Best Stocks For Building A Barbell For Midterms And Geopolitical Risk

May 07, 2026 CRDO, ICHR, CSTM, NEM, PSTL, THG

Steven Cress, Quant Team

SA Quant Strategist

Summary

- Volatility has historically increased ahead of midterm elections, especially with other market pressures, such as geopolitical tensions, weighing on investor sentiment. We saw a similar macro backdrop in 2022.

- By pairing well-positioned growth companies with income-generating, rate-sensitive assets, investors can build a portfolio that can withstand volatile markets amid midterm elections and geopolitical tensions.

- To do this, a barbell approach, which provides a balanced portfolio built for managing both opportunity and uncertainty, has historically worked well.

- I am Steven Cress, Head of Quantitative Strategies at Seeking Alpha. I manage the quant ratings and factor grades on stocks and ETFs in Seeking Alpha Premium. I also lead Alpha Picks, which selects the two most attractive stocks to buy each month, and also determines when to sell them.

Best Stocks for Volatility: A Barbell Approach

With U.S. midterm elections now just six months away, markets are entering a period where policy uncertainty combines with seasonal volatility and lingering geopolitical uncertainty. While investors cheer all-time highs and can expect pockets of growth in AI-related stocks, multiple headwinds are likely to create significant volatility in the months ahead.

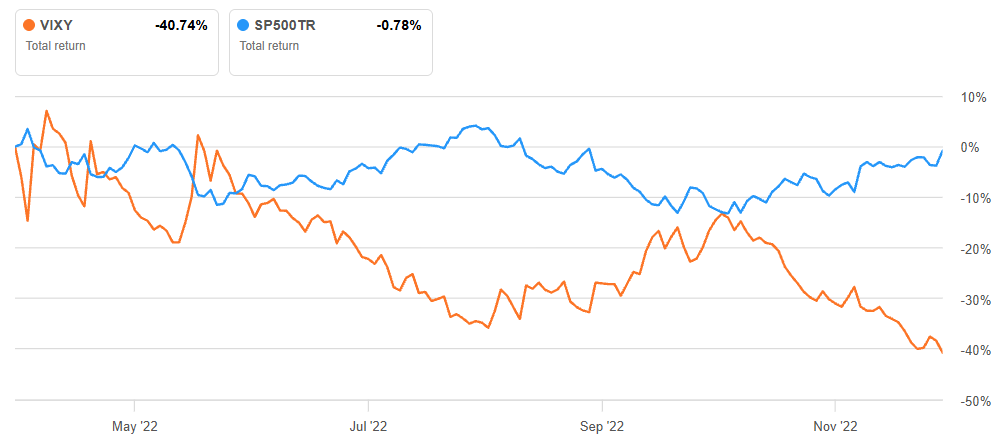

This period draws many parallels to the summer of 2022, when the Russia-Ukraine conflict was causing geopolitical tensions while the U.S. was headed into midterms during Joe Biden’s first term. That macro backdrop created mixed performance as investors struggled to price in 40–year-highs for inflation, oil supply disruptions, and political shifts.

Volatility Increased Leading Up to 2022 Midterms

In environments like these, a barbell approach that pairs high-quality, income-generating defensive stocks with selective, high-growth opportunities has historically helped to minimize downside risk while still participating in upside. The following mix of six Quant Strong Buy stocks is designed to navigate volatility while remaining well positioned for longer-term growth.

How I Chose the Best Stocks to Build a Barbell Structure

To arrive at the best stocks for my barbell mix, I used the Seeking Alpha Stock Screener and chose the respective category in diverse categories, including Information Technology, Basic Materials, and Financials, then filtered for specific industries, such as semiconductors, gold, and property and casualty. I only considered highly rated Quant Strong Buys for my top six.

Growth Side: Offensive Exposure to AI and Infrastructure

AI infrastructure beneficiaries and select materials stocks are strong candidates for the growth side of the barbell.

