If I Were Retired Today, These 3 Income Machines Would Be My First Buys

Mar. 14, 2026

Leo Nelissen

Summary

- Ares Capital Corp., Agree Realty Series A Preferred, and Rayonier offer compelling, diversified income opportunities for a retirement portfolio.

- ARCC yields 10.4%, trades below book value, maintains a BBB rating, and has a sustainable dividend supported by low nonaccrual rates.

- ADC.PR.A offers a 6.2% yield, trades well below liquidation value, and benefits from Agree Realty’s A-rated balance sheet and net lease tenant base.

- RYN provides 5.2% yield, cyclical upside, and inflation protection, though a recent dividend reduction followed a merger; each pick addresses distinct risk/reward themes.

Introduction

As some of you may know, I was a Corporate Treasury intern in the past. That was back in 2019 when I was still figuring out what I wanted to do in life. A few months after I left to finish my master’s degree in International Business Administration (with a focus on purchasing and supply chains), my former boss retired. That’s old news and doesn’t affect your portfolio at all. However, because Henkel (the company where I interned) is a European heavyweight, he was interviewed, as he was a rather powerful treasury manager.

I’m bringing that up because I just re-read the piece. One thing stood out to me:

Treasury chief Michael Reuter has left consumer-goods company Henkel and retired at the end of September, as DerTreasurer has learned. Shortly before his departure, he and his team were able to make a splash in the capital market: Henkel issued two sterling bonds totaling the equivalent of 850 million euros, both with a negative yield. – Der Treasurer (translated)

Again, this isn’t about Henkel or about my past. This is about the last line in that paragraph, which mentioned that Henkel issued the equivalent of EUR 850 million in negative-yielding debt. Back then, people paid corporations to take their money. Sure, Henkel is an A-rated giant with terrific diversification, but it’s still “nuts” if you think about it.

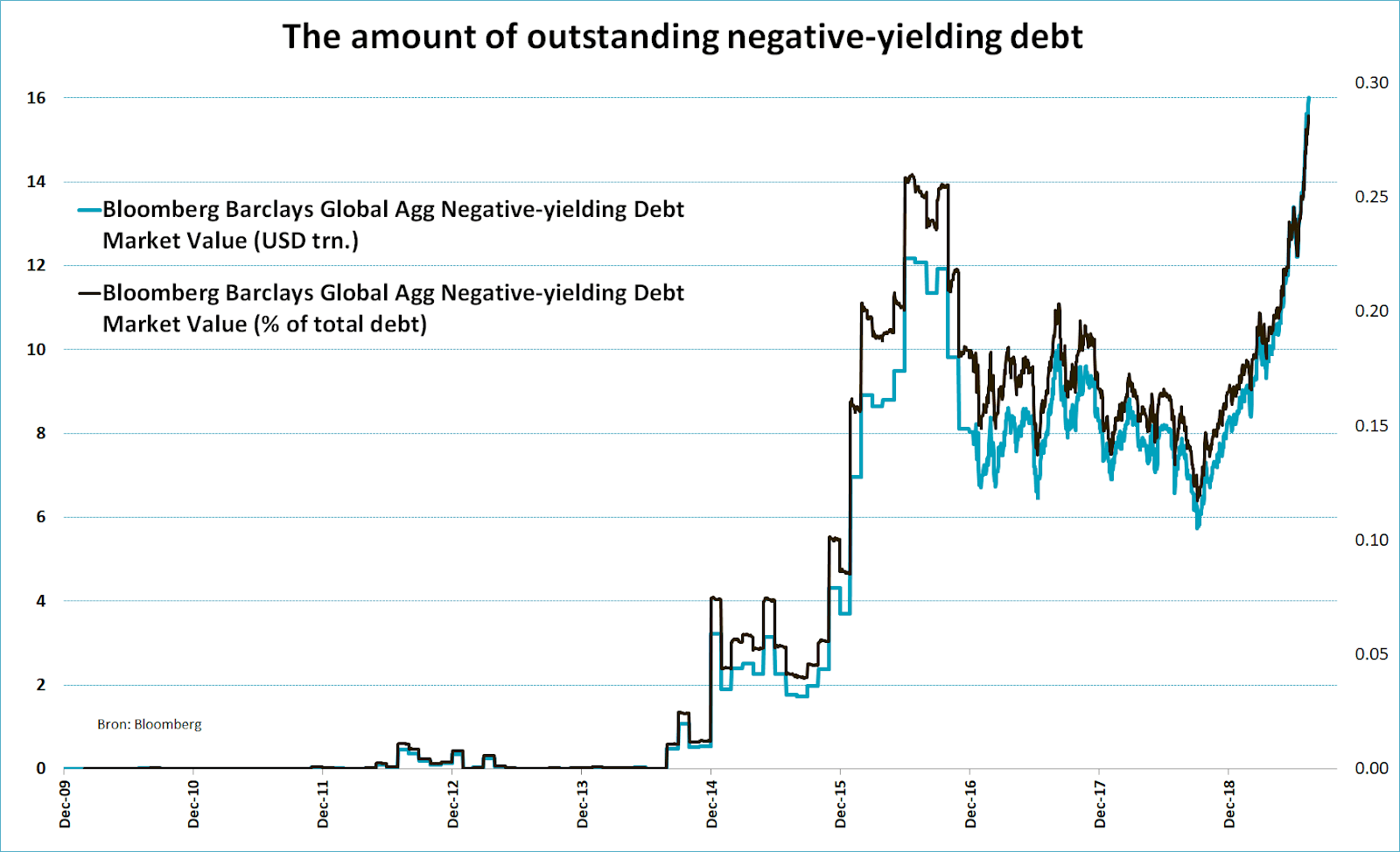

And, to use a chart from 2019, it wasn’t unusual. Back then, the total amount of debt with a negative yield was $16 trillion. More than 28% of the debt tracked by the Bloomberg Barclays Global Aggregate Index had a yield of less than 0%.

