Revisiting FAIR Oaks Income

The high yield (14.6%) world of CLOs

Thanks for reading The Oak Bloke’s Substack! Subscribe for free to receive new posts and support my work.

Dear reader

This is an idea from the OB 2024 (which are up 1.3% in 2025), and one of the highest yielding shares out there. In fact your broker asks you to “prove” you are sophisticated enough to buy this share.

This article recaps the principle of a “CLO” and examines performance and considers what 2025 might bring.

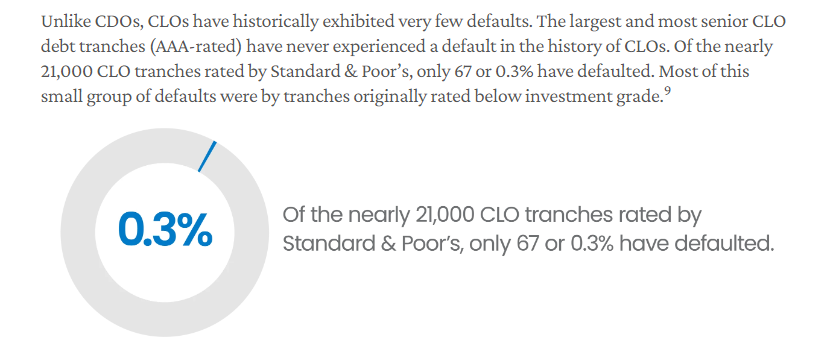

So you’ve heard of junk bonds, probably. What makes it “junk” exactly? Risk. BB rated or below is junk. Above BB is “investment grade”. The theory is lending to the government is perfectly safe, and then lending to business is risky. Those risks range from AAA down to CCC. Investment grade you’ll earn 5%-6%. Junk you’ll earn much more. 10%-17%. Some loans are “junkier” than others. The “junkiest” can be picked up for pennies in the pound. Bit like factoring. But is “junk” actually junk? Or is there brass where there’s muck?

So a CLO is basically a packaging up and pooling of various loans into a vehicle which funds itself via what it calls equity and debt. The debt investors get diversification and credit-enhancement benefit, while CLO equity investors get higher returns.

Confused? If only I had someone like Margot Robbie to explain.

Now Margot, if you paid attention, explained CDOs and MBS Mortgage Backed Securities and just gave you quite a negative view of these. CLOs aren’t CDOs (which are based on residential mortgages) – CLOs are business loans instead. But the principle is similar. Hence the video.

So CLOs are bad?

Potentially yes. But this blog article “how CLOs” endured the great financial crisis” provides an excellent explanation of why the great short (poor man) Michael Burry wouldn’t (and to my knowledge didn’t) bet the house (so to speak ha ha) against CLOs.

CLOs or Collateralised Loan Obligations are managed by clever firms who, on your behalf, sniff out and buy a package of loans, but who also borrow money to enhance returns and manage risk. To “over collateralise” means to buy CLOs that come with a degree of protection. If defaults remain at X% then you don’t lose out. That’s called a cushion…. a margin of safety. It’s about 4%-5% in FAIR’s case. More on that when we speak about the Covid crisis later.

How do you even buy FAIR? Well you have to become a “sophisticated investor”. In plain English this means your broker will have a short, online questionnaire. Once you answer those satisfactorily this unlocks certain investments you couldn’t access before. Put them in your ISA or SIPP same as any other share. Each time you access FAIR’s web site you have to agree some T&Cs before they’ll let you see any info.

One of these “sophisticated” options are CLOs run, bought and managed by firms like Fair Oak Income. These invest in both equity and debt. They run a lot of mathematical models to control for risk and because loans are bought and sold much like stocks and shares they recycle funds into new CLOs and CLNs. The OCF charge is 1.29% so they make good money in this world.

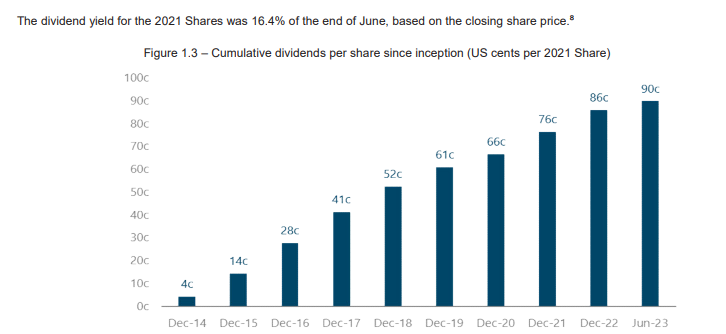

The dividend yield is currently above 14%. And FAIR has been consistently churning out dividends since 2014. It’s fair to say you aren’t going to achieve great capital gains but if your objective is to generate income then this investment has quite some attraction.

