The recognised financial advise is to concentrate on the body and leave the tail to luck. Don’t buy anything unless you are prepared to hold for a minimum of 5 years is the mantra.

Good news for those charging for the advice, no complaints for at least 5 years.

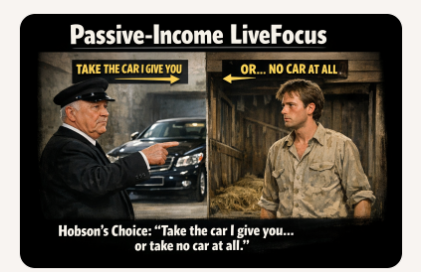

When you want to take income from your portfolio, one piece of advice is to buy an annuity.

Canada Life figures show the 65-year-old with a £100,000 pension pot could buy an annuity linked to the retail price index (RPI) that would generate a starting annual income of £3,896. That’s up from £2,195 in the New Year following a 77% spike in rates this year.

Oct 22

A huge gamble with your future as the rate could be as above or higher but you have to surrender all your capital so Hobson’s choice.

The next option is to use the 4% rule, you can DYOR using the search button above.

Some people will not trade a dividend re-investment plan as they only concentrate on growing their capital.

If you trade a Snowball, as you never intend to sell any shares as you need the income to live on, the capital figure is of no importance.

A dividend investment plan is the only plan that you write down the yearly outcome and thus a total amount of income you will have when your retire.

You need to major on a ‘secure’ dividend, although no dividend is 100% secure, some dividends are more secure than others.

For those who near to their retirement date may prefer to

move their Snowball to less risky dividends, if they have achieved their plan.

If you have longer to retire you still need some ‘secure’ dividends as a bed rock for your Snowball but could include more higher yielding Investment Trusts and ETF’s. All still subject to the rules for the SNOWBALL

Leave a Reply