May 20, 2026

Rida Morwa

Investing Group Lead

Follow Seeking Alpha on Google for the latest stock news

Summary

- Stop trying to gamble on prices. Treat your portfolio like a cash-producing business instead.

- Dividend cash flow provides a tangible, calming metric that prevents panic selling during violent market drawdowns.

- Never Forced to Sell: High-yield dividends generate constant liquidity, meaning you dictate the terms of your portfolio, not your monthly bills.

- You don’t need a massive lump sum subjected to daily market whiplash; you need a permanent, recurring paycheck.

- Looking for a helping hand in the market? Members of High Dividend Opportunities get exclusive ideas and guidance to navigate any climate.

Co-authored with Beyond Saving

You are preparing for retirement, or maybe you have recently retired, and you have decided that you want to manage your own investments.

Congratulations! You have already taken two steps that a very large number of people never take: you saved up capital, and you took charge of it. Too many people just go through life crossing their fingers and hoping everything will work out.

Now what?

Every day, I talk to investors who treat the stock market like a lottery ticket. They scour the market looking to make quick trades, hoping that they can buy something that will become popular and then sell it before it becomes unpopular. There are several strategies that attempt to achieve this. Some focus on technical trading signals that attempt to be ahead of the popularity curve. Others focus on trying to predict news cycles, trading in and out of sectors as their popularity increases or decreases based on what’s happening in the news cycle. Others will buy ideas that they think might become the next big thing, hoping to find the next NVIDIA Corporation (NVDA) to offset the fizzles like Beyond Meat, Inc. (BYND). All of these strategies revolve around the idea of buying a stock to sell it at some point in the future, hopefully at a higher price.

There are many ways to make money investing in the stock market, and I encourage you to find a strategy that works for you. Our strategy is different from all of those above. Our strategy isn’t to buy things because we believe we will find some sucker willing to pay a price higher than we would be willing to pay. Our strategy isn’t to spend our later years selling off the shares we worked so hard to accumulate.

We are income investors. Our strategy is to turn our portfolios into a cash-producing business. A business that produces enough cash to meet our needs in retirement and retain enough to reinvest for future growth. Today, let’s address the top three reasons why we are income investors.

Reason 1: Emotional Control

The stock market is a volatile place. While we’ve been in an extended bull market where the market is green more often than not, I am old enough to remember the arrogant swagger of the dot-com bubble. Investors felt invincible; they were up so much, and everything they invested in was making so much money.

I remember going into the Great Financial Crisis; smart people were frequently saying things like, “Buy real estate, it only goes up!” People who had no construction or real estate experience at all were getting into flipping houses. Investors were piling into mortgages and mortgage derivatives.

Then the bubbles popped, the stock markets collapsed, and the people who were so sure of themselves the previous year panicked. Sure, it’s easy to say, “Don’t panic,” and that is fantastic advice. Yet, the reality is that for all of us, that big number in our brokerage account represents something that is “a lot” of money to us. When “a lot” becomes a lot less, panic is a natural reaction.

Intellectually, we can know that market sell-offs happen and that the market has always recovered in the past, and it will probably recover this time too. Yet, the very fact that sell-offs happen is proof that people sell when they get scared.

Focusing on the cash flow that your portfolio produces gives you a tangible metric that measures the underlying performance of the companies you invest in, not the emotional sentiment driving prices. When the market is falling around you, I have found that focusing on the income my portfolio is capable of producing provides a framework for working through decisions in an emotionally charged time. Instead of reacting emotionally, it gives me tangible numbers to work with and navigate stressful situations.

Reason 2: Never Be Forced To Sell

Most of us are investing for retirement, which means that we intend to withdraw money from our portfolios to pay for things while we are retired.

Many investors have the idea that they will save up $X and then, during their retirement years, withdraw a certain amount. Those withdrawals will be funded by selling shares. Which is great—if share prices go up.

