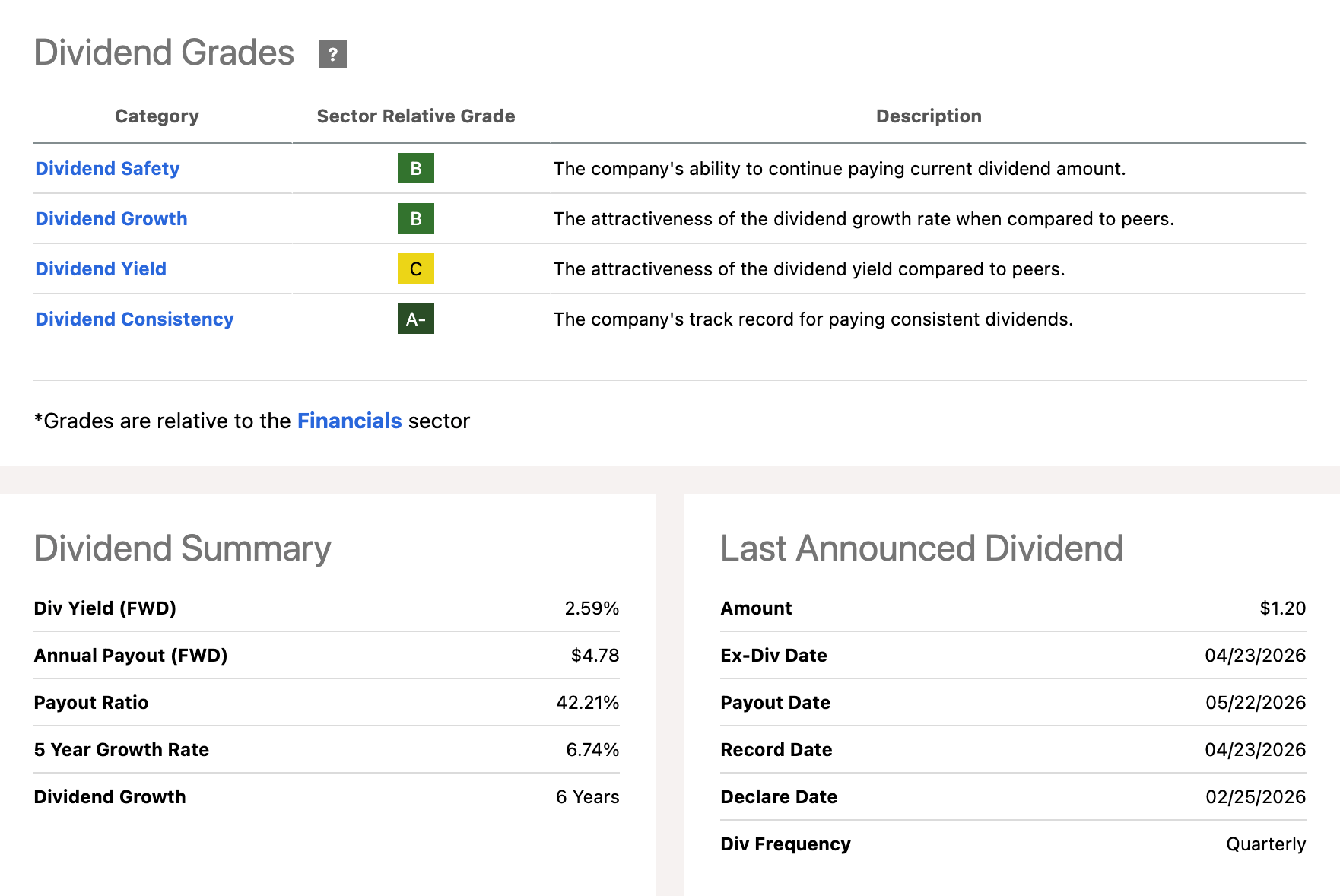

Dividend Grade Scorecard

In its most recent quarter, RBY reported a record net income of $5.8 billion, up 13% year-over-year [YoY]. Backed by this strong cash flow, the bank maintains a secure 42% payout ratio paired with a 6.74% five-year growth rate.

