Let’s Talk About Seeking Alpha’s Favorite Preferred ETF: PFFA

Jun 26, 2026, 12:11 PM ETVirtus InfraCap US Preferred Stock ETF (PFFA)PFF, OXLC, ECC

Summary

- Virtus InfraCap U.S. Preferred Stock ETF targets income investors seeking high recurrent yield via active management and leverage.

- PFFA has outperformed passive peer PFF in total returns due to higher distributions, but both funds exhibit negative price returns and capital erosion.

- PFFA’s current distribution exceeds its 30-day SEC yield and recent net investment income, signaling unsustainable payout levels and elevated risk of future cuts.

- Management’s incentives may not align with investors, as high yields attract assets and fees even when distributions outpace fund earnings.

- Looking for a portfolio of ideas like this one? Members of The Dividend Kings get exclusive access to our subscriber-only portfolios.

When it comes to retirement, investors love to have a steady stream of expected income pouring into their bank accounts.

Seeking Alpha seems to be a home to the largest community of income investors anywhere on the Internet. Looking at other investing websites, if you research dividends, you find a significantly greater focus on total returns than you do here on Seeking Alpha. Reddit, for example, has countless conversations regarding dividend investing but still focuses on lower yield, lower risk, and higher total return potential that seems to be the most popular with readers and Investing Groups on Seeking Alpha.

That’s because Seeking Alpha has effectively catered to this niche section of investors for the last decade. It should come as no surprise that the largest investment groups on Seeking Alpha also focus on this niche sector. They’ve grown together by focusing on this underserved population.

One key staple for income investors is the demand for high recurrent income. Preferred securities are a hybrid class of security that mixes both aspects of common equity and debt together. A common dividend cannot be paid before the preferred security dividend is paid, but missing a preferred dividend does not cause the company to go into default like a true debt instrument would. This middle ground allows preferred securities to have a higher yield than other forms of traditional debt but a greater degree of safety than common equity. That greater degree of safety, though, means that you are trading potential capital upside for higher recurrent income in the present. Preferred securities, however, are still not readily understood by many investors, and they will choose to sidestep investing in individual preferred securities and use exchange-traded funds instead.

Today, I want to look at one of the most popular exchange-traded funds for preferred securities on Seeking Alpha and discuss what it’s doing well, but also the brewing risks under the surface. If you’re an income investor and you love recurrent regular income that is potentially growing and hopefully not getting cut, then this may be a solid read for you.

Let’s dive in!

Hello Old Friend

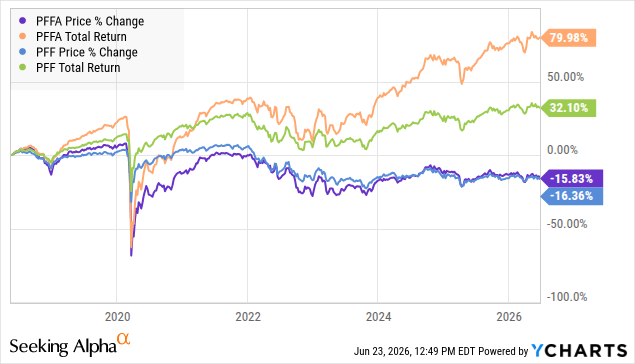

Virtus InfraCap U.S. Preferred Stock ETF (PFFA) is an actively managed leveraged preferred security ETF that aims to meet a niche investor population. From its inception, PFFA has readily outperformed the passive index tracking preferred security ETF, the iShares Preferred and Income Securities ETF (PFF).

PFFA has outperformed PFF by a margin of over 40% in total returns. However, when we look at the actual price change returns from PFFA’s initiation, both have similarly negative price returns. This means that while what you’re getting in your pocket is significantly more, your capital is eroding in value. PFFA does not provide more capital preservation than PFF.

The reason for this is that both of these ETFs simply buy and hold. PFF blindly follows the index as it changes and does so on a quarterly basis, selling and buying regardless of premium or discount to par.