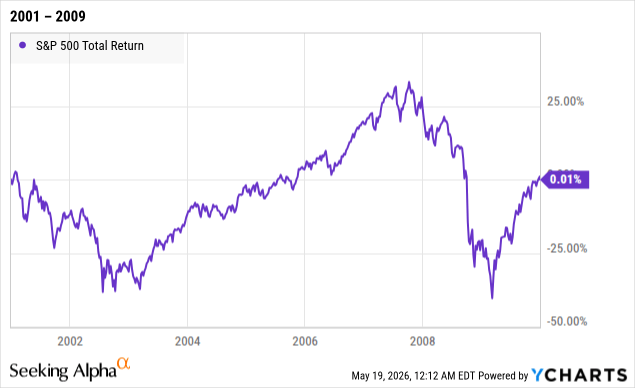

However, the reality is that shares don’t always go up. They can go down, and they can stay down for a very long time. For example, from January 2001 to January 2010, the S&P 500 had a total return of 0.01%:

That is the total return with $0 withdrawn. On a $1 million portfolio, you had a gain of approximately $100. Maybe you can sell shares for more than you paid, but maybe you can’t. That is an uncertainty that all retirees have to deal with because you don’t know if you are retiring in 2001 or 2010.

Many investors have come to expect the short-term drawdowns we experienced with COVID-19 or in 2022. Those are relatively easy because it is reasonable to wait for 6-12 months to liquidate shares. When you’re 70 or 80 years old, waiting for 10 years so you can sell stock at a higher price might not be practical.

By having a portfolio that is producing income, you have a constant cash flow in your portfolio, whether prices are high or low. You get to choose how much of that cash flow to withdraw, how much to reinvest, and how much to hold in cash. When your cash flow is high enough to meet your liquidity needs, you are never forced to sell a share. Certainly, you will sometimes decide to sell shares because the market is offering you a great price, or maybe you decide the investment is no longer an attractive risk. But the key is that the decision is yours to sell because you believe it will improve your portfolio, rather than selling because you have to pay bills.

Reason 3: Building A Perpetual Income Machine

When I started investing for income, my goals were quite modest. How cool would it be if I had an income stream that was enough to pay my water bill every month? I’d never have to pay a water bill again because my portfolio would generate enough cash flow to cover that bill. After that, it became about paying the internet bill, then the electric bill, and the goal kept moving higher until the income from my investment portfolio exceeded all of my bills.

Warning: Income investing may be addictive!

As part of the Income Method, we recommend planning on reinvesting a minimum of 25% of your income. This provides two benefits. First, it creates a built-in cushion to absorb dividend cuts and fluctuations from investments that pay variable dividends. Dividends aren’t guaranteed, and even bonds default sometimes, so it is prudent to build in a cushion so that when things happen, it doesn’t negatively impact your ability to withdraw what you need.

Second, it means that your portfolio is constantly reinvesting. You are always a net buyer, and those new shares that you are buying pay more dividends. Every month, you own more shares and are collecting more dividends than the month before. Over time, the power of compounding works its magic on your cash flow. Your income continues to grow, even if you aren’t adding any new capital to the portfolio.

That is the ultimate goal, where the cash flow your portfolio is producing is growing on its own, even as you withdraw a portion of it to fund your needs and wants. Where you don’t have to worry about outliving your portfolio because you aren’t selling it off. Your portfolio is providing the cash for you to invest more every month.

Conclusion

Look, there is no magic bullet when you’re investing. There is no “get rich quick” scheme that consistently works, and there are no guarantees. The Income Method isn’t about being “conservative”; it’s about being methodical. It’s about approaching your investing like a business that you are building from the ground up.

It’s about having a clear goal that is fixed, and you can clearly measure your progress. How much money do you need to retire? $1 million, $3 million? The answer greatly depends on when you retire because $1 million in 2001 is a lot less than $1 million in 2003. Stock prices change every day. How much income do you need to retire? Well, you know how much you make while you’re working, so that should give you an excellent handle on how much money you need every year to pay your bills and fund the retirement lifestyle you choose to live. That number doesn’t change, except for inflation. So, you can measure your progress clearly and know whether you are getting closer and whether you are on track. Saying “I need my portfolio to generate $80,000 in recurring cash flow” is much clearer than saying “I need a portfolio with a value of $1 million.”

When you retire, you don’t need a big lump sum of cash. Odds are that you are going to leave a substantial portion invested in the stock market, where the prices will change with the next news alert. What you need is the knowledge that you can withdraw the cash you require every single year for the rest of your life. When you retire, you are losing an income stream. So, replace your income stream with an income portfolio.

That is why I follow the Income Method.

Leave a Reply