The RGL of the hero from Sherwood Forest

Considering the rent update from Regional REIT – RGL

The Oak Bloke

Jun 30

It was the 18th June when OB pick for 26 RGL announced £1.1m of new rent. This enigmatic news in a riddle wrapped up in an enigma was so well hidden from the market that RGL went up by zero.

Why do I believe this is a Quadruple-Win?

This single deal improves Regional REIT’s bottom line in three distinct ways:

New Revenue Stream: They have secured £1,075,000 per year in new rent.

Cost Eradication: Because these buildings were 100% vacant, Regional REIT was paying £700,000 per year just in “void costs” (business rates, security, basic maintenance, insurance). This cost now drops to zero as the tenant takes on those costs as a charge through.

Capital appreciation: £5m upgrade of facilities.

The fourth win is not RGL’s… because the Client wins too. Paying just £7.35 per square foot is a super cheap price. No wonder they were prepared to invest £5m to upgrade the space. Going rate for Nottingham on Rightmove is about double that price. £13m/sq.ft is the cheapest I can see. Or can you find plenty of office space for £1 a square foot? In Poundland maybe? Or on the Hindenburg? More on that later.

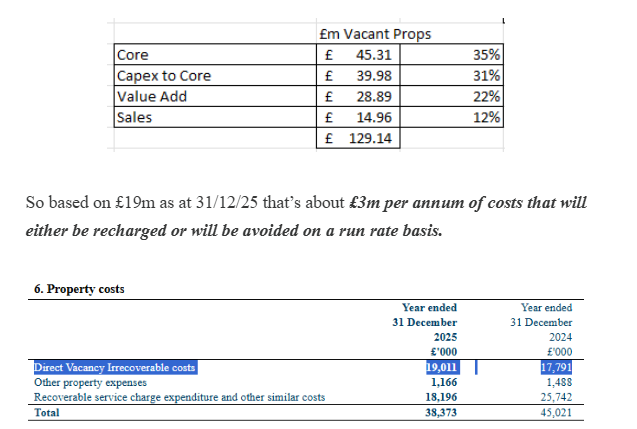

In 2026 based on the YTD £15m of disposals at an average 90% vacant and this Newstead Unit 1 and 2 deal (~£10m of property) which were 100% vacant (and presumably part of the Capex to Core?) that equates to approximately one sixth of RGL’s irrecoverable costs (in 2025).

The Net Swing: By passing on a £700k cost and gaining a £1.075m income, this single deal represents a massive ~£1.78 million per annum positive annual swing for the company’s cash flow. Overall an estimated movement of around £3m at the half year.

Compared with £22.2m cash from ops in FY25 that’s a potential 8%-13% improvement to cash gen.

A Free £5 Million Property Upgrade

The announcement notes that the offices were rented in an “unrefurbished condition” and the tenant is spending £5 million of their own money on improvements.

Usually, landlords have to pay for expensive refurbishments to attract tenants.

Here, the tenant is footing the entire bill. This immediately increases the capital value of Regional REIT’s portfolio without Regional REIT spending a single penny.

1 & 2 Newstead are each listed as below £5m so that is approximately a 50% gain on the value of the property subject to valuation rules.

High-Quality Lease Terms

The structure of the 20-year lease is highly favourable to RGL:

Long-Term Stability: A 20-year lease is exceptionally long for modern office spaces, guaranteeing long-term income. While there are “breaks” (opportunities for the tenant to cancel) at years 10 and 15, securing at least 10 years locked-in is a great result.

Inflation Protection: The lease includes five-yearly RPI (Retail Price Index) rent reviews. This means every five years, the rent will automatically increase to keep up with inflation, protecting the landlord’s real returns.

Strong ESG Standing: Both buildings already hold an EPC B rating, which is highly energy efficient. This protects the landlord from looming, stricter environmental regulations that are currently forcing other landlords to spend millions retrofitting older buildings.

The Strategic Takeaway

The CEO’s commentary highlights a broader trend: because developers aren’t building new regional offices, there is a supply shortage.

Regional REIT is proving that even “raw,” unrefurbished office space is highly valuable if it’s in the right location (like right off the M1 motorway). By getting a manufacturing tenant to lock in for 20 years and inject £5m of their own capital into the buildings, Regional REIT has successfully de-risked these assets while significantly boosting their dividend-paying capacity.

Location, Location, Location – the Portfolio Breakdown

According to Regional REIT’s latest property and strategy assessments, approximately 80% of its portfolio is classified as being in the right location and meeting modern occupier preferences (or capable of being enhanced to do so).

With a total portfolio of 110 properties, I was curious as to the breakdown of what is in the “right location” versus what is being phased out is distributed as follows:

The Core Portfolio (~80% / approx. 90 properties): These are the high-quality assets located in major regional UK hubs outside the M25 motorway (such as the Nottingham offices mentioned in the update). These properties benefit from excellent transport links, strong regional tenant demand, and are being actively retained to drive long-term rent and capital growth.

The Non-Core Portfolio (~20% / approx. 20 properties): These are properties that no longer fit the “right location” or quality criteria due to structural shifts in the office market. Regional REIT is aggressively selling off these underperforming or non-core assets to reduce debt and reinvest capital into its core regional assets.