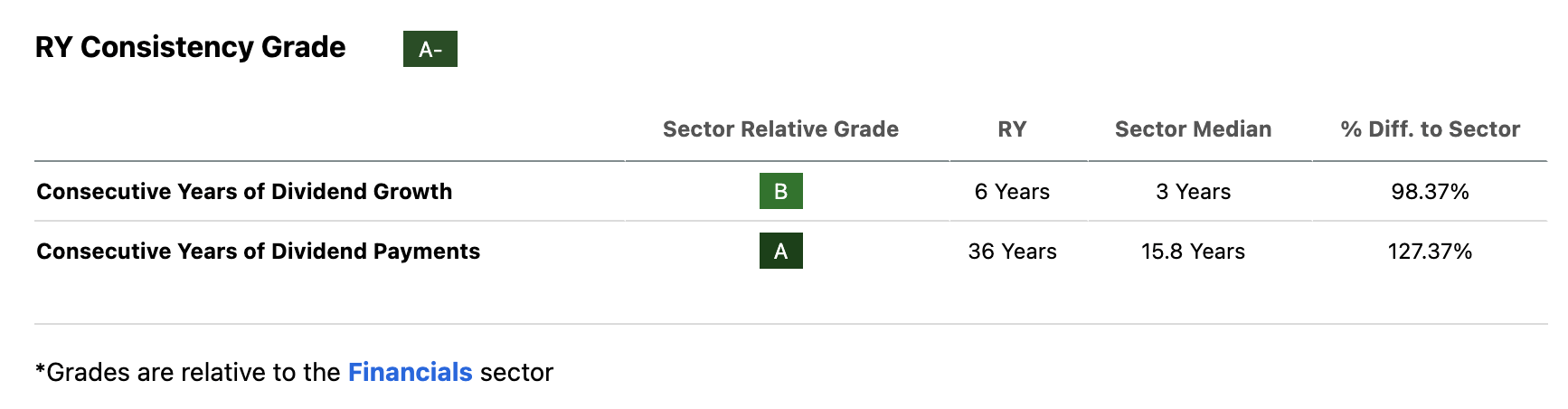

RY’s Dividend Consistency Grade of an ‘A-‘ is backed by its 36-year track record of dividend payments and six-years of dividend growth. Both doubled their respective sector medians, an indication that RY has the potential balance sheet strength to continue rewarding shareholders even in a challenging rate environment.