Back then, it was truly the best time to own low-risk, high-quality dividend growth stocks, as investors were aggressively chasing income as if the world would end. This was obviously fully supported by ultra-low rates in developed nations.

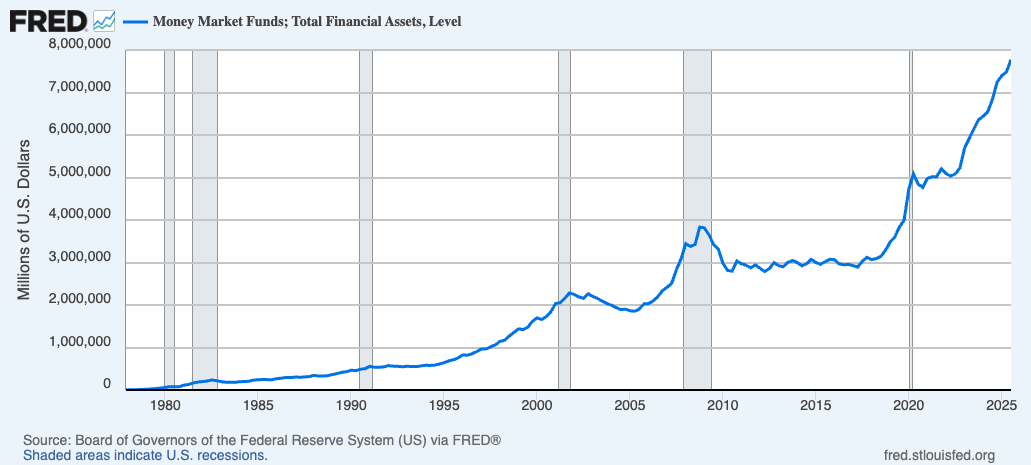

To me, it’s a perfect example of how major capital shifts impact our portfolios. Less than two years ago, when rates spiked, the exact opposite happened. Some investors (I’m painting with a broad brush again) sold equities and went into short-term bonds that yielded more than 5%. That explains the massive surge in money market assets, as we can see below.

While I am typing this, there’s close to $8 trillion in money market funds, which is basically short-term government debt (risk-free income, so to speak).

In 2020, that number was $5 trillion. Between 2010 and 2019, it was $3 trillion on a very consistent basis, as investors were buying income in other places, as the yield on short-term debt was close to zero.

