How to become an Isa millionaire

As savings rates fall, and tax bills rise, it’s a key time to reassess your Isa strategy – doing it well could make you a millionaire.

At the last count, there were nearly 5,000 Isa millionaires in Britain, and the top 25 have pots averaging a whopping £11.3m.

But joining this exclusive club does not just happen overnight – it takes time and patience.

An Isa is an all-important tax shelter for your savings, where you will escape tax on dividends and capital gains tax on any profits when you sell, as well as income tax.

How much you invest, the investments you choose and their performance, are the main factors that will determine whether you can one day reach the £1m milestone.

Chancellor Rachel Reeves has confirmed reforms to cash Isas will be introduced in 2027 for savers under 65, but there is no suggestion (at the moment) that stocks and shares Isas are under threat.

If anything, the Government wants to encourage more small investors to put their money into the stock market, particularly into London-listed shares and infrastructure.

Here, Telegraph Money explains how to invest your way to £1m.

Could I become an Isa millionaire?

To get to £1m, investors will need to max out their Isa each year, and their investments must provide a certain level of returns.

Someone starting from scratch today putting the full £20,000 annual allowance into a high-risk stocks and shares Isa could expect to reach millionaires’ row in under 21 years, assuming 8pc annual return

If you’re more comfortable with lower-risk investments, investing at this same rate could still get you to £1m – but it would take around 35 years, assuming 2pc annual returns.

The average Isa millionaire has £1.35m, investment company Plum found. But the top 25 Isa investors are sitting on pots averaging £8.8m.

Lord John Lee became an Isa millionaire more than 20 years ago and has written for Telegraph Money sharing his insights.

Plum’s Rajan Lakhani said Isa millionaire wealth was continuing to grow “even as other savings and investment products lose a little of their shine due to rising complexity and lower interest rates.

“A large part of the Isa’s appeal is the flexibility and liquidity it offers investors. In simple terms, you can crystallise your wealth whenever you choose and regardless of age, unlike, for example, pension holdings or buy-to-let properties.”

It’s not just a feat for the elderly, either – at brokers AJ Bell, the youngest Isa millionaire is just 33 – and the oldest is 100

How to become an Isa millionaire in four simple steps

There are four key habits that will help you become an Isa millionaire:

- Maximise your contributions

- Diversified investments

- Regular portfolio reviews

- Commitment to investing over the long-term

1. Maximise your contributions

To get to £1m as quickly as possible, the first step is to invest the maximum each year.

It is arguably easier to become an Isa millionaire today, with a £20,000 a year Isa allowance for savers (assuming you can afford to put away the maximum), compared to older investors who started out when Isas launched in 1999 with a £7,000 limit.

If you started saving today and the Isa limit remained at £20,000, it would take you 25 years to become an Isa millionaire, assuming an average annual return of 5pc.

The next key part of your strategy could be to invest early in the tax year. It means you will have up to an additional year invested, which will also help power portfolios in a rising market, as more of your assets are invested for longer.

When it comes to selecting investments you’ll need a diverse, balanced mix according to your risk appetite. Buying individual shares can produce outstanding returns, but you are very exposed to a small number of companies (read on to discover the most popular shares held by Isa millionaires this year).

The alternative is investing in funds, either actively managed or “passive” where an algorithm mirrors a given index or industry. You might also wish to consider listed funds, also called investment trusts, which have been a good bet over the years.

At Interactive Investor, Britain’s second largest stockbroker, equities are the most popular type of holding among millionaires, accounting for 39pc of portfolios. Investment trusts come in a close second, at 34pc.

A total of 50 investment trusts would have made investors more than £1m if they had invested the full annual Isa allowance in the same company each year to 2024, according to research from the Association of Investment Companies, a trade body.

Investing the full Isa allowance each year from 1999 to 2024 – a total of £326,560 – and reinvesting the dividends into one of the four investment companies below would have generated a tax-free pot of over £2m at the end of January 2025.

