Trust Intelligence from Kepler Partners

Investor Edition

Special report

SIPPing from the income cup

Income diversification provides flexibility in retirement.

David Brenchley

Updated 17 May 2026

Disclaimer

This is a non-independent marketing communication commissioned by Schroder Investment Management. The report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on the dealing ahead of the dissemination of investment research.

Two point one trillion dollars is a large number. At just over £1.5trn, it would buy you the 15 largest companies listed on the London Stock Exchange, including the drugmakers AstraZeneca and GSK, the banking groups HSBC, Lloyds, Barclays and NatWest, the defence specialists Rolls-Royce and BAE Systems, as well as the oil explorers Shell and BP, outright.

It’s also the total amount of cash that was paid out in dividends by the largest 1,600 companies around the world last year, according to the asset manager Capital Group. It’s an annual record, 7% higher than the total paid to shareholders in 2024. More on this later.

Dividends are one of the most powerful components of an investor’s total return. Reinvesting your dividends helps to compound your wealth – the more dividends you reinvest, the larger the stakes you have in a certain investment, for little extra cost.

Alternatively, you could take your dividends as cash, allowing you to draw down a natural income stream in retirement while keeping your capital base largely intact and, hopefully, growing. You could, of course, do a combination of the two – take the income from some investments and reinvest others.

Either of the previous two options provide SIPP investors with attractive investment opportunities as well as flexibility on how and when they take their retirement income, in our view.

Investment trusts can play a key role in the building of said portfolio: the Association of Investment Companies’ (AIC) list of dividend heroes, trusts that have grown their dividends for 20 or more consecutive years, gets bigger every year, while the AIC’s universe encompasses a wider range of sectors than others, boosting one’s ability to diversify successfully – a key aspect of planning that is often overlooked, we think.

A new approach to retirement

For much of their history, pensions followed a simple formula: build the largest pot you can, take the 25% tax-free lump sum at retirement and convert the rest into an annuity, providing an income for life. Growth stopped when the annuity began and portfolios gradually de-risked from equities into bonds as retirement approached.

The Pension Schemes Act of 2015 fundamentally changed that model, introducing pension freedoms. You can still buy an annuity but now have the option to keep your pension invested and draw income flexibly. With retirement potentially lasting 25 years or more, it’s become less about a point of conversion and more a new phase of investment management.

This shift has driven a six-fold increase in the number of self-invested personal pensions (SIPPs) over the last decade. With the state pension age rising to 68, investors are turning to SIPPs to bridge the gap between stopping work and receiving the state pension, while retaining control over a portfolio that can keep compounding alongside income throughout retirement.

The cost of a cautious mindset

Despite greater flexibility, many investors still carry an annuity-era instinct into retirement, sharply reducing equity exposure in favour of cash or low-risk assets. This may feel prudent but can significantly undermine long-term outcomes.

For someone retiring at 60 with a 25- to 30-year horizon, insufficient growth over the long-term is arguably a greater risk than short-term market volatility. A high allocation to cash may smooth stock market fluctuations, but savings rates have not kept pace with inflation over the past decade. Over three decades, this erosion in spending power can have a material impact on lifestyle.