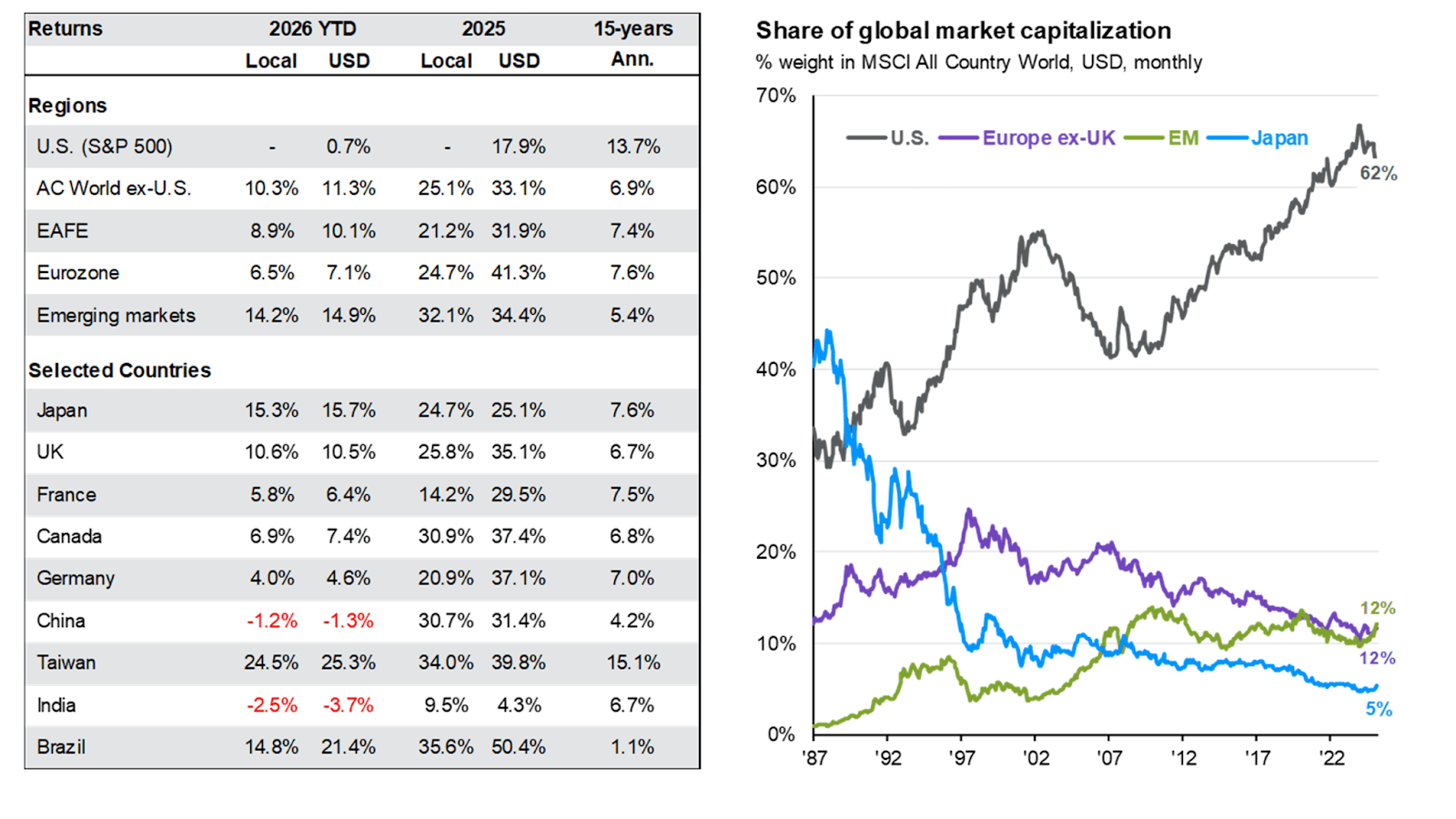

These are the capital rotations I care so much about, as they are crucial for asset management. We’re seeing the same in equities. In the first two months of this year, investors wanted cyclical value stocks (that’s my core thesis, as most readers will know) and non-U.S. equities.

As we can see below, over the past 15 years, U.S. stocks were the place to be. However, on a year-to-date basis in 2026 (that’s January-February), U.S. stocks lagged international stocks.

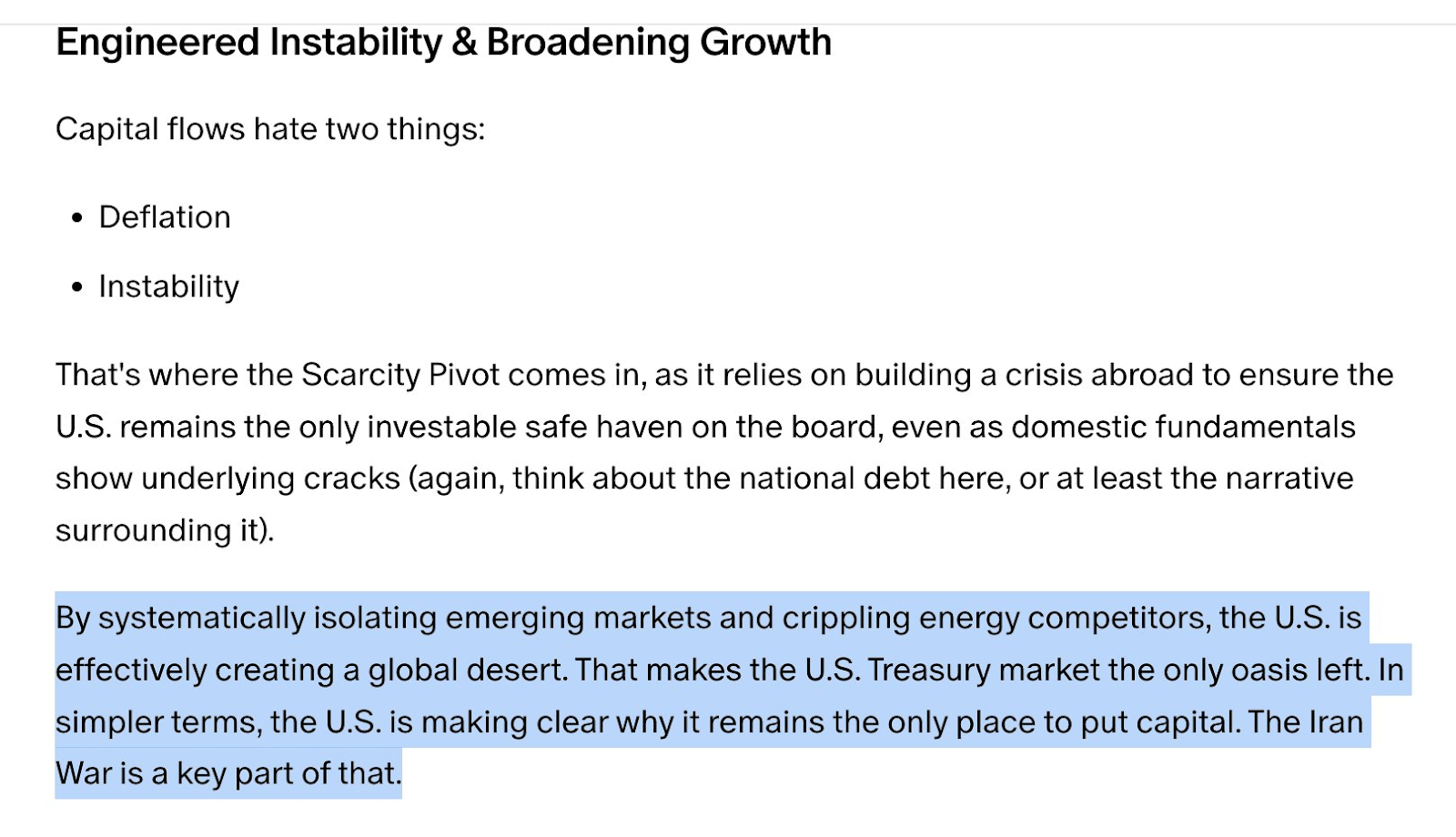

The war in Iran changed that.

My friend and business partner, Albert Marko, wrote on that, as he made the case that the U.S. is using the conflict to create new capital flows into the U.S., based on the realization that in times of distress, it has the safest supply chains (think of its oil supply), dollar safety, military power, and other tailwinds.