1. Credo Technology Group Holding Ltd (CRDO)

- Market Capitalization: $36.57B

- Quant Rating: Strong Buy

- Quant Sector Ranking (As of May 7, 2026): 12 out of 527

- Quant Industry Ranking (As of May 7, 2026): 6 out of 69

- Sector: Information Technology

- Industry: Semiconductors

Beginning with a stock that’s in both my Alpha Picks and Pro Quant Portfolio lineups, Credo Technology is a key AI infrastructure supplier providing high-speed connectivity solutions within hyperscale data centers. Credo’s products act as the “plumbing” that GPUs and servers, helping to ensure high speed communication as workloads scale across data centers. In today’s macro environment, where hyperscalers continue massive capex spending despite the broader market uncertainty, CRDO offers direct exposure to the best growth opportunities of 2026.

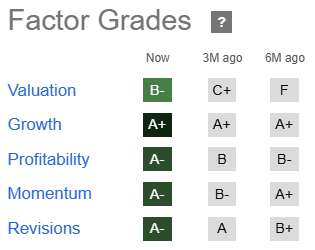

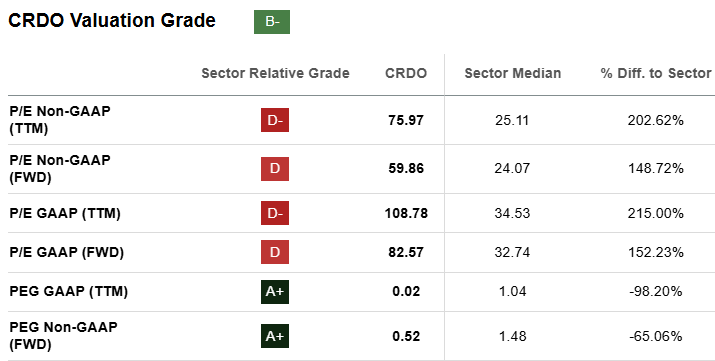

Despite what appears to be a large premium from a pure P/E perspective, CRDO’s forward PEG of 0.52 offers more than a 65% discount to the sector median. My readers and subscribers know that the PEG is my favorite valuation metric because it adjusts for forward growth, which is CRDO’s strongest attribute.

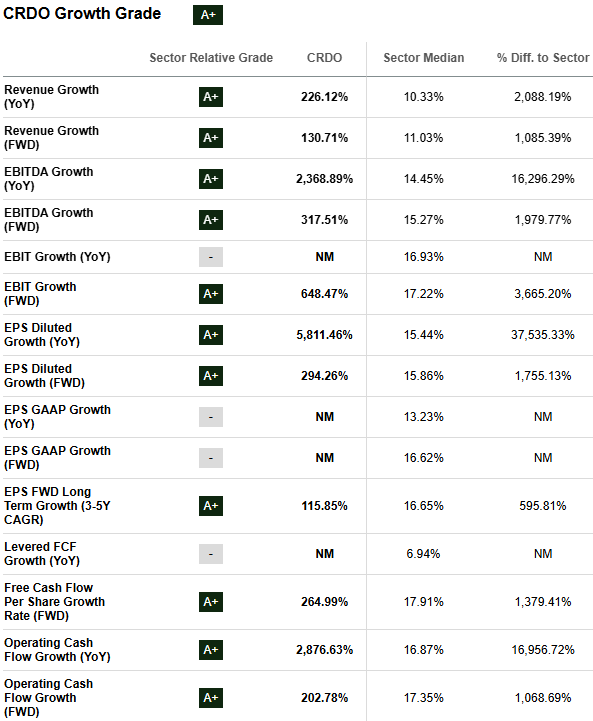

Investors who follow Quant know that you won’t find many stocks with ‘A+’ growth metrics as deep into the score card as Credo. Digging beneath the surface of its sector-crushing forward revenue growth, CRDO’s forward EBITDA, which shows how the company’s growth can translate into stronger earnings power, is more than 317%, which is more than 20x above the sector median. Demonstrating that earnings are translating into real cash, CRDO’s forward Operating Cash Flow Growth is above 200%, which is more than 1,000% ahead of sector peers. This also enables Credo to strategically invest in more growth opportunities, as it did with its recent deal to acquire DustPhotonics. Within the barbell framework, CRDO anchors the growth side with AI-focused strength. That infrastructure demand naturally takes us into semiconductor production capacity, where our next stock for the growth/offensive side.