Analysis of Postcodes:

This was an interesting exercise. Analysis shows of RGL 112 properties (as at 31/12/25):

a/ 41 are within 0.5 miles of a railway station.

b/ 50 are within 1.5 miles of a Motorway Junction

c/ 21 are outliers i.e. neither of these. Let’s examine those.

c1. Regional High Street Retail Assets

A few assets are located deep inside historic regional town centers. Motorways are miles away and no railway station serves them, but they are close to the town’s primary shopping footfall, their specific physical entrances sit just outside our strict half-mile rail-station boundary:

27/29 King St, Belper (6.5 miles to M1 link)

Shrewsbury Arms Shopping Mall, Rugeley (9.8 miles to M6 Toll)

High Street/Bank Street, Dumfries (13.1 miles to A74(M))

c2. Deep Urban / Infill Corporate Offices

These are offices located in the suburban areas of major cities (like Leeds or Birmingham). Their nearest motorway junction is physically further than 1.5 miles away, and their walk to the central train terminal spans between 0.6 and 1.2 miles.

Trinity Court, Newport Road, Cardiff (3.8 miles to M4 / 0.6 miles to Cardiff Queen St)

31 Foleshill Road, Coventry (4.3 miles to M6 / 0.6 miles to Coventry Central)

Bennett House, Hanley, Stoke-on-Trent (3.8 miles to M6 / 0.9 miles to Stoke Station)

Global Reach, Cardiff (3.4 miles to M4 / 1.1 miles to Grangetown Station)

Northbank One, Sheffield (3.5 miles to M1 / 0.6 miles to Sheffield Station)

Albert Edward House, Preston (2.2 miles to M55 / 1.5 miles to Preston Central)

5 Temple Sq, Liverpool (3.5 miles to M53 / 0.7 miles to Lime Street mainline)

84 Albion Street, Leeds (1.9 miles to M621 / 0.6 miles to Leeds City)

c3. “Drive-To” Regional Business & Industrial Parks

These are large commercial parks positioned on regional A-roads. They capture local vehicular commuter workforces but aren’t proximate to a motorway.

Cyan Building, Rotherham (4.2 miles to M1 J36)

Fairfax House, Wolverhampton (2.8 miles to M54 J2)

Bering House & Timor House, Clydebank, Glasgow (3.4 miles to A82 / M8 link)

Tasman House & Caspian House, Clydebank, Glasgow (3.4 miles to A82 / M8 link)

Wilkinson Building, St Helens (3.9 miles to M57 J2)

Columbus House, Coventry (4.8 miles to M6 J3)

Eagle Court, Coventry Road, Birmingham (2.1 miles to M6 J6 / 2.5 miles to M42 J6)

Linford Wood Business Park, Milton Keynes (3.6 miles to M1 J14 / 1.2 miles to station)

Century Park, Altrincham, Manchester (2.8 miles to M56 J7)

Leo House, Wallington, London Periphery (5.4 miles to M23 J7)

The Whole List (this includes two disposed properties YTD – don’t know which those are)

Flagship Properties Valued £10m+

As can be seen below these are located attractively for transport. The “worst” in terms of distance Eagle Court which is on a dual carriageway a short way from the NEC.

Midrange £5m to £10m

The theme continues where few properties are not near transport links. The outliers tend to be retail/leisure and non-office therefore presumably part of the “Sale” cohort.

Finally the below £5m properties are generally also generally well located:

With nearly zero new office supply (compared with average new demand of 2m sq.ft per year) and a determination by the incoming PM for a “levelling up” (and some regions shall be more level than others?) who is better placed than RGL for this bounty of effort by the Labour Government from now until they’re gone in 2029?

RGL faces very little competition from new supply.

We’ve seen the transformative effect even just moving the BBC had back in the noughties on Media City Salford. Transformation indeed.

Conclusion

From zero to hero? Stranger things and an outlaw hiding in places like the motorway junction edge of Sherwood Forest, could be the start of the revival of the regions. The signs of recovery are already there even before Burnham coronated his way into his post.

The ERV per tenant, per property and per unit of RGL’s portfolio has been rising for a while too.

The Equivalent/Reversionary Yield too.

Buying RGL for 92p buys 328p of property where you owe a net -£1.30 a share to lenders (£1.98 NAV) and where even the unwanted property has been selling at or close to its book value.

Maybe I’m wrong, and this article is your sell signal. RGL could descend in flames. Some appear to want to believe that. Just like the airship Hindenberg which disastrously leaked hydrogen and crashed in flames.

I get that people dislike RGL. I get that there are those who claim there are “better quality” alternative REITs. But you pay handsomely for that quality. I’ve checked.

When you look at RGL assets, and consider the average 1% GDP growth, things are not going as bad as the media would portray. The interventionist Labour government will likely be a tailwind for RGL. However you feel about that, in my opinion it is the way the wind is blowing.

RGL is, I believe, another of these and yes in the recent past RGL raised money and diluted shareholders and has a poor track record, you can point the finger at management, blah de dah de dah. The point is it’s now 2026. It’s just 92p a share. They have refinanced debt, reset the dividend, paid out £70m of dividends over the past 3 years, on a mar cap of £150m mind you. RGL debt is today much more under control (and falling) and the upside potential for well-located offices and a capex program driving EPC A and B upgrades and demand for upgraded regional offices is growing too.

Here’s a final thought: Two years ago post dilution, RGL was at 140p a share. Compared with its former self as at July 2024, the July 2026 version of RGL is over 40% cheaper…. fitter and leaner, but also unjustifiably cheaper, given its improving outlook.

Regards

The Oak Bloke.

Disclaimers:

This content is for educational and informational purposes only. It does not consider your personal circumstances and is not financial, investment, tax, legal, or professional advice. Nothing here is a recommendation, offer, or solicitation to buy, sell, or hold any investment.

Leave a Reply