2 Hidden High-Yield Gems That You’ve Likely Never Heard Of

Rida Morwa

Investing Group Leader

Summary

- Wall Street is busy chasing the loudest stories, while some high-quality income investments continue quietly rewarding shareholders.

- We highlight two overlooked dividend payers with durable cash flows, resilient business models, and the ability to continue generating dependable income through market volatility.

- We are building wealth, one dividend at a time. Check out our top picks with +6% yields.

- Looking for more investing ideas like this one? Get them exclusively at High Dividend Opportunities.

Co-authored with Hidden Opportunities

The best things are often the least obvious and sometimes less known or less advertised.

I recently visited Toronto and went to Añejo Restaurant in Downtown. The reason for the choice of restaurant was that my wife was craving Tres Leches, and this was the only place nearby that featured it on the menu, according to Google. Google also seemed to tell us that Añejo is a popular spot, known for its lively atmosphere, drink selection, and tacos. During my visit, I got the sense that this is the kind of place you’d visit if you were looking for a fun night out. We were there only for a specific dessert; we had already finished our dinner elsewhere.

Now, Añejo’s Tres Leches is different. On the physical menu, it said “lemon cake”, “dulce de leche,” and “candied lemon,” and I told my wife, “This may not be what she was craving,” but she agreed to give it a try.

We received a slightly unconventional take on the popular Latin American dessert, but it was much better than the original. It was not flashy or heavily promoted and certainly not the reason most people walk through the door (in fact, the waitress appeared a bit disappointed when we only ordered two of these desserts and did not go with anything on their popular drinks menu). Yet, it ended up being extremely delicious and easily became the most memorable part of our trip.

That’s often how it works. The things that deliver the best value aren’t always the ones that get the most attention. They sit quietly in the background, overlooked, underestimated, and underappreciated. Investing is no different.

While headlines chase the loudest names and the most talked-about opportunities, some of the best income-generating investments remain largely unnoticed, quietly doing their job, quarter after quarter.

Today, we’re going to look at two such opportunities.

Pick #1: KRC – Yield 6.3%

Readers often ask how large our portfolio is since we discuss some ideas every day. Portfolio management is an art; it requires careful analysis not only at the time of buying but also periodic updates based on business performance. This due diligence is reserved for members of High Dividend Opportunities, and as such, we don’t normally share our Buys and Sells.

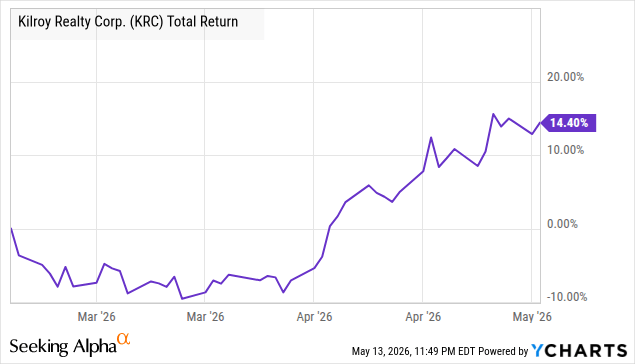

Kilroy Realty Corporation (KRC) is one such company we have never publicly discussed but have covered several times within HDO since our purchase a couple of months ago. KRC is an internally managed REIT that develops, acquires, and manages office, life science, and mixed-use property types in Los Angeles, the San Francisco Bay Area, Seattle, and Austin. KRC is the 46th largest property REIT in the United States by market cap, with a portfolio of 123 buildings, leased to 438 tenants, and a portfolio occupancy of 77.6% as of March 31, 2026. In addition, KRC also has 608 residential units in San Diego, with an occupancy of 95% as of March 31, 2026. KRC stock is up ~15% since we began buying, and this equity REIT has a lot more to deliver as we look ahead.

Strong Leasing Activity

During Q1, KRC reported record leasing activity, totaling 568K sq. ft. About 40K sq. ft. of the leases were on previously vacant properties, while 80K sq. ft. was new leasing on occupied spaces. Leases for 82K sq. ft. were renewed.

Asset Dispositions and Acquisitions

During the quarter, KRC sold $350 million in non-core properties, and management noted having used the proceeds from asset disposition towards debt repayments and share repurchases. In April, KRC repaid the $50 million of its 4.300% Private Placement Senior Notes Series A due July 2026, at par. During the quarter, the REIT purchased 2.4 million shares of common stock for $72.7 million.

In February 2026, KRC entered into a Joint Venture, by acquiring a 97% ownership interest in a land site in Downtown Redwood City, supporting a 251K sq. ft. office building. Construction will commence in 2027 and will cost $330 to $350 million, and the project is 58% pre-leased via a 20-year lease with a leading global law firm—Cooley LLP—for 145K sq. ft. Management expects delivery to be in 2030.

Operating Results & Enhanced Guidance

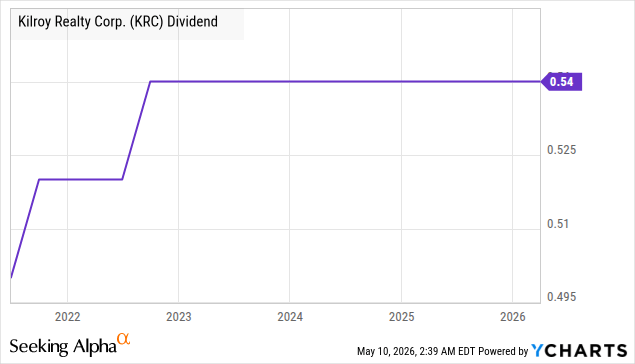

Q1 2026 revenues were relatively flat YoY at $270.1 million, while FFO (Funds From Operation) dropped to $108.8 million ($0.91/share). As originally guided, KRC’s net occupancy levels and FFO will be lower in 2026 due to KOP2 (Kilroy Oyster Point Phase 2) being added to its square footage, largely unoccupied but incurring costs. Excluding the new development at KOP2, the REIT’s occupancy was 81.5% with 84.3% leasing as of March 31, 2026. Management shared their upgraded guidance for 2026, expecting FFO between $3.49 and $3.63 (from the previous range of $3.25 to $3.45). This places KRC’s $2.16 annual dividend at a modest 60% payout ratio.

