Category: Global high‑yield equities Yield: ~11% Role: Global diversification + high income Why monthly: UCITS “SuperDividend” share classes pay monthly

This prevents the portfolio from becoming too US‑centric.

4) Global Enhanced‑Income Equity (Monthly) – 20%

Category: Global equity income with option overlays Yield: ~5–6% Role: Smooths income when volatility drops Why monthly: UCITS enhanced‑income share classes pay monthly

Here are five of the highest‑yielding ETFs that are tradeable in the UK, based strictly on current yield data from UK‑accessible sources. These are all UCITS ETFs, meaning they can be bought via UK brokers and held in an ISA or SIPP.

Top 5 High‑Yielding ETFs (UK‑Tradeable)

Ranked by current dividend yield (GBP‑based where available)

1. Global X Nasdaq 100 Covered Call UCITS ETF (QYLD‑style UCITS version)

Yield:12.11%

Type: Covered‑call equity income

Region: US (Nasdaq 100)

Notes: Very high yield due to option‑writing; lower growth potential.

2. Global X SuperDividend UCITS ETF (SDIP)

Yield:11.11%

Type: Global high‑dividend equities

Region: Global

Notes: Screens for the highest‑yielding stocks globally; income‑maximising.

3. Global X S&P 500 Covered Call UCITS ETF

Yield:9.91%

Type: Covered‑call equity income

Region: US (S&P 500)

Notes: High income, reduced upside due to call‑writing.

Deep Discounts, High Yields: 4 BDCs Paying Up to 13%

Brett Owens, Chief Investment Strategist Updated: June 12, 2026

Stocks are sky-high, but us contrarians are looking for dividend deals. And we found them in one forgotten corner of the Wall Street world. Here, we’re going to bank yields between 11% and 13%.

That’s right—up to 13%, for as little as 68 cents on the dollar.

What does that mean? Well, these funds are trading at discounts as large as 32% off their book values.

Where are we looking? We’re talking about business development companies, or BDCs. These are publicly traded firms that lend to mostly privately held companies—small and medium-sized businesses.

The BDC business itself can be a bit of a cardiac kid. It’s all about getting paid back on these loans. The smart lenders can do very well over time. The sector is so potentially lucrative that it attracts some less-than-ideal managers—hence a bit of a shady reputation.

But in these shadows is where we can find value.

2026 has been rough sledding for BDCs. There have been fears about the creditworthiness of the loans they’ve extended. It’s come to fruition—about one in four companies in the non-penny-stock BDC world have cut their dividends over the past few months.

Ugly, ugly, ugly.

So why are we diving in this dumpster for dividends? Well, we’ve got three reasons to be intrigued.

BDCs tend to own floating-rate debt, which means their income rises as short-term rates move up. And inversely, it drops as rates drop. High oil prices have put Federal Reserve rate cuts on hold indefinitely, and this has helped stabilize BDC income.

Even after the dividend cuts we’ve seen, BDCs still remain one of the top sources of income for dividend investors. I mean, come on—where can we find yields like these?

Hey—these stocks are rarely this cheap. Industry valuations haven’t been this low since COVID. As contrarian investors, we are stepping in to sort through the wreckage.

So let’s talk about these dividend payers, dishing between 11.8% and 13% yields. We are looking for values here, not falling dividend knives, so these details matter.

Nuveen Churchill Direct Lending Corp (NCDL) Dividend Yield: 11.8%

Investing in business development companies often means hitching our wagons to the market’s most prominent asset managers. Take, for instance, Nuveen Churchill Direct Lending Corp. (NCDL), which bears the name of both fund manager Nuveen (the asset manager for TIAA) and BDC manager Churchill, a Nuveen affiliate.

