Dividend re-investment in the real world and total returns

Theory is all well and good, but what about what happens in the real world?

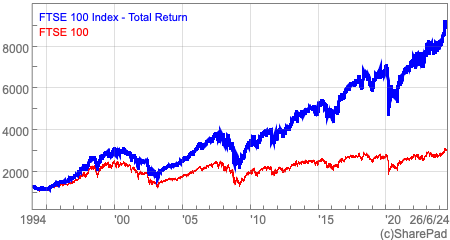

The chart below compares the value of the FTSE 100 (the lower or red line) with the value of the FTSE 100 Total Return index (the higher or blue line), which includes the effect of reinvested dividends since 1994.

You can now see that the total return index is worth a lot more than the FTSE 100 index.

This is important as it should make you look at investment results in a different way. Investing in shares is not just about the changes in share prices, it’s about the total returns which includes the dividends you receive.

However, the point I want to get across is that dividends matter and can make up a large chunk of the returns that you get from owning shares over the long run.

Dividend reinvestment with individual companies

Buy the right share at the right time and the right price and you can see spectacular results. Take British American Tobacco (LSE:BATS) for example.

Let’s say you bought 1,000 shares of this company on the first trading day of 2000 for 332.5p (an investment of £3325 excluding stamp duty and dealing costs) when it was paying an annual dividend of 22.2p (or a dividend yield of 6.7%). The shares were very cheap as many investors ignored them and put their money into glamorous internet shares.

Just over fifteen years later though in January 2015, BAT shares are priced at 3522p and are paying an annual dividend of 144.9p. Most people would be quite happy. The shares have soared as has the annual dividend per share.

Even if they had spent their annual dividend income, their investment would have increased in value more than ten-fold to £35,220. The dividend income as a percentage of the original price paid (144.9p/332.5p) – or the yield on cost – would be an impressive 43.6%.

But say you’d reinvested your dividend income every year and bought more shares with it. Your investment would have soared in value to £69,335 with an annual dividend income of £2753.64 – or a yield on cost of 82.9%.

An investment of 1,000 shares in BAT since January 2000

| Left alone | With dividends reinvested | |

|---|---|---|

| Value of shares | £35,220 | £69,335 |

| Income Received | £1,112.60 | N/A |

| Investment value Jan 2015 | £36,332.60 | £69,335 |

| Annual income Jan 2015 | £1,449 | £2,753.64 |

| Yield on cost | 43.60% | 82.90% |

Of course, hindsight is a wonderful thing but this example does highlight three very important rules of a successful dividend re-investment strategy:

- It helps to buy shares at a cheap price. Back in 2000, companies like BAT were out of favour as investors piled into glamorous internet and technology shares. With a dividend yield of 6.7%, the shares looked – and turned out to be – very cheap given that the business was not in trouble and had been increasing its dividend.

- The importance of dividend growth. Your returns can be turbo-charged if the company is capable of delivering high rates of dividend growth. BAT’s annual dividend growth over the last 15 years averaged 13.3%.

- The power of time. The longer you invest for, the greater the power of compounding on your investment returns.

The emotional benefits of dividend re-investment

This is a very powerful investing strategy, especially for shares with high dividend yields that are capable of growing their dividends year after year.

What’s particularly good about it is that you focus your attention on the performance of the company and its ability to keep paying a growing dividend rather than what’s happening to the share price. The bigger the amount of your investment return that comes from dividends and their reinvestment, the less you tend to worry about share prices.

In fact, with this investment strategy you can actually welcome falling share prices. As long as the underlying business is sound, a falling share price allows your dividend to buy more new shares which means more dividends to potentially boost your long term returns.

With this mindset, you worry less and concentrate on what’s important rather than the short-term whims of the stock market. To me this is proper investing and more people would be better off – financially and emotionally – if they put their money to work this way.

That said, evidence suggests that very few investors follow this strategy as the average time that people hold shares is becoming increasingly shorter which means that there is insufficient time for it to pay off.

Buy and hold is not the same as buy and forget

This strategy is based on holding on to a share for a long period of time. This is known as a buy and hold strategy. However, this must not be confused with a buy and forget strategy.

Whilst you do hear stories of people who had left shares invested and forgotten about them for 30 years, and then to find out they had become millionaires, it is probably wiser to keep an eye on your investment from time to time.

I’m not talking about obsessing about share prices every day. Instead you should read the company’s half year and full year results statements to see that all is well and that your dividend is still safe and growing.

The other thing to keep an eye on from time to time is the dividend yield on your shares. This is important because it represents the rate of interest you are getting on your reinvested dividends.

Back in 2000, the dividend yield on BAT shares was 6.7%. This was the income return you would get by reinvesting the dividend. In January 2015, the dividend yield – and reinvestment rate – had fallen to 4.1%. The rate of dividend growth has also slowed down a lot. When this happens, the incremental value from reinvesting diminishes.

