JLEN Environmental Assets – Vote against discontinuation

- 18 July 2024

- QuotedData

Vote against discontinuation

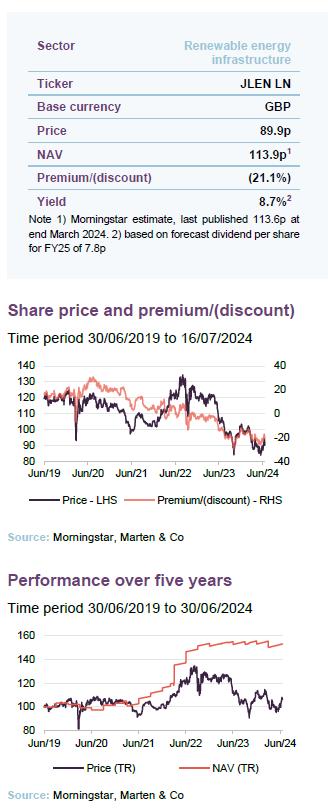

JLEN Environmental Assets (JLEN) and the wider renewable energy infrastructure sector have traded at a persistently wide discount with investor sentiment continuing to wane. This has triggered the activation of a discontinuation vote at JLEN’s AGM in September. We strongly believe shareholders should vote against discontinuation, taking into account the strong long-term track record of the company, which has produced NAV total returns of 119.5% since its launch just over 10 years ago to the end of June and delivered dividend growth every year.

The fundamental growth story for the sector remains as strong as ever, with investment in the energy sector continuing to swell – the majority of which is going to clean energy technology such as renewables, low carbon fuels, nuclear, grids and battery storage.

Progressive dividend from investment in environmental infrastructure assets

JLEN aims to provide its shareholders with a sustainable, progressive dividend, paid quarterly, and to preserve the capital value of its portfolio. It invests in a diversified portfolio of environmental infrastructure projects generating predictable wholly or partially index-linked cash flows. Investment in these assets is underpinned by a global commitment to support the transition to a low-carbon economy and mitigate the effects of climate change.

Fund profile

JLEN invests in infrastructure projects that use natural or waste resources or support more environmentally-friendly approaches to economic activity, support the transition to a low carbon economy, or mitigate the effects of climate change.

JLEN’s assets are broadly categorised as intermittent renewable energy generation, baseload renewable energy generation and non-energy-generating assets that have environmental benefits. Intermittent energy generation investments include wind, solar and hydropower. Baseload renewable energy generation investments include biomass technologies, anaerobic digestion and bioenergy generated from waste. Non-energy-generating projects include wastewater, waste processing, low carbon transport, battery storage, hydrogen and sustainable solutions for food production such as agri- and aquaculture projects.

JLEN aims to build a portfolio that is diversified both geographically and by type of asset. This emphasis on diversification reduces the dependency on a single market or set of climatic conditions and helps differentiate JLEN from the majority of its peers, which tend to specialise in solar or wind.

Reflecting its objective of delivering sustainable, progressive dividends and preserving its capital, JLEN does not invest in new or experimental technology. A substantial proportion of its revenues is derived from long-term government subsidies.

JLEN’s AIFM is Foresight Group LLP (Foresight). Foresight is one of the best-resourced investors in renewable infrastructure assets, with £12.1bn of AUM as at 31 March 2024. This includes Foresight Solar Fund, which sits in JLEN’s listed peer group. Foresight has a highly experienced and well-resourced global infrastructure team with 175 infrastructure professionals managing around 4.7GW of energy infrastructure. It is a global business, with offices in eight countries. The co-lead managers to JLEN are Chris Tanner and Edward Mountney.

