A High Court freezing order covers founders Stephen and Stuart Pratt and two associates

The brothers behind a suspected motorway service station Ponzi scheme have been hit by a multi-million-pound asset-freezing order.

Administrators for Godwin Capital, which collapsed in June last year, successfully obtained a £155m High Court freezing order against the directors and associated companies. The order covers the business’s founders, brothers Stephen Pratt and Stuart Pratt, and two other associates.

Administrators of MHA cited mismanagement, fraudulent trading and breach of fiduciary duty when obtaining the order, according to a letter seen by The Telegraph.

Godwin Capital’s collapse last year left thousands of Britons out of pocket. The company had raised hundreds of millions of pounds from thousands of small-time investors who provided loans of between £5,000 and £50,000 each and were promised returns of 10pc or higher.

Investors were told their money would be used to build residential and commercial properties, including motorway service stations, and that their loans would be secured against the properties.

Some of the projects were built, such as the Ram Jam Service station on the A1.

However, after Godwin collapsed, administrators allegedly discovered that loans were not secured against properties and funds had instead been used to repay other investors in an apparent Ponzi scheme.

Overall, it is believed that around 2,500 investors could have lost as much as £150m.

Martin Richardson, senior partner at Richardson Hartley Law, which is representing some of the investors who lost money in the scheme, said: “Investors’ money was clearly not spent in a way for which they intended when they sent the money.

“We have scores of clients whose lives have been ruined by this incredibly sophisticated scheme that took tens of millions of pounds with little or no returns.”

Barry Coffey, a partner at law firm Mishcon de Reya who specialises in fraud investigation and recovery, told Bisnow, a commercial real estate newspaper: “If there was money coming in which has been used to pay off prior investors, that would appear to be a Ponzi scheme.”

‘They seemed very professional’

Hilary Randall, a 72-year-old retired lab technician, lost £20,000 investing in Godwin Capital – almost all of her entire life savings – after being introduced to the scheme by a friend.

She was promised annual returns of up to 12pc and was repeatedly asked to invest more money in the scheme. After she asked to withdraw her funds, she was told to wait another 12 months, during which time the company collapsed.

Ms Randall is now entirely reliant on her pension to support her.

“I was contemplating having to sell the house to get some money taken out for me to live off,” she said. “I want to go on holiday; that’s what this money was supposed to be for after I retired, and I was going to get the money out, ironically, and then obviously it all went kaput.”

Stephen Jones, a 62-year-old self-employed landscape gardener, invested £90,000 with Godwin Capital – his savings and also his pension. He received no further communications from the company after investing and has been unable to contact anyone since.

“I’d gone to the office in Birmingham, and they’d cleared the stuff out two or three weeks before they went into administration,” Mr Jones said.

“They sent a proper professional leaflet with all the directors explaining the debenture. Yeah. And they told you about the directors, people with a lot of experience, a lot of years of investment.

“These men would have nice houses. They’d have had a good salary out of it. They seemed very professional. So why do what they’ve done?”

Lawyers for the directors were contacted for comment.

In 2003, the Pratt brothers began converting a former office building in central Nottingham, owned by their father, into luxury homes. The project was planned and administered from their parents’ dining room, giving rise to the company name Godwin Developments, after the 19th-century architect who designed their family home.

It wasn’t until 2018 that they launched the company’s associated finance division, Godwin Capital, and started raising money from retail investors in earnest.

It’s difficult enough buying companies quoted on a stock market, it’s a potential can of worms if you venture outside of the market.

Chart includes income but re-invested back into your Snowball or used to pay the grocery bill. The SNOWBALL previously held SDIP and sold for a profit of £1,563, using good ole hindsight it could have been bought back after the April dip, of course subject to funds being available.

With the Gulf of Hormuz opening to shipping, unless it doesn’t, I’ve decided to invest the money invested at XSTR into monthly paying ETF’s.

The SNOWBALL is overweight with Renewables for their higher yield but as time ticks by there is likely to be consolidation in the sector and any cash will need to be re-invested. There will only be a modest amount invested in each ETF to monitor the reaction between income and capital loss/growth.

A blended variable yield of 9.5%, which give the SNOWBALL another £770 in income versus the holding in XSTR

The miracle-growth of compound interest – or how to make £100,000 without really trying

13 February 2020 | by Dominique Riedl

£100,000 may seem like an unreachable goal when you first put money aside but the incredible force of compound interest can transform regular, small payments into large, life-changing sums.

Albert Einstein reputedly called compound interest the Eighth Wonder of the World. Warren Buffett calls it the most important factor in successful investing. Better still, every single investor can profit from “man’s greatest invention” (Albert Einstein), not just geniuses or billionaires.

The compound interest effect refers to the snowball of money that grows on your behalf when you reinvest your interest.