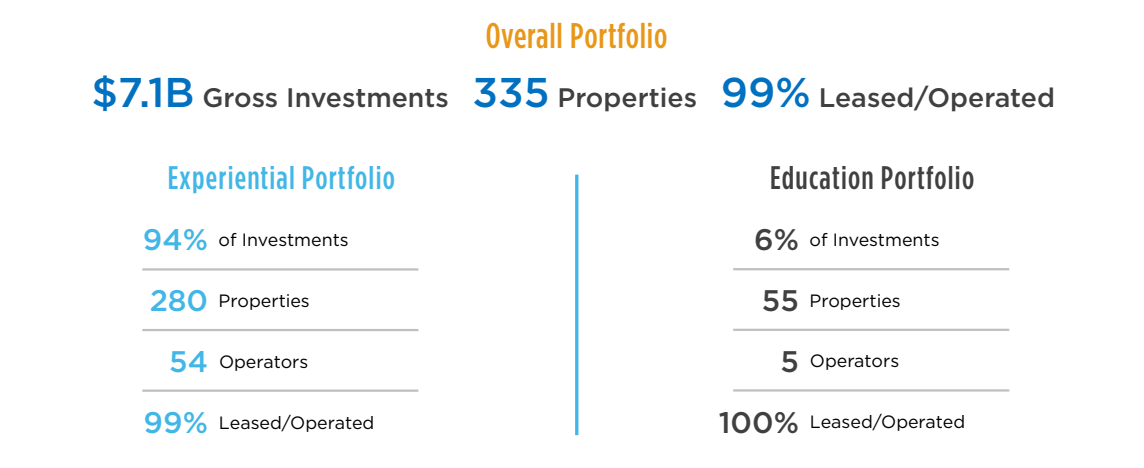

2. EPR Properties (EPR)

- Market Capitalization: $4.43B

- Quant Rating: Strong Buy

- Sector: Real Estate

- Industry: Other Specialized REITs

- Quant Sector Ranking: 4 out of 171

- Quant Industry Ranking: 1 out of 11

- Dividend Yield (FWD): 6.42%

EPR Properties is a premier player in experiential real estate, out-of-home leisure, and entertainment venues. EPR’s portfolio spans across high-traffic destinations such as golf complexes, ski and winter resorts, theme parks, and theaters. This second pick is complimented by the insights shared by Powell during his last press conference heading the FOMC:

Recent indicators suggest that economic activity has been expanding at a solid pace. Consumer spending has been resilient… Inflation has moved up and is elevated, in part reflecting the recent increase in global energy prices.

What Powell signals is that, despite the escalating energy price shock and bump to headline inflation, the US consumer is portraying spending behavior that shows little fear of long-term price pressures.

The Resilient Consumer

I think it’s important to note that consumers are tightening their belts in some areas, specifically related to certain finished goods expenditures such as motor vehicles, but discretionary spending on real-world experiences and events has remained strong. Today’s consumer has shown an inherent behavior to prioritize memories and experiential services over goods.

Over the past four years, the Federal Reserve instituted one of the most restrictive monetary tightening campaigns in decades. Traditional retail and commercial offices were already struggling to come out of the COVID-19 shock, and the higher cost of capital added salt to the wound.