Annual results

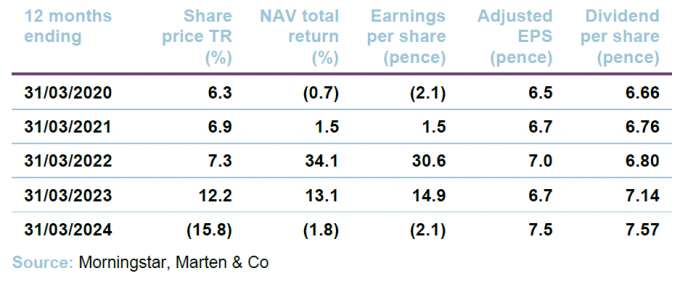

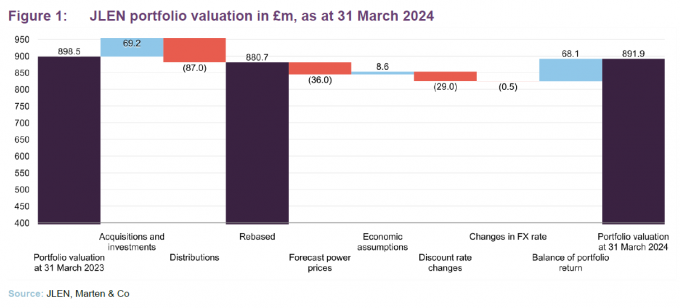

In annual results announced last month, JLEN reported a total NAV of £751.2m or 113.6p per share at 31 March 2024 – a 7.7% fall over the year. This equated to a NAV total return of -1.6% including dividends of 7.57p (which were 6% up on the prior year). JLEN’s NAV total return since IPO is 115.9% (8.0% annualised).

Cash from projects at record high underpinning the dividend

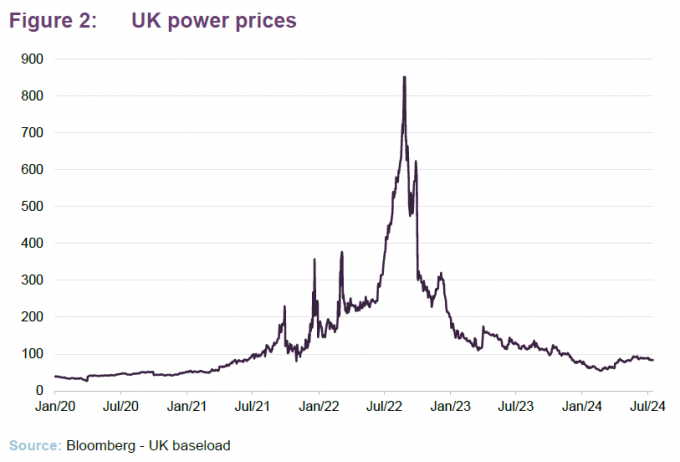

Distributions received from projects were at a record high of £87.0m (2023: £83.6m) and underpinned the dividend with a coverage of 1.3 times. The value of the portfolio fell £6.6m over the period, as shown in Figure 1, due mainly to changes in power price and discount rate assumptions, offset by underlying growth in the portfolio.

Discontinuation vote

As with many of its renewable energy and infrastructure peers, JLEN’s shares have been trading at a wide discount since interest rates ballooned in 2022. With the discount having averaged more than 10% in the financial year, a discontinuation vote has been triggered, which will take place at the company’s AGM in September.

Somewhat counterintuitively, shareholders should vote against the resolution if they want the company to continue. We believe this is the course investors should take, given the strong long-term track record of the company (see page 15), including delivering dividend growth every year since its launch 10 years ago (see page 19 for the dividend section).

Change in name and cut in management fee proposed

A reduction in the investment management fee will come into effect from 1 October (see page 21 of this note for details), while the board has proposed to shareholders a change in name of the company to Foresight Environmental Infrastructure – to reflect the fact that it has been five years since Foresight acquired the management team of John Laing (which informs the current name). The board states that it has assessed the benefits available through a closer association with the investment manager – including the scale afforded by its broader marketing initiatives and strong market reputation – and believes that there are clear commercial benefits to renaming the company. Should shareholders approve the proposed change of name, the board is recommending the company’s ticker change to FGEN and its website address switch to FGEN.com.

Market backdrop

The timing and pace of the impending interest rate cutting cycle is unknown, but the general consensus seems to be that the first rate cut in the UK will come in August – despite inflation falling back to the Bank of England’s target 2% in May. The first downward move in the base rate will be an important moment for many sectors, not least renewable energy infrastructure, where the higher interest rate landscape has put a substantial downward pressure on NAVs and, even more so, investor sentiment.

A general acceptance that the eventual pace of cuts is likely to be slower than first thought, plus the impact of falling inflation on cash flows from energy-generating assets and continued geopolitical instability, has seen discounts across all infrastructure companies remain persistently wide.