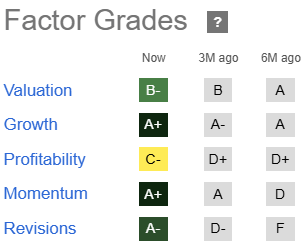

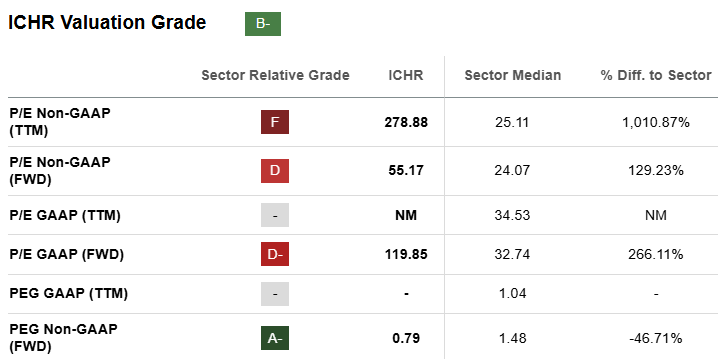

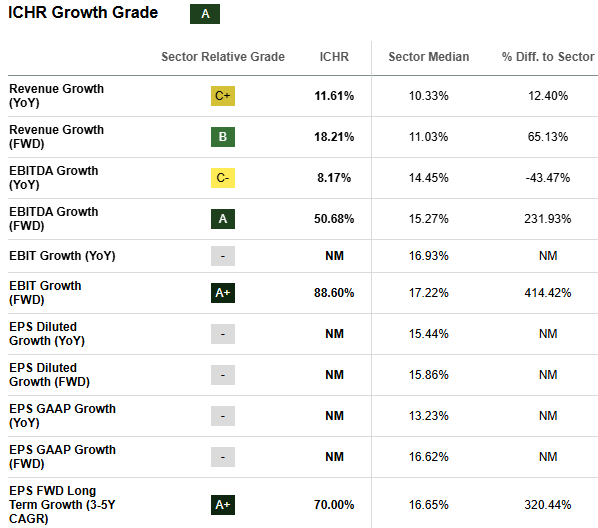

2. Ichor Holdings, Ltd. (ICHR)

- Market Capitalization: $2.52B

- Quant Rating: Strong Buy

- Quant Sector Ranking (As of May 7, 2026): 5 out 0f 527

- Quant Industry Ranking (As of May 7, 2026): 2 out of 32

- Sector: Information Technology

- Industry: Semiconductor Materials & Equipment

A recent addition to my Pro Quant Portfolio, Ichor Holdings designs, engineers, and manufactures fluid delivery systems for semiconductor equipment. This places ICHR upstream in the chip production cycle, working closely with leading wafer fabrication equipment providers, making it an early beneficiary of capex spending. As the AI buildout drives the need for more advanced chips, Ichor can continue to benefit from new data center buildouts.

As I like to do with many of the growth stocks I feature in articles or add to portfolios, the superficial valuation metric, the trailing P/E, makes ICHR look incredibly expensive. While the forward P/E looks less expensive, investors should consider the forward PEG to get a clearer picture of growth-adjusted valuation. For ICHR, this metric suggests more than a 46% discount to the sector median. Focusing on the PEG has proved largely effective for me and many subscribers in picking growth stocks.

Wafer fabrication equipment demand is expected to grow by 15-20% in 2026. Forward EBITDA Growth is expected at above 50%, which is more than 3x the sector median. In this week’s quarterly earnings call, CEO Philip Barros framed Q1 as early execution in what he called “a multiyear growth cycle,” saying, “Q1 revenues of $256 million came in at the upper end of our expectations, up 15% from Q4,” and adding, “Our Q2 forecast now reflects unconstrained demand exceeding $300 million.” Ichor’s early cycle buildout exposure supports its growth profile through the barbell’s offensive sleeve. Finishing that growth sleeve, we turn to physical materials that support electrification and industrial demand.