Risk

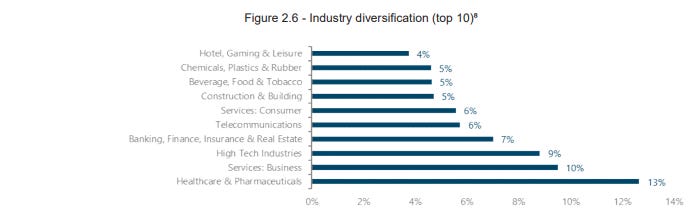

While a huge black swan event would affect CLOs and rising levels of default could affect future returns it’s also the case that CLOs are generally managed to spread risk by geography, by industry and by specific lender. Your eggs aren’t in a single basket.

This is the industry diversification of FAIR. So quite some degree of diversification.

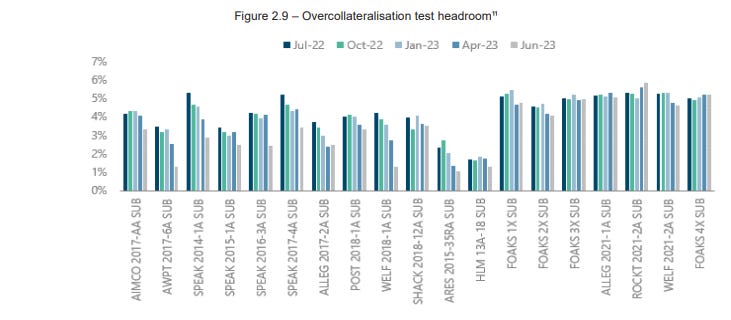

Generally things would have to get “really bad” to actually lose money as in above 5%. Below this level is called “Distress”.

A few years back we had elevated “Distress” during covid. Fair Oaks annual report shows us what happened next. Distress in green spiked and then fell. Defaults in blue rose and receded. Overcollateralisation meant FAIR – or FAIR shareholders – didn’t lose anything…. on that occasion.

In the event of things getting bad beyond Covid level bad, a further level of bad would be dividends are cut (but in 2020/2021 they weren’t). Level 2 bad would be capital loss. But this is rarer than you might think. The link to Clarion shows this statistic.

But the other perspective about “things getting bad” is that new loans get cheaper and more profitable (aka reinvestment spreads). For example Clarion tells us “Historically, wider reinvestment spreads can mitigate or exceed elevated loan losses during economic downturns. Reflecting this dynamic, total returns for CLOs rose in the years following the GFC.” (The GFC is not a Roald Dahl character but instead the Great Financial Crisis i.e. 2008-2009)

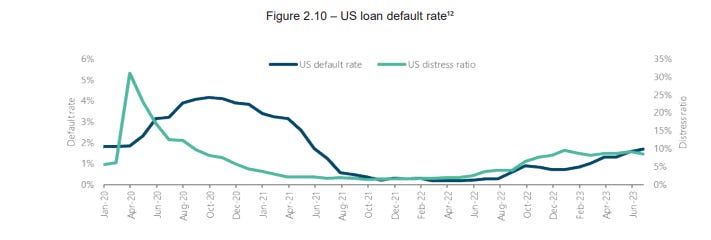

This is illustrated in Fair Oaks 2022 report – during Covid you could buy loans for “25% off” during the 1st lockdown. So a 20% yield jumps to a 27% yield, so losing 12% through defaults, is countered by +5% over collateralisation plus gaining +7% yield on new investments. So these are opposing forces which suddenly makes CLOs – and Black Swans – a bit less scary. In my mind at least. Especially if your mathematical models mean you build and conserve cash ahead of bad events and can therefore take advantage of said bad events by buying at 25% off.

The CLO Business Model

The above chart is basically what gives these outsize returns. If a business is being charged say 10% interest for a loan, then the price of the risk of that loan means you can buy that 10% loan for say 94p in the pound. By borrowing money a CLO equity holder can earn well over 20% through leverage. That’s roughly the business model.

Do the sums add up?

Looking at the 2022 and 2021 accounts you can see there’s a fair value through P&L gain in 1 year and a loss in another. Roughly speaking “distributions” which are the loan repayments fund the dividend and then fair gains and losses increase or decrease the capital.

To my mind, looking at FAIR’s P&L there are actual returns “distributions” funding the dividend so this isn’t a snake eating its own tail. It’s also true, however, these are complicated accounts so isn’t as simple as buying and selling widgets. See my back of a fag packet assessment further on.

Why FAIR and not another CLO operator?