These top four performing funds are: Allianz Technology Trust, HgCapital Trust, Polar Capital Technology and Scottish Mortgage. Among the common investment themes in these listed funds are technology and smaller companies.

While these figures are compelling, it is not advised to have all your money in one investment or one investment type.

The average Isa millionaire portfolio includes 23 holdings, according to AJ Bell.

3. Regular portfolio reviews

While choosing long-term investments is often a good strategy, it is still advisable to periodically assess and adjust your investment choices. As you approach retirement, your appetite for risk may decline.

Laura Suter, head of personal finance at AJ Bell, said: “Most Isa millionaires are in their 60s and 70s, illustrating the crucial impact of compound returns over the long-term. Nonetheless, nearly a fifth of Isa millionaires have hit the milestone before their 60th birthday.

“Astonishingly, a handful of extremely successful Isa investors in their 40s have racked up portfolios worth over £3m. Although it’s worth pointing out those with a sizeable portfolio at such a young age often tend to pursue a high conviction strategy focused on specific stocks, which won’t be for everyone.”

Ms Suter warned there was “no guaranteed recipe for success”.

“Some investors invest in highly diversified portfolios, while others have just a handful of positions. And while shares and trusts are especially popular among millionaires, there are plenty using funds too. The important thing is to invest in what you feel comfortable with and understand the level of risk you are taking in return for the potential reward.”

4. Commitment to investing over the long term

Investing over a long period is a tried and tested strategy.

The sooner you start saving the more you can put aside, and early contributions are the most valuable because they have the longest to grow.

