Why Interest Rates Matter to Fund Investors

We live in an age when investors are obsessed with central bankers’ actions and words. To cut or not to cut seems to be the question on everyone’s mind. In truth, investors have always been worried (and excited) about macroeconomic policy, but the current environment is especially focused on rate decisions. We unpack the importance of interest rates for investors in a simple ten-step way.

By David Stevenson•05 Sep, 2024

Over the last few months, stock markets have zig-zagged up and down based on worries about interest rates, especially in the U.S. – remember that U.S. stocks overwhelmingly dominate global equity markets. Last week, the first major signs of the much-anticipated interest rate pivot emerged. The Federal Reserve chair Powell observed,

“Overall, the economy continues to grow at a solid pace. But the inflation and labour market data show an evolving situation. The upside risks to inflation have diminished. And the downside risks to employment have increased. As we highlighted in our last FOMC statement, we are attentive to the risks to both sides of our dual mandate. The time has come for policy to adjust. The direction of travel is clear, and the timing and pace of rate cuts will depend on incoming data, the evolving outlook, and the balance of risks. We will do everything we can to support a strong labour market as we make further progress toward price stability. “

In plain English – We are more worried now about rising unemployment than we are about surging inflation, which could imply a recession, so the time for interest rate cuts is fast approaching.

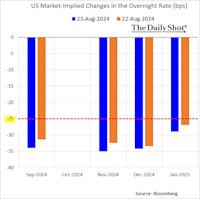

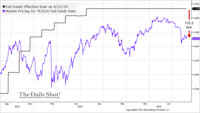

Within minutes of this gnomic declaration the market was pricing in a higher possibility of a 50 bps cut at each upcoming Federal Open Market Committee meeting. The next two charts show market reactions from a week or two ago via the excellent macro-economic news service, The Daily Shot.

Overall, investors are now pricing in 105 bps (1.05%) of rate cuts for this year. Personally,, I think that is a little overcooked, but the market is betting that the U.S. interest rate will be closer to 4% than 5%. And what starts in the U.S. will almost certainly apply to the UK— most investors now expect UK interest rates to stabilise somewhere between 4 and 4.5% by early 2025.

This all sounds terrifically exciting if you are a dismal economist – or potential mortgage applicant – but why does it matter to ordinary investors? As a market observer, I’m painfully aware that analysts and strategists get carried away with jargon and make bold assumptions about investors’ knowledge. For instance, it’s almost a given that investors join up all the dots about rate cuts, whereas my guess is that most investors only have the simplest understanding of why rate cuts matter.

To help bridge that gap, I thought I’d zip through ten reasons why investors should care about interest rate cuts. Forgive me if it’s a bit simplistic, but the point is simple – investors should care greatly about these cuts.

- Interest rates are a signalling device, telling markets what central bankers are worried about. Read that statement by Powell carefully, and it’s obvious he and his colleagues are growing more concerned about increasing unemployment and a weak labour market. That suggests the concerns of an economic slowdown in the U.S. are real and valid. That should concern investors because it suggests that central bankers are worried that the miraculous soft landing – much anticipated – might be replaced by a bumpy landing. That implies you should take seriously if you are a bond investor, the risks of increased corporate defaults (which have been steadily increasing for the last year). That means you need to demand a higher risk premium for lending to risky corporates.

- Declining interest rates are good news, by contrast, for indebted corporate borrowers, especially in the real assets (infrastructure and real estate) sector. These sectors are interest rate-sensitive, and thus, declining rates, all things being equal, should mean lower refinancing costs.

- Lower interest rates imply that central bankers are much less worried about surging inflation. There is still every chance that core measures of inflation might crawl back up again, possibly breaching the 3% before coming back down again. But the substantive point is that central bankers are NOT worried about a massive inflation surge pushing past 5% year on year. That might mean the inflation assumptions for many funds invested in real assets might have to be notched down again, which cut into revenue growth if they own inflation-linked assets

- Lower interest rates will reduce the implied real interest rate to more sustainable levels. I’ve already discussed in these articles why real interest rates (the nominal interest rate minus the market forecast for inflation rates in the not-too-distant future) have been heading steadily towards zero for decades but shot up in the last two years. Sustained positive real rates tend to slow down investment spending and generally hinder economic growth. Lower real rates – I guess they’ll stabilise at around 1% in the U.S. and the UK – might mean faster economic growth and improved capex spending. All in all, that’s good news for equities in general.