PFFA relies on active management to try to outperform the index, leading to portfolio turnover rates of sometimes over 60% on an annual basis. It’s this increased portfolio turnover and their use of leverage that is designed to help fuel greater return potential. PFFA uses between 20-30% leverage in an attempt to boost returns. This adds greatly to the volatility the fund experiences over short periods, as leverage works like an amplifier of both positive and negative returns. It also boosts the expenses of the fund to 2.11%, with 0.8% being their management fee and the rest the cost of their leverage. PFFA pays out a much larger distribution but does so at the expense of any type of additional capital-preservation measures.

Clearly, PFFA is paying out more and providing a greater total return because all of the return that they have in excess of PFF comes strictly from the distributions that they make, and this is what predominantly attracts investors to PFFA.

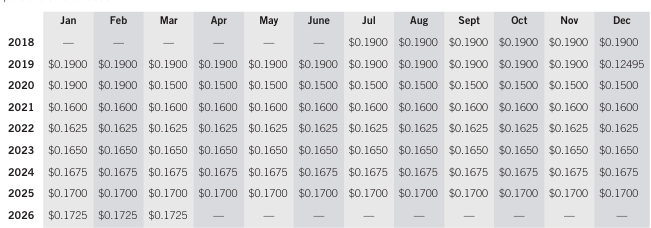

Over its lifetime, PFFA has had to cut its distribution only once. It has been raised multiple times, but never to its prior level. This means that original investors in PFFA are still receiving less each month than they received when they first invested in PFFA.

The key to remember is the fact that PFFA is not a preferred security investment by itself. You are investing in a fund that is actively managed using leverage and investing in preferred securities, and as such, you’re not going to receive the same level of income stability and security that you would from investing in individual high-quality preferred securities. You’re also going to receive potentially a significantly higher yield than you would from investing in those types of securities. You can find preferred securities offering anywhere from a 6-8% yield that is significantly lower risk and less volatile than you would find with PFFA, but you’re not going to benefit from the active trading activities of PFFA’s management team or the use of their leverage. So long as their management team can find excellent opportunities to achieve great returns, then you can expect the dividend to be consistent.

The risk is when environments are not favorable to their trading activity. When I last covered PFFA, I highlighted that if interest rates continued to drop, their ability to generate the high yield they’re providing would become strained. Thankfully, it looks as if interest rates are not going to be cut any further anytime soon, and there is a potential for interest rate hikes on the horizon if the economy remains strong and inflation remains high. There is a lot of gray in the outlook, and we only provide long-term outlooks to Dividend Kings members.

PFFA is currently not sustaining its present yield.

According to the fund’s own website, its present distribution rate exceeds that of its 30-day SEC yield. The 30-day SEC yield is a measurement of the fund’s current earnings over the last 30 days, subtracting any of the expenses the fund has incurred, and then expressed as a yield. This allows us to know if, in the last 30 days, the fund has readily achieved or covered its yield from the income, distributions, and capital gains that it has achieved over that timeframe. PFFA has not.

Furthermore, when we look into the fund’s history, we can see that they did not cover their yield for the annual period going from October 2024 to October 2025 either. The fund generated a net investment income of $98 million and realized trading gains of $32 million but paid out $148 million in distributions, overpaying by $18 million. These figures include any gains from their active trading and options trading.

This means that management was well aware they were overpaying when they hiked the distribution in 2026. The question remains how much they are willing to fall behind in their distribution coverage before they are either forced to do another cut or stop growing their distribution.

This is one major risk area when it comes to investing in funds versus buying the individual securities yourself. Fund managers are not necessarily aligned with you personally because they receive revenue tied to the size of the fund, and a high yield above what you can readily find in the preferred security space will attract more investors to invest in PFFA, thus growing their management fees. The management team is incentivized to overpay to maintain that higher yield. The fund itself attracted over $550 million worth of new investment in 2025, meaning that while assets under management are growing and the management fee is growing, even if the fund itself can’t afford the distributions it’s paying.

One does not have to look beyond Oxford Lane Capital Corporation (OXLC) or Eagle Point Credit Company Inc. (ECC) to understand the dangers of overpaying a distribution to attract investors to a high yield. Once the music stops, the damage falls out. Thankfully, PFFA is an ETF and cannot trade at the same extreme discounts or premiums that closed-end funds like Oxford Lane and Eagle Point Credit can. Over-distributing your earnings still leads to NAV erosion regardless.