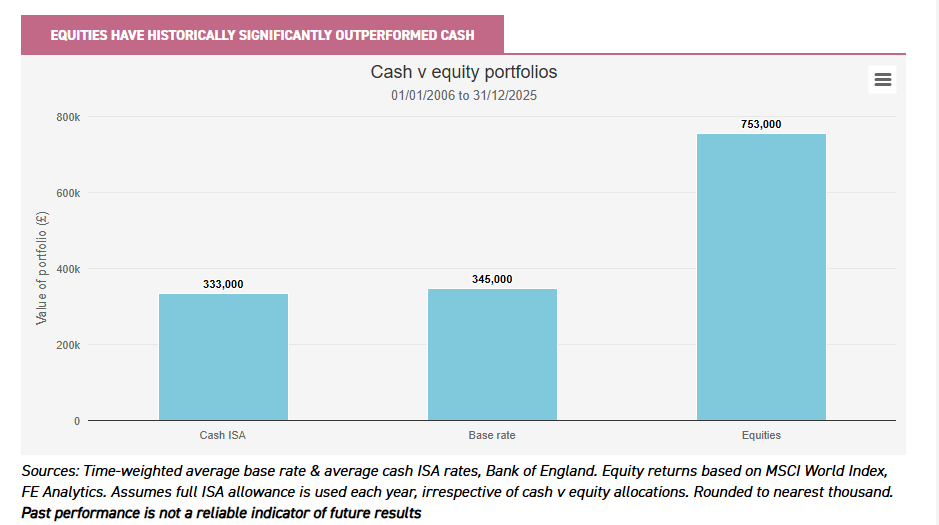

The chart below illustrates this trade-off: maximising ISA allowances each year over the past two decades would have produced a pot worth just under £350,000 in cash. The same contributions invested in global equities would have grown to over £750,000 – in other words, more than double the amount.

Equities have historically significantly outperformed cash

Sources: Time-weighted average base rate & average cash ISA rates, Bank of England. Equity returns based on MSCI World Index, FE Analytics. Assumes full ISA allowance is used each year, irrespective of cash v equity allocations. Rounded to nearest thousand.

Past performance is not a reliable indicator of future results

For SIPP investors in drawdown, this points to an alternative way of viewing risk. A temporary fall in portfolio value is uncomfortable but recoverable for long-term investors. However, a ‘safe’ portfolio that grows too slowly can leave investors unable to sustain the income they need or force them to delay retirement to make up the shortfall.

The natural income approach

Drawdown provides valuable flexibility but funding retirement primarily through asset sales can be problematic. Markets are naturally cyclical and selling investments during a downturn crystallises losses, as well as permanently reducing the capital base available to support future income and growth. This can be particularly damaging during the early stages of retirement when the portfolio has less time to recover.

The natural income approach offers a practical alternative: rather than selling assets to generate a quasi-income stream, the dividends, interest and distributions from investments provide the income element while the capital base remains invested, without needing to resort to forced sales when markets dip.

If an investor is keen to take income out of capital, one can find investment trusts to do this for them while still taking their own income naturally. The likes of Schroder Japan (SJG) provides an income out of capital, while Schroder Income Growth (SCF) and Schroder Real Estate (SREI) use revenue reserves to top up their dividends.

Finding the right balance

Natural income is not a single strategy but a spectrum that can be tailored to your appetite for risk.

At the more conservative end, UK equity income funds offer relatively stable dividends from blue-chip companies, providing a dependable income stream with lower volatility. Further along the risk curve, sectors such as Asian equities and healthcare can combine meaningful income with stronger growth potential, as we explore later in this report.