Estimated $2.8trn invested in energy sector in 2023, the majority of which aimed at clean energy technology

However, the fundamental growth story for the renewable energy infrastructure sector and JLEN remains as strong as ever, with the green agenda an urgent priority of most global governments. The International Energy Agency (IEA) has estimated that investment in the energy sector amounted to $2.8trn in 2023, of which more than 60% was invested in clean energy technology such as renewables, low carbon fuels, nuclear, grids and battery storage.

There seems to be political support across the benches for boosting clean energy capabilities in the UK and in Europe (key markets for JLEN), despite the recent European Union elections. The new Labour government in the UK has pledged to ‘make Britain a clean energy superpower’ and has vowed to work with the private sector to double onshore wind, triple solar power, and quadruple offshore wind by 2030, while also investing in carbon capture and storage, hydrogen and marine energy to ensure the country has the long-term energy storage it needs. This is in contrast to the US, where a Trump administration seems likely to scrap the Inflation Reduction Act (IRA, which has worked well in incentivising investment in green technology).

JLEN’s diversified portfolio and the manager’s strong track record and expertise in the sector seems completely at odds with its current discount of 21.1%. JLEN’s board has set out its approach to capital allocation, which includes prudent management of debt and consideration of share buybacks if they are NAV accretive. We explore the factors impacting JLEN’s NAV in detail below, beginning with power prices.

Power prices

Despite having already fallen steeply from highs seen in 2022, electricity prices continued to fall further and faster than anticipated over the last year, as shown in Figure 2.

The overall change in forecasts for future electricity and gas prices compared to forecasts at 31 March 2023 negatively impacted JLEN’s NAV by £36.0m or 5.4p in the year to the end of March 2024.

Fixed prices secured on the majority of portfolio

JLEN looks to de-risk its exposure to volatile market prices and has fixed prices for the majority of its output. At 31 March 2024, the portfolio had price fixes secured over 61% for the Summer 2024 season and 58% for Winter 2024/25 season. Short-term market forward prices for the next two years are used to value the portfolio where contractual fixed price arrangements do not exist. After the initial two-year period, the project cash flows assume future electricity and gas prices in line with a blended curve informed by the central forecasts from three established market consultants.

Based on the portfolio at end March 2024, a 10% fall in power prices over the remaining life of JLEN’s assets would take off £37.4m or 5.7p from the NAV and a 10% increase would add £37.0m or 5.6p to the NAV. Even though the last months of the previous year had already seen electricity prices fall sharply from the highs seen during the energy crisis in 2022, electricity prices continued to fall further and faster than anticipated. In the year to March 2024, power prices reduced by a further £40/MWh – equivalent to approximately 40%.

JLEN’s manager states that in the extreme event that electricity prices fall to only £40/MWh, the company would maintain a resilient dividend cover for the next three financial years.

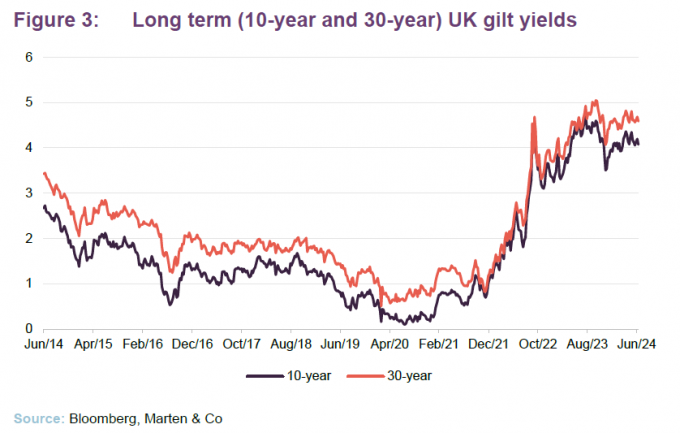

Discount rates

Gilt yields have remained at an elevated level for almost two years, as shown in Figure 3. Government borrowing costs rose sharply from the beginning of 2021 and accelerated in the fallout from the ‘mini budget’ of September 2022 and have remained elevated since.

The weighted average discount rate now sits at 9.4%

JLEN’s weighted average discount rate has remained unchanged over the six months to 31 March 2024 at 9.4%. This is 100bps higher than a year prior due to an upward movement in the discount rate applied in June and September 2023, reflecting the sustained increase in UK gilt yields as well as continued investment into JLEN’s ongoing development and construction projects (which are valued using higher discount rates to reflect the development risk). However, the discount rate was reduced on some construction projects that achieved key milestones during the year.