The compound interest effect: Interest on interest

An interest (or dividend) payment you put to work in the market today will generate more interest for you tomorrow. That’s because your interest also earns interest. And the longer you give your interest to pile up, the mightier your snowball becomes. Let’s look at a practical example to illustrate the compound interest effect…

If you invest £10,000 at a 5% rate of return then you will earn £16,288.95 over ten years, not just £15,000.

The compound interest effect creates an extra £1,288.95 that you would not have earned if you had just spent the interest every year.

The effect becomes more powerful over time.

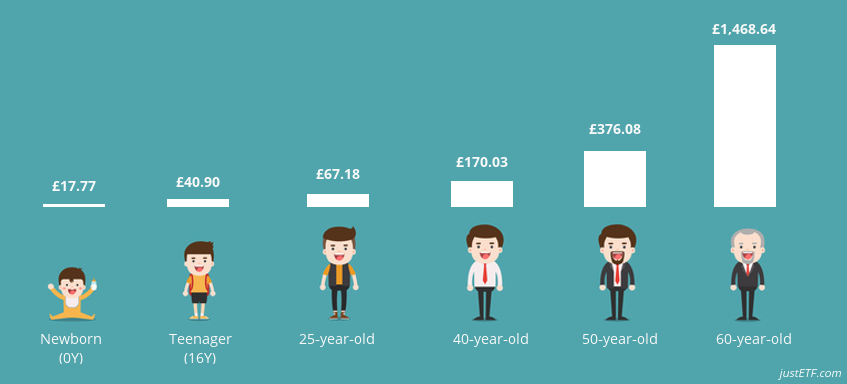

Imagine that an investor – we’ll call him David – wants to save up a nest egg of £100,000 by the time he retires at age 65.

The chart below shows how much David needs to put away to reach his goal depending on how soon he starts saving. (We assume an annual growth rate of 5%, which is quite conservative by the standards of the last 40 years.)

Monthly savings required to reach £100,000 by age 65

The key takeaway is that the longer compound interest gets to work its magic, the less David needs to pay in himself.

If David does nothing until age 60 then he needs to find a whopping £1,468.64 per month to hit his target. There is little time for compound interest to help his cause.

But if some kindly relative starts saving for David from the day he is born then only £17.77 needs to be found a month – a snip for David to save himself once he starts earning.

Even if David waits until age 25 then he need only put aside a modest £67.18 per month to reach £100,000 by 65.

The difference in required savings between each of the start dates is how much of the £100,000 is taken care of by your accumulating interest payments.

Even small contributions can snowball if compound interest is given enough time to generate its own momentum.

Let your money do the work

If you start early enough then compound interest payments will eventually surpass the amount of money that you pay in.

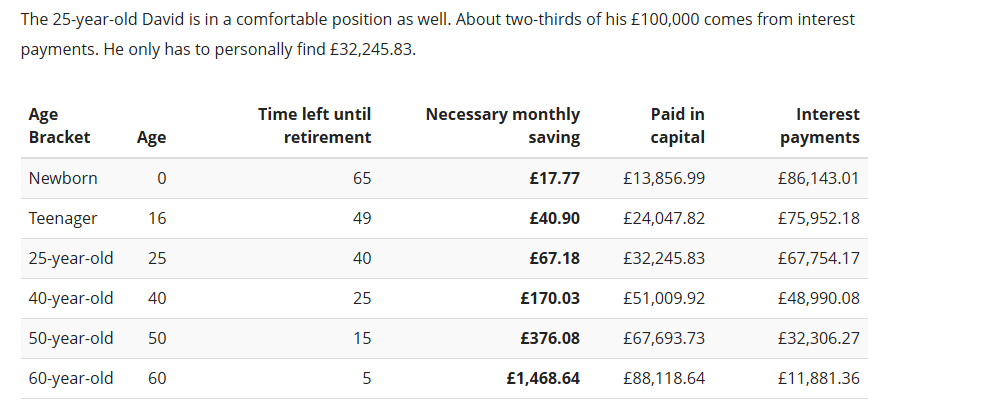

Returning to our David example, you can see below how much of his £100,000 target comes from compound interest (orange bar) versus paid in savings (white bar).

How time and interest work together

In this scenario, David’s interest payments are 6.2 times greater than his actual paid in savings! Compound interest does the vast majority of the work – bringing home £86,143.01 without David having to lift a finger.

The 25-year-old David is in a comfortable position as well. About two-thirds of his £100,000 comes from interest payments. He only has to personally find £32,245.83.

An early start benefits you in the long run

The earlier you can start saving, the more compound interest will do the heavy lifting for you.

It’s one of the most valuable yet underestimated factors in an investor’s long-term plan because its effect is relatively imperceptible at first. Compound interest is the financial equivalent of the old Chinese saying: The man who moves a mountain begins by carrying away small stones.

The greater your return on investment, the more powerful the compound interest effect becomes, which is why it’s best leveraged by reinvesting the profits you make in the stock market.