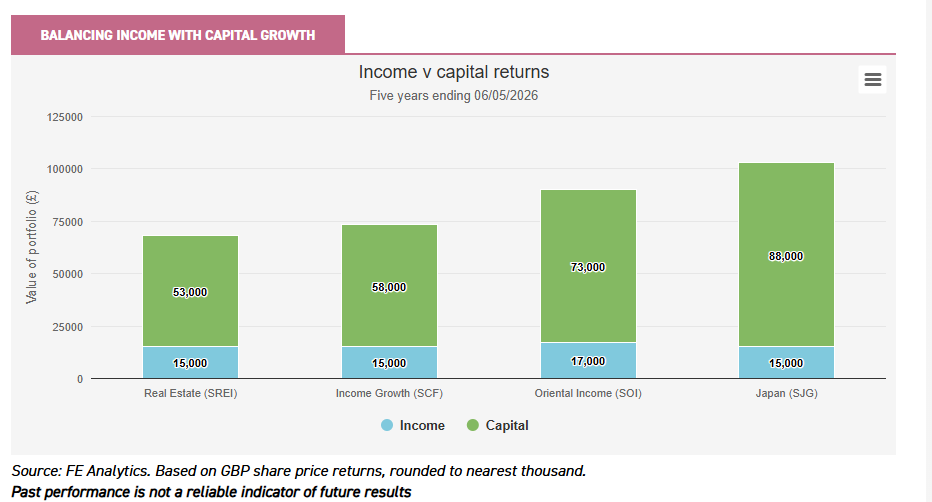

The chart below illustrates how a portfolio can generate both significant capital growth, alongside income. Investing £50,000 in Schroder Japan five years ago would have generated £15,000 in income alongside capital growth of £38,000. Similarly, investors would have received £17,000 in income from Schroder Oriental Income (SOI), as well as a further £23,000 in capital growth.

Balancing income with capital growth

Source: FE Analytics. Based on GBP share price returns, rounded to nearest thousand.

Past performance is not a reliable indicator of future results

Investment trusts are particularly well suited to a natural income approach across this spectrum. Unlike OEICs, they can retain a portion of income in stronger years and draw on these reserves to support dividends in weaker ones. This smooths payments across market cycles, rather than passing on income volatility to investors.

Their track record speaks for itself. There are now 20 dividend heroes, half of which have sustained increases for more than half a century – weathering recessions, market crashes and geopolitical challenges along the way.

The objective is to build a balanced portfolio that combines flexibility of drawdown with assets capable of a generating sustainable, growing income while preserving capital for the long term.

Spread your risk

That diversification has been described as the only free lunch in investing has become a rather well-worn cliché, but there’s a reason for that: it’s true, and it arguably only becomes truer the shorter your investment time horizon, and the more income-focused your requirements become.

In your 30s and 40s, it makes sense for many to be invested only in equities, with the point of diversification here being to spread your risk around, by investing in companies listed all around the world. Don’t just bet all on red (the US); have a little on black (the rest of the world, including emerging markets), too.

As we’ve already said, reducing volatility too significantly in the early stages of your retirement in favour of bonds or cash can have the opposite effect from which you’d intended and see you fail to keep up with inflation, thus reducing your future purchasing power significantly.

Equities should always, in our view, make up the bulk of an investor’s portfolio, no matter what their age and objectives. However, there are alternatives available for those looking to take all or some of their income naturally.

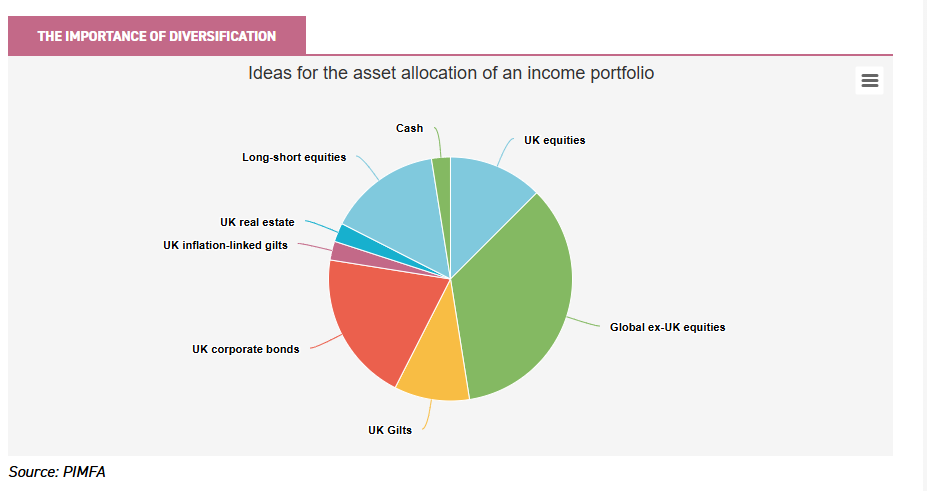

Below, you can see the suggested asset allocation of the income-focused Morningstar PIMFA Private Investor Index, which aims to represent the investment aims of wealth managers.

