A three-quarter year review of London’s Investment Company Sector

As Q3 2024 wraps up, we analyse London’s investment company sector to identify this year’s winners and losers. The FTSE Closed End Investment Index (FTSE CEI) rose +0.5% for the quarter, maintaining positive returns but trailing the FTSE All-Share’s +9.9% year-to-date. Top-performing sectors include Growth Capital and Leasing, while Renewable Energy Infrastructure and Regional REITs struggled.

By Frank Buhagiar

With the numbers in for Q3 2024, it’s time to check in on London’s investment company space. Which investment companies are having a year to remember and which are having a year to forget?

Three for three

Another positive quarter for the FTSE Closed End Investment Index (FTSE CEI). The sector closed up +0.5% for the three months ended 30 September 2024. That’s a little off the +2.3% sterling total return delivered by the FTSE All-Share over the same period, but at least the record of posting positive returns for each quarter of the year has been maintained: Q1 / Q2 2024, the FTSE CEI was up +2.3% / +3.4% respectively. With just Q4 to go, the clean sweep is on.

Year-to-date, the FTSE CEI is now showing a +6.3% positive return. Once again, a little behind the FTSE All Share’s total return of +9.9% for the first nine months of the year. Barring a barn-stopping Q4, looks like a fourth successive year of the FTSE CEI falling short of the All-Share. As the table below from FTSE Russell shows, 2020, the last year London’s closed-end space outperformed the wider market:

The shoe is on the other foot

Worth pointing out though that London’s investment companies haven’t always struggled to keep pace with the wider market. Indeed, the opposite could be argued – the wider market has struggled to match London’s closed-end sector. For, as the table above shows, over the ten-year period 2014-2023, the FTSE CEI outperformed the wider market in six of the ten years. And it turns out between 2017-2020, the closed-end fund index had its own four-year winning streak. The FTSE All-Share then merely catching up with London’s investment companies.

And according to the above table, the FTSE CEI chalked up a handsome +113% gain between 2014-2023. The FTSE All-Share by contrast could only manage a cumulative gain of +68% over the same ten-year period. The FTSE 100 too is only up +68%. Over the ten years to 2023, London’s investment companies have trounced the wider market.

In terms of the average share price discount to net assets, this stood at 13.7% as at end of September, no change on the end of August level. This compares to the average 12.8% discount as at the end of 2023 and 10.8% as at the end of 2022.

The standouts – regional and sector levels

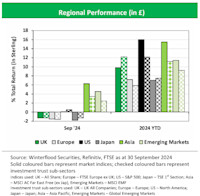

Given the UK market’s well-documented troubles – companies leaving London for the US and elsewhere; pension funds internationalising their portfolios at the expense of UK allocations; and persistently low valuations – perhaps surprising to see the UK All Companies subsector joint top year-to-date in terms of best-performing investment trust region. Alongside North America, UK All Companies up +12.2% over the first nine months of the year. As the below graphic from Winterflood shows, all regions are in positive territory year-to-date with the worst-performing investment trust region Europe still managing a +5.8% gain:

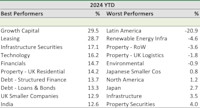

At the wider sector level, Growth Capital tops the list with a +29.5% share price total return to show for the first nine months of the year – the eight-fund sector includes the likes of Chrysalis (CHRY) which recently commenced a share buyback programme as part of its capital allocation programme; Petershill Partners (PHLL) which returned US$222m during the first half of 2024 via a mixture of dividends, a tender offer and buybacks; and the Baillie Gifford-run Schiehallion (MNTN). At the half-year stage, the sector was up +21.53% and was second in the table behind then leader Technology and Technology Innovation which boasted a gain of +28.03%. Three months on and the Technology sector has slipped to fourth after its year-to-date gain shrank to +16.2%. An underwhelming reporting season for the Magnificent Seven mega-techs weighing on sentiment there.

Not far behind Growth Capital is Leasing with a share price total return of +28.7%. Both aircraft and shipping leasing companies have been performing strongly this year. The two Doric Nimrod Air Funds reacted well to news that DNA2 is selling its five remaining aircraft to United Arab Emirates for an aggregate combined total of US$200m or £153.53m. The valuation had positive read across for sister fund DNA3 – share prices of both funds reacted well to the news.

The table below from Winterflood lists the ten best and worst performing sectors year-to-date:

Below Growth Capital and Leasing, interest-rate sensitive subsectors, such as Property, Debt and UK Smaller Companies, well represented in the best performers column. As for the worst performers, sectors comprised of just one or two funds feature highly, including Latin America (BlackRock Latin American) and Property RoW (Ceiba Investments and Macau Property Opportunities). Renewable Energy Infrastructure completes the bottom three – a mix of higher-for-longer interest rates, weaker power prices and bad weather all at work here.

The standouts – investment company level

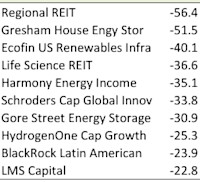

First, the laggards. Regional REIT the worst performer to date – a deeply discounted rights issue to blame. Elsewhere, five Renewable Energy Infrastructure funds in the bottom ten. As highlighted above, a range of top-down reasons for this, but also company-specific ones too. For example, a failure to find a buyer for its portfolio did for Ecofin US Renewables Infrastructure, while the suspension of its dividend didn’t help sentiment at Gresham House Energy Storage.

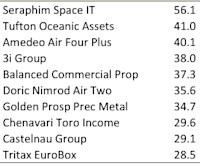

As for the winners, no surprise to learn that investment companies belonging to this year’s top-performing sectors feature highly in the best performers list. In first place, Seraphim Space from Growth Capital keeps hold of top spot, a position it held at the half-year stage. That’s despite seeing its gain on the year fall slightly to +56.1% from +58.72% as at 30 June.

As the table below shows, a small gap between Seraphim and the rest of the pack. The next two top performers both herald from the Leasing sector – Tufton Oceanic Assets and Amedeo Air Four Plus up +41% and +40.1% respectively. DNA2 also makes it into the top ten courtesy of a +35.6% rise.

Elsewhere, strong gold prices lie behind Golden Prospects Precious Metals’ seventh place. Meanwhile 2023’s top performer 3i Group still in the hunt to retain its crown – shares are up +38% over the nine months to end September. A little ground to make up true, but certainly doable. At the half-way stage, 3i shares were up +28% which was only good enough to squeak into the table in tenth place. Three months later and 3i is up to fourth spot. What’s more, the gap between the private equity giant and Seraphim has narrowed from +30.7% to +18.1%. The race to be London’s best-performing investment company in 2024 is well and truly on.

Leave a Reply