Bloomberg just confirmed that:

But the developments since the US and Israeli attacks on Iran reveal that America is still the go-to market for investors. If the US has warts, it remains the center of global innovation and home to the deepest and most liquid markets on the planet, a feature that becomes indispensable when economic shocks hit. After 14 chaotic months, we’re also seeing signs emerge of institutional resilience at the Federal Reserve and Supreme Court, an additional source of comfort. – Bloomberg

That’s a good thing, as it not only supports my thesis that America remains a terrific (if not the best) market for long-term capital allocation, but also because the market’s biggest companies are now in need of massive funding. While most hyperscalers (think of the Mag-7) have terrific balance sheets, AI spending is now forcing them to diversify these risks.

It was just reported that Amazon (AMZN) is issuing $37 billion in bonds. According to Reuters, the bond deal resulted in $126 billion worth of demand, which is a good sign for Amazon. And then there’s Alphabet (GOOGL), which raised $100 billion, including through a 100-year bond. It was observed 10x, according to Seeking Alpha.

At this point, I have to admit that my intro seems to be all over the place (and close to 1,000 words – sorry!).

However, it brings me to my main point, which is that as global markets are getting volatile, the U.S. once again defeats the argument that it’s not the go-to place for capital anymore. We also see that Americans are using it to issue debt for the AI transition.

Unfortunately, this creates a bit of an issue. As rates are potentially falling, the environment isn’t great for income anymore. And while we’re far away from a 2019 scenario where it costs money in some cases to lend money to corporations, it’s not a scenario where I want to be forced into deals like financing the AI revolution. I want no part in that, at least not through bonds.

This brings me to the question that people ask me quite frequently, which is what I would own if I were retired right now? It’s high-quality U.S. income that comes with both income and unique characteristics that add value to most income portfolios.

With all of this in mind, let’s look at three income ideas I would buy today if I were retired.

Here’s What I Would Buy

A big part of the intro was about the credit market. I have often said that I do not like bonds, as I’m an “equity guy.” I want to own a share of a company and grow with it over time, while generating income, in some cases.

Right now, that lending market is under fire. While Alphabet and Amazon are not having a hard time finding buyers, the private credit market is seeing cracks. Many asset managers and their Business Development Companies have sold off hard this year, including some of the best players like Ares Management (ARES) and Apollo Global Management (APO), which I consider the gold standard of private credit.

Fears are basically created by software disruption and some negative headlines regarding “unexpected” defaults that make people wonder how much bad debt is hidden in this industry. When adding that private credit is very cyclical, it explains why I am so careful in this industry.

However, I still would buy exposure here, as there are some great deals out there. One of them is Ares Capital Corp. (ARCC). It’s the BDC owned by Ares Management. Right now, I am actually looking to buy ARES in the months ahead (I’ll update you on my liquidity and plans soon). However, if I were retired, I would buy the higher-yielding BDC.