Who Is PFFA For?

PFFA is designed to provide a high level of recurrent income today, even if that income isn’t covered by the net investment income and the capital gains of the fund itself.

This makes the fund extremely attractive to income investors who are not particularly concerned about overall total return or capital preservation. This goes against the very fundamental process that we follow in Dividend Kings.

We are focused not just on capital preservation but also on capital gains on top of the dividends we receive. PFFA works as a diversification tool to gain exposure to a wider array of preferred securities, but not as a replacement for individual preferred security holdings we have within our Model Portfolio. We can get a slightly lesser yield but significantly greater levels of capital preservation and capital gains from our own investing activity, just like you can by investing in high-quality individual preferred securities.

One should not accept a fund manager overpaying the distribution to attract new investors to enrich themselves at the expense of their own capital eroding over time.

This is the dichotomy that exists within PFFA. It vastly outperforms the standard index while duplicating its fundamental flaw. On one hand, investors receive wonderful and strong income in the present from it. But on the other hand, you’re accepting that the capital you’re putting in there is going to be eroded because of the misalignment that management has with shareholders.

I can already hear some of you jumping to the comment section to disagree with me and say that Jay Hatfield, the portfolio manager, has readily said that he has a vast majority of his personal net worth invested in PFFA. That’s a great marketing tool for him, but you have to remember he doesn’t just receive the distributions that you do. He also receives the management fees from you. So he is willing to accept a 15% loss in capital value because he’s collecting significant sums of management fees on top of that as well.

PFFA also works well for investors who want exposure to preferred securities but still lack the basic understanding of how the sector works. It outperforms the passive index tracking PFF and provides a similar level of capital preservation. It does. This means that if you are looking to just use an ETF to meet your needs in this sector, PFFA is a no-brainer choice compared to PFF. I would encourage you, though, not just to stop there, but to gain a personal knowledge base and exposure to how preferred securities work and your own personal risk tolerance so that you can use PFFA as a temporary base to springboard into the deeper pool of understanding.

Conclusion

PFFA is designed to meet a particular niche desire that is extremely popular on Seeking Alpha, if not elsewhere on the Internet. Investors who are looking for strong income opportunities can use PFFA to meet that income desire while accepting that it is not going to provide any greater degree of capital preservation than PFF.

Individual investors would tremendously benefit from learning how to invest in individual preferred securities on their own, whether they seek out that knowledge through articles on Seeking Alpha, other places on the Internet, or the Preferred Security Primer within Dividend Kings.

You can generate a similar yield with a higher degree of capital preservation as a manager of your own portfolio, completely aligned to your own goals. The biggest issue when investing in a fund is recognizing that management is not strictly aligned with your benefit but benefits from growing the fund, even if it is at your expense.

Over the long term, PFFA has outperformed PFF and provides an easy exposure to preferred securities for novice investors, retirees, and those seeking a higher degree of recurrent income and potentially less capital risk than investing in common equity or debt. However, investing in preferred securities is a tradeoff. You receive higher yields now and less potential capital gains in the future.

The current environment gives some positive room for PFFA. If management effectively benefits from the unchanged interest rates we’re seeing right now by trading into those holdings that will benefit from the potential hikes in the future, then the distribution may be covered in 2026 when it wasn’t in 2025. The risk is that management gets caught flat-footed and they’re not able to adjust, or they make the wrong call. If they move into more floating-rate securities and interest rates decline, their holdings and their revenue will fall. If they move into fixed-rate holdings and interest rates are hiked. They may again see the same issue.

With a high turnover ratio, management does not regularly hold positions for long periods, unlike most preferred security investors. I don’t expect management to cut the distribution in the near term. They may be forced to in the long term because of overpayment. In the short term, it is too effective as a beacon to draw in new capital. I would not hold my breath for any sort of large distribution hike from them, given the fact that they are knowingly overpaying already. As long as the yield is attractive to investors and capital keeps pouring in, then the distribution will stay put.

Leave a Reply