A 360 view of the latest results from EWI, BNKR, RICA

Frank Buhagiar

19 Jan, 2024

Contrarians of the week

“Many of the companies with the greatest potential to deliver change are ones the market is shunning. They’re seen as reckless pre-profitable companies, early in their lifecycle with the temerity to believe that things can be different from how they’ve always been. With the market reflexively punishing such companies and aggressively discounting their potential, those of us who believe in progress, long-term relevance and human ingenuity have become the contrarians.” Edinburgh Worldwide (EWI) Investment Managers.

A period of unprecedented scientific innovation and technological change

Final Results from Edinburgh Worldwide (EWI). Chair Henry Strutt opens his statement with a reminder of what the fund is all about: “The Company’s mission is to invest in innovative businesses that are developing next generation products and services. We are living through a period of unprecedented scientific innovation and technological change. Edinburgh Worldwide (‘EWIT’) is designed to provide investors, who are otherwise unable to access this dynamic asset class, a way to participate in the exciting developments we are seeing across a whole range of foundational technologies from biotechnology and gene sequencing, through aeronautics and space technology, automation and artificial intelligence to semi-conductors, data processing and energy transformation and storage. We have always believed that in order to take full advantage of these opportunities and access the potential for the outsized returns these could generate, requires a five-year investment horizon, and in many cases up to 10 years.”

Problem is: “The…pandemic…, geopolitical tension, the resurgence of inflation…and…aggressive central bank responses have all conspired to drastically shorten investors’ time horizons and increase risk aversive behaviour. These have in turn hit valuations of growth companies particularly hard, with a consequent knock-on effect on…portfolios such as EWIT’s…” How hard? “NAV…per share, when calculated by deducting borrowings at fair value, decreased by 23% and the share price by 27.7%. The comparative index, the S&P Global Small Cap Index…total return, decreased by 4.3% in sterling terms…” And yet, “The portfolio is invested for the most part in companies with solid finances and good economics as well as outstanding future potential. The majority have been performing well operationally and have strong cash positions…” So, the Board “…continues to encourage the portfolio managers to focus on smaller entrepreneurial companies, as we believe these are better able to deploy the best in human ingenuity and imagination to embrace disruptive technologies and processes at scale than larger companies who are inevitably hidebound by legacy practices and business models and layers of bureaucracy and hierarchy.”

Winterflood points out: “As at 31 October 2023, EWI held 14 private companies, accounting for 26.0% of total assets (31 October 2022: 14; 20.1%) vs limit of 25% as at time of investment…Over FY, the private companies saw 130 revaluations, resulting in -1.1% average decrease in share price.”

Numis adds: “We note that the number of portfolio holdings has reduced from 110 at October 2022, to 98 at October 2023, in part reflecting the sale of several lower conviction holdings. In addition, recent performance has improved, with the fund outperforming the index by c.5% post-period end, in part owing to expectations of lower interest rates, although we expect that expectations for rates is likely to continue to be volatile. For sentiment to improve, we believe the portfolio needs to deliver on operational milestones and deliver the growth that the manager is expecting to drive longer time value, independent of interest rates.”

Difference of the week

“I have rarely seen markets so narrowly focussed on a few winners where the decision to own one or two stocks has meant the difference in under or outperforming the index.” Bankers (BNKR) Fund Manager Alex Crooke.

Patient investors

An almost in line full-year performance from Bankers (BNKR). Chair Simon Miller reports a “…net asset value total return over the year ended 31 October 2023 of 5.2% (2022: -11.3%) just narrowly underperforming the FTSE World Index total return of 5.7% (2022: -2.8%) and a share price total return of -0.7% (2022: -13.4%).” The Chair goes on to remind investors that “The Board has long set a twin objective to grow capital and dividends.” However, “The US market is increasingly dominated by zero yielding stocks, which is causing problems for income investors, with five of the Magnificent Seven not paying a dividend. We therefore only own two of these seven companies. Other funds and in particular some in our peer group hold all seven and this is reflected in their performance this year. Our investment style has long focussed on those growth stocks that pay dividends. The size and scale of these companies that probably have little prospect of paying a dividend now means we need to be more flexible with revenue reserves to enable a broader investment pool.”