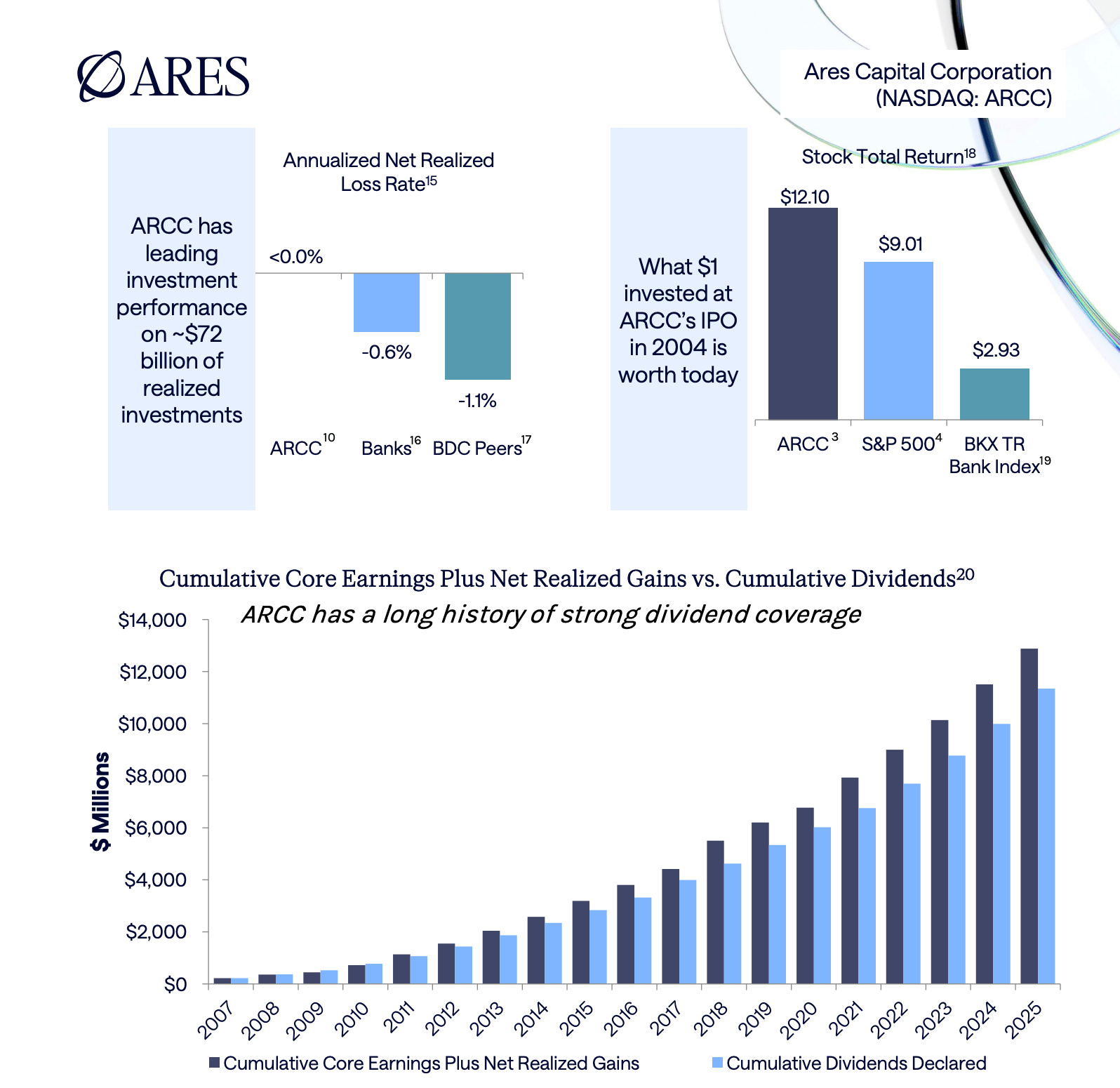

Ares Capital currently yields 10.4%. This dividend hasn’t been cut since the Great Financial Crisis. And, as of December 31, 2025, it’s a BDC with a superior total return compared to banks and BDC peers, as Ares has figured out how to find a great balance between risk (yield) and safety (picking the right deals).

Moreover, not only is this the biggest BDC on the market, but also a BDC with terrific fundamentals, as it has a BBB credit rating from all three major rating agencies (Fitch even has a positive outlook, which could mean a path to BBB+), and more than $6 billion in liquidity.

Its portfolio has a nonaccrual rate of 1.8% (at cost). That’s in line with prior year levels, according to the company. Moreover, it’s below its own long-term average of 2.8% and below the BDC industry average of 3.8%. At fair value, that number is just 1.2%.

The company also believes its dividend is sustainable:

We believe ARCC is in a good position to maintain its dividend despite market expectations for further declines in short-term interest rates. We generally set our dividend level based on our view of the earnings power of our company. While lower short-term rates present an earnings headwind, we believe there are multiple factors that can support our earnings and thus, our current dividend level for the foreseeable future. – ARCC 4Q25 Earnings Call

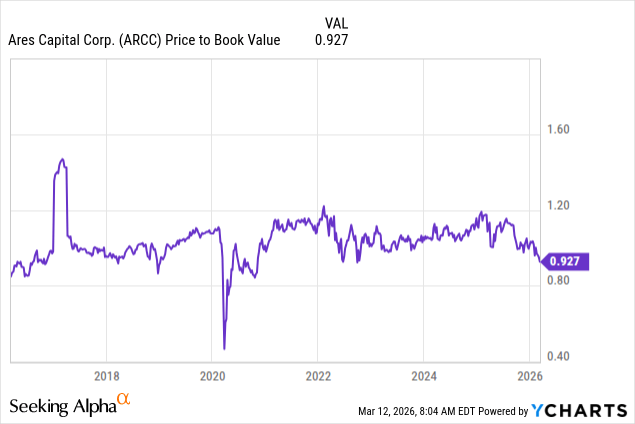

And to incorporate higher risks, ARCC is now being traded at 7% below book value.

