The SNOWBALL has a comparison share VWRP, the comparison being, you buy VWRP and forget about it until you enter drawdown, with the intention of using the 4% rule to fund your retirement.

The SNOWBALL

I don’t update this very often has it has little relevance to the plan as your Snowball should be different to the SNOWBALL has it reflects the years you have before you enter drawdown.

(Note the spike on the graph is a software glitch.)

The comparisons

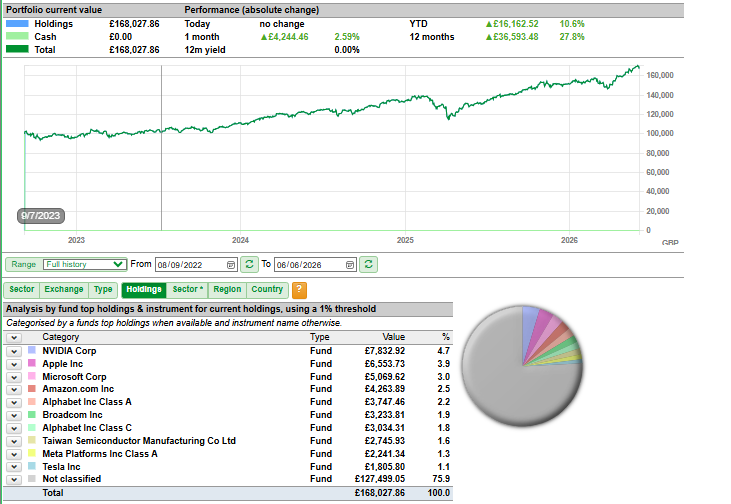

VWRP £168,027

The SNOWBALL £106,178. There is around 1k of xd dividends but it makes no difference to the outcome.

The comparison that matters.

VWRP using the 4% rule would provided income of £6,721

The SNOWBALL current income is £12k.

This gap will continue to grow, especially has VWRP has had a period of out performance that is unlikely to be replicated.

The third option is to invest in VWRP with the intention of buying an annuity.

You have to surrender your capital but currently it would provide income of

£11,671.

The two know unknowns are what will your capital be when you enter drawdown and the annuity rate it could be………….

Canada Life figures show the 65-year-old with a £100,000 pension pot could buy an annuity linked to the retail price index (RPI) that would generate a starting annual income of £3,896. That’s up from £2,195 in the New Year following a 77% spike in rates this year.

Oct 22.

One huge gamble.

VWRP used as the example but there are very many other options to invest in.

Leave a Reply