Category: Global high‑yield equities Yield: ~11% Role: Global diversification + high income Why monthly: UCITS “SuperDividend” share classes pay monthly

This prevents the portfolio from becoming too US‑centric.

4) Global Enhanced‑Income Equity (Monthly) – 20%

Category: Global equity income with option overlays Yield: ~5–6% Role: Smooths income when volatility drops Why monthly: UCITS enhanced‑income share classes pay monthly

Here are five of the highest‑yielding ETFs that are tradeable in the UK, based strictly on current yield data from UK‑accessible sources. These are all UCITS ETFs, meaning they can be bought via UK brokers and held in an ISA or SIPP.

Top 5 High‑Yielding ETFs (UK‑Tradeable)

Ranked by current dividend yield (GBP‑based where available)

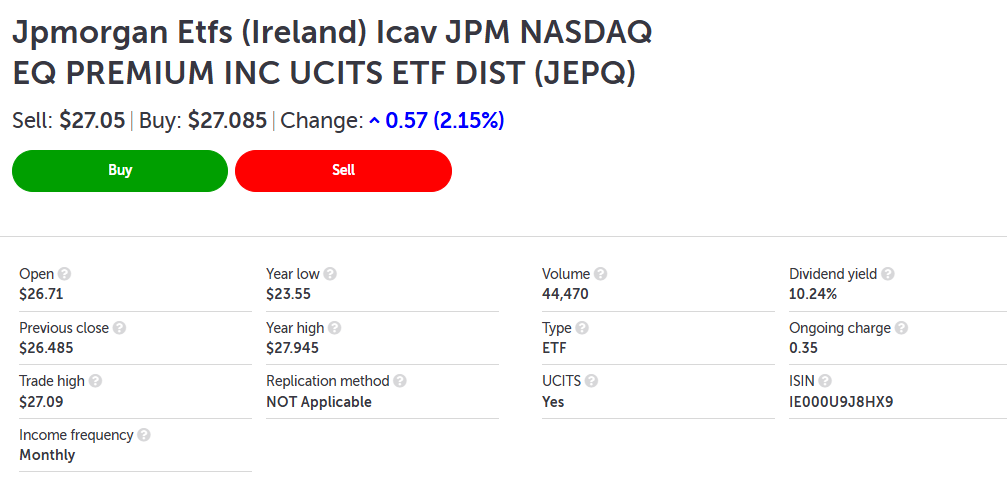

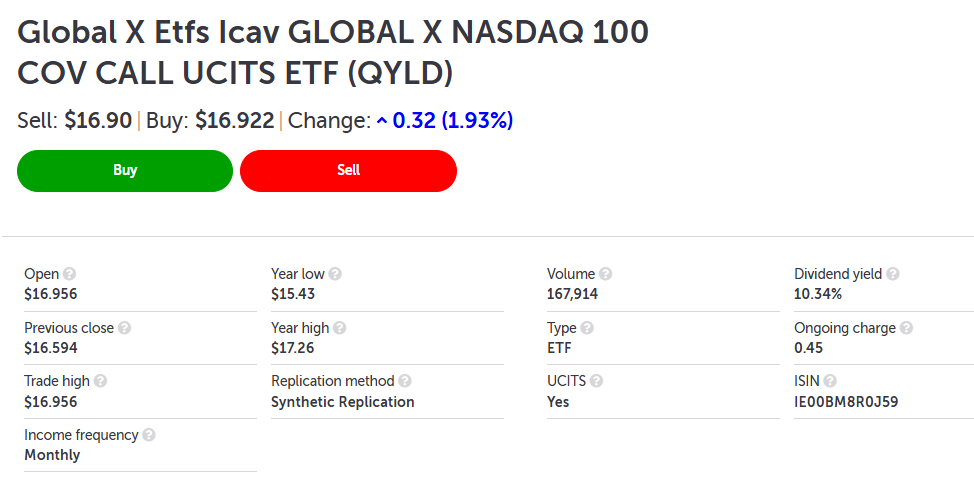

1. Global X Nasdaq 100 Covered Call UCITS ETF (QYLD‑style UCITS version)

Yield:12.11%

Type: Covered‑call equity income

Region: US (Nasdaq 100)

Notes: Very high yield due to option‑writing; lower growth potential.

