Are UK income trust yields a problem for investors?

By Val Cipriani IC

Published on March 17, 2026

It’s a basic principle of investing: when prices go up, yields go down. This applies to equity income assets as well as bonds. In the past year, UK companies have seen their share prices rise enthusiastically – even after the dip caused by the war in Iran, the FTSE All-Share is up 22.4 per cent in the year to 16 March

The flipside is that a stock market known for its income generation actually generates a lot less income than it used to, at least as a proportion of the price you pay for the assets. In December 2023, AJ Bell estimated a dividend yield for the FTSE 100 of 3.9 per cent for that year and 4.2 per cent for 2024. Fast forward two years, and the figures were 3.2 per cent for 2025 and 3.4 per cent for 2026. The drop has also partly been caused by companies sometimes prioritising buybacks over dividends.

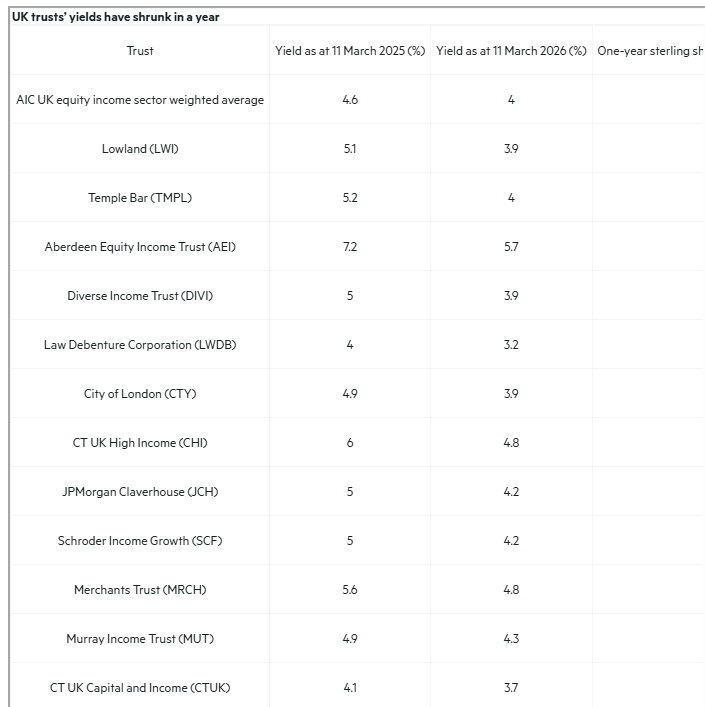

Investment trusts in the Association of Investment Companies’ UK equity income sector are also yielding less as a result. In the past year, the sector’s average yield has fallen by 0.6 percentage points. The table below shows how the trusts’ yield has changed over the course of a year, as well as their share price performance over the period.

As you’d expect, there is some correlation between those that have performed particularly well and those on lower yields. The six top performers, whose shares returned around 30 per cent or more, all saw their yields decrease by more than a percentage point. These trusts tend to take a value approach, particularly Lowland (LWI) and Temple Bar (TMPL), which now yield around 4 per cent, and traditionally invest in dividend-rich sectors, such as financials.

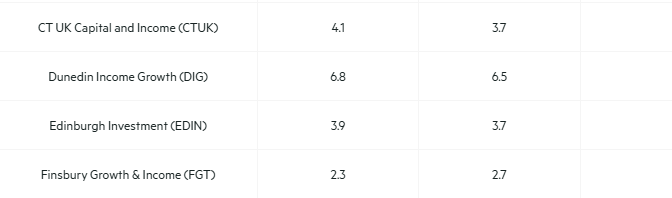

Then there are trusts with a quality tilt, whose performance has been less strong. Some of these have traditionally tended to have lower yields than their value counterparts, but now look more attractive on this metric – at 3.7 per cent, Edinburgh Investment Trust (EDIN) now yields nearly as much as City of London (CTY), for example. Nick Train’s Finsbury Growth & Income (FGT), the one trust in the sector that lost money this year, actually saw its yield increase as a result of this drop, albeit at 2.7 per cent it remains relatively meagre compared with peers.

For some trusts, discounts to net asset value (NAV) have also narrowed as well as yields, with the sector’s average discount dropping from 5.6 per cent on 28 February 2025 to 3.7 per cent a little more than a year later.

Of course, yields are not everything. Dunedin Income Growth (DIG) has the highest yield in the sector – 6.5 per cent – after introducing an ‘enhanced’ dividend policy that will see it pay out 6 per cent of its NAV, partly out of capital; but its performance record over the past five years looks decidedly poor.

After such a long period of lukewarm performance for the UK market, it would be ridiculous to complain about this change in fortune, regardless of whether or not it lasts. But income investors are less spoiled for choice. They may want to review their portfolio, and remember that the UK market is not the only option – for example, investment trusts in the AIC global equity income and Asia Pacific equity income sectors yield 3.8 per cent and 5 per cent, on average, respectively. That compares with a UK average that has fallen from 4.6 per cent to 4 per cent over the past year.

BUYING YIELD

It’s a win, win, because when you buy a dividend hero Trust the yield you will receive is the yield when you buy, gently increasing as long as you own the Trust

Remember as an example only if you buy PHP today you should receive 5 dividends in just over the calendar year, an enhanced yield of around 9%. of course there is a chance of a capital gain/loss but if you need to pay your grocery bill, a Trust to DYOR

RUNNING YIELD

It’s a win,win because if you buy a dividend hero as the price rises the yield falls and hopefully, you could if you

You could achieve

In that you take out your stake, when/if the Trust doubles and re-invest in another high yielder, also receiving income from a Trust that sits in your Snowball at zero, zilch cost. If the Trust you own becomes a low yielder because the price has risen, you can always re-invest the dividends back into your high yielding shares in your Snowball.

The power of the market is that if you don’t CPA, losses are limited to 100% but gains are unlimited.

Leave a Reply