The importance of diversification

Source: PIMFA

We’d suggest a much reduced (or even no) exposure to long-short equities in favour of a higher allocation to real estate and, perhaps, an additional investment into infrastructure and/or renewable energy infrastructure.

Before we get into the nitty gritty, the first thing to note is that US exceptionalism, while being questioned by some, remains a strong theme. An allocation here for a portion of your retirement portfolio is prudent.

However, the headline yield on the S&P 500 is a lowly c. 1.2%, suggesting it’s not a deep, dividend-oriented market. Indeed, the FTSE All-World High Dividend Yield Index has 38.6% of its assets invested in the US. That’s a significant allocation, but a c. 35% underweight to the US’s c. 60% weighting in the FTSE All-World Index.

The solid base

You don’t have to look far to find the gold standard for dividend investing: our domestic stock market has the biggest yield of all major regions and countries. The large-cap FTSE 100 yields c. 3.1% and its mid-cap counterpart the FTSE 250 yields c. 3.7%, according to FTSE Russell. This makes the UK’s dividend yield higher than all the other major markets around the world.Source: FTSE Russell

Clearly, the UK has long had a strong dividend culture, but it should be noted that not all dividends in the UK stock market have been created equal. UK dividend growth has lagged most other regions, according to Capital Group. Core UK dividends, which adjusts for factors like one-off special dividends and exchange rates, grew just 1.9% year-on-year.

That said, the median growth rate was 7%, showing a big difference between the haves and the have nots, as it were. To us, this shows the pitfalls of investing in a passive UK equity income fund that discriminates between neither the fundamental quality of a company’s dividends nor whether a stock is overpriced or underpriced, which active management does. Hence, our view is that one needs to take an active view.

One trend we’ve observed over the past couple of years is the increasing prevalence of UK companies diverting some cash that in times gone by would have gone towards paying a dividend towards buying back their own shares. Again, active strategies can put themselves in the best possible place to take advantage of this.

To put this in some context, using SCF as an example, during the trust’s most recent financial year, 31 of its 47 portfolio holdings, 67% by portfolio value, conducted buybacks, up from 60% in 2024 and 38% in 2023.

This may perturb those fully focused on dividend income, but we think it’s a positive trend – as does Sue Noffke, manager of SCF. The fact that SCF is benefitting from share buybacks shows that Sue’s process of finding businesses with healthy cash flows and solid balance sheets is working well. It also gives us confidence in the capital allocation decisions being made by the boards of UK plc. That said, we wouldn’t be surprised if buyback activity slowed and we saw more companies reinvesting for growth, which would also be a welcome development.

SCF is one of the dividend heroes we mentioned earlier, having grown its dividend every year since its first full financial year in 1996, making this its 30th year of increases.

The dividend has grown 4.1% on an annualised basis, versus annualised inflation of 2.5%, from launch to 31/08/2025, equating to real annual growth of 1.6%, helping to grow shareholders’ purchasing power.

This, in our view, shows the power of retaining a good slug of cash in equities, even when many would suggest dialling back significantly. The achievement is even more impressive when set against the fact that in those 30 years, we’ve seen the global financial crisis and the Covid-19 pandemic, when dividends fell sharply.

The up-and-comer

There’s no doubt that the pretender to the dividend crown is Japan. The MSCI Japan and TOPIX indices’ dividend yield of c. 2% may seem rather measly, especially when compared with the UK. However, the headline level yield hides a plethora of nuances.

In core terms, Japanese dividends grew by an impressive 12.5% in 2025 – the best among the major markets by a long way. One key driver of Japan’s income story is the accelerating corporate governance reforms.

Newly elected Prime Minister Sanae Takaichi continues to put pressure on companies to deploy excess cash reserves and to use capital more efficiently. This has led to both record dividends and share buybacks, transforming Japan’s income culture.