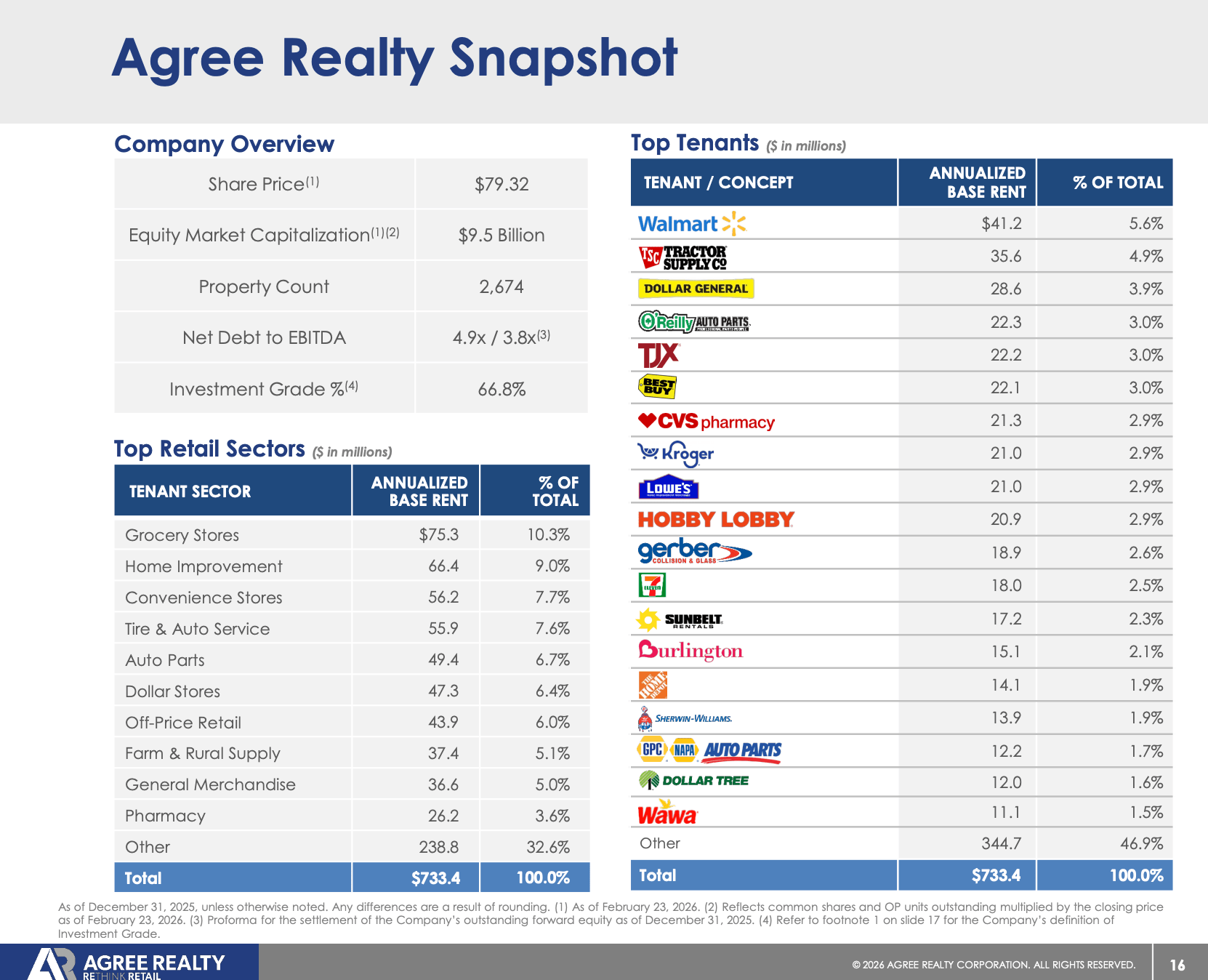

Another stock I would buy is Agree Realty Series A (ADC.PR.A), which is Agree Realty’s preferred stock. In other words, it’s somewhat of a hybrid between a bond and a stock. Investors get exposure to Agree Realty (equity ownership), yet no voting rights and no dividend growth. What they do get is bond-like dividend payments and more safety, as preferred stock is more “senior” than common equity.

Generally speaking, I dislike capped upside, which applies to assets without dividend growth. However, the risk/reward of this preferred stock is great, as it trades at $17.19 while I am writing this. That’s substantially lower than the liquidation price of $25. That’s the price you’ll get if the company were to buy back the preferred stock.

That limited upside isn’t great for long-term growth investors, yet it’s perfect for income, as it is a premium of 45% compared to the current price. That’s the upside you’ll get before you potentially lose these shares in a buyback. Moreover, because of the low price, the monthly dividend yield is 6.2%. That’s a terrific yield, roughly 200 basis points above the 10-year government bond.

As a comparison, Agree Realty (ADC) common stock yields 3.9%. That dividend has a five-year CAGR of 1.9%. On October 14, it raised the dividend by 2.3%. If we assume that the dividend growth rate holds, investors will end up with a yield on cost of 4.9% after ten years, which is still way below the rate on the preferred stock.

It also helps that Agree has an A-rated balance sheet, a portfolio that mostly caters to ultra-safe net lease tenants, and growth opportunities in areas like sale-leaseback. Moreover, as this preferred stock is cumulative, if Agree were to run into issues leading to dividend cuts, it would have to make preferred shareholders whole before it would be allowed to pay a common dividend again.

I really like this preferred stock. And, if I were to retire today, I would buy this in a heartbeat.