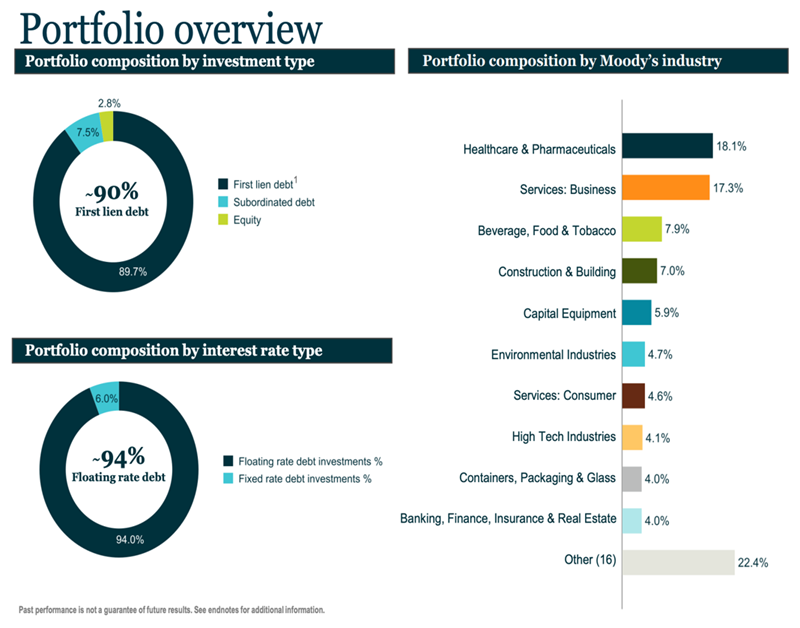

NCDL targets U.S. middle-market companies backed by private equity sponsors. It’s currently invested in 236 companies across 26 industries, with significant bents toward healthcare/pharmaceuticals and business services. It spreads out risk well, too—its top 10 holdings make up just 13% of the portfolio’s weight.

Nuveen’s BDC does most of its financing via first-lien debt, and the lion’s share of that is floating-rate in nature—helpful in that higher interest rates can boost loan income, though they can also drive down loan demand.

Nuveen Churchill Direct Lending has less than three years’ worth of trading under its belt, most of it just pinballing up and down. And because we’re in the midst of one of its sharp downturns, we can buy it for a cavernous 26% discount to its net asset value (NAV).

But what would we be buying?

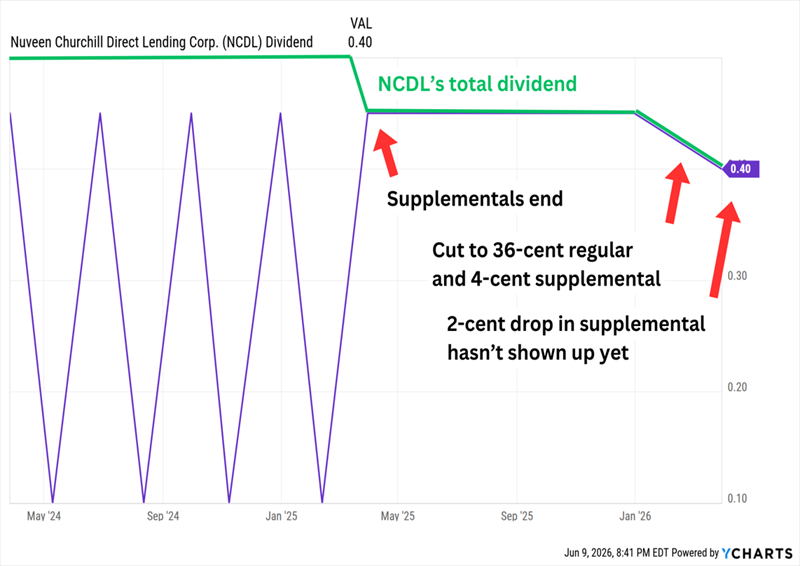

A big dividend, sure—but one that’s been quietly shrinking since NCDL first hit the market. The 45-cent quarterly with a 10-cent supplemental on top? Gone. The supplemental dried up first. Then this year, the base got cut to 36 cents, with a 4-cent top-up thrown in as a consolation. Then that supplemental shrank to 2 cents in Q2.

Death by a Thousand Trims?

What makes the underperformance and dividend difficulties surprising is that NCDL at least appears to be a solid operator. Non-accruals grew in the most recent quarter, but at just 1.3% of the portfolio at cost, so credit quality is excellent. (Non-accruals are loans that are delinquent for a prolonged period, usually 90 days.) It has a favorable fee structure thanks to waivers. Management is conservative and steeped in private-credit experience. Software exposure is low.

Patient investors might eventually be rewarded. Until then, Nuveen’s BDC clearly isn’t treating the dividend with kid gloves.