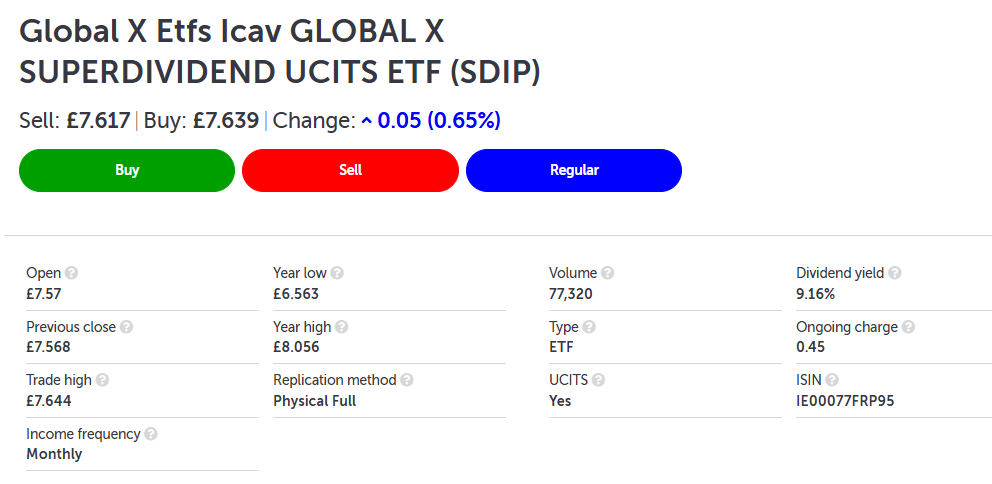

2. Global X SuperDividend UCITS ETF (SDIP)

Yield:11.11%

Type: Global high‑dividend equities

Region: Global

Notes: Screens for the highest‑yielding stocks globally; income‑maximising.

3. Global X S&P 500 Covered Call UCITS ETF

Yield:9.91%

Type: Covered‑call equity income

Region: US (S&P 500)

Notes: High income, reduced upside due to call‑writing.

Deep Discounts, High Yields: 4 BDCs Paying Up to 13%

Brett Owens, Chief Investment Strategist Updated: June 12, 2026

Stocks are sky-high, but us contrarians are looking for dividend deals. And we found them in one forgotten corner of the Wall Street world. Here, we’re going to bank yields between 11% and 13%.

That’s right—up to 13%, for as little as 68 cents on the dollar.

What does that mean? Well, these funds are trading at discounts as large as 32% off their book values.

Where are we looking? We’re talking about business development companies, or BDCs. These are publicly traded firms that lend to mostly privately held companies—small and medium-sized businesses.

The BDC business itself can be a bit of a cardiac kid. It’s all about getting paid back on these loans. The smart lenders can do very well over time. The sector is so potentially lucrative that it attracts some less-than-ideal managers—hence a bit of a shady reputation.

But in these shadows is where we can find value.

2026 has been rough sledding for BDCs. There have been fears about the creditworthiness of the loans they’ve extended. It’s come to fruition—about one in four companies in the non-penny-stock BDC world have cut their dividends over the past few months.

Ugly, ugly, ugly.

So why are we diving in this dumpster for dividends? Well, we’ve got three reasons to be intrigued.

BDCs tend to own floating-rate debt, which means their income rises as short-term rates move up. And inversely, it drops as rates drop. High oil prices have put Federal Reserve rate cuts on hold indefinitely, and this has helped stabilize BDC income.

Even after the dividend cuts we’ve seen, BDCs still remain one of the top sources of income for dividend investors. I mean, come on—where can we find yields like these?

Hey—these stocks are rarely this cheap. Industry valuations haven’t been this low since COVID. As contrarian investors, we are stepping in to sort through the wreckage.

So let’s talk about these dividend payers, dishing between 11.8% and 13% yields. We are looking for values here, not falling dividend knives, so these details matter.

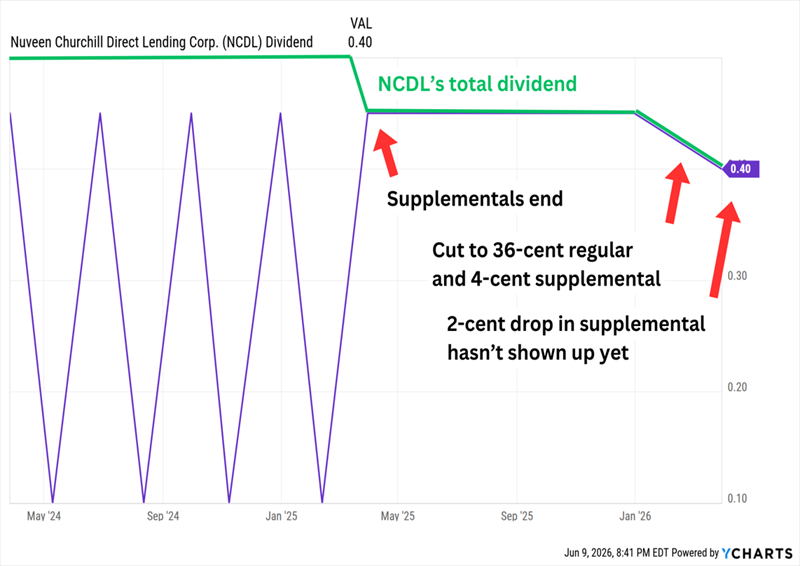

Nuveen Churchill Direct Lending Corp (NCDL) Dividend Yield: 11.8%

Investing in business development companies often means hitching our wagons to the market’s most prominent asset managers. Take, for instance, Nuveen Churchill Direct Lending Corp. (NCDL), which bears the name of both fund manager Nuveen (the asset manager for TIAA) and BDC manager Churchill, a Nuveen affiliate.