- Lower interest rates have another very important transmission mechanism via the risk-free rate, widely used in discounted cash flow models and investment trust NAV calculations. You will often see mention of net asset values calculated with reference to a discount rate. A real asset produces a stream of cashflows (rents, payments), which are then plugged into a forward-looking cash flow model. A number is generated representing the potential future value of those cash flows, but then it is discounted back using the risk-free rate. The risk-free rate is the return you could get from holding cash, i.e., it is risk-free, assuming you have bank guarantees. The lower the interest rate, the lower the risk-free rate, the lower discount and the higher the NAV. This risk-free mechanism will take time to work its way through to fund valuations – maybe as long as a year, but the impact should be positive.

- That lower risk free rate also has a wider impact across all asset classes. When savings rates and risk-free government bonds paid you 5% or more, many investors were reluctant to go all in for risky equities. 5% risk-free is a great return, and money flooded into money market funds. Cash savings and money market account returns will seem less attractive as rates decline. That, in turn, makes equities more attractive. Dividend-paying, higher-yielding equities might be particularly attractive, especially if the sustainable dividend yield is well above the risk-free rate, i.e. above 4 to 5% per annum.

- Lower interest rates in the U.S. make the dollar less attractive. Over the last few years, high U.S. interest rates – relative to Europe and Japan – have made the U.S. Dollar a desirable currency. The dollar index, which measures the dollar against a basket of currencies, has been historically quite high but has weakened in recent weeks. Even sterling has shown some strength in recent months, as has the Japanese yen. Overall, a weak dollar is good news for indebted emerging market economies and good news for gold. But a weaker dollar and a stronger pound is bad news for UK investors in U.S. equities.

- Central bankers have not entirely given up worrying about inflation, but interest rates are not their only mechanism for controlling the economy. They also run extensive balance sheet processes such as buying up bonds and, in Japan, ETFs. In recent decades, these activities have mushroomed into huge quantitative easing (QE) programmes worth hundreds of billions. Central banks have been keen to rein back in these programmes and have initiated quantitative tightening (QT) measures. That’s resulted in central banks quietly selling assets and marking up losses. These losses must be paid for by treasuries, crimping government spending programmes. Lower interest rates usually tend to go along with quantitative easing, i.e. central bankers are worried about increasing recession risks and flooding the market with bank cash. However, central banks are also keen to unwind those QE programmes via QT in the long term. The 64 trillion dollar question is whether QT will continue, which might crimp global liquidity and cause financial stress or retreat their QE programmes.

- Lower interest rates are also good news for indebted governments, including the U.S. and the UK. Lower debt costs help improve the government fiscal position as interest rate costs on gilts decline. However, that could be offset by the losses accumulated on past QE programmes, which are being passed on to treasuries (as noted above). It’s also worth remembering that much of government debt is fixed at long-term rates, so the immediate impact isn’t always direct. However, the UK government borrows heavily using inflation-linked gilts and shorter-term debt, and these costs will fall markedly, allowing the government more headway to spend more (or cut taxes). That’s a positive for the UK economy.

- Residential property markets are a significant driver of consumer spending-dominated economies like the UK. A huge wealth of data suggests that when house prices have stopped falling and are rising again, consumers feel wealthier and spend more. The same argument also applies to equity markets, i.e., when the S&P 500 surges in the U.S., wealthy Americans spend more. All things being equal, lower rates should help stabilise housing markets, even though most mortgage holders have locked in their rates for a few years. Again, that’s potentially great news for the domestic economy and thus corporate profits.

Leave a Reply