Blackstone Secured Lending Fund (BXSL) Dividend Yield: 12.9%

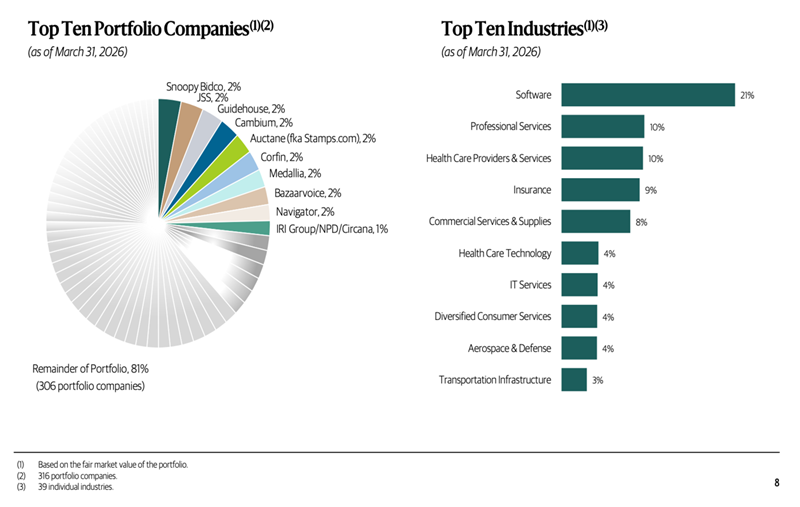

Blackstone Secured Lending Fund (BXSL) leans on the rich resources of Blackstone (BX) and its Blackstone Credit & Insurance arm. And that brings up another important aspect of many BDCs: They’re not just lenders and stakeholders. BXSL’s 316 portfolio companies also enjoy the expertise and operational support of one of the world’s largest alternative credit platforms—and Blackstone Credit & Insurance doesn’t claw fees away from the BDC for the privilege.

Blackstone’s BDC deals almost entirely in floating-rate first-lien debt. It likes larger companies in sectors with historically lower default rates. It’s plenty diversified, too, with its top holdings making up less than 20% of assets.

However, while the portfolio is spread across nearly 40 industries, that top industry is a red flag.

BXSL took a big step back in Q1. Non-accruals jumped to 4.7% at cost, while its net asset value declined by more than 2% quarter-over-quarter.

Every other BDC seems to be hacking its dividend. Blackstone Secured Lending Fund’s has held at 77 cents. But it might just be late to the wake: Net investment income (NII) covered the payout this quarter, yet full-year 2026 and 2027 estimates are sliding toward levels that can’t sustain it.

Shares have lost 20% of their value since July 2025, which has plumped up its static dividend to a yield of nearly 13%. But deterioration in net asset value has kept BXSL from falling into deep value territory—it currently trades at a decent 9% discount to NAV.

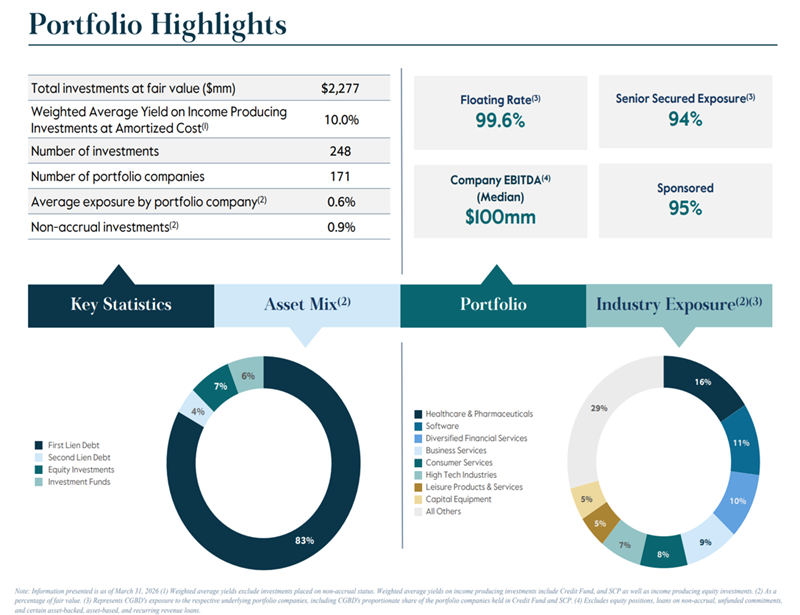

Carlyle Secured Lending (CGBD) is yet another double-digit-paying BDC tethered to a well-known asset manager: Carlyle Group (CG). It invests in middle-market companies sponsored by PE. And its preferred deal type is floating-rate first-lien debt.