The overall uplift in discount rate over the year took £29.0m off the NAV.

The discount rates that are used in the discounted cash flow calculations that inform the NAVs of many alternative assets funds, including those in the renewable energy sector, can be broken down into the risk-free rate – derived from the yield on a government bond with equivalent duration – plus a risk premium. The risk premium element of the discount rates calculation is influenced by various factors including the composition of the portfolio and investors’ risk appetite for these sectors and projects, based on recent comparable market transactions.

An independent verification exercise of the methodology and assumptions applied in JLEN’s NAV calculation is performed by a leading accountancy firm and an opinion provided to the directors on a semi-annual basis.

Inflation

Inflation assumptions upgraded slightly

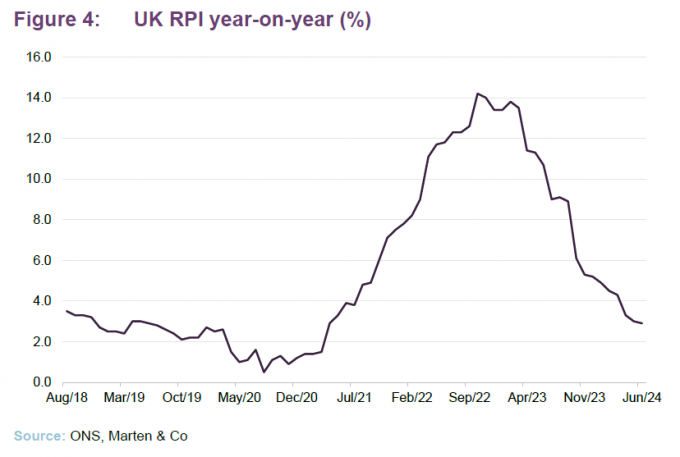

62% of JLEN’s forecasted revenues are contractually linked to inflation (as measured by the RPI) through government-backed subsidies and long-term contracts. An uplift in inflation assumptions used to value JLEN’s portfolio (based on actual data and independent forecasts) to 3.5% RPI inflation for 2024 (from an assumption of 3.0% at 31 March 2023) – reverting to 3% until 2030, and then falling to 2.25% thereafter – resulted in an overall increase in value of £8.6m.

Figure 4 shows that RPI inflation fell to 2.9% in June 2024. JLEN’s sensitivity to changes in the inflation rate is about +£19.3m or 2.9p on the NAV for every 0.5% increase in the forecast inflation rate and a decrease of £18.9m or 2.9p on the NAV if rates were reduced by the same amount.

Useful economic lives

The assumption JLEN uses for the useful economic life of investments is the lower of lease duration and 35 years for solar assets, 30 years for wind farms and 20 years for anaerobic digestion (AD) facilities – being the life of the RHI subsidy. JLEN applies a conservative valuation in regard to its AD assets, with the assumption that the facilities will simply cease to operate beyond the life of their RHI tariff. The manager says that it has seen a growing case of evidence, including several transactional datapoints, pointing towards a positive change in market sentiment for valuing these assets – including the potential to run anaerobic digestion facilities on an unsubsidised basis.

In light of this change, the manager has provided a sensitivity extending the useful economic lives of its AD portfolio by up to five years – capped at the duration of land rights already in place. Such an extension would result in an uplift in the portfolio valuation of £21.9m or 3.3p.

Taxation

As we discussed in more detail in previous notes (links to which can be found on page 24), the UK government introduced a temporary windfall tax on electricity generators – the Electricity Generator Levy (EGL) – in response to higher energy prices. JLEN’s wind, solar and biomass assets are affected by the levy, which saw the government take 45% of revenues above a price of £75/MWh from 2023 to April 2024, and thereafter adjusted each year in line with inflation (as measured by CPI) on a calendar-year basis until the levy comes to an end on 31 March 2028. JLEN paid £5.5m on the EGL tax in the financial year, with the annual liability for the 2025 financial year estimated to be lower, reflecting the drop in power price forecasts year-on-year.

Around 42% of JLEN’s assets at the end of September 2023 fell completely outside of the levy. The managers say that this is a strength of having a diversified portfolio that has a combination of assets that generate electricity (and fall in the scope of the levy), assets that generate gas (the anaerobic digestion plants), and assets that do not generate energy at all (batteries, CNG refuelling stations, and the controlled environment assets).

Leave a Reply