Sequoia Economic Infrastructure Income (SEQI) 17 July 2026

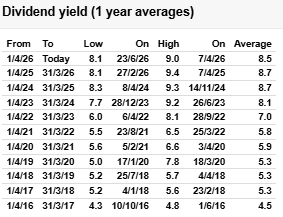

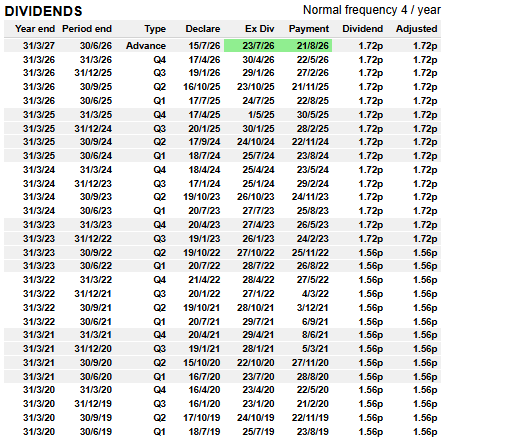

SEQI’s dividends are being held in a world of otherwise falling cash and bond yields.

Sequoia Economic Infrastructure Income (SEQI) generates a very high yield (8.2% at the time of writing) by lending money to infrastructure projects, from roads, railways and ports, through to data centres, renewable power generation and broadband networks. Its loans are heavily backed by real assets, with an average loan-to-value of 68%, and made to borrowers which typically receive steady and contractual cashflows, spread across a broad variety of sectors and geographies to provide diversification.

Over the last year the discount has steadily marched in, but remains in double digits at 10.1%. Despite cuts to base rates in the UK, US and EU over the past few years, SEQI has held its dividend target for 2027 where it has been since 2023. With the board committed to a significant buyback programme, and with the prospect for rates to fall further in this cycle, we think yield and the Discount are increasingly attractive.

In order to broaden the geographical diversification and take advantage of the growing opportunities in private debt in Asia-Pacific, the board is proposing to amend the investment policy to allow up to 30% to be invested in that region and 10% in other jurisdictions (including Canada and Latin America), so long as the country of origin is in the OECD or has an investment grade credit rating. There is no intention to alter the current defensive, cautious approach to lending, or make a dramatic near-term re-allocation to Asia, but the change should bring SEQI’s policy into line with the rapidly developing market for opportunities in developed jurisdictions such as Japan, Korea or Singapore (in addition to Australia and New Zealand, where SEQI has previously invested), in which major infrastructure private equity managers are making investments in sectors such as digitalisation and energy transition.

Analyst’s View

SEQI looks to us to have a clear path to a sustained discount narrowing. While there was some uncertainty around the path for interest rates when the Iran conflict broke out, it now seems like rate cutting cycles will be resumed. As yields on cash and government bonds come down, and with spreads in the corporate debt market looking narrow, we would expect SEQI’s yield to look ever more attractive to income-seeking investors.

While the term ‘private debt’ is being bandied about negatively in the press at the moment (especially regarding US credit funds’ exposure to sectors such as software), as we discuss below, we think SEQI is a very different proposition to the US funds that have run into trouble, and there is no more natural read-across than there would be in the equity space from, for example, a geared, small-cap tech fund to a large-cap defensive infrastructure fund. Since the GFC, private credit has become a diverse and well-established asset class, with SEQI’s planned expansion into Asia-Pacific markets highlighting its continued growth. Just because some private debt funds have run into trouble, doesn’t mean the space should be rejected, any more than poor returns in some equity funds mean equities should be rejected.

We think the diversification in the portfolio, along with the high backing by real assets and regular turnover of the investments (with a short average life of less than 3.5 years) all speak to the prudent, low volatility source of this very high yield. There is no free lunch in investing, and for SEQI stock-specific risk has to be borne in mind, as does the potential for single loans to run into trouble, but the track record of the management team is encouraging in handling these situations.

Bull

- High dividend yield from ungeared portfolio with relatively low credit risk

- Strong technical picture with withdrawal of banks from the sector and few competing funds

- Specialist team with many years of experience in this space pre-SEQI launch

Bear

- Falling interest rates will create a challenge to maintain the yield

- Unfamiliar asset class which is less transparent to the average investor

- Sentiment to the shares may be negatively affected by private debt problems in the US, although we think there is little read-across

Leave a Reply