But CGBD stands out for a much tighter portfolio of just 60 companies. And its financing is more spread out—first-lien debt makes up less than 85% of fair value; it also has mid-single-digit exposure to second-lien debt, equity investments and investment funds.

Around this time last year, I wrote that CGBD’s first half of 2025 was a “train wreck.” It had just put together back-to-back earnings disappointments, experienced rising non-accruals, and failed to issue a supplemental dividend for the first time in years.

Since then? Some ups, and some downs.

The distribution was pared down even more. After a couple quarters of keeping the dividend level, CGBD in April announced a 12.5% cut to 35 cents per share.

But the company has been putting together more promising results. While CGBD’s NAV declined by more than 2% during the first quarter, NII beat estimates, and non-accruals declined to just 1% of cost after portfolio company Alpine restructured its balance sheet. Carlyle Secured Lending also has a pair of joint ventures—Middle Market Credit Fund (MMCF) and Structured Credit Partners (SCP)—that are continuing to ramp.

When I looked at Carlyle Secured Lending in mid-2025, it had been greatly underperforming other BDCs for months. It has continued to decline since then, but its red ink has been more in line with the industry. Still, that has dragged CGBD’s price down to a 32% discount to NAV, putting this Carlyle vehicle in the cheapest third of traded BDCs.

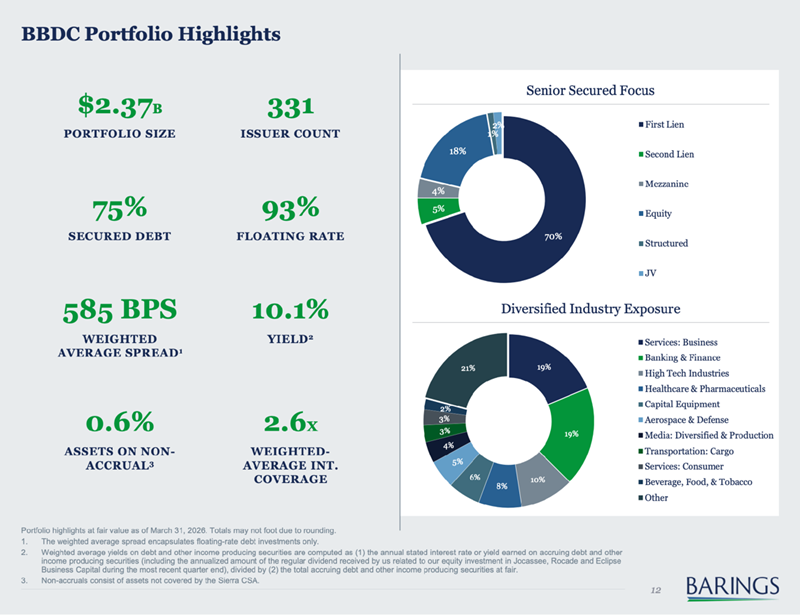

Barings BDC (BBDC) Dividend Yield: 12.3%

Barings BDC (BBDC) hasn’t always been tied up with manager Barings LLC. It was known as “Triangle Capital” for many years until August 2018, when the company rebranded, trying to put years of write-offs and dividend cuts in the rear-view mirror.

It wasn’t just a brand refresh, either. The new name reflected its new relationship with global financial services firm Barings, which became an external advisor and went to work cutting out the portfolio’s rot.

Today, Barings invests primarily in middle market companies owned by PE, though about 5%-15% of its investments are “non-sponsored” upper-middle-market and opportunistic middle-market deals, and another 5%-10% is exposure to Eclipse Business Capital and Rocade Capital—originators of middle market first-lien loans. BBDC has the lowest exposure to first-lien debt of the group, at just 70%. Roughly 20% of its deal mix is in equity, and the rest is scattered among second-lien and mezzanine debt, as well as other financing options.

We’ve already booked gains in Barings BDC twice through our Dividend Swing Trader service, so I constantly keep my eye on BBDC for short- and long-term opportunities alike.

Last year, I was encouraged by a string of small quarterly supplementals—the company hadn’t made “top-up” specials in a decade. They didn’t last, but the regular dividend has remained intact, powering a 12%-plus yield.