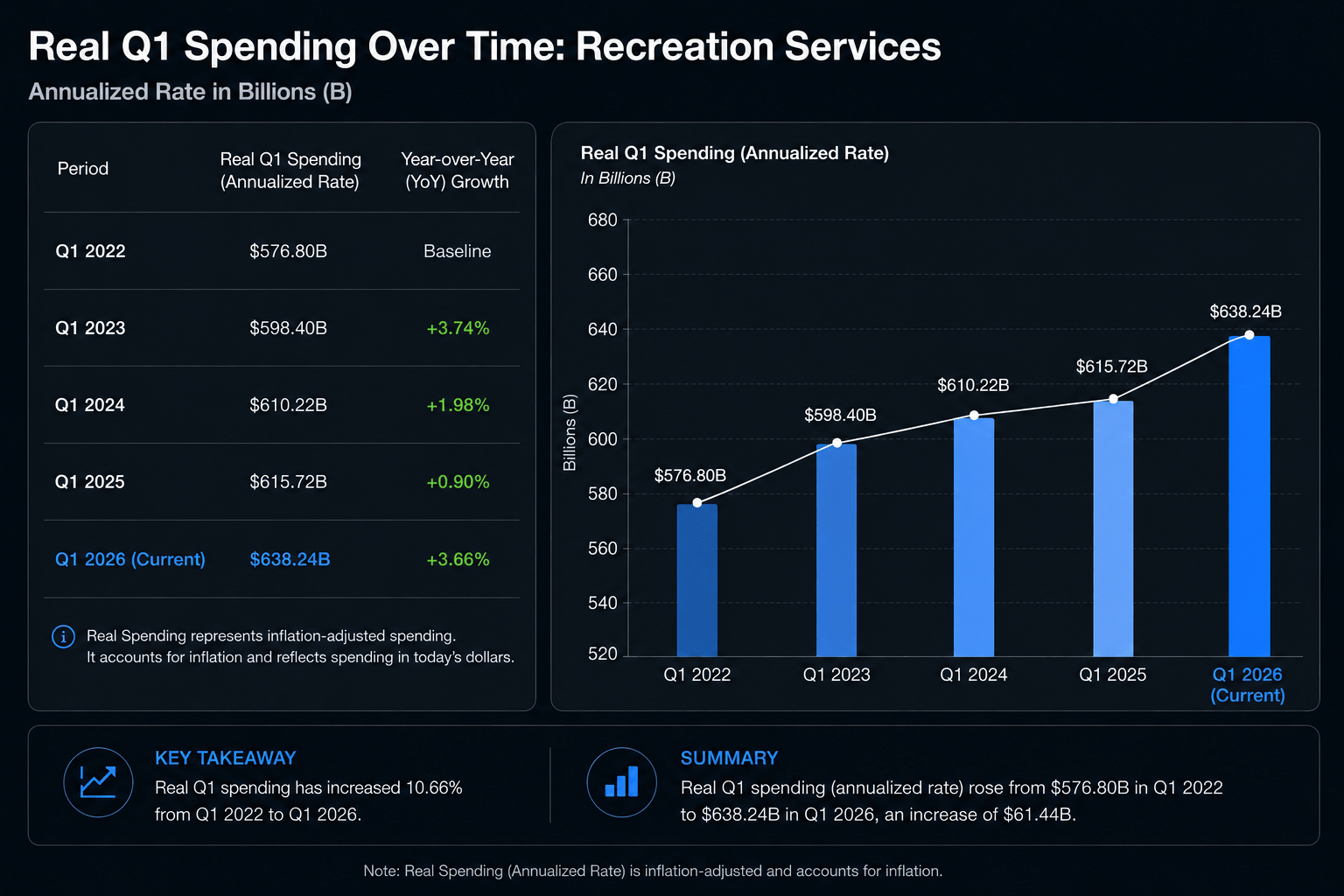

However, recreational demand not only remained resilient but also showed growth during this period. If you take a look at the image below, you’ll see inflation-adjusted spending from consumers on recreation services over the last five first-quarters.

This structural foundation of consumer behavior and an expanding market is what creates such a strong tailwind for EPR Properties, as 94% of its portfolio is concentrated in experiential properties.

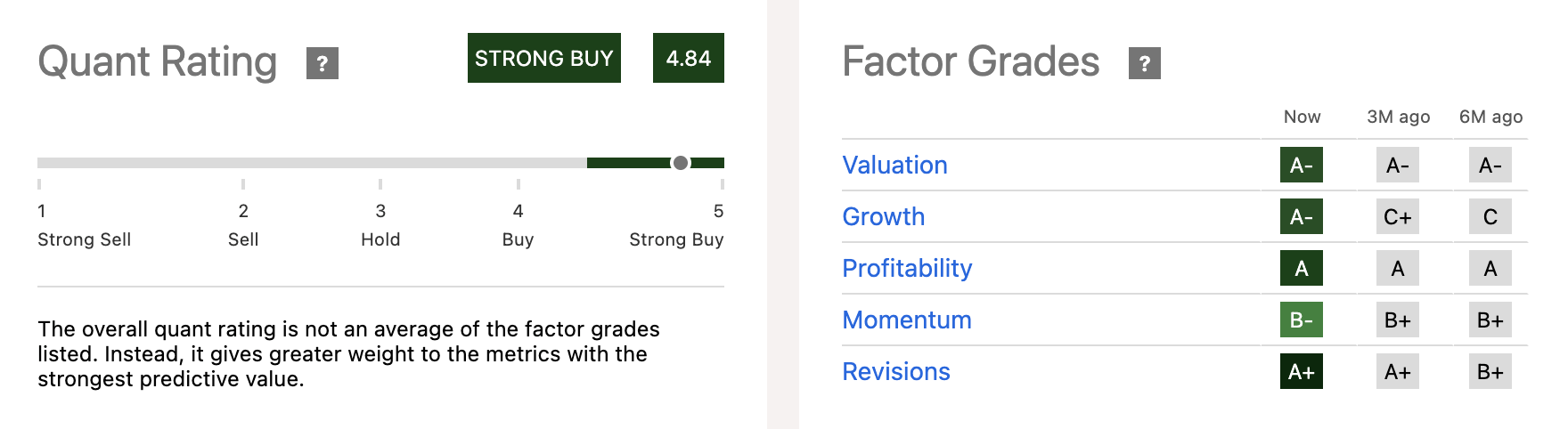

EPR is currently rated as a Strong Buy according to Seeking Alpha’s Quant System, backed by an exceptional suite of underlying Factor Grades.