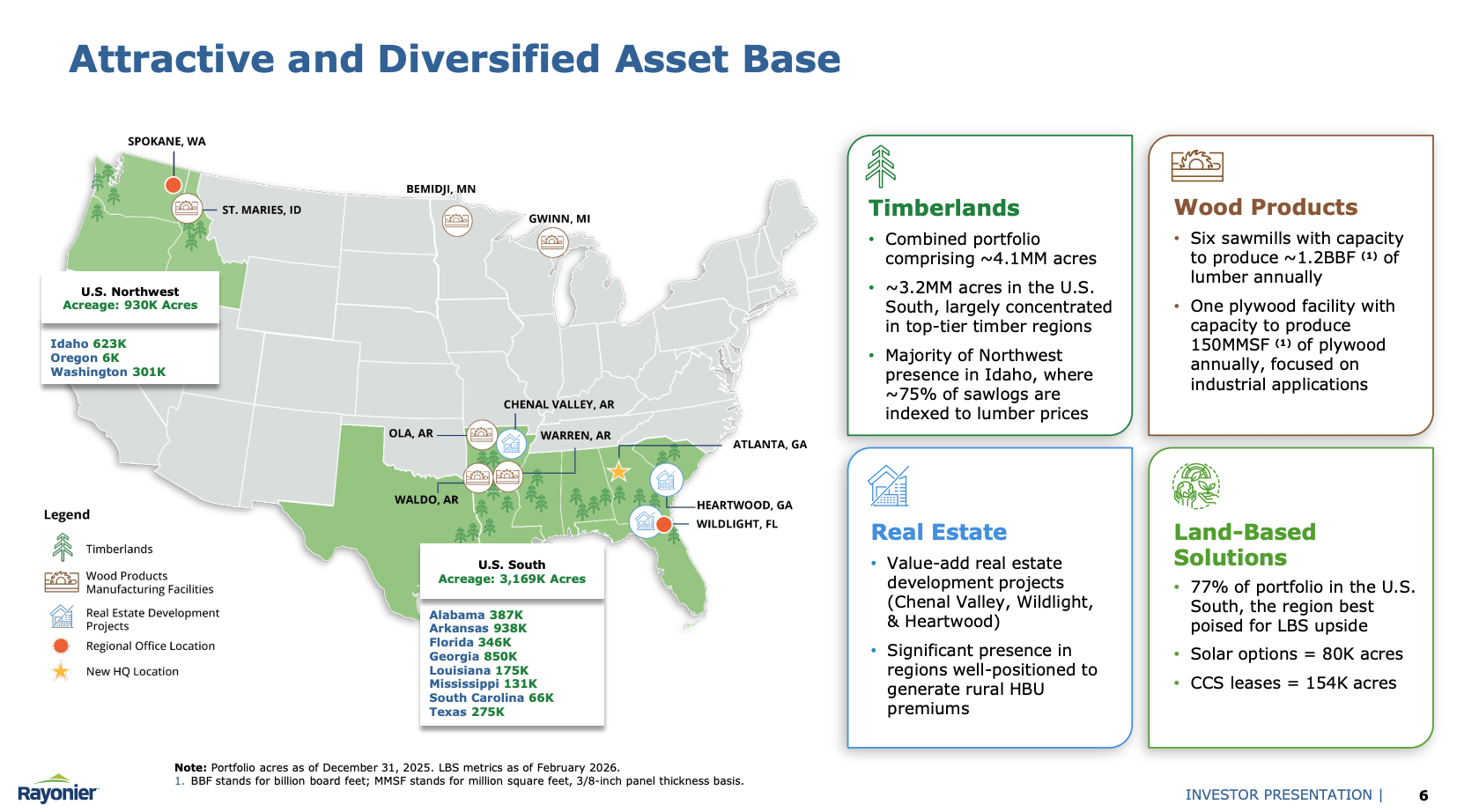

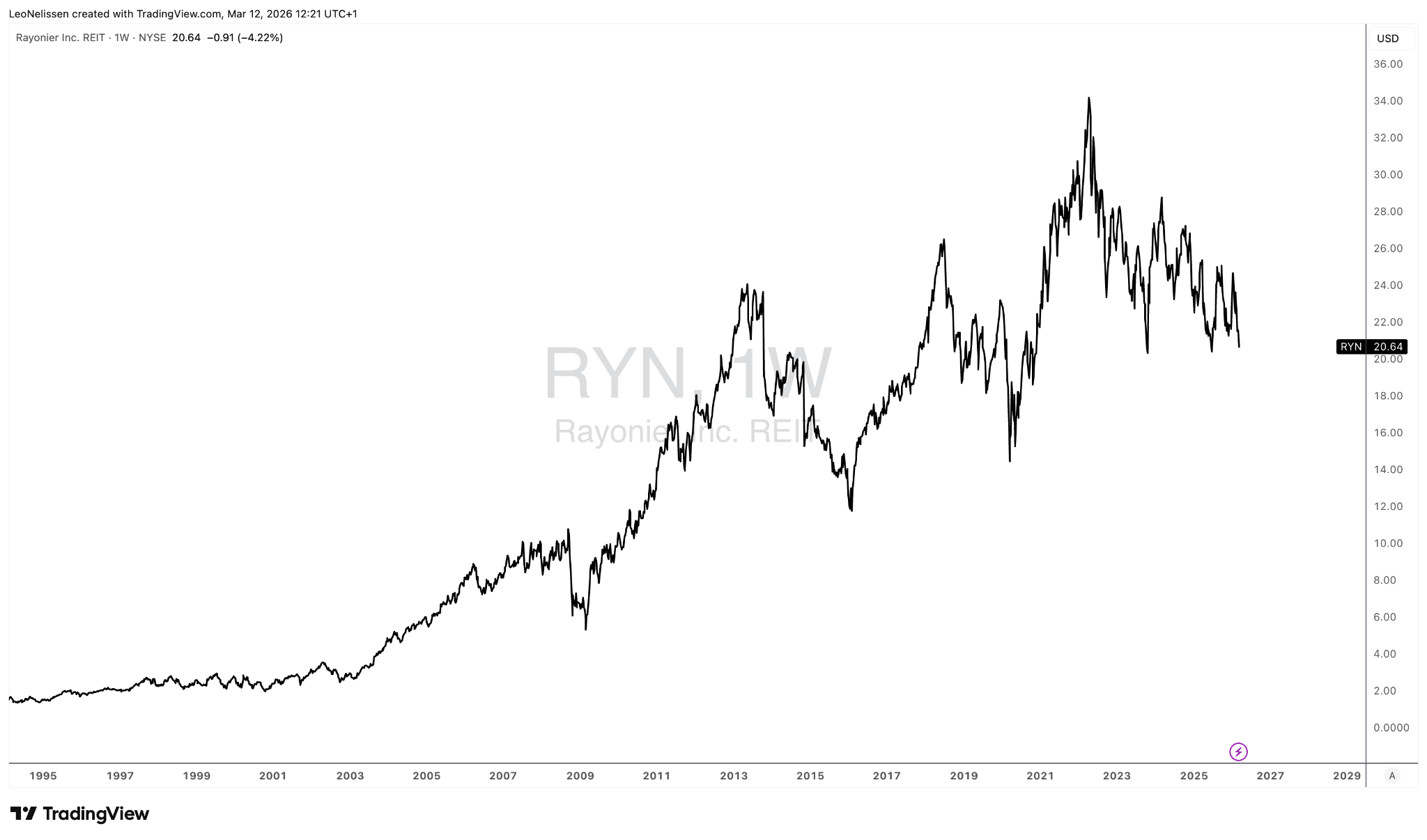

The third pick is somewhat unusual, as it’s Rayonier (RYN). This company is a specialty REIT. Technically, it’s a “Land Resources REIT,” as it owns timberland that covers more than 4 million acres after merging with PotlatchDeltic.

As a result, their business model is based on three factors. They sell timber to lumber mills, where lumber for a wide range of purposes is created. Homebuilding is a major factor. This business is cyclical, as it depends on pricing and demand. It also generates high-quality revenue from strategic master-planned communities. That’s high-quality developed land for new housing communities. It’s much less volatile than selling timber.

Last but not least, they use land for value-adding opportunities like solar, carbon credits, bioenergy, and so much more.

As we can see in the total return chart below (capital gains + dividends), RYN isn’t a low-volatility stock, which is why I have always avoided it. If I want a volatile stock, I prefer buying a housing supplier that tends to rise faster during times of strong economic growth.

The good news is that the RYN risk/reward looks highly attractive.

