Investor Edition

Fund Profile

Invesco Bond Income Plus (BIPS)26 May 2026

Disclaimer

Disclosure – Non-Independent Marketing Communication

This is a non-independent marketing communication commissioned by Invesco Bond Income Plus (BIPS). The report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on the dealing ahead of the dissemination of investment research.

BIPS continues to issue new shares for its high-yielding portfolio.

Overview

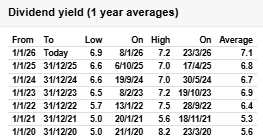

Invesco Bond Income Plus (BIPS) is managed by Rhys Davies who aims to deliver a significant yield pick up over gilts and cash without taking imprudent risks. Rhys invests in the high yield bond space, and will delve into subordinated bank debt and other corners of the market, but always with a keen eye on valuation to ensure he isn’t taking excessive credit risk to deliver the income. BIPS yields 7.1% at the time of writing, and has raised its dividend for five consecutive years despite the manager being cautiously positioned for most of this period .

Rhys continues to view the market overall as quite expensive, leading to the continued defensive positioning. He has a relatively high proportion of the fund in investment-grade debt rather than high yield, and has let Gearing fall to slightly below the usual 10-15% range. Nonetheless, the dividend target for 2026 has been held at the same level as last year. The trust has healthy revenue reserves, and Rhys is confident of hitting this target from current year income anyway, despite his defensive positioning.

BIPS has continued to see strong demand for its shares, even during the volatility surrounding the outbreak of war in the Gulf. It has traded on a premium for most of the past three years, and issued large amounts of new shares, including a placing and retail offer in February. At the time of writing, the premium was 1.8%. BIPS is the largest trust in the AIC Debt – Loans & Bonds sector, and this helps it offer the lowest charges by some distance.

Analyst’s View

We think BIPS should have strong appeal for the typical investor looking for an income. The yield is significantly higher than that on offer from gilts or cash, but the prudent approach to risk should limit the volatility in the value of the portfolio and help preserve the real value of the capital. The trust has held or raised its dividend each year for over a decade, and with healthy revenue reserves is in a strong position to continue this record. When we do eventually see a sell-off in credit markets, which tends to occur when equity markets sell off too, Rhys will be in a strong position to recycle some lower-risk positions into higher-yielding credits and boost the income once more. BIPS’ size brings low charges and liquidity in the shares, which helps make it an easy option for investors seeking a higher yield.

In the short term, the war in the Gulf has led to the market expecting modest rate hikes in the UK over the coming months. This would hit bonds’ capital value, but on the other hand would mean higher yields should be available in the market. BIPS is positioned to take advantage if this happens, with a defensively positioned portfolio which should limit the hit to the NAV and allow Rhys to add to higher yielding investments. We would add that one of its strengths is the geographical diversification into Europe and the US which means it is not overly sensitive to UK policy or indeed the health of the UK economy. With the UK looking exposed to energy prices and enjoying some Italian-style politics, although sadly not the weather or the ice cream, this is another defensive feature we find attractive at this point in time.

Bull

- Experienced and well-resourced team with international presence

- Risk-conscious approach could provide stability through tougher markets

- Attractive yield on offer with high average credit rating

Bear

- Gearing also magnifies losses in falling markets as well as gains in rising markets

- Income would come under pressure with any sustained fall in market yields (as it would for peers)

- Duration would lead to losses if rates were hiked

Leave a Reply