Disclosure – Non-Independent Marketing Communication

This is a non-independent marketing communication commissioned by Greencoat UK Wind (UKW).

Overview Analyst’s

Re-examining the fundamentals behind UKW.

Greencoat UK Wind (UKW) was the first renewable energy infrastructure trust to launch in the UK, and it contributes around 2% of electricity generation in the UK each year. UKW’s success has been the result of a straightforward investment proposition, and a focus on the higher financial returns and cash flows from wind farms relative to other renewables assets, not to mention the scale economies that come with having a £5bn portfolio of assets.

We discuss the financial returns that UKW has delivered for investors in the Performance section. At a basic level, UKW gives investors a relatively pure exposure to the economics of wind farms. Those economics, in their simplest form, rely upon a basic ‘price × volume’ equation; i.e. how much electricity the wind farms produce and the price received (via subsidies and merchant power prices). UKW generates a predictable amount of power over the long term. On the other hand c. 50% of UKW’s lifetime cash flows are exposed to merchant power prices that vary over time. Long term, the ‘energy transition’ is in full swing. Electricity demand looks well set to increase thanks to widespread adoption of EVs, heat pumps, and not forgetting AI and data centres. This growth in demand should underpin both power prices and the demand for additional renewable capacity.

Operational wind farms are highly cash generative, and UKW’s high structural dividend cover gives investors a degree of comfort that the dividend will be paid through the ups and downs of energy prices and wind speeds. As we discuss in greater detail in the Dividend section, the inflation-linked dividend that UKW has paid since launch is core to its attractions. Having a high dividend cover is beneficial as it gives the trust flexibility to deploy surplus income accretively into the best opportunities available to the manager. Reinvestment into the portfolio is key to sustaining cash flows that underpin the dividend (wind farms depreciate over time, and have an assumed 30-year operating life). We expect the manager to increasingly allocate excess capital towards reinvestment to deliver an evergreen portfolio, supporting its sector leading CPI-linked dividend pledge.

Analyst’s View

UKW’s long term NAV total returns have been 7.01% per annum since IPO to 31/03/06 (Bloomberg). Whilst the years since interest rates rose in 2022 have detracted from UKW’s strong track record, we believe the fundamental attractions of the investment proposition have not been impaired. Underpinning everything is the trust’s ability to contribute very significantly to UK homes’ and businesses’ energy demands. As we discuss in the Dividend section, UKW has structurally strong dividend cover. This enables the trust to not only weather short term volatility in energy prices and wind speeds, but also provides enough excess cash generation (post dividend payment) to reinvest into the portfolio to ensure an evergreen portfolio capable of supporting the sector leading CPI-linked dividend pledge.

On the other hand, there has been scrutiny on the subsidy regimes that apply to renewables, given the high cost of energy in the UK and tight public finances. No one expects UK politics to return to stability any time soon. The truth is that the UK needs to continue to attract long-term private sector investment in renewables (and other infrastructure) so the government would need to be very careful about impacting the confidence of investors. Further, renewables is both quicker to market and cheaper to deliver than the alternatives (gas and nuclear).

As we discuss in the Discount section, worries about what a new energy price regime will look like are part of the reason for UKW’s shares trading at a wide discount to NAV. With the manager focussed on maximising NAV total returns and the reinvestment of excess cash flows (see Performance section), whilst also de-gearing the trust to below its self-imposed limit of 40% of GAV, there is clear potential for any resolution in political worries to boost shareholder returns through the discount narrowing. In the meantime, shareholders stand to benefit from the attractive dividend yield of 10.2%.

Bull

- High dividend yield, well covered by cash flows, gives plenty of flexibility to managers for accretive investment activity

- Continued commitment to CPI-linked dividend growth, yet trading on a wide discount to NAV

- Diversified portfolio of institutional-scale assets, spread around the UK

Bear

- Discount to NAV may persist, meaning UKW cannot augment organic reinvestment with new equity

- Gearing exacerbates underlying asset valuation movements

- Valuations based on long-term assumptions that may (or may not) prove optimistic