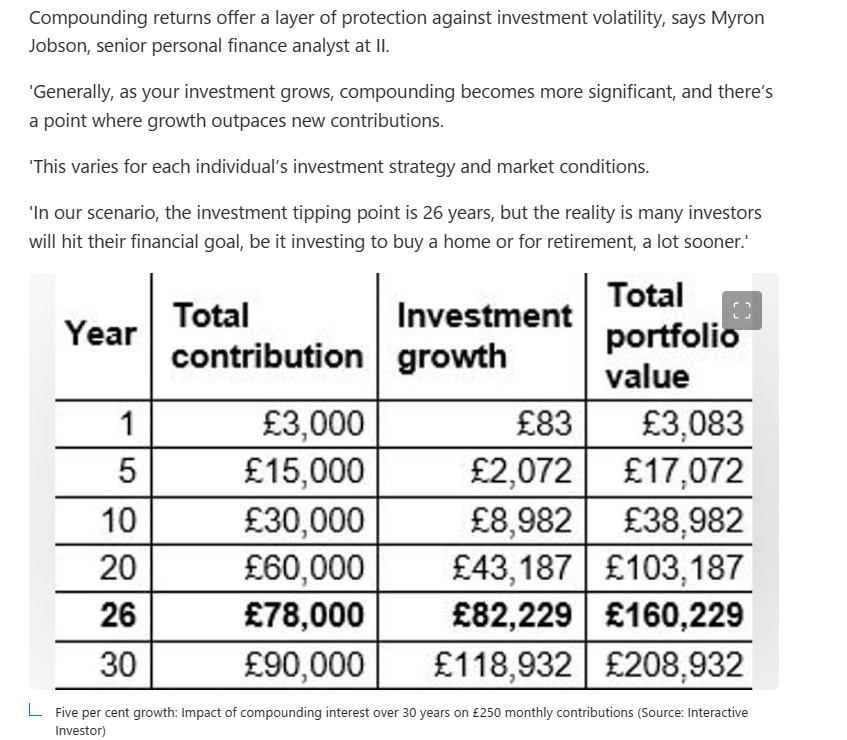

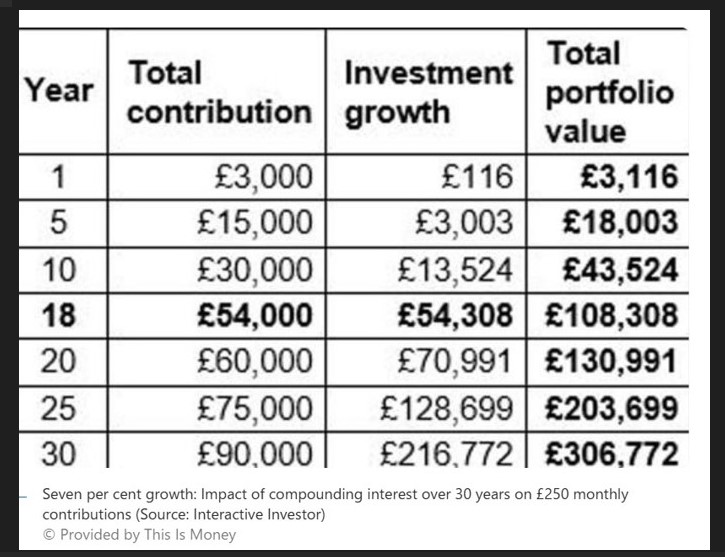

Compounding will also boost returns. In simple terms, your money earns a return in the first year and both the original cash and the return benefit from any growth in the second year. In the third year your investment is further enhanced by any returns achieved. This snowball effect is known as compounding.

Experts insist that getting rich slowly is a smart strategy.

Sarah Coles, head of personal finance at Hargreaves Lansdown, says: “Isa investors don’t take enormous risks.

“Their focus is to consistently invest as much as possible of their annual allowance, as early as possible in the tax year, in a diverse and balanced portfolio. And they’ve done this every year for decades.”

What does an Isa millionaire’s portfolio look like?

Listed investment funds have powered Isa millionaire portfolios at Interactive Investor, and account for the largest share of Isa portfolios.

Alliance Witan and Scottish Mortgage are the two most common investment trust stocks found in the average Isa millionaire top 10 holdings.

Investment trusts, the oldest form of collective investment in the UK, have several advantages over unlisted funds, according to advocates. One of these is their ability to hold back some of the income they receive from their underlying investments in good years to pay out to investors when times are tougher.

They can borrow money to invest extra than that provided by their investors to boost performance in an upturn. Many also have great track records for paying dividends. The downside is they can be expensive to trade, with many brokers charging flat fees for the purchase of shares, while units in unlisted funds can be purchased for a negligible fee.

Many investors have had success from unlisted funds, however. Popular funds include Rathbone Global Opportunities, Lindsell Train Global Equity, Fundsmith Equity and Fidelity Special Situations.

FTSE blue chips are widely held in Isa millionaire accounts. They include Shell and BP; Lloyds Banking Group and Aviva; GSK; and National Grid.

How to become an Isa millionaire in four simple steps

How to become an Isa millionaire in four simple steps

There is one passive fund in the top 10 at brokers Interactive Investor. These funds use computer algorithms to automatically track an index such as the FTSE 100. A common thread here is being – almost – fully invested.

Camilla Esmund, senior manager at Interactive Investor, said: “The not-so-secret sauce of Interactive Investor’s Isa millionaires is staying invested and being diversified – the latter involves spreading money across different asset classes, sectors, and geographies.

“Their success requires time, patience, and benefiting from the magic of compounding. Plus, our Isa millionaires are savvy to the fees they are paying, making sure they aren’t paying a percentage fee that risks eating into their growing pots.”

Best stocks and shares Isa providers

This is one of the most common questions we get asked on the Telegraph Money desk.

The truth is that the best stockbroker, fund supermarket or “platform” to hold your Isa investments depends on several factors: how much money is in your Isa, what support you need, and the types of investment you plan to make.

You pay holding fees to your provider, which can be a percentage or a flat charge.

On top of this you will pay fund management charges, which will vary greatly – you can find this information on the fund’s factsheet.

While a percentage charge can be cheaper for those with smaller holdings, it can quickly start eating into your returns as your portfolio grows. It’s a good idea to revisit your fees regularly and check whether you could get a better deal elsewhere.