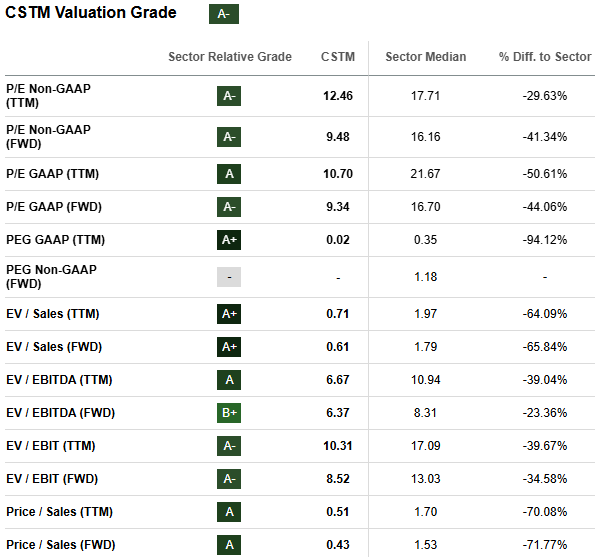

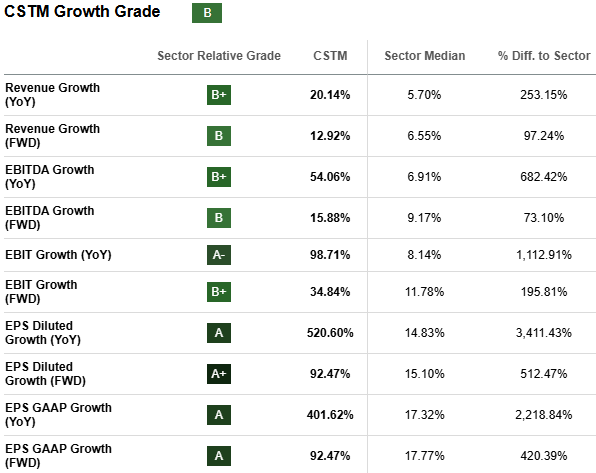

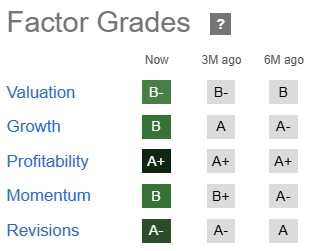

3. Constellium SE (CSTM)

- Market Capitalization: 4.54B

- Quant Rating: Strong Buy

- Quant Sector Ranking (As of May 7, 2026): 5 out of 283

- Quant Industry Ranking (As of May 7, 2026): 1 out of 5

- Sector: Materials

- Industry: Aluminum

Another holding in my Alpha Picks portfolio, Constellium is a global producer of advanced aluminum products for a broad range of applications, including aerospace, automotive, and packaging markets. In a challenging macro backdrop in 2026, CSTM benefits from demand for all its products in a range of spaces, including electrification, infrastructure investment, and industrial reshoring. This provides a complement to our AI stocks in the growth sleeve of our barbell mix.

CSTM has the most attractive valuation of our growth stocks, and we don’t need the forward PEG ratio to prove it. The company’s forward P/E starts off the value story, weighing in at 9.48, which is more than a 40% discount to the sector median. This attractive discount suggests CSTM’s price has room to run, especially when considering its solid forward growth numbers.

In last week’s Q1 earnings call, CEO and Director Ingrid Joerg announced, “We are very pleased with our first quarter performance, including record adjusted EBITDA,” and “we are also raising our outlook for the full year and expect 2026 to be a record year for the company, both in terms of adjusted EBITDA and free cash flow.” CSTM’s outlook for 2026 looks promising, as management’s guidance for the year expects that favorable market conditions will continue amid supply shortages of automotive rolled products in North America as well as in aerospace.

Income Side: Defensive Plays for Volatility

Gold miners stand to benefit from a falling dollar and lower real yields in a post-Iran conflict environment, while property and casualty insurers provide stability.