Dividend

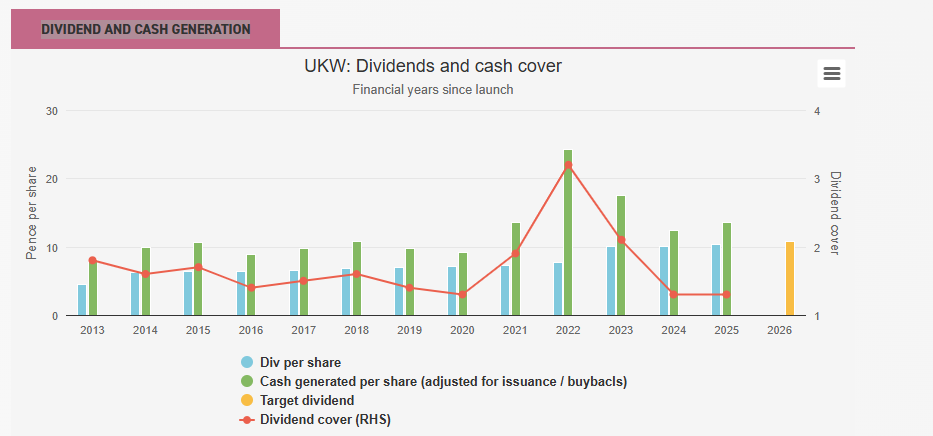

As we discuss in the Portfolio section, wind farms are highly cash generative and UKW was IPOed to deliver to shareholders a high and attractive income stream, linked to inflation, alongside preservation of the NAV in real terms. As such, the historic dividend serves as one important yardstick of whether the trust has achieved its aims. As the chart below shows, UKW has increased its dividend each year from an annualised 6p per share at IPO in 2013 to 10.35p paid last year. UKW’s dividend target for 2026 is 10.7p per share, equivalent to a yield of 10.2% at the current share price. The board has an explicit aim of raising the dividend in line with inflation, which they have achieved since IPO, and they continue to repeat this ambition publicly.

Clearly the board’s aims may or may not reflect reality, and so other than its wish to avoid being seen to have failed, we believe shareholders should also take a lot of comfort from the strong dividend cover that UKW has exhibited historically. In fact, UKW’s dividend cover has averaged 1.7× since launch, which provides protection against the natural variability in energy production and cyclicality in energy prices. Underpinning cash flows is UKW’s subsidies’ explicit link to inflation. According to the manager, over the next seven years (2026 onwards), 59% of the portfolio value will be comprised of fixed cash flows, the vast majority of which are explicitly linked to inflation. The graph below shows that the last two years have seen below target dividend cover of 1.3×, mostly a reflection of below average wind speeds and lower energy prices.

The managers appear confident that dividend cover will improve in coming years. During the current financial year, UKW has reported a strong start to 2026 with Q1 output 4% ahead of budget and anecdotal evidence suggesting Q2 will also be above budget. Higher power prices as a result of the Iran war might suggest that the trust could return to dividend cover more in line with the long-term average of 1.7× for 2026. Over the next five years, according to the company, UKW expects to achieve a dividend cover of 1.7–2.1×. In early 2026, the UK government announced that, given RPI is being discontinued as an inflation measure, subsidies previously linked to RPI will be linked to CPI in future. Mirroring this move, UKW’s board has adopted CPI as the new target for the 2026 dividend increases, and for future dividends henceforth.

DIVIDEND AND CASH GENERATION

Source: Schroders Greencoat

Past performance is not a reliable indicator of future results

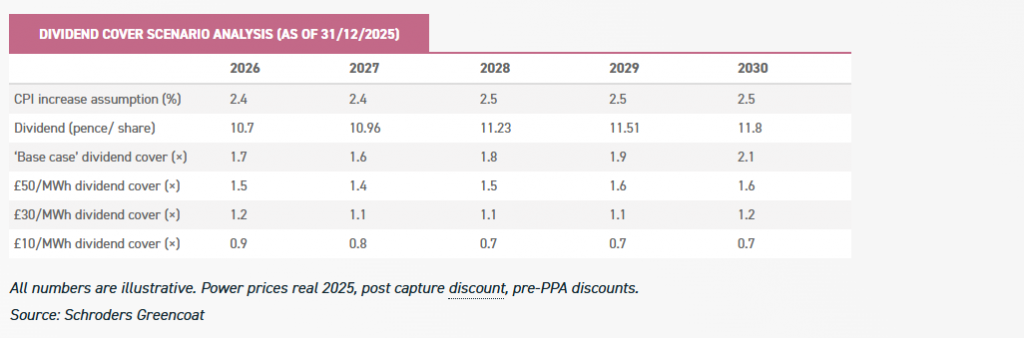

President Trump’s ill-thought-out war with Iran, and the potential for a lasting truce or end to the war, have meant energy prices have been volatile. UKW has been a beneficiary of this turbulence, and took the opportunity in Q1 2026 to fix around a quarter of its expected electricity output for 2026 at an attractive rate. If a lasting peace is secured then energy prices might be expected to fall. In this context, UKW provides this table, which should provide reassurance to shareholders that UKW’s dividend should remain resilient in the coming years, even if electricity prices fall precipitously.

DIVIDEND COVER SCENARIO ANALYSIS (AS OF 31/12/2025)

Source: Schroders Greencoat

Leave a Reply