In terms of outlook, the Chair points out that “Equity markets have been driven higher by a small set of companies supported by investors’ enthusiasm for the transformative power of generative AI. In the rush to invest in the US and these few leaders, the vast bulk of quoted companies are trading on undemanding valuations and look attractively priced for patient investors, like ourselves.” Fund Manager Alex Crooke adds: “We have undoubtedly missed some opportunities in the US market through our preference for dividend paying companies. We intend to widen our focus in the coming year although we will maintain our preference for cash generative companies with well defended market positions. Our stock selection seeks to avoid the overvalued and under invested companies, prioritising higher quality and lower geared companies, offering earnings resilience.”

Winterflood notes: “Underperformance attributed to US underweight (index >68% US), particularly with respect to ‘Magnificent Seven’, as well as weakness in Asian markets, chiefly in China’s property market, which affected consumer sentiment. Share price TR -0.7%, as discount widened from 8.1% to 13.4%; repurchased 60.6m shares. Dividend for the year raised by +10.0% to 2.56p, compared with CPI of +4.6%, while revenue earnings return rose by +16.2% to 2.72p per share. Dividend growth of at least 5% expected in FY24…”

Comment from Numis: “Performance looks weak relative to global markets, with the NAV underperforming over the last three years, which has impacted the long-term performance record… The shares currently trade on a c.12.5% discount to NAV, and we note that this has remained around this level since a temporary pause in buybacks in mid-2023, which have since resumed. Bankers has typically been a low cost…way to access global equity markets, although we can understand if sentiment remains weak given the share price returns in recent years.”

JPMorgan is neutral: “BNKR’s has a strong long-term track record, is one of the larger global funds in the peer group (market cap £1,243m), has low ongoing costs (0.50%) and now trades at one of the wider discounts in its peer group (12.6%). It is making significant share buybacks which is also a positive. But we think an improvement in the relative NAV performance is likely required for the discount to significantly narrow. We remain Neutral.”

Reason of the week

“By far the most obvious reason to be bullish was that most investors were bearish.” Ruffer’s (RICA) Investment Managers Period End Review.