But that yield might have a clock on it. Earnings are pacing below the dividend, and the math only works as long as spillover earnings can bridge the gap.

One helpful development just popped up about a week ago. Barings BDC terminated a credit support agreement, which will result in a $67 million payout by the end of the month—money the company can use to fund additional investments.

And while BBDC has been a source of relative strength in 2026, down just a few percent versus double-digit declines for the BDC industry, it’s still dirt-cheap. This mega-payer currently trades at a 23% discount to NAV.

Avoid the Retirement ‘Death Spiral’: Collect 8% or More for Life

You’ve seen what these BDCs are paying. Now imagine a portfolio engineered to generate 8% or more—without the dividend cuts, the NAV erosion, or the Fed uncertainty hanging over private credit.

And you need that level of income, because traditional strategies just aren’t cutting it anymore.

Just look at people trying to get by with the “4% rule.” It works until it doesn’t.

Every few years, the market will dip and force you to sell more shares when prices are low—which means when shares rebound, you need an even bigger gain just to get back to your original value.

TR chart, where because of the modest yield you might have re-invested the dividends back into your higher yielding shares in your Snowball.

The holy grail of investing is where you take out your capital and re-invest in another high yielder and still receive income from you original purchase at a cost of zero, zilch nothing and a yield of

The current yield is 3.7%, so everything crossed for a market crash, if you want to buy.

Lots of patients needed as you see from the chart, it spends most of the time going sideways or falling because of the dividends being paid.

If you bought just before the xd date, the price has currently always moved higher than the price fall due to the dividend going xd.

Anyone buying nearer to the end of a bull market than the beginning is likely to lose money.

If you can get a decent entry price/yield the share could be pair traded and the ‘secure’ income re-invested into a higher yielder in your Snowball.

Investment trusts offer a huge range of investment possibilities, and are a great way for beginner investors to get their money working harder for them over the long term.

Anyone getting started in investing will likely be intrigued by the concept of investment trusts. There is, on the face of it, a lot to learn, from whether or not to worry about discounts to how different trusts use gearing.

But for beginner investors, investment trusts can be boiled down to fairly simple fundamentals. They are a form of active fund that trades on a stock exchange, just like a stock. In fact, they are stocks – each investment trust is a listed company in its own right.

“Investment trusts offer diversified portfolios and many have long records of preserving and growing the value of people’s savings,” says Nick Brotton, research director at the Association of Investment Companies (AIC), an industry body that represents nearly 300 investment trusts.

“Many trusts make great first-time investments whether you’re looking for income, growth or a mixture of the two,” he adds.

The AIC has collated the recommendations of various investment industry experts to build a list of the best investment trusts for beginner investors.

UK investment trusts for beginners

Beginner investors who want to use investment trusts to gain exposure to the UK market could consider one of these for their portfolio.

City of London Investment Trust

City of London (LON:CTY) is one of the AIC’s dividend heroes, meaning that it has increased its dividend payout every year for 20 consecutive years.

It is over 100 years old, and manager Job Curtis has run the fund for 34 years, favouring “good quality, well-managed companies, bought at reasonable share prices”, says Emma Wall, head of platform investments at Hargreaves Lansdown.

“A new investor may want to consider an investment trust with a long track record and a manager who has been at the helm through many economic cycles,” said Paul Chilver, director and financial planning manager at Birkett Long IFA. “The City of London Investment Trust ticks both these boxes.”

Chilver added that City of London’s focus on well-known FTSE 100 stocks would be reassuring to beginner investors.

Fidelity Special Values

For a broader play on the UK’s stock market beginner investors could consider Fidelity Special Values (LON:FSV).

“The UK stock market has performed very well this year, but it’s been led by the big blue chips of the FTSE 100,” said Laith Khalaf, head of investment analysis at AJ Bell. “If small and mid caps start to motor, this trust stands to benefit more than most broad UK stock market funds, including index trackers.”

Global investment trusts for beginners

Here are the experts’ picks for investment trusts with a global focus.

Scottish American Investment Company

Scottish American (LON:SAIN) is “a great one-stop-shop trust for those with an appetite for risk, investing predominantly in global equities but with a small allocation to bonds, property and infrastructure”, says Wall.

Its managers James Dow and Ross Mathison seek out companies with dependable income alongside the potential for inflation-beating profit growth.