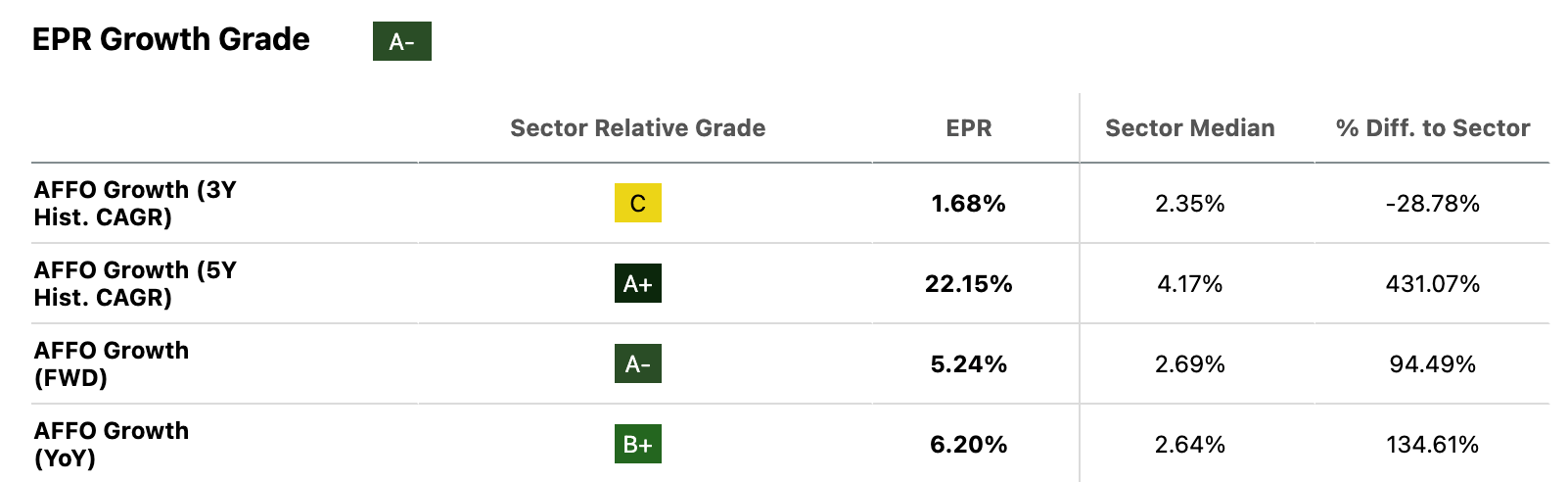

Our Quant System currently highlights EPR’s rapid Growth Grade increase–currently an ‘A-’, when only six months ago it was rated a ’C’. Investors should consider capturing this momentum heading into the summer. As shown below, EPR scores strongly on its AFFO Growth (5Y CAGR and FWD) scores, with its AFFO Growth [FWD] nearly doubling the sector median figure at 5.24%.

In a traditional commercial real estate setup, high interest rates have the potential to derail cash flow as maintenance management costs rise. However, EPR’s triple net lease structure [NNN] protects them from rising inflationary pressures on margins.

Under long-term agreements, tenants are legally obligated to pay for 100% of the property-level costs that are subject to rising input costs. This includes taxes, insurance, and utility costs. This structure has provided an exceptionally strong buffer for AFFO growth.

Additionally, EPR includes annual rent escalators, which are usually tied to the Consumer Price Index [CPI]. This helps to insulate the company’s cash flow from internal cost pressures. And ultimately, providing the basis for a phenomenal dividend profile.