A second bite at the cherry

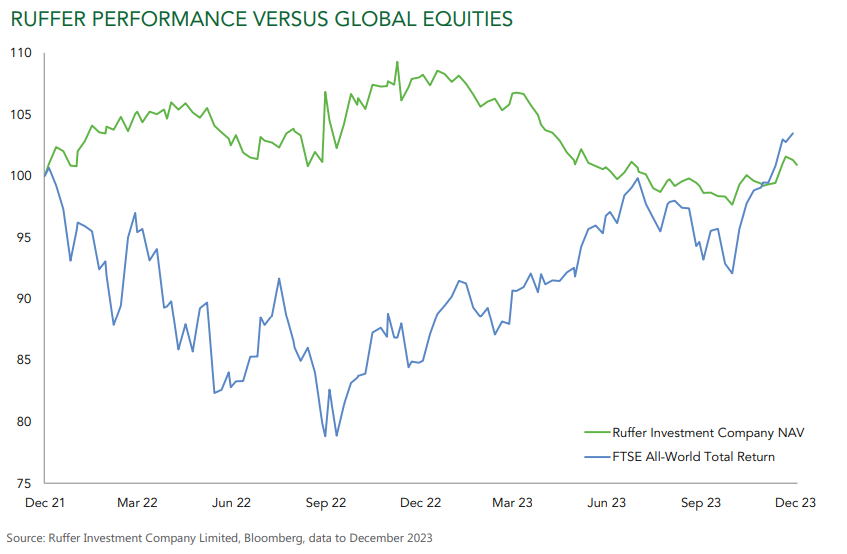

Ruffer’s (RICA) Investment Manager’s Review gets straight down to performance: “NAV TR…for the six months to 31 December 2023 was 0.6%…NAV TR for the calendar year to 31 December 2023 was -6.2%…The annualised NAV TR since inception of the Company in 2004 is 7.0%, which is in line with UK equities, behind global equities, but with a much lower level of volatility and drawdowns than both.” As the investment managers explain, something unusual happened to the fund early in 2023: “It isn’t often that we find ourselves positioned with the consensus, but at the start of 2023 our bearish positioning was not as contrarian as perhaps we thought. Most other investors were also cautious; we underestimated the ability and willingness of market participants to re-risk and re-leverage their portfolios when recession and liquidity risks did not emerge…There is no hiding from 2023 being a disappointing year, the worst in the history of Ruffer Investment Company. However, zooming out a little does provide some perspective, and shows a more balanced outcome. Taking 2022 and 2023 together, effectively the beginning of the Fed tightening cycle, the NAV TR of the portfolio is 1.3%. As seen in the chart below, global equities are also slightly positive over two years but with a very different journey which points to the usefulness of Ruffer as an uncorrelated diversifier and volatility dampener to multi-asset portfolios…”doceo360 ruffer 19.01.24

More from the investment managers: “What’s the lesson of the last couple of years? Some would say ‘HODL’ (hold on for dear life), ignore the noise, have a long-time horizon. We take a different lesson. 2022 gave a taste of what the new regime might look like. The illusion of diversification hurt portfolios with stocks and bonds positively correlated whilst falling, many alternatives were just duration in disguise. It’s no longer conjecture that conventional portfolios are insufficiently protected and diversified…Crucially, our philosophy of aiming to protect and grow capital in all market conditions remains unchanged, and we think the set-up for our portfolio from here is attractive…we have very differentiated positioning to protect against and prosper from the various scenarios we see, and the portfolio today holds powerful offsets which are now even cheaper and more interesting than they were a year ago. This gives investors a golden opportunity, we have seen what inflation volatility can do to portfolios and now we have a second chance to prepare. A second bite at the cherry.”

Numis is positive: “…recent performance has been challenging, and the fund lagged in the mega cap rally in 2023, with unconventional portfolio protections the largest drag on performance. The nature of the portfolio means that the NAV will inevitably lag if equity markets remain strong, but the managers express caution over the direction of travel in 2024. They expect inflation volatility to persist and are sceptical that the battle against inflation has been won. The managers have been active in making portfolio changes, which includes reducing duration through the sale of US TIPS, as well as removing exposure to Gold. The managers highlight attractive opportunities in the UK and Japan, as well as commodity stocks which they believe offer attractive risk premiums. We continue to believe that the fund can be regarded as a portfolio diversifier as Ruffer has an impressive record of insulating against market falls, most notably during 2022, Covid-19 and the global financial crisis. The fund traded on a premium in 2022 and early 2023, and was one of the largest issuers, but the shares have since moved to a discount (currently c.5%).”

Reassurance of the week

“Be assured that the steady progress of human ingenuity is very much alive and well.” Edinburgh Worldwide (EWI)

This article bursts with life and inspiration — beautiful!

You’ve got serious talent — this is spectacular!

Wow!! I’m honestly amazed by how good this was!

You write with such spark — I’m genuinely impressed!

I can’t stop smiling — this post made my day!

This lit up my whole mood — thank you for this!

You always deliver top-notch content — keep it up!

This was a total joy to read — loved every second!

Thank you for expressing this so clearly.

I learned so much from this one article.

You communicate ideas better than almost anyone else I follow.

I learned more from this than from many other blogs combined.

Comment 69: This blog post is truly outstanding and provides such a

refreshing depth of insight. I found myself fully engaged from start to

You’ve created something vibrant and exciting — amazing job!

Your writing is a powerhouse of enthusiasm — great job!