NCDL targets U.S. middle-market companies backed by private equity sponsors. It’s currently invested in 236 companies across 26 industries, with significant bents toward healthcare/pharmaceuticals and business services. It spreads out risk well, too—its top 10 holdings make up just 13% of the portfolio’s weight.

Nuveen’s BDC does most of its financing via first-lien debt, and the lion’s share of that is floating-rate in nature—helpful in that higher interest rates can boost loan income, though they can also drive down loan demand.

Nuveen Churchill Direct Lending has less than three years’ worth of trading under its belt, most of it just pinballing up and down. And because we’re in the midst of one of its sharp downturns, we can buy it for a cavernous 26% discount to its net asset value (NAV).

But what would we be buying?

A big dividend, sure—but one that’s been quietly shrinking since NCDL first hit the market. The 45-cent quarterly with a 10-cent supplemental on top? Gone. The supplemental dried up first. Then this year, the base got cut to 36 cents, with a 4-cent top-up thrown in as a consolation. Then that supplemental shrank to 2 cents in Q2.

Death by a Thousand Trims?

What makes the underperformance and dividend difficulties surprising is that NCDL at least appears to be a solid operator. Non-accruals grew in the most recent quarter, but at just 1.3% of the portfolio at cost, so credit quality is excellent. (Non-accruals are loans that are delinquent for a prolonged period, usually 90 days.) It has a favorable fee structure thanks to waivers. Management is conservative and steeped in private-credit experience. Software exposure is low.

Patient investors might eventually be rewarded. Until then, Nuveen’s BDC clearly isn’t treating the dividend with kid gloves.

Blackstone Secured Lending Fund (BXSL) Dividend Yield: 12.9%

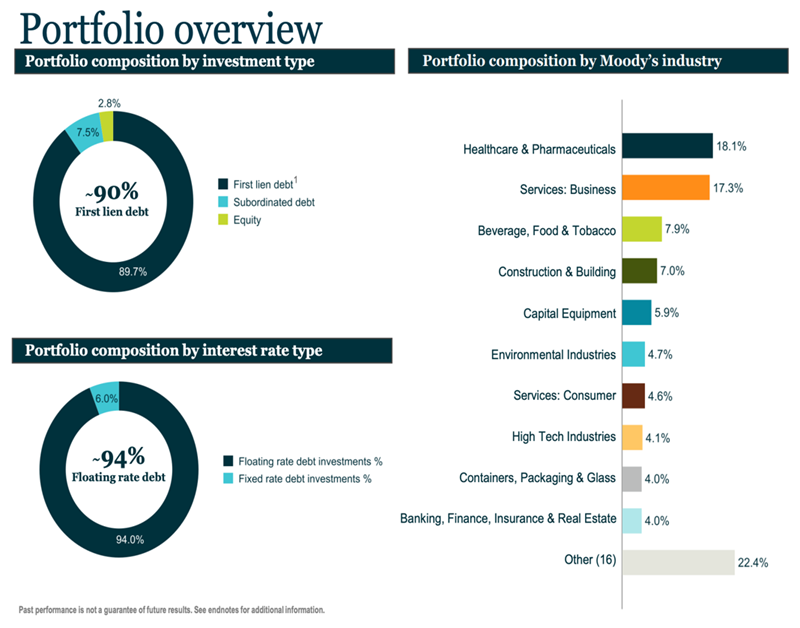

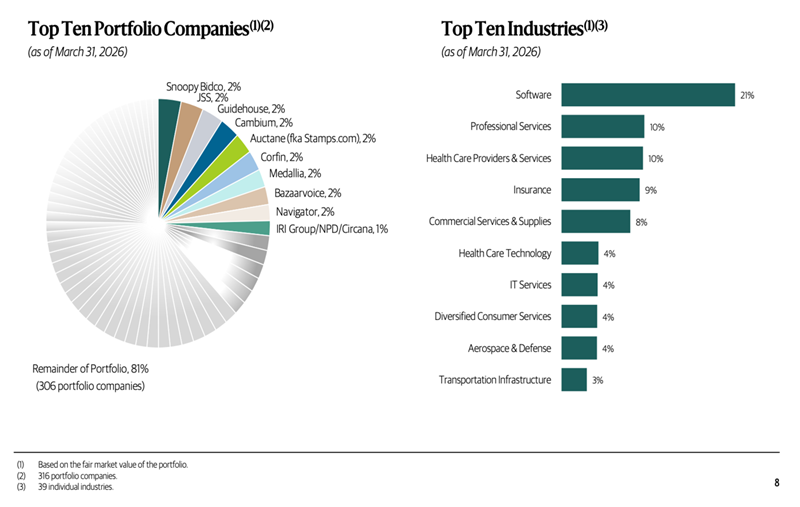

Blackstone Secured Lending Fund (BXSL) leans on the rich resources of Blackstone (BX) and its Blackstone Credit & Insurance arm. And that brings up another important aspect of many BDCs: They’re not just lenders and stakeholders. BXSL’s 316 portfolio companies also enjoy the expertise and operational support of one of the world’s largest alternative credit platforms—and Blackstone Credit & Insurance doesn’t claw fees away from the BDC for the privilege.