There’s plenty of room for this to grow even further in the coming years, particularly as just under 60% of TOPIX companies are sitting on net cash, versus around 20% for the S&P 500 and STOXX 600. In addition, while payout ratios are rising, they also remain below US and European levels.

There’s no doubt that active management can offer considerably more above and beyond Japan’s headline yield. SJG has adopted an enhanced dividend policy, which pays out 4% of average NAV each year, placing it at the top of the AIC Japan sector with a current yield of 3.6% against a sector average of 1.7%.

Japan’s not just about the income story, though – there’s growth aplenty, too. Indeed, the TOPIX delivered twice the GBP return of the S&P 500 in 2025.

It’s eminently possible that this will continue. Artificial intelligence is emerging as a compelling tailwind in the Japanese market, as investors start to broaden their exposure to the theme from semiconductors to the physical infrastructure of an AI-enabled economy. Japanese industrial and robotics expertise is becoming a strategically important part of this supply chain.

This all translates into forecasts for double-digit earnings growth for the MSCI Japan Index in both 2026 and 2027. Despite all this, Japan’s major bourse still trades at a significant discount to its American counterpart.

There may be a clear push to making Japanese companies more shareholder friendly, but it remains a market that is hard to navigate, given the near-4,000 companies listed. There’s also a real dearth of research coverage for much of the small and mid-cap part of the market, which appeals as both attractively valued relative to large-caps as well as exhibiting stronger earnings growth prospects and reduced exposure to tariff risk given its more domestic orientation.

Around half of SJG’s portfolio is invested in small- and mid-cap companies, providing a meaningfully different exposure to Japan’s growth story than a passive solution while still participating in the income dynamics.

The underappreciated for income region

Across the sea and looking towards mainland Asia, we find a rather under-the-radar region when it comes to dividend investing. Asia has been prized for its growth prospects – and for good reason: the continent boasts thriving economies, a burgeoning consumer class and a new generation of global market leaders, particularly within technology.

At the same time, though, Asia has long had a strong dividend culture that is becoming even more ingrained. Pacific ex-China, Hong Kong and Japan saw core dividend growth of 6.8% in 2025, according to Capital Group, with Taiwan a real driver. China and Hong Kong’s core growth was 3.1%, meanwhile. Yields are now challenging even the most established income markets.

Further, earnings growth across the region is forecast by Goldman Sachs to accelerate from around 10% in 2025 to 30% in 2026, while around 40% of Asia (ex-Japan) companies are net cash positive, with payout ratios well below the US and Europe.

This all suggests the region is set for further dividend growth, especially as ongoing corporate governance reforms encourage cash to be returned to shareholders, as well as providing scope for capital gains, making it very much a total return story.

Schroder Oriental Income offers the best of both worlds in this regard. The trust has topped the AIC Asia Pacific Equity Income sector over the past five years. SOI has also grown its dividend for 19 consecutive years, putting it on track to become the first Asian fund to become a dividend hero.

Manager Richard Sennitt brings over 30 years of experience, supported by an extensive team of more than 40 analysts across six regional offices, providing the ability to dig deep into what is a large and fertile universe of companies.

Richard’s bottom-up approach seeks both a clear income rationale and the potential for capital gains, rather than filling the portfolio with the highest-yielding stocks. He focuses on quality businesses with strong balance sheets, solid earnings growth and sustainable dividend prospects. This better places SOI to capture capital growth than peers, since its income is fully derived from the underlying portfolio.

Richard also applies a top-down country and sector overlay, aimed at capitalising on a region that often sees a clear dispersion of both yields and returns at the country level. Take Korea and Indonesia as an example of this. MSCI Korea delivered a total return of 86% last year, leaving it offering a headline yield of 0.9%. MSCI Indonesia, meanwhile, offers a high 4.8% yield, but saw a meaningful decline last year.