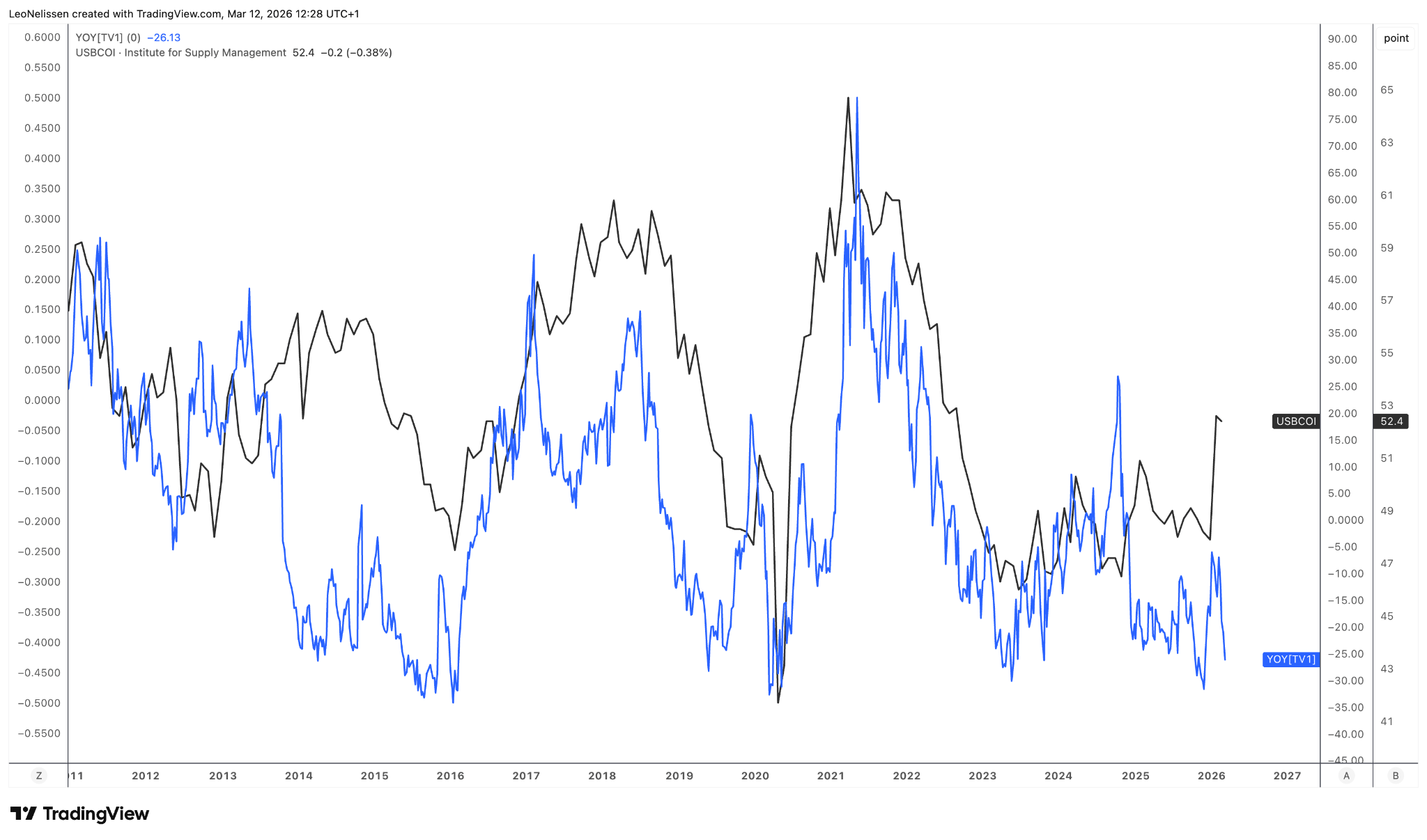

As we can see below, despite the increase in the ISM Manufacturing Index (the black line), the year-over-year performance of RYN has continued to go down. At this point, I like the risk/reward a lot.

If we get broadening economic growth, we’ll see both pricing and demand tailwinds in this space. Moreover, while the dividend was cut by 4.6% in February, it was part of the merger. Currently, it yields 5.2% based on a quarterly dividend of $0.27.

At points like these, I think RYN makes for a great investment that provides income, a great risk/reward, as well as inflation protection for an income portfolio, as this stock tends to do well in times of rising inflation.

Generally speaking, I truly believe that all three of these picks bring something truly unique to the table that I find highly compelling for an income portfolio. And, as I always say, stay tuned for more ideas!

For now, here’s a short takeaway:

Takeaway

My introduction was pretty chaotic today. However, my point is that it’s all about identifying capital rotations and finding the best risk/reward for an income portfolio, or any portfolio, really.

At a time when money market funds are overflowing with capital, rates are likely to be pressured, and economic growth is set to rebound, I like to apply a diversified approach to buying high-quality income.

If I were retired today, I would buy ARCC for elevated BDC income, preferred Agree Realty stock due to a 6% yield and a terrific risk/reward, and Rayonier because it provides 5% income and cyclical tailwinds and elevated inflation protection.

These are three different themes, but all have one thing in common, which is a unique ability to add value to an income portfolio.

Three Risks You Need To Know

- The biggest risk for ARCC is credit risk. While it is protected against further declines in short-term rates, a domino effect in credit could lead to elevated non-accrual rates.

- For Agree Realty’s preferred stock, the biggest risk is a surge in long-term government debt rates. As these compete with preferred stock due to the bond-like dividend payments, they could keep a lid on capital gains.

- For RYN, the biggest risk is a sluggish housing market and related pricing headwinds in lumber.

Leave a Reply