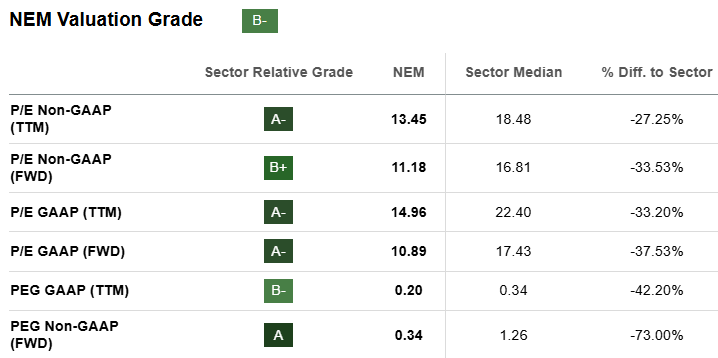

4. Newmont Corporation (NEM)

- Market Capitalization: $122.88B

- Quant Rating: Strong Buy

- Quant Sector Ranking (As of May 7, 2026): 18 out of 283

- Quant Industry Ranking (As of May 7, 2026): 2 out of 49

- Sector: Materials

- Industry: Gold

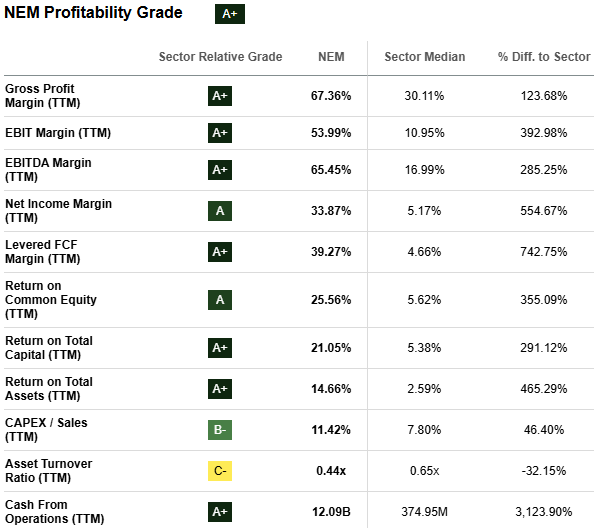

Another one of my Alpha Picks holdings, Newmont Corporation, is one of the world’s largest gold producers. Although not the most leveraged miner to buy within its peer group, it’s a large-cap, dividend-paying business that stands out due to its scale, diversified asset base, and solid fundamentals, making NEM the right choice for my barbell mix. Miners like Newmont are also mostly oversold and have moved inversely to oil as the dollar has strengthened. Tuesday’s move was a prime example as hopes for peace in the Middle East drove oil prices down, settling the day around 5% below where it started. Meanwhile, gold moved higher, and NEM’s price jumped 5.6%. From a Quant perspective, Newmont’s valuation and profitability are standouts that help to support its ‘A+’ Dividend Growth score.

In an environment where gold can move higher, but volatility is expected, a large miner with an attractive valuation supports the income/defense sleeve of my barbell structure. NEM’s forward P/E of 11.18 already offers more than a 33% discount to the sector median, but the PEG is even more attractive at 0.34, indicating a growth-adjusted 73% discount to its peers.

A mature miner with scale like Newmont can manage operating costs while benefiting from higher gold prices, as is evidenced by the EBITDA Margin of more than 65%, which is 285% better than the sector median. NEM’s monstrous Cash From Operations of 12.09B provides more support for the profitability story, helping to earn its ‘A+’ for the Quant Factor. It also supports growth for its dividend. Should the economy slow more than expected, NEM becomes a defensive shield as it benefits from falling real yields. That rate sensitivity extends into the Real Estate sector, where our next income/defensive piece of the barbell comes into play.

5. Postal Realty Trust (PSTL)

- Market Capitalization: $810.07M

- Quant Rating: Strong Buy

- Quant Sector Ranking (As of May 7, 2026): 1 out of 171

- Quant Industry Ranking (As of May 7, 2026): 1 out of 16

- Sector: Real Estate

- Industry: Office REITs

Featured in a dividend article I wrote last week, Postal Realty Trust is a niche REIT that owns properties leased primarily to the U.S. Postal Service, providing sovereign-backed stability with 100% rent collection. This makes PSTL attractive as a rate-sensitive asset acting as a defensive anchor against 2026 election-year volatility. Its near-full occupancy and growth acquisition strategy set it apart from the typical REIT.

