The S&P 500 Is Flashing an Ominous Warning That’s Been Observed Only Once Before. Will History Repeat Itself?

Free Article Explore Premium Services

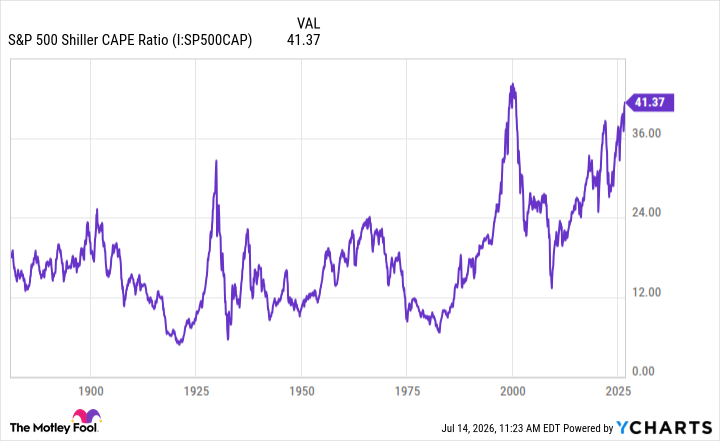

The S&P 500 Shiller CAPE ratio is on the verge of reaching its highest level in history.

By Adam Spatacco – Jul 17, 2026

Key Points

- The Shiller CAPE ratio measures valuation trends across the entire S&P 500 index.

- The CAPE ratio sustained a reading of more than 40 during the dot-com bubble.

- Today, the CAPE ratio hovers close to its peak levels seen between 1999 and 2000.

The S&P 500 has long served as a barometer of investor sentiment. Among the tools used to assess the index’s valuation, the cyclically adjusted price-to-earnings (CAPE) ratio stands out for its ability to sift through short-term noise and reveal whether stocks are priced reasonably relative to their long-term earnings history. Understanding this metric helps explain both market extremes and the steps smart investors can take when prices climb sharply.

What does the CAPE ratio measure?

The CAPE ratio divides the current level of the S&P 500 by the average of inflation-adjusted earnings over the past 10 years. This approach removes the fluctuations that can distort ordinary price-to-earnings (P/E) ratios, which can appear artificially low during periods of abnormally high profits or artificially high after a single down year.

Image source: Getty Images.

A conventional P/E might appear “expensive” simply because earnings per share (EPS) have collapsed in a recession, even if stock prices have not fully adjusted. The CAPE ratio, by contrast, reflects a smoother picture of sustainable profitability across different economic cycles.

When the CAPE ratio begins to climb, it usually signals that stock prices are increasing at a faster rate relative to underlying earnings. While this can stem from investor optimism about future growth, it can also reflect mounting speculation or easy credit conditions. Over the long term, higher CAPE readings have been followed by more modest stock returns because frothy markets leave less room for further multiple expansion and more room for eventual compression when reality sets in.

The current environment in the technology sector echoes the dot-com bubble

Historical annual averages show that the CAPE ratio reached or surpassed a level of 40 for consecutive years only once: in 1999 and 2000, when it reached 42.1 and 41.7. These readings occurred during the peak of dot-com euphoria.

S&P 500 Shiller CAPE Ratio data by YCharts

At that time, investors were pouring capital into internet start-ups and established technology companies alike, hoping that the emerging digital economy would generate limitless growth. As a result, many companies commanded stretched valuations despite minimal revenue traction and nonexistent profits. The broader market’s valuation expanded dramatically as enthusiasm outpaced concrete fundamentals.

As the chart above illustrates, the subsequent unwinding after the dot-com bubble was painful. Beginning in 2000, the realization that many internet businesses lacked a viable path to sustained earnings triggered prolonged selling pressure. Naturally, technology stocks led the decline, with the Nasdaq falling more than 75% from its peak and the S&P 500 entering a bear market that lasted into 2002.

This episode demonstrates how quickly sentiment can reverse once valuation detaches from reality. While the market eventually recovered, the scars of the extremes witnessed during the dot-com era remain etched in investor memories even today.

How should you invest in 2026?

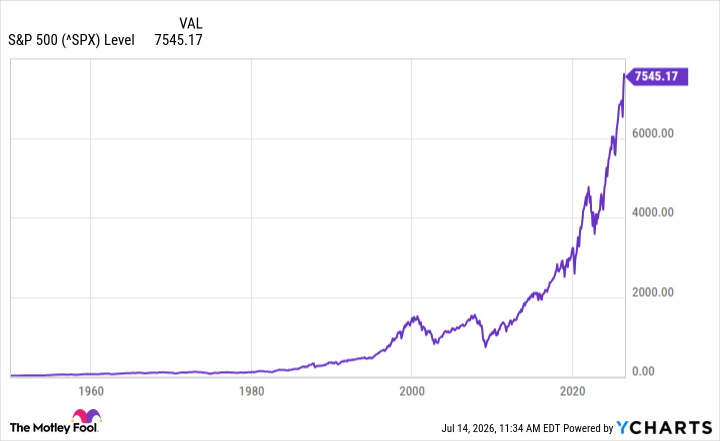

As the chart above shows, the current CAPE ratio is inching closer to its dot-com-era highs. This elevated level invites caution even if it has not yet matched the extremes seen more than two decades ago. A continued rise in the CAPE ratio could foreshadow a period of weaker total returns or a meaningful drawdown — though such outcomes are never certain.

Rather than attempting to time the market, smart investors can benefit from maintaining broad diversification across sectors and asset classes. Within stocks, keeping an emphasis on blue chip companies with diversified business models, strong balance sheets, and a proven ability to navigate economic cycles provides greater resilience than a concentrated bet on any single theme or growth narrative. Established businesses tend to generate more predictable cash flows and often return capital to shareholders through dividends, offering a degree of downside protection during volatility.

In addition, holding a meaningful cash allocation alongside stocks will further strengthen your portfolio. Cash serves as both a defensive buffer during volatility and as dry powder for purchasing quality businesses at more attractive prices should the opportunity arise.

Above all else, history shows that the S&P 500 has always absorbed economic shocks, corrected its excesses, and resumed an upward trajectory as the economy grows and companies innovate. Through diversification, a focus on durable business models, and prudent cash reserves, investors can participate in that resilience while reducing the impacts of valuation-driven turbulence.

Leave a Reply