Blackstone’s BDC deals almost entirely in floating-rate first-lien debt. It likes larger companies in sectors with historically lower default rates. It’s plenty diversified, too, with its top holdings making up less than 20% of assets.

However, while the portfolio is spread across nearly 40 industries, that top industry is a red flag.

BXSL took a big step back in Q1. Non-accruals jumped to 4.7% at cost, while its net asset value declined by more than 2% quarter-over-quarter.

Every other BDC seems to be hacking its dividend. Blackstone Secured Lending Fund’s has held at 77 cents. But it might just be late to the wake: Net investment income (NII) covered the payout this quarter, yet full-year 2026 and 2027 estimates are sliding toward levels that can’t sustain it.

Shares have lost 20% of their value since July 2025, which has plumped up its static dividend to a yield of nearly 13%. But deterioration in net asset value has kept BXSL from falling into deep value territory—it currently trades at a decent 9% discount to NAV.

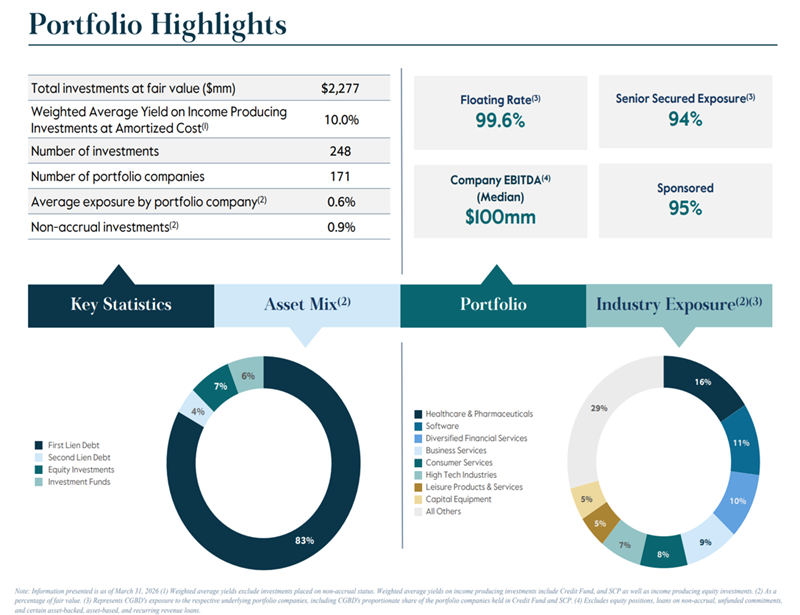

Carlyle Secured Lending (CGBD) is yet another double-digit-paying BDC tethered to a well-known asset manager: Carlyle Group (CG). It invests in middle-market companies sponsored by PE. And its preferred deal type is floating-rate first-lien debt.

But CGBD stands out for a much tighter portfolio of just 60 companies. And its financing is more spread out—first-lien debt makes up less than 85% of fair value; it also has mid-single-digit exposure to second-lien debt, equity investments and investment funds.

Around this time last year, I wrote that CGBD’s first half of 2025 was a “train wreck.” It had just put together back-to-back earnings disappointments, experienced rising non-accruals, and failed to issue a supplemental dividend for the first time in years.

Since then? Some ups, and some downs.

The distribution was pared down even more. After a couple quarters of keeping the dividend level, CGBD in April announced a 12.5% cut to 35 cents per share.

But the company has been putting together more promising results. While CGBD’s NAV declined by more than 2% during the first quarter, NII beat estimates, and non-accruals declined to just 1% of cost after portfolio company Alpine restructured its balance sheet. Carlyle Secured Lending also has a pair of joint ventures—Middle Market Credit Fund (MMCF) and Structured Credit Partners (SCP)—that are continuing to ramp.

When I looked at Carlyle Secured Lending in mid-2025, it had been greatly underperforming other BDCs for months. It has continued to decline since then, but its red ink has been more in line with the industry. Still, that has dragged CGBD’s price down to a 32% discount to NAV, putting this Carlyle vehicle in the cheapest third of traded BDCs.