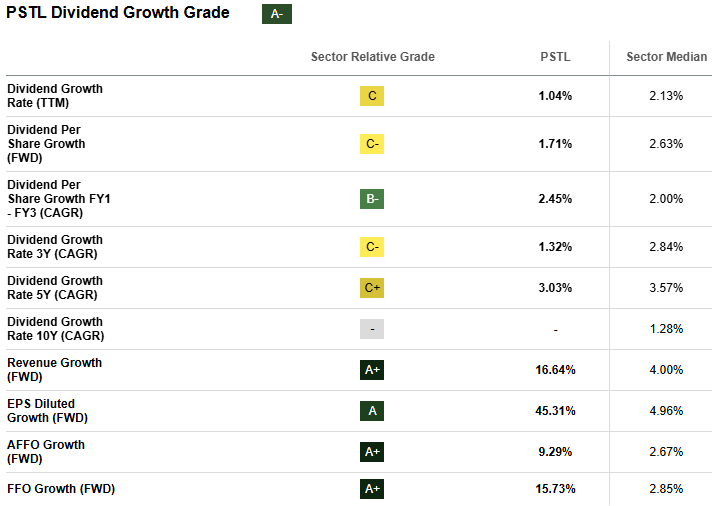

PSTL’s predictable cash flows and 4.22% yield make it especially attractive in a falling rate environment where investors seek reliable income alternatives to fixed income. From a Quant perspective, PSTL demonstrates strong forward earnings potential and high scores for dividend growth.

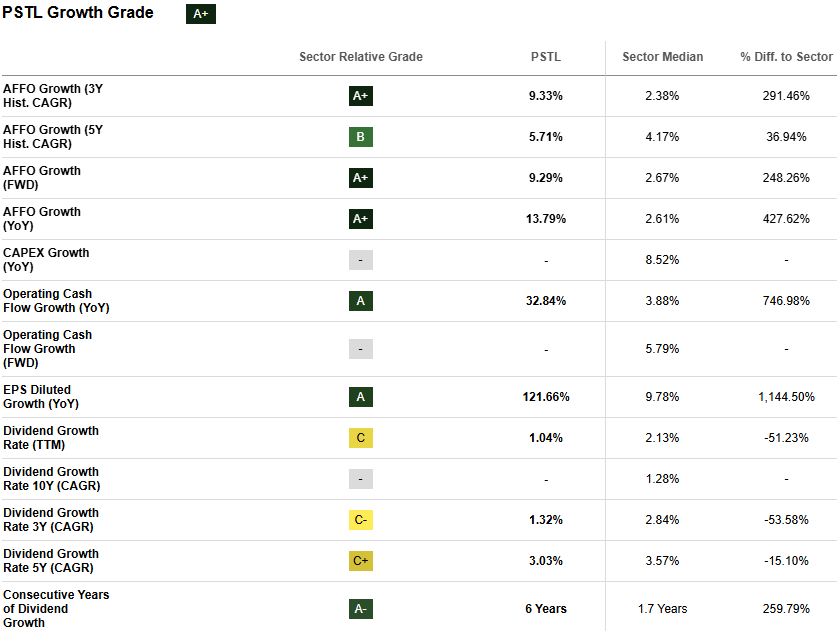

PSTL’s forward AFFO Growth of 9.29%, which approaches 250% above the sector median, signals that the company is expected to grow its true cash flow per share at a much faster rate than peers, which is notable for a traditionally slow-growing, income-oriented REIT. In other words, PSTL is not only a solid bond proxy, but it also combines stable, government-backed income with above-average, acquisition-driven growth. In its Q4 earnings call, CEO Andrew Spodek noted PSTL’s strong acquisition pipeline, highlighting that initial 2026 guidance is $115 million to $125 million in acquisitions at a mid-7% weighted average cap rate. This cash flow stability combined with growth potential supports further dividend strength.

While PSTL’s 4%+ yield is solid, there’s room for growing its payout ratio as the Quant Growth Dividend grade of ‘A-’ suggests. As noted in the growth factor metrics, PSTL’s forward AFFO is more than 3x the sector median, demonstrating sustainable cash flow available to shareholders. While real estate companies like PSTL offer stable cash flow, insurance introduces another layer of defense through pricing power, which brings us to the next piece of our income/defensive barbell stock.