Asia is a notoriously volatile region, a characteristic that many would suggest isn’t a great ingredient for an income-focused portfolio. Indeed, high headline yields offered on Asian funds and trusts could end up being unsustainable and come at the cost of capital growth.

SOI’s focus on companies paying sustainable, growing dividends makes it a steadier and more reliable income trust that grows sustainably over the long term, in our view. Its dividend yield of c. 3.2%, is on par with the UK with much better prospects for earnings and capital growth, too. You wouldn’t want to miss out.

The diversifier

Equities aren’t the only place one can consider for a well-balanced, diversified, income-generating portfolio. Bonds are clearly much more attractive than they were, say, five years ago, so they now warrant a place in a portfolio. That said, 2022 did highlight some growing concerns when it comes to their safe-haven status.

Bonds perform poorly when inflation rises for a sustained period of time because of their correlation with interest rates, which tend to rise to combat rising prices. The huge debt burdens Western nations have placed upon themselves pose potential challenges for government bond markets down the line.

Real assets can take up some of the slack. The likes of infrastructure and property tend to have inflation-linked revenue streams that can both increase the real value of your dividends as well as cushion any falls in prices if inflation ramps up once more.

From a headline perspective, the dividend yields available on UK commercial real estate investment trusts are attractive versus government bonds. Schroder Real Estate (SREI), for example, currently yields c. 7.3% versus c. 4.9% for the 10-year gilt and c. 4.4% for the two-year gilt, a premium of c. 240 and 290 basis points respectively.

The asset class has some interesting dynamics at play that underpin that income generation – as well as providing the basis for growth of capital at the same time.

On the income front, rents have been remarkably resilient in recent years. Between June 2022 and around September 2024, the MSCI UK Monthly Property Index fell c. 25%, yet the UK All Industrial rental growth index, for instance, rose c. 25%.

The supply-demand picture looks supportive, too. There is a lack of good-quality commercial property around, meaning current operators can charge higher rents and the pipeline of new developments remains thin because construction costs are rising, making it more expensive to build new properties.

On the capital growth side of things, we see scope for a recovery, especially when one considers that businesses are demanding higher sustainability specifications on their properties, crimping demand for ‘brown’ buildings.

SREI is a market leader in this respect. Its brown-to-green investment strategy sees it focus its asset management on improving the energy credentials of its portfolio of assets, allowing it to harness the growing evidence we’re seeing of a green premium: the higher rents and stronger valuations commanded by more energy efficient properties.

We’ve witnessed a slight recovery in real estate asset valuations since their most recent nadir, a fact underlined by SREI’s success in disposing of assets above book value, in the main.

Add in SREI’s 8.3% reversionary yield, a proxy for its underlying yield potential, and a sensible dividend policy and SREI looks attractive for a portion of an income seeker’s portfolio.

Breaking free of the annuity shackles

The dawn of pension freedoms ushered in a brave new world where taking an annuity after withdrawing your tax-free lump sum was no longer seen as the default option. It’s opened up a world of opportunity for savvy investors, but has also meant that proper SIPP planning is now more important than ever.

Indeed, there are, as they say, many ways to skin a cat – and just as many ways to access your hard-earned pension savings in retirement.

The 4% rule, where one leaves their capital invested and draws down 4% of the portfolio’s value each year, adjusted for inflation, has become a real no-brainer, helped no doubt by more than a decade of seemingly abnormally good returns from equity and bond markets.

We think that moving forward, one should adjust their expectations of equity returns, with most stock markets currently trading at record highs, the US at extended valuations and the rest of the world, while relatively attractively valued versus America, at perhaps fair value to their own histories.

That’s no reason to shun equities, even in retirement, but does put more importance on seeking investments that can help you to draw a natural income that grows with inflation. This includes diversifying across stock markets across the big, wide world as well as leaning into income-generating real assets such as commercial real estate.

Leave a Reply