KRC continues to invest in high-quality assets, and as these developments move through the buildout phase, we are seeing a temporary YoY dip in operating metrics. This is part of the value creation process, not a sign of deterioration. Meanwhile, investors are paid to wait. The dividend remains well-covered and steady, allowing us to collect steady income while today’s capital investments position the company for future FFO growth.

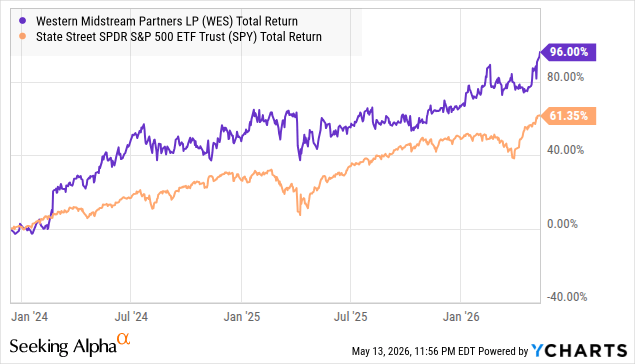

Pick #2: WES – Yield 8.2%

In our February article on Western Midstream Partners, LP (WES), we noted that management was eyeing accretive acquisitions as part of its capital allocation in 2026.

WES’ capital allocation plans also indicate potential pursuit of accretive acquisitions in 2026, similar to the Aris transaction, for inorganic growth and asset expansion. – HDO, February 27, 2026

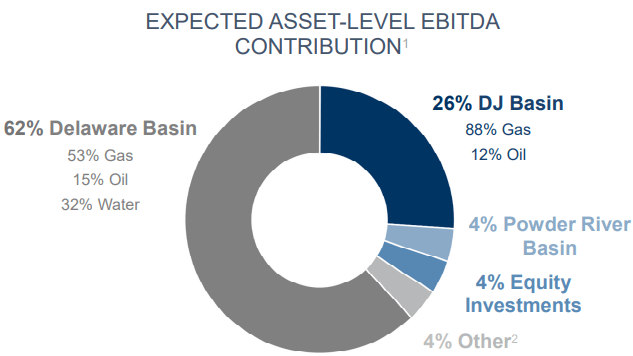

We didn’t have to wait too long to find out more. On May 6, WES announced the agreement to acquire Brazos Delaware II for $1.6 billion. Brazos Delaware is one of the largest privately held gathering and processing platforms in the Texas-Delaware Basin. It owns and operates ~900 miles of pipeline and 460 Mcf/d natural gas processing capacity. The transaction will involve $800 million in cash and $800 million in stock and is expected to close towards the end of Q2 2026. In 2025, WES generated ~62% of its Adj. EBITDA through its operations in the Delaware Basin. Source

This proportion is expected to rise after the Brazos transaction closes, supplemented by the completion of the Pathfinder Pipeline and North Loving II in 2027. We will note that Brazos comes with long-term contracts with a weighted-average life of over 9 years and with its top seven customers (leading energy names in the U.S. like ConocoPhillips, Exxon Mobil, Diamondback Energy, etc., accounting for ~80% of total volumes).

WES has been one of our strongest performers since we added it to the HDO model portfolio in December 2023. The partnership delivered three distribution raises and market-beating total returns through our ownership, and there is a lot more of it as we look ahead.

During Q1, WES generated a record Adj. EBITDA of $683.1 million, a 15% YoY increase, as a result of a full-quarter contribution from the Aris acquisition. Higher commodity prices towards the end of Q1 and a 7% reduction in operation and maintenance expenses provided further tailwinds. WES reported record crude oil (4% YoY) and NGL (6% YoY) throughput in the Delaware Basin, while produced water throughput reached 2,795 MBbls/d (a 140% YoY increase primarily driven by the full quarter contribution from the Aris acquisition).

From a balance sheet standpoint, WES paid down $440.5 million of senior notes due 2026 with proceeds from the senior notes issued in the fourth quarter of 2025 ($600 million of senior notes due 2031). The company ended Q1 with liquidity of over $2.6 billion and maintains an investment-grade BBB- balance sheet.

WES management has raised its 2026 guidance and expects Adj. EBITDA between $2.50 billion and $2.70 billion and Distributable Cash Flow between $1.85 billion and $2.05 billion, while affirming its CapEx between $850.0 million and $1.00 billion.

Last month, we predicted that WES would raise its distribution soon to $0.93/share, and they did. The partnership recently issued a 2.2% increase to its quarterly distribution to exactly $0.93/share, representing a forward yield of 8.2%. WES is growing organically and inorganically and continues to fully fund its pursuits, in addition to paying a growing distribution to shareholders. The stock offers an 8.6% yield and continues to present an excellent opportunity for income investors.

Conclusion

The most memorable experiences often come from the least expected places. Similarly, some of the best income opportunities are likely the ones quietly operating outside the spotlight.

Wall Street often focuses on what is exciting and trendy. Income investors, however, are paid to focus on what works, quietly. Our two picks discussed in this article, KRC and WES, will never dominate headlines, but both continue to quietly generate steady cash flow and reliable income. This is how we build wealth at High Dividend Opportunities, quietly, one dividend at a time.

Leave a Reply