6. The Hanover Insurance Group, Inc. (THG)

- Market Capitalization: $6.52B

- Quant Rating: Strong Buy

- Quant Sector Ranking (As of May 7, 2026): 12 out of 683

- Quant Industry Ranking (As of May 7, 2026): 1 out of 54

- Sector: Financials

- Industry: Property and Casualty Insurance

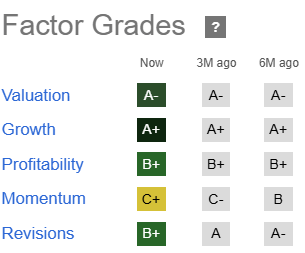

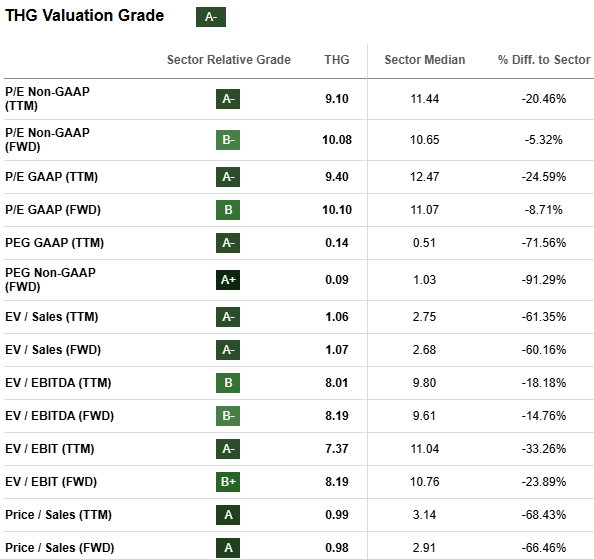

Hanover Insurance Group is a property and casualty insurer focused on personal, commercial, and specialty lines, known for a diversified portfolio and disciplined underwriting. The Top Property and Casualty Insurance stock, THG stands out through strong premium growth, healthy profit margins, and attractive dividend scores. In the current environment, pricing power allows the company to grow earnings, despite economic uncertainty, providing a defensive balance to our barbell mix. The insurance exposure also adds diversification to the gold and REIT complements. From a Quant perspective, THG’s impressive valuation and dividend scores stand out for this stock.

In an environment where U.S. midterm election uncertainty combined with geopolitical tensions may create significant market volatility, THG’s forward PEG of 0.09, which is more than a 90% discount to sector peers, suggests stability and potential price appreciation. In its Q1 earnings, THG “achieved record first quarter performance, including operating return on equity of 20.3% and operating earnings per share of $5.25.” CFO Jeffrey Farber added that, “for the full year, we continue to expect an expense ratio of 30.3% as the benefit of growth leverage skews toward the latter part of the year.” This indicates efficient cost control and stronger underwriting ability, further supporting the company’s impressive Quant Dividend Scorecard.

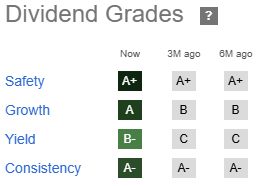

For purposes of our barbell mix, THG’s 2.04% yield isn’t as much for income purposes as it is for a signal of stability and fundamental strength. Seeing improvements in the past six months in its Dividend Growth from a ‘B’ to an ‘A’ and its Yield from ‘C’ to ‘B-’ provides evidence of the defensive characteristic needed to complete our barbell structure. Together, these six Quant Strong Buy stocks illustrate how a diversified barbell can capture growth while managing risk in a coming macro environment where midterms, seasonality, and geopolitics combine for market volatility.

Conclusion: Managing Both Opportunity and Uncertainty

This barbell structure combines high-growth exposure to AI infrastructure growth from massive hyperscale capex spending as well as industrial demand. Balancing the growth side is defensive positions in gold, real estate, and insurance. By pairing well-positioned growth companies with income-generating, rate-sensitive assets, investors can build a portfolio that can withstand volatile markets amid midterm elections and geopolitical tensions. However, risks remain. AI stocks may face valuation pressure if spending slows, and gold prices and insurance profitability can fluctuate with macro shifts. Despite these risks, a barbell approach provides a balanced portfolio built for managing both opportunity and uncertainty.

We have many stocks with strong buy recommendations, and you can filter them using Stock Screens to suit your specific investment objectives. Subscribe to Premium for unlimited access to Seeking Alpha quant ratings and expert content. Alternatively, if you’re looking for a select number of Quant Strong Buy recommendations on a monthly basis, you might want to explore Alpha Picks.

Leave a Reply