I can’t answer that. There are several out there all delivering a high dividend. BGLF was another reader idea. Fair is one of the highest yielders. One could argue lower yielders potentially offers higher chances of capital growth. This video gives you a glimpse into the world of CLOs.

Oak Bloke Rationale for FAIR

- Speaking personally I was impressed with the CVs of the managers.

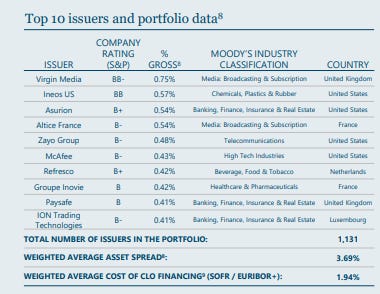

- I was also impressed that when you dig beyond the “junk bond” label you are lending to a wide range of businesses and the likes of Virgin Media, Ineos and McAfee. Default percentages start to feel a little less scary when you think it’s businesses like these. The label “Junk” feels inaccurate. Remember, too, bond holders get dibs over equity holders. (Although it’s also true that BB loans are going to be behind “Investment Grade” or Senior Loans – or indeed Tax owed to government for example)

- Buy backs. The fact that when a discount opens up FAIR aggressively buy back shares which also boosts value and delivers capital gains as well as dividend returns.

- What also appealed to me is the idea there’s “hidden value”. And what I mean is simply this. Please show me a single occasion where CLOs get any kind of positive write up by any other investment analyst? Okay, okay, Hardman’s coverage of Volta is the exception. Watching Serge Demay of Volta being interviewed helped me feel more comfortable about CLOs.

For most investment writers this topic area is difficult & complicated. Far easier to talk about the likes of a company selling widgets. When writing an article about FAIR it’s an easy cop out to focus negatively on the risk – writing such an article is almost the simplest way to explain (and dismiss) Fair Oaks or CLOs like this.

But otherwise all articles are negative, negative, negative. Risk, risk, risk. Go and search for yourself – here’s a link to Google news for Fair Oaks.

A bit of back of a Fag Packet Maths: (based on the 2022 accounts)

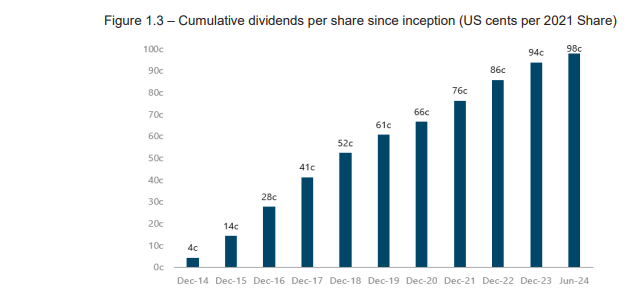

8c dividends cost $36m/year. So 90 cents distributed is about $405m cumulatively.

$432m original share capital and -$170m negative retained earnings (that sounds scary doesn’t it?) is $260m net (and $240m as at the last accounts 30/06/24).

So in 8 years, FAIR has more or less returned ALL capital (okay 93.75% $432m-$405m if you’re being picky). Plus still has assets of $260m (which is about 55p a share) and that 55p is like a profit. Okay dividend distributions eats into that number, but it’s still a profit. Not a snake eating itself which was the reason to do that maths and to think about that $170m apparent LOSS. So what I’m saying is if you’d bought FAIR on day 1 (in 2014) you’d still be quids in still in 2025.

This analysis is my attempt to explain the opprotunity and gives the good and bad of Fair Oaks income. Hopefully it helps also demystify this complicated area a little bit and gives you a starting point for your own research and to consider whether you should become a “sophisticated” investor.

Prospects for 2025

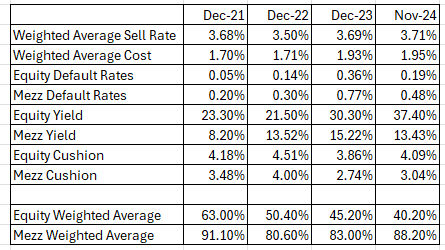

I ran through the different metrics over the past 4 years to get an idea of how FAIR fares over time.

CLO Equity at the end of 2024 offers increasing yields but can be bought at lower levels. While Mezzanine debt is in front of equity the low default rates and a reasonable average 3%-4% OC Test Cushion offers quite some comfort.

I personally continue to hold FAIR and it is nice to see the dividend roll in each quarter. I don’t expect it to deliver capital returns, in fact my analysis expects some limited amount of capital losses, but as a tasty dividend machine the dials appear to point to still point green in 2025. In fact those growing CLO equity yields look positively ripe.

Regards

The Oak Bloke

Disclaimers:

This is not advice, make your own investment decisions.

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as “blue chip”

Leave a Reply