What you need to be constantly asking yourself is whether you can reinvest at a higher rate elsewhere? You can search for shares with high dividend yields and dividend growth potential with ShareScope. I’ll be showing you how to do this shortly.

How to set up your own dividend reinvestment plan

Reinvesting your dividends is fairly straightforward. With funds (not exchange traded funds or ETFs) you can buy what are known as accumulation units that do this for you. Alternatively you can set up an automatic dividend reinvestment plan for individual shares with your broker (often restricted to shares that are in the FTSE 350 index) who will reinvest dividends for you for a small fee.

If you don’t want to reinvest back into the same share (for example if the price has gone up a lot and the dividend yield is too low), you can always just let your dividends increase your cash account over a year and then reinvest the money later on when you find a good dividend paying share at a reasonable price.

Looking for reliable dividend payers with ShareScope

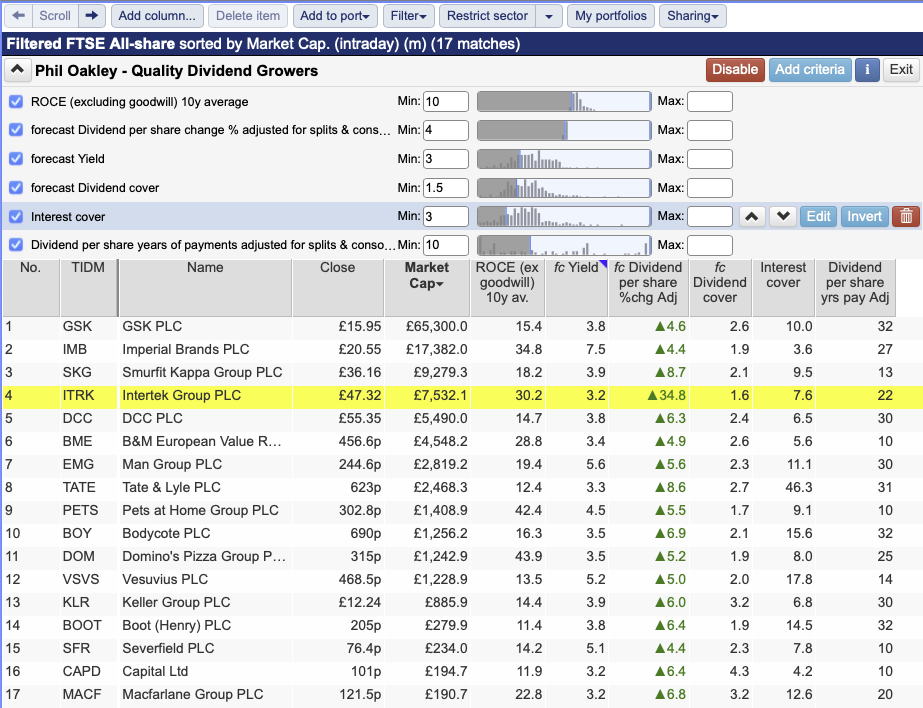

I’m now going to show you how to look for the shares of companies that could be good dividend shares in ShareScope. This is fairly easy to do with the filter function and by adding the criteria that you want the shares to match. You can see a filter that I’ve built below.

I’ve set up this filter to look for shares with the following criteria:

- A minimum dividend yield of 3% – I want a reasonable starting dividend return.

- Minimum dividend cover of 1.5 times – the higher the cover, the better. However, I don’t want to exclude mature industries such as tobacco, telecoms and utilities where dividend cover can be lower but still mean that the dividend can be quite safe.

- Dividend years of payments – At least 10 years. This means that companies that have missed a dividend payment – and often do when times get tough – can be excluded from the list of possible investments.

- A minimum return on capital employed (ROCE) of 10% – This would indicate that the company concerned is a reasonable business and can earn respectable returns on the money it invests, which in turn suggests that it can keep on paying a dividend.

- Forecast dividend growth greater than the rate of inflation – I’ve set a minimum growth rate of 4% so that the dividend increases in value after inflation.

The temptation when you find shares that look interesting based on their numbers is to rush in and buy them.

This can often be a mistake.

Take your time and do your homework.

- Study the company’s financial history

- Read the latest news

- Check that the directors own a decent chunk of shares

- Look at the recent share price performance.

This should be seen as the bare minimum amount of research that you should do.

Following a disciplined approach means that you can learn a great deal about a company.

I also like to read the front half of the company’s annual report which gives a flavour of the company and its short- and longer-term objectives.

You won’t know everything – no outside investor ever does – but you should have enough information to know what you are buying and why.

The real skill in investing often rests with having the patience to wait and pay the right price.