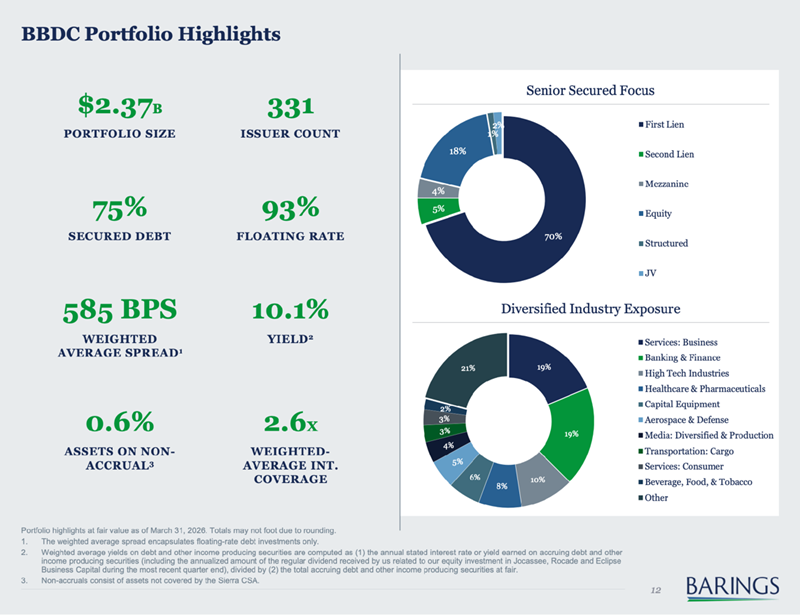

Barings BDC (BBDC) Dividend Yield: 12.3%

Barings BDC (BBDC) hasn’t always been tied up with manager Barings LLC. It was known as “Triangle Capital” for many years until August 2018, when the company rebranded, trying to put years of write-offs and dividend cuts in the rear-view mirror.

It wasn’t just a brand refresh, either. The new name reflected its new relationship with global financial services firm Barings, which became an external advisor and went to work cutting out the portfolio’s rot.

Today, Barings invests primarily in middle market companies owned by PE, though about 5%-15% of its investments are “non-sponsored” upper-middle-market and opportunistic middle-market deals, and another 5%-10% is exposure to Eclipse Business Capital and Rocade Capital—originators of middle market first-lien loans. BBDC has the lowest exposure to first-lien debt of the group, at just 70%. Roughly 20% of its deal mix is in equity, and the rest is scattered among second-lien and mezzanine debt, as well as other financing options.

We’ve already booked gains in Barings BDC twice through our Dividend Swing Trader service, so I constantly keep my eye on BBDC for short- and long-term opportunities alike.

Last year, I was encouraged by a string of small quarterly supplementals—the company hadn’t made “top-up” specials in a decade. They didn’t last, but the regular dividend has remained intact, powering a 12%-plus yield.

But that yield might have a clock on it. Earnings are pacing below the dividend, and the math only works as long as spillover earnings can bridge the gap.

One helpful development just popped up about a week ago. Barings BDC terminated a credit support agreement, which will result in a $67 million payout by the end of the month—money the company can use to fund additional investments.

And while BBDC has been a source of relative strength in 2026, down just a few percent versus double-digit declines for the BDC industry, it’s still dirt-cheap. This mega-payer currently trades at a 23% discount to NAV.

Avoid the Retirement ‘Death Spiral’: Collect 8% or More for Life

You’ve seen what these BDCs are paying. Now imagine a portfolio engineered to generate 8% or more—without the dividend cuts, the NAV erosion, or the Fed uncertainty hanging over private credit.

And you need that level of income, because traditional strategies just aren’t cutting it anymore.

Just look at people trying to get by with the “4% rule.” It works until it doesn’t.

Every few years, the market will dip and force you to sell more shares when prices are low—which means when shares rebound, you need an even bigger gain just to get back to your original value.

TR chart, where because of the modest yield you might have re-invested the dividends back into your higher yielding shares in your Snowball.

The holy grail of investing is where you take out your capital and re-invest in another high yielder and still receive income from you original purchase at a cost of zero, zilch nothing and a yield of

The current yield is 3.7%, so everything crossed for a market crash, if you want to buy.

Lots of patients needed as you see from the chart, it spends most of the time going sideways or falling because of the dividends being paid.

If you bought just before the xd date, the price has currently always moved higher than the price fall due to the dividend going xd.

Anyone buying nearer to the end of a bull market than the beginning is likely to lose money.

If you can get a decent entry price/yield the share could be pair traded and the ‘secure’ income re-invested into a higher yielder in your Snowball.

Investment trusts offer a huge range of investment possibilities, and are a great way for beginner investors to get their money working harder for them over the long term.

Anyone getting started in investing will likely be intrigued by the concept of investment trusts. There is, on the face of it, a lot to learn, from whether or not to worry about discounts to how different trusts use gearing.