“They also need to show resilience through the economic cycle,” said Wall, adding that the trust is a dividend hero having increased its dividends for more than 50 years.

F&C Investment Trust

Beginner investors that want a broad play on the global stock market could consider F&C (LON:FCIT).

“It provides access to a very broad and well managed portfolio, delivering steady long-term capital growth alongside an attractive dividend income,” says Philippa Maffioli, senior adviser at Richmond Investment Managers.

Murray International Trust

Maffioli also recommends Murray International Trust (LON:MYI) to beginner investors.

“The trust focuses on achieving long-term returns that outpace inflation, giving investors a strong foundation for the future,” she says.

Alliance Witan

With ten-year returns of 219%, Alliance Witan (LON:ALW) is the highest-performing investment trust over the last decade on this list.

It has an unusual approach to portfolio construction, whereby several external fund managers are asked to pick around 20 of their best stock ideas.

“The result is a portfolio of over 200 stocks, covering a wide range of countries and sectors,” says Kyle Caldwell, funds and investment education editor at Interactive Investor. “For investors prepared to take on a bit more risk, Alliance Witan offers a well-diversified portfolio of global shares.”

Brunner Investment Trust

Brunner Investment Trust (LON:BUT) is a growth-focused investment trust that offers “a modest but steady dividend”, says Maffioli.

“Under the experienced management of Julian Bishop and his team, Brunner has demonstrated resilience and consistency, making it a solid option for those taking their first steps into investing,” she adds.

Capital preservation investment trusts for beginners

Beginner investors might want to take a more cautious approach with their money, especially if venturing into the investing world from predominantly cash savings. These two trusts are solid choices for beginner investors that want to keep their money safe.

Personal Assets Trust

Three experts – Chilver, Khalaf and Wall – recommended Personal Assets Trust (LON:PNL) for beginner investors.

“It has a long track record in protecting investors’ money during periods of stock market volatility and currently has high exposure to government bonds and gold,” said Chilver.

Khalaf particularly likes the balance between these defensive assets with high-quality companies, and Wall highlights the focus of managers Charlotte Yonge and Sebastian Lyon on preserving investors’ capital.

“As well as a good first-time option, this trust can provide ballast to more established equity-biased portfolios,” Wall adds.

Capital Gearing Trust

Capital Gearing Trust (LON:CGT) makes a sound choice for cautious beginner investors because of its heavy weighting towards bonds.

“For those dipping their toes into the stock market for the first time, seeking out funds that provide plenty of diversification is a sensible start as it helps to keep a lid on risk,” said Caldwell. “Among the options is Capital Gearing, which has a third of its portfolio in risk assets (equities), a third in short-dated government bonds and corporate bonds, and a third in index-linked bonds.

Glenstone, the largest shareholder in Alternative Income REIT (AIRE), has made a £56.3m cash bid for the company, three weeks after making a public approach.

The 70p per share offer is 3.5p, or 5.3%, higher than its previous offer of 66.5p which the AIRE board rejected in November 2025. However, it is just 0.4% above AIRE’s 69.7p share price on 14 May before Glenstone confirmed its approach and 1.4% more than last night’s closing price of 69p.

Moreover, it is pitched at 17% below net asset value at 31 March compared to the 3% discount AEW UK REIT (AEWU) offered in its potential proposal which the board deemed fair value but did not proceed after talks broke down in April.

Glenstone, a £97m REIT listed on Guernsey’s International Stock Exchange (TISE), owns 24% of AIRE’s shares and Adam Smith, a Glenstone director who sits on AIRE’s board, holds 2.4%, giving it a total stake of 26.4%.

In addition, Glenstone has received a written indication of support from Hawksmoor Investment Management, holder of a 6.2% stake.

Glenstone said it was a long-standing shareholder of AIRE, having first bought shares in a tender offer in November 2020. In the light of AIRE’s performance and failure to grow since its flotation in 2017, Glenstone said it was “disappointed” that a transaction capable of delivering an exit for shareholders had yet to be achieved, despite a period of sector consolidation that has seen other sub-scale real estate investment trusts be sold or taken private.

It repeated its demand to know why talks with AEWU had broken down in April during the due diligence process.

Our view

James Carthew, head of investment company research, said: “Glenstone REIT has made its opening offer for Alternative Income REIT and it looks a bit mean, coming at a 17% discount to a NAV that has been edging up recently. The question is, will anyone else step into the fray?”