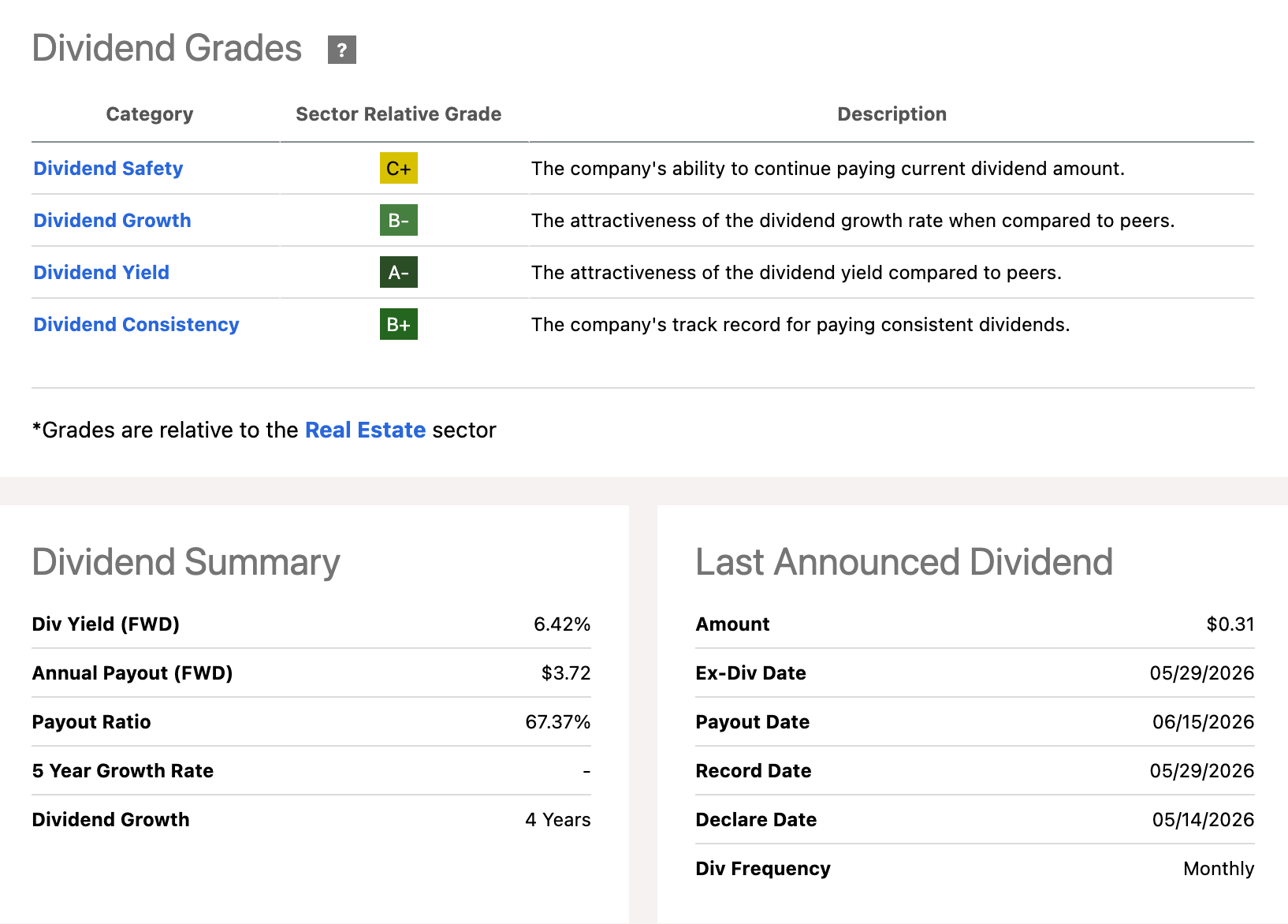

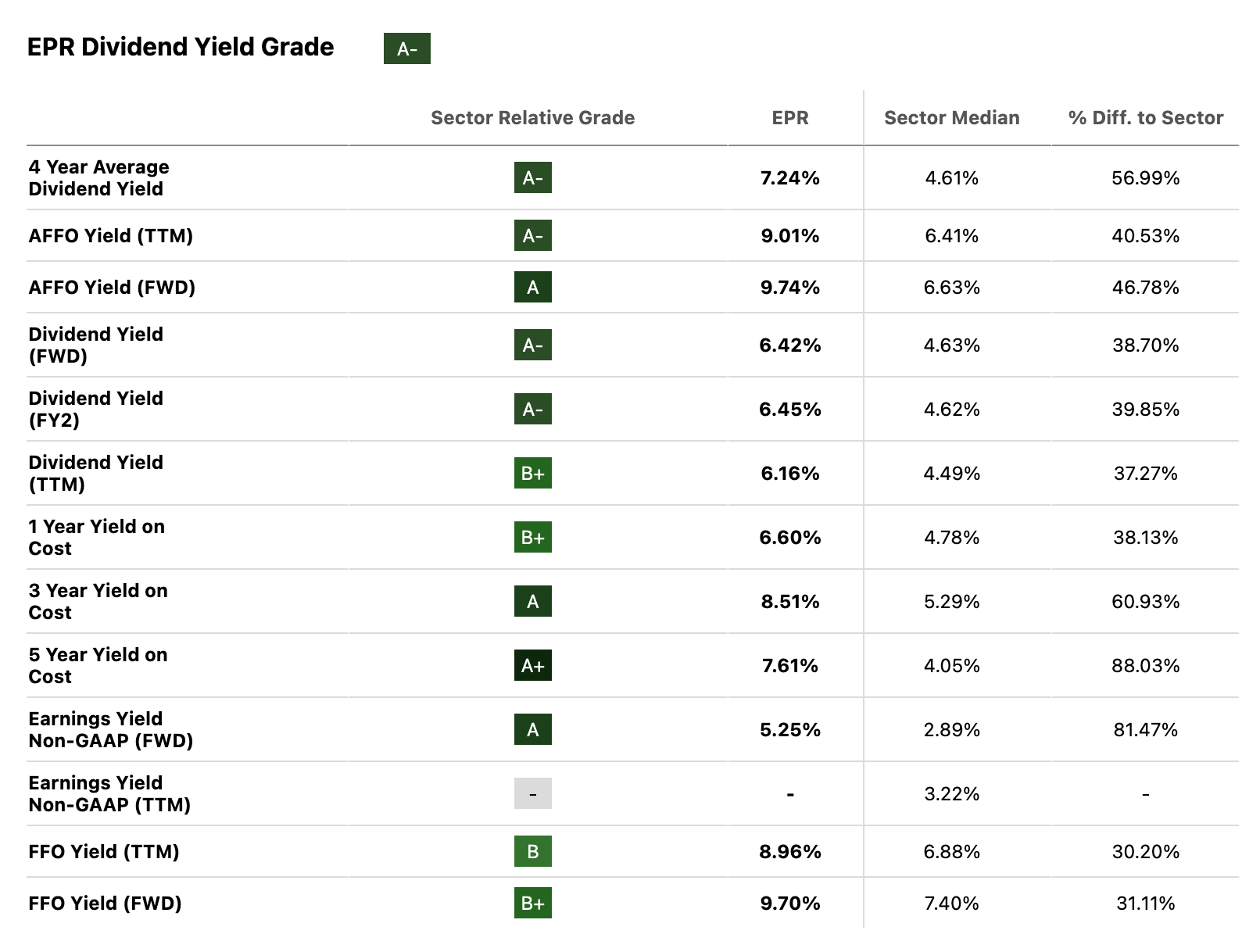

Dividend Grade Scorecard

EPR’s balance sheet strength passes through to its incredible ‘A-’ Dividend Yield Grade. The income profile is headlined by its 6.42% Dividend Yield [FWD], outperforming the sector median by 40%. More importantly, its 9.74% AFFO Yield [FWD] is nearly 47% higher than the sector median and provides a profitable yield gap of 3.42%, anchoring the company for strong growth ahead while protecting its payout.

Looking Ahead: Income Investing Strategies

With yields once again on the move, the passive playbook for income investors is quickly becoming obsolete. Navigating this higher-for-longer rate environment requires active management and a tactical rotation into companies that can not just survive, but thrive.

The coming months could be difficult for growth and value opportunities that lack income-generating payments. It’s probably timely for investors to build a portfolio that can withstand volatile markets amid rising inflation concerns, midterm elections, and geopolitical tensions. Ultimately, today’s picks prove that income opportunities are still very much available in today’s market environment–delivering strong, safe returns while actively shielding your capital from broader market volatility

Leave a Reply