But for beginner investors, investment trusts can be boiled down to fairly simple fundamentals. They are a form of active fund that trades on a stock exchange, just like a stock. In fact, they are stocks – each investment trust is a listed company in its own right.

“Investment trusts offer diversified portfolios and many have long records of preserving and growing the value of people’s savings,” says Nick Brotton, research director at the Association of Investment Companies (AIC), an industry body that represents nearly 300 investment trusts.

“Many trusts make great first-time investments whether you’re looking for income, growth or a mixture of the two,” he adds.

The AIC has collated the recommendations of various investment industry experts to build a list of the best investment trusts for beginner investors.

UK investment trusts for beginners

Beginner investors who want to use investment trusts to gain exposure to the UK market could consider one of these for their portfolio.

City of London Investment Trust

City of London (LON:CTY) is one of the AIC’s dividend heroes, meaning that it has increased its dividend payout every year for 20 consecutive years.

It is over 100 years old, and manager Job Curtis has run the fund for 34 years, favouring “good quality, well-managed companies, bought at reasonable share prices”, says Emma Wall, head of platform investments at Hargreaves Lansdown.

“A new investor may want to consider an investment trust with a long track record and a manager who has been at the helm through many economic cycles,” said Paul Chilver, director and financial planning manager at Birkett Long IFA. “The City of London Investment Trust ticks both these boxes.”

Chilver added that City of London’s focus on well-known FTSE 100 stocks would be reassuring to beginner investors.

Fidelity Special Values

For a broader play on the UK’s stock market beginner investors could consider Fidelity Special Values (LON:FSV).

“The UK stock market has performed very well this year, but it’s been led by the big blue chips of the FTSE 100,” said Laith Khalaf, head of investment analysis at AJ Bell. “If small and mid caps start to motor, this trust stands to benefit more than most broad UK stock market funds, including index trackers.”

Global investment trusts for beginners

Here are the experts’ picks for investment trusts with a global focus.

Scottish American Investment Company

Scottish American (LON:SAIN) is “a great one-stop-shop trust for those with an appetite for risk, investing predominantly in global equities but with a small allocation to bonds, property and infrastructure”, says Wall.

Its managers James Dow and Ross Mathison seek out companies with dependable income alongside the potential for inflation-beating profit growth.

“They also need to show resilience through the economic cycle,” said Wall, adding that the trust is a dividend hero having increased its dividends for more than 50 years.

F&C Investment Trust

Beginner investors that want a broad play on the global stock market could consider F&C (LON:FCIT).

“It provides access to a very broad and well managed portfolio, delivering steady long-term capital growth alongside an attractive dividend income,” says Philippa Maffioli, senior adviser at Richmond Investment Managers.

Murray International Trust

Maffioli also recommends Murray International Trust (LON:MYI) to beginner investors.

“The trust focuses on achieving long-term returns that outpace inflation, giving investors a strong foundation for the future,” she says.

Alliance Witan

With ten-year returns of 219%, Alliance Witan (LON:ALW) is the highest-performing investment trust over the last decade on this list.

It has an unusual approach to portfolio construction, whereby several external fund managers are asked to pick around 20 of their best stock ideas.

“The result is a portfolio of over 200 stocks, covering a wide range of countries and sectors,” says Kyle Caldwell, funds and investment education editor at Interactive Investor. “For investors prepared to take on a bit more risk, Alliance Witan offers a well-diversified portfolio of global shares.”

Brunner Investment Trust

Brunner Investment Trust (LON:BUT) is a growth-focused investment trust that offers “a modest but steady dividend”, says Maffioli.

“Under the experienced management of Julian Bishop and his team, Brunner has demonstrated resilience and consistency, making it a solid option for those taking their first steps into investing,” she adds.

Capital preservation investment trusts for beginners

Beginner investors might want to take a more cautious approach with their money, especially if venturing into the investing world from predominantly cash savings. These two trusts are solid choices for beginner investors that want to keep their money safe.

Personal Assets Trust

Three experts – Chilver, Khalaf and Wall – recommended Personal Assets Trust (LON:PNL) for beginner investors.

“It has a long track record in protecting investors’ money during periods of stock market volatility and currently has high exposure to government bonds and gold,” said Chilver.

Khalaf particularly likes the balance between these defensive assets with high-quality companies, and Wall highlights the focus of managers Charlotte Yonge and Sebastian Lyon on preserving investors’ capital.

“As well as a good first-time option, this trust can provide ballast to more established equity-biased portfolios,” Wall adds.

Capital Gearing Trust

Capital Gearing Trust (LON:CGT) makes a sound choice for cautious beginner investors because of its heavy weighting towards bonds.

“For those dipping their toes into the stock market for the first time, seeking out funds that provide plenty of diversification is a sensible start as it helps to keep a lid on risk,” said Caldwell. “Among the options is Capital Gearing, which has a third of its portfolio in risk assets (equities), a third in short-dated government bonds and corporate bonds, and a third in index-linked bonds.