Dividends to live on

People regularly rely on the dividend income from shares as a source of income to live on – especially in retirement and they are not buying an annuity.

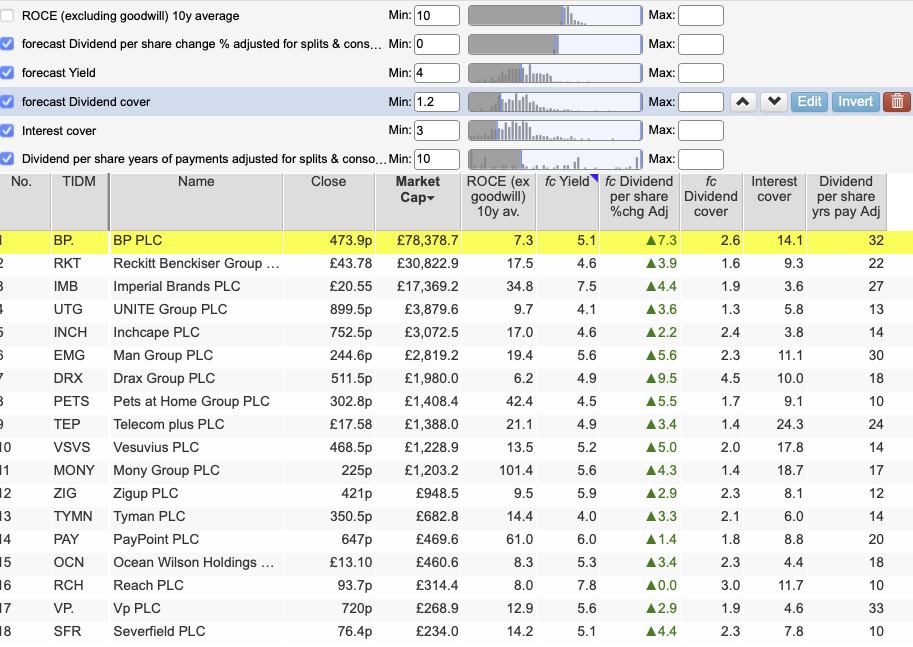

If you are looking for dividend income to supplement your pension, then you can look for shares that might help you to do that in ShareScope. Again, I’ve used the filter function in ShareScope to do this.

The criteria you choose for your filter are up to you. I’ve chosen slightly different criteria to my previous dividend growth filter.

- A minimum dividend yield of 4% – The yield needs to be sufficiently high to provide a reasonable amount of income.

- Dividend cover of at least 1.2 times – so reasonably covered by profit but allowing a large portion of profits to be paid out.

- Continuous dividend payments for at least ten years. I want some comfort that the company has been able to pay some dividend when times have been tough. This gives me some confidence that it might be able to weather economic storms in the future.

- Minimum forecast dividend growth of zero. I am looking for the dividend to be at least maintained at its current level.

Using dividends to find outstanding companies

Outstanding companies don’t necessarily have to pay a dividend or have paid one for a long period of time.

However, companies that have a long track record of increasing their dividend per share every year are often those with the characteristics of great companies.

An ability to keep increasing a dividend payout in recessions, pandemics and in the face of competition is one that generally serves investors well – again with the proviso that they buy the shares at a fair price.

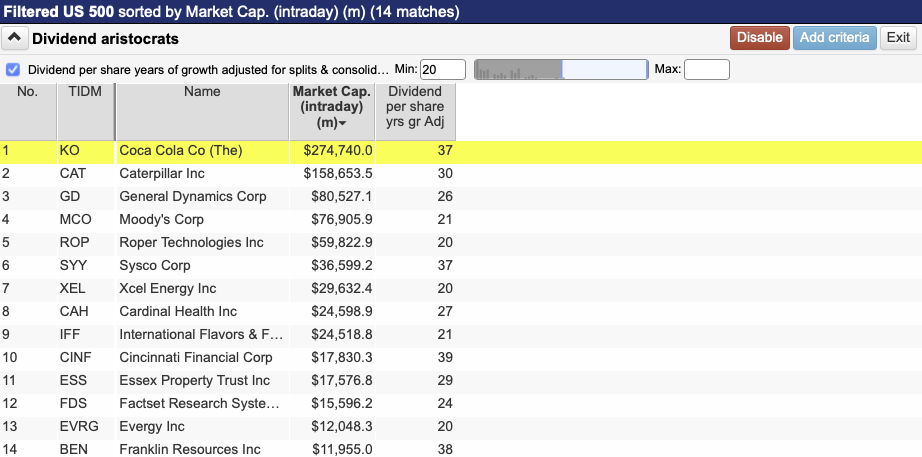

When it comes to the UK stock market, only 10 companies have been able to increase their dividend per share for 20 years or more.

In the S&P 500 over in the US